Nội dung toàn văn Official Dispatch No. 943 TCT/TNCN, on Tax payment of foreign contractor

|

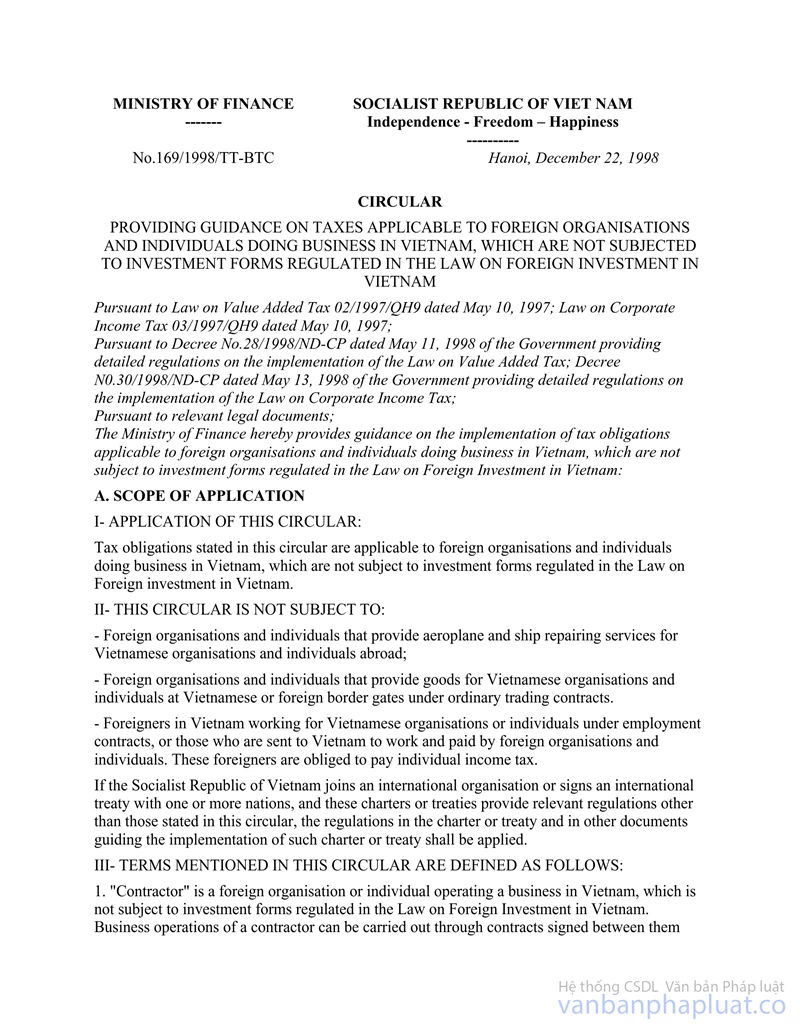

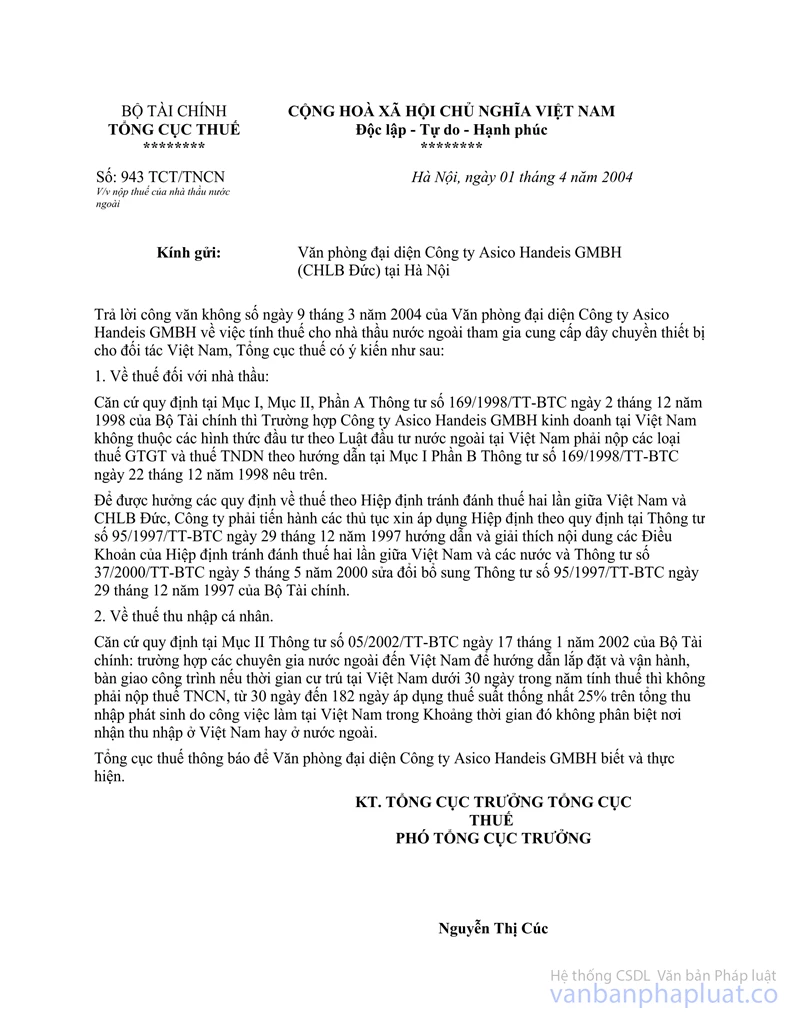

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No: 943 TCT/TNCN |

Hanoi, April 01, 2004 |

To: The Representative Office of the Asico Handeis GMBH Company (Germany) in Hanoi

In response to the official letter dated March 9, 2004 of the Representative Office of the Asico Handeis GMBH Company regarding the tax calculation for foreign contractor engaging in the supply of equipment line to Vietnamese partner, following are opinions of the General Department of Taxation:

1. Taxes for Foreign Contractors

Pursuant to provisions of Sections I and II of Part A of Circular No. 169/1998/TT-BTC dated December 22, 1998 of the Ministry of Finance, in case of doing business in Vietnam not in the forms of investment under the Law on Foreign Investment in Vietnam, the Asico Handeis GMBH Company shall pay Value Added Tax and Corporate Income Tax as guided in Section I of Part B of Circular No. 169/1998/TT-BTC dated December 22, 1998 stated above.

To benefit from the tax provisions in accordance with the Agreement on the Avoidance of Double Taxation between Vietnam and Federal Republic of Germany, the Company should fulfill the procedures for applying the agreement as set forth in Circular No. 95/1997/TT-BTC dated December 29, 1997 providing guidelines and interpretation of provisions of the Agreement on the Avoidance of Double Taxation entered into by Vietnam and other countries and Circular No. 37/2000/TT-BTC dated May 5, 2000 amending and supplementing Circular No. 95/1997/TT-BTC dated December 29, 1997 of the Ministry of Finance.

2. Personal Income Tax

Pursuant to Section II of Circular No. 05/2002/TT-BTC dated January 17, 2002 of the Ministry of Finance, a foreign expert, who enters into Vietnam for guiding the installation, operation and handover of construction works, (i) is not required to pay personal income tax if his/her length of stay in Vietnam is less than 30 days in a taxable year, and (ii) shall pay 25% of total income sourced in Vietnam regardless of where such income generated from Vietnam or abroad if his/her length of stay in Vietnam is 30 days to 182 days.

The General Department of Taxation hereby notifies the Representative Office of the Asico Handeis GMBH Company for implementation.

|

|

FOR THE GENERAL DIRECTOR |