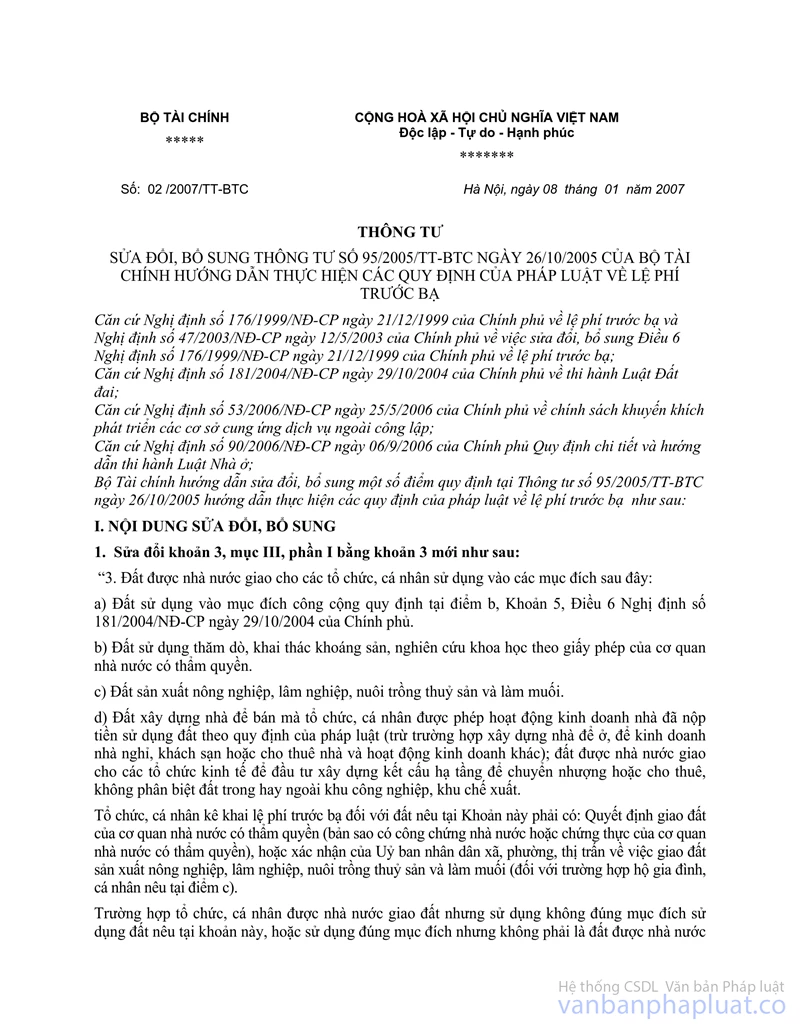

Circular No.02/2007/TT-BTC of January 08, 2007 amending and supplementing the finance ministrys Circular No. 95/2005/TT-BTC of October 26, 2005, guiding the implementation of the provisions of law on registration fees đã được thay thế bởi Circular No. 68/2010/TT-BTC guiding the registration và được áp dụng kể từ ngày 10/06/2010.

Nội dung toàn văn Circular No.02/2007/TT-BTC of January 08, 2007 amending and supplementing the finance ministrys Circular No. 95/2005/TT-BTC of October 26, 2005, guiding the implementation of the provisions of law on registration fees

|

THE MINISTRY OF FINANCE |

OF VIET |

|

No. 02/2007/TT-BTC |

, January 08, 2007 |

CIRCULAR

AMENDING AND SUPPLEMENTING THE FINANCE MINISTRY’S CIRCULAR No. 95/2005/TT-BTC OF OCTOBER 26, 2005, GUIDING THE IMPLEMENTATION OF THE PROVISIONS OF LAW ON REGISTRATION FEES

Pursuant to the Government’s Decree No. 176/1999/ND-CP of December 21,

1999, on registration fees and Decree No. 47/2003/ND-CP of May 12, 2003,

amending and supplementing Article 6 of the Government’s Decree No.

