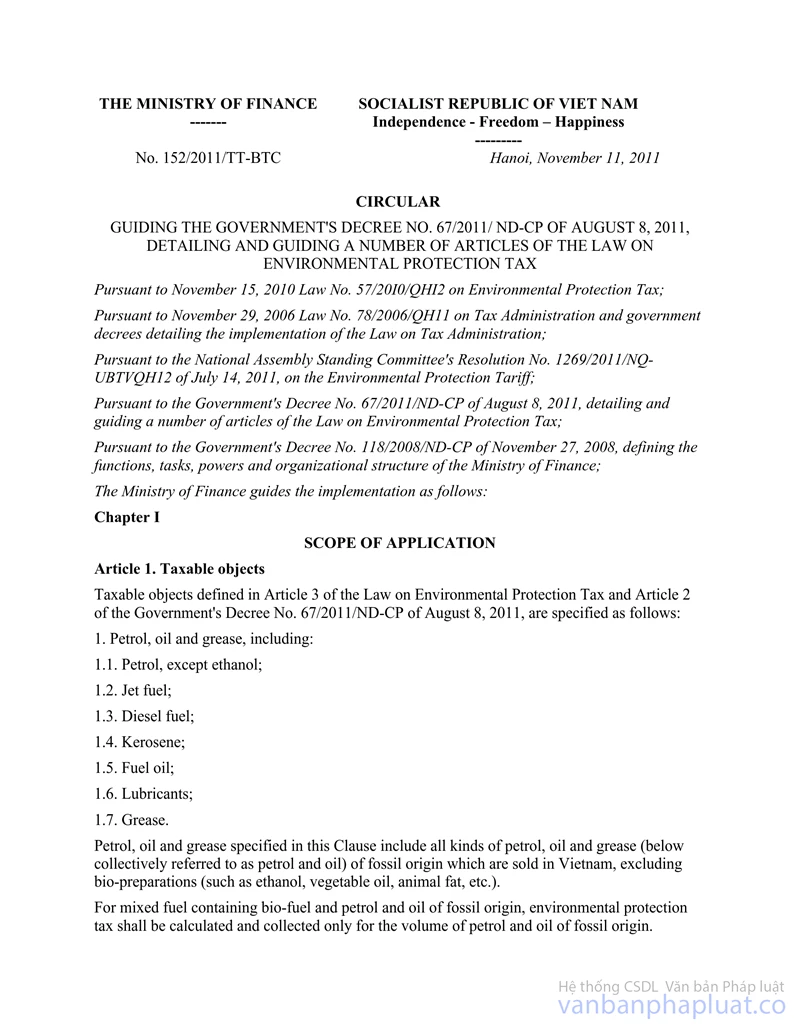

Circular No.06/2001/TT-BTC, promulgated by the Ministry of Finance, proguiding the implementation of the Government's Decree No.78/2000/ND-CP of December 26, 2000 on petrol and oil charges. đã được thay thế bởi Circular No. 152/2011/TT-BTC guiding the Government's Decree No. 67/2011/ ND-CP và được áp dụng kể từ ngày 01/01/2012.

Nội dung toàn văn Circular No.06/2001/TT-BTC, promulgated by the Ministry of Finance, proguiding the implementation of the Government's Decree No.78/2000/ND-CP of December 26, 2000 on petrol and oil charges.