176/1999/ND-CP of December 21, 1999, on registration fees;

Pursuant to the Government’s Decree No. 181/2004/ND-CP of October 29, 2004, on

the implementation of the Land Law;

Pursuant to the Government’s Decree No. 53/2006/ND-CP of May 25, 2006, on

policies to encourage the development of non-public service establishments;

Pursuant to the Government’s Decree No. 90/2006/ND-CP of September 6, 2006,

detailing and guiding the implementation of the Housing Law;

The Finance Ministry hereby guides amendments and supplements to a number of

provisions of Circular No. 95/2005/TT-BTC of October 26, 2005, guiding the

implementation of law on registration fees as follows:

I. CONTENTS OF AMENDMENTS AND SUPPLEMENTS

1. To amend Clause 3, Section III, Part I into the following new one:

“3. Land assigned by the State to organizations and individuals for use for the following purposes:

a/ The public purposes defined at Point b, Clause 5, Article 6 of the Government’s Decree No. 181/2004/ND-CP of October 29, 2004;

b/ Mineral exploration and exploitation or scientific research under permits granted by competent state agencies;

c/ Agricultural or forestry production, aquaculture or salt-making;

d/ Construction of houses for sale, for which the organizations or individuals licensed to conduct housing business have paid land use levies in accordance with law (except for cases of building houses for residence, for inn business, hotel business, for lease or other business activities); investment in the construction of infrastructure for transfer or lease, with regard to land assigned by the State to economic organizations, regardless of whether that land is inside or outside industrial parks or export processing zones.

Organizations or individuals making registration fee declaration for land defined in this Clause are required to obtain land assignment decisions of competent state agencies (copies notarized by state public notaries or authenticated by competent state agencies), or written certifications of commune/ward/township People’s Committees of the assignment of land for agricultural or forestry production, aquaculture or salt making (for households and individuals mentioned at Point c).

When organizations or individuals are assigned land by the State but use that land for purposes other than those mentioned in this Clause or when they use land for proper purposes but that land is not assigned by the State (such as transferred, exchanged or reclaimed land...) they shall pay registration fees before they are granted land use right certificates.”

2. To amend Clause 4, Section III, Part I into the following new one:

“4. Land rented from the State, organizations or individuals with lawful land use rights.”

3. To add Clause 8a to before Clause 9, Section III, Part I as follows:

“Houses of families or individuals created through the development of separate houses under the provisions of Point b, Clause 2, Article 50 of the Government’s Decree No. 90/2006/ND-CP of September 6, 2006, detailing and guiding the implementation of the Housing Law;

The development of separate houses of households or individuals shall comply with the provisions of Article 41 of the 2005 Housing Law, specifically:

1. Development of separate houses means that households or individuals invest by themselves in the construction of houses in the land premises under their use rights.

2. Construction of separate houses of households or individuals takes in one of the following forms:

a/ Self-construction of houses;

b/ Hiring other organizations or individuals to build houses;

c/ Cooperating with and assisting one another in house construction in rural areas.”

4. To amend the first paragraph of Point b, Clause 9, Section III, Part I as follows:

“b/ Assets under the ownership or use rights of enterprises (state enterprises or other enterprises) which have been equitized into joint stock companies. Houses and land under the management of state enterprises but without house ownership or land use right certificates, if equitized into assets of joint stock companies which register their ownership or use rights over those assets, are also not liable to registration fee.

When the joint stock companies do not register their ownership or use rights over those assets but transfer them to other organizations or individuals for ownership or use right registration, the transferees shall pay registration fees.”

5. To add to the end of the fourth em rule, Point d, Clause 10, Section III, Part I the following:

“When the property owner no longer retains or has lost the registration fee payment voucher, he/she shall request the tax office which has collected the registration fee to check the dossier and certify (the tax office’s head shall write his/her signature and full name and append a seal for certification) the collection of the registration fee or the fact that the moved property is not liable to registration fee. Upon receiving the property owner’s request for certification, the local tax office which has collected the registration fee for the moved property shall, within 3 (three) working days, check the dossier in archives in order to certify that the registration fee has been paid, has not been paid or needs not be paid for the property. If detecting that the property owner has not paid a registration fee, the tax office shall collect it and impose a fine on that owner in accordance with current regulations.

When a property has been granted an ownership or use right certificate but the retroactive time limit for registration fee payment defined in Clause 3, Article 11 of the Government’s Decree No. 176/1999/ND-CP of December 21, 1999, on registration fees (below called Decree No. 176/1999/ND-CP for short) has expired, the property owner needs not present the registration fee payment voucher or the tax office’s written certification that he/she has paid or is not liable to registration fee.”