|

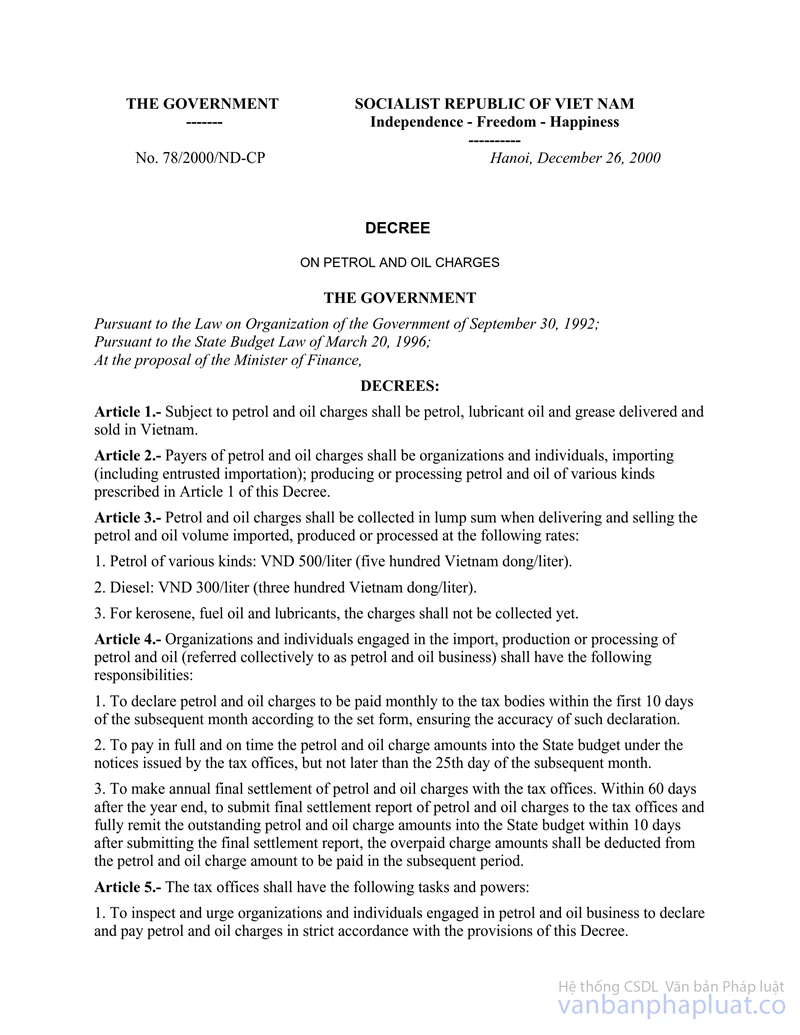

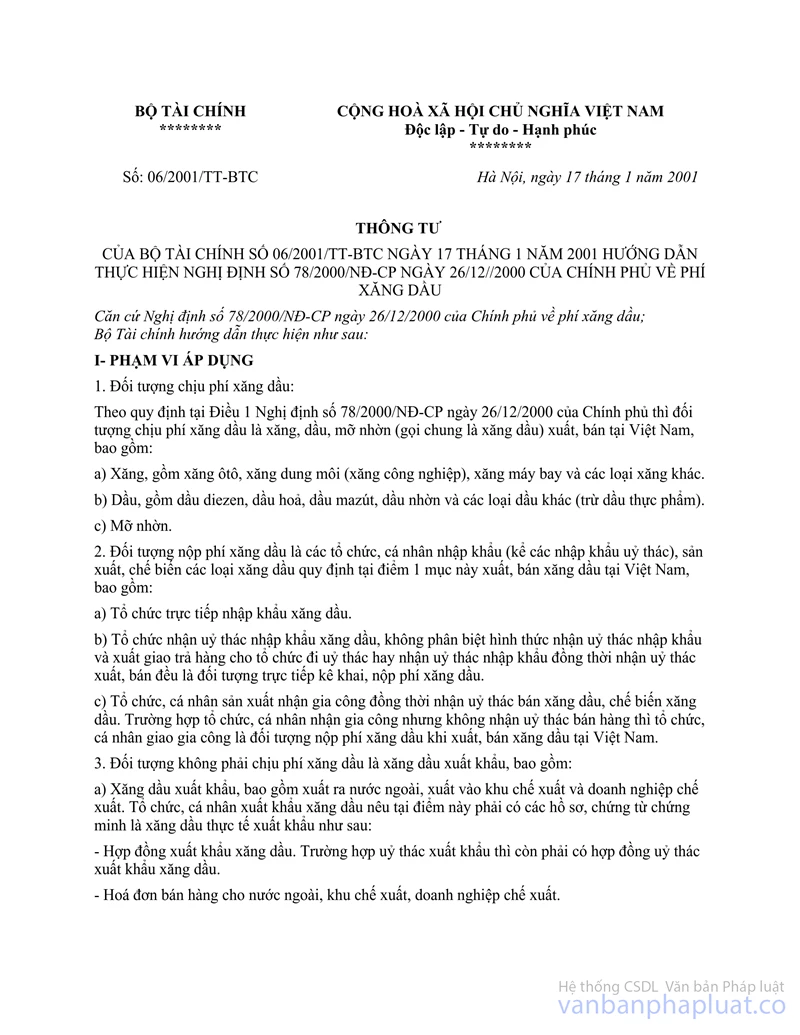

THE

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No: 06/2001/TT-BTC |

Hanoi, January 17, 2001 |

CIRCULAR

GUIDING THE IMPLEMENTATION OF THE GOVERNMENT’S DECREE NO. 78/2000/ND-CP OF DECEMBER 26, 2000 ON PETROL AND OIL CHARGES

Pursuant to the Governments Decree No.

78/2000/ND-CP of December 26, 2000 on petrol and oil charges

The Ministry of Finance guides the implementation thereof as follows:

I. SCOPE OF APPLICATION

1. Objects liable to petrol and oil charges:

According to Article 1 of the Governments Decree No. 78/2000/ND-CP of December 26, 2000, objects liable to petrol and oil charges are petrol, oil and grease (called collectively petrol and oil), delivered and/or sold in Vietnam. They include:

a/ Petrol, including car petrol, solvent petrol (industrial petrol), aircraft petrol and other kinds of petrol.

b/ Oil, including diesel oil, kerosene, fuel oil, lubricants and other kinds of oil (except vegetable oil).

c/ Grease.