6. To add Clause 15 to Section III, Part I as follows:

“15. Houses and land under the management or lawful use rights of non-public establishments which register their rights to own houses or to use land for education and training; medical; cultural; physical training and sports; scientific and technological; environmental; population, family or child protection and care purposes under the Government’s Decree No. 53/2006/ND-CP of May 25, 2006, on policies to encourage the development of non-public service establishments. When enterprises operating under the Enterprise Law use houses or land for those purposes, or non-public establishments register house ownership or land use rights but do not actually use such houses or land for those purposes, they shall pay or retrospectively pay registration fees under regulations.”

7. To amend Point d, Clause 1 (1.2), Section I, Part II into the following new one:

“d/ For land transferred from organizations or individuals (business or non-business), the registration fee calculation price is the actual transfer price written in the invoice, transfer contract, sale and purchase document or registration fee declaration form, which, however, must not be lower than the land price set by the provincial People’s Committee and applied at the time of registration.”

8. To amend Point e, Clause 1 (1.2), Section I, Part II into the following new one:

“e/ When a land user has been granted a land use right certificate, then permitted by a competent agency to use the land for another purpose and at the time of making registration fee declaration, the land price set by the provincial People’s Committee for the new use purpose is higher than that set for the original use purpose stated in the land use right certificate (with a positive difference), that land user shall pay a registration fee calculated on the difference value; if the land price set for the new use purpose is lower than that set for the original use purpose (with a negative difference), the land user is neither liable to pay a registration fee nor refunded the paid registration fee amount.

When a land user has been granted a land use right certificate without having to pay a registration fee, then permitted by a competent agency to use the land for another purpose for which the land is liable to registration fee, the land user shall pay such registration fee based on the land price set for the new use purpose by the provincial People’s Committee.”

9. To annul Point f, Clause 1 (1.2), Section I, Part II.

10. To amend Point 2.3, Clause 2, Section I, Part II into the following new one:

“2.3. The ratio (%) of the residual quality of the house liable to registration fee is determined as follows:

a/ First-time registration fee declaration: 100%;

b/ Registration fee declaration for the second time on:

|

Use period |

Grade-I houses (%) |

Grade-II houses (%) |

Grade-III houses (%) |

Grade-IV houses (including villas) (%) |

|

- Under 5 years |

95 |

90 |

90 |

80 |

|

- Between 5 and 10 years |

90 |

85 |

80 |

65 |

|

- Between over 10 and 20 years |

80 |

70 |

60 |

40 |

|

- Between over 20 years and 50 years |

60 |

50 |

40 |

40 |

|

- Over 50 years |

40 |

40 |

40 |

40 |

The use period of a house is counted from the time (year) the construction is completed and the house is handed over (or put to use) to the year of declaration and payment of registration fee for that house. When the dossier lacks grounds for determination of the house construction year, the year of purchase or receipt of the house is used instead.

11. To amend Point b, Clause 3 (3.6), Section I, Part II into the following new one:

“b/ The ratio (%) of the residual quality of a registered property is specified as follows:

* First-time registration fee declaration in :

- New property: 100%

- Used property imported into : 85%.

* Registration fee declaration from the second time on in :

- The use period of under 3 years: 85%.

- The use period of between 3 and 6 years: 75%.

- The use period of between over 6 and 10 years: 60%.

- The use period of over 10 years: 40%.

* The use period of a property is determined as follows:

- For property manufactured in , its use period is counted from the time of its manufacture to the year of declaration of registration fee;

- For imported brand-new property, its use duration is counted from the time of its import to the year of declaration of registration fee. When the time of import of the property is unidentifiable, the time of its manufacture is used instead;

- For imported used property, for which the registration fee declaration is made for the second time on, its use period is counted from the time of its manufacture to the year of declaration of registration fee and the value of the property used for determination of the registration fee calculation price is the price of a corresponding brand-new property set by the provincial People’s Committee. When the time of manufacture of the property is unidentifiable, the property’s use period is counted from the time of its import and the value of the property used for determination of the registration fee calculation price is the price of a corresponding used property (85%).

II. ORGANIZATION OF IMPLEMENTATION

This Circular takes effect 15 days after its publication in “CONG BAO.” The provisions of the Finance Ministry’s Circular No. 95/2005/TT-BTC of October 26, 2005, which are not amended or supplemented in this Circular remain effective.

Organizations and individuals are requested to report all problems arising in the course of implementation to the Finance Ministry for study and additional guidance.

|

|

FOR THE FINANCE MINISTER |