2. Payers of petrol and oil charges are organizations and individuals that import (including those undertaking entrusted import), produce and/or process petrol and oil of those kinds specified at Point 1 of this Section and deliver and/or sell them in Vietnam, including:

a/ Organizations directly importing petrol and oil.

b/ Organizations undertaking the entrusted import of petrol and oil, regardless of whether they undertake the entrusted import of petrol and/or oil and deliver them back to the entrusting organizations or undertake both the entrusted import and the entrusted delivery and/or sale thereof, shall all have to declare and pay petrol and oil charges.

c/ Organizations and individuals producing, undertaking both the processing and the entrusted sale of, or processing petrol and oil. Where organizations and/or individuals undertake the processing but not the entrusted sale of petrol and oil, the processees, being either organizations or individuals shall have to pay petrol and oil charges when delivering and/or selling petrol and oil in Vietnam.

3. Export petrol and oil shall not be subject to petrol and oil charges, including:

a/ Export petrol and oil, which are exported either abroad or into export-processing zones or to export-processing enterprises. Organizations and individuals exporting petrol and oil specified at this Point must have the following documents and vouchers proving that petrol and oil have been actually exported:

- The petrol and oil export contracts. For cases of entrusted export, the contracts for entrusted petrol and oil export are also required.

- The invoices for the sale of petrol and oil to foreign countries, export-processing zones or export-processing enterprises.

- The export customs declaration forms, with the volumes and kinds of actually exported goods liquidated and certified by the customs offices.

b/ Temporarily imported petrol and oil for re-export; temporarily exported petrol and oil for re-import. Organizations and individuals dealing in petrol and oil in the forms specified at this Point must have the following documents and vouchers:

- The export or import quotas, granted by the Ministry of Trade (or the authorized body), clearly stating that the goods are temporarily imported for re-export or temporarily exported for re-import.

- The export and import goods customs declaration forms, with the volumes and kinds of the actually exported and imported goods liquidated and certified by the customs offices.

- The foreign trade contracts signed with the purchasers and the sellers.

For cases of entrusted export and import, the entrusted import and export contracts are also required (for goods exported and imported by entrustment). In this case, if selling petrol and oil in Vietnam, organizations and individuals shall have to register with, declare and pay petrol and oil charges to, the provincial/municipal Tax Departments of the localities where they are headquartered.

II. CHARGE RATES AND BASES FOR COLLECTION OF PETROL AND OIL CHARGES

1. Petrol and oil charges shall be collected in lump sum upon the delivery or sale of the imported volumes of petrol and oil (including volumes of petrol and oil imported by entrustment), the production and processing (including volumes of petrol and oil delivered for internal consumption, delivered for exchange for other products and goods, delivered back to the goods import entrustors, sold to other organizations and individuals), at the rates prescribed below:

a/ Assorted petrol, including car petrol, aircraft petrol, industrial petrol and petrol of other kinds: VND 500/liters (five hundred dong/liter).

b/ Diesel oil: VND 300/liters (three hundred dong/liter).

c/ Kerosene, fuel oil, lubricants, grease and oil of other kinds (except petrol and diesel oil specified at Items a and b of this Point): Charges shall not be collected yet.

2. Bases for collection of petrol and oil charges include the volumes of petrol and oil delivered and/or sold in Vietnam and the charge rates, calculated according to the following formula:

Petrol The volume of petrol The charge

or oil = or oil delivered and/or x rate

charge sold in Vietnam (dong/liter)

Where the volumes of petrol and oil delivered and/or sold are calculated in other measurement units, they must be converted into liter.

III. ORGANIZATION OF THE COLLECTION AND PAYMENT OF PETROL AND OIL CHARGES

1. Organizations and individuals liable to pay petrol and oil charges as specified at Point 2, Section I of this Circular (collectively called the charge payers) shall have to:

a/ Register, declare the petrol and oil charges payable into the State budget with the Tax Departments of the provinces or centrally-run cities where they are headquartered.

b/ When delivering or selling petrol and oil:

- Calculate the petrol and oil charges at the rates specified at Point 1, Section II of this Circular.

- Issue the petrol and oil sale invoices to the purchasers.

In order to keep consumers not liable to VAT on the petrol and oil charges and avoid upset in their cost-accounting work, when writing the petrol and oil sale invoices (both wholesale and retail), the petrol and oil trading units must inscribe the petrol and oil charges on a separate line of such invoices; specifically, on the total lines of such invoices, the sans-VAT sale prices (exclusive of petrol and oil charges), the VAT, the petrol and oil charges and the payment prices must be clearly inscribed.

- Pay the petrol and oil charges and settle the proceeds from the sale of petrol and oil at the same time.

- Open accounting books to separately monitor and update the arising petrol and oil charges for settlement with the State budget. For petrol and oil trading units that do not directly declare and pay petrol and oil charges, the collected petrol and oil charges shall not constitute a turnover of petrol and oil trading activities and thus must not be accounted into the trading units’ turnover.

c/ Once every 15 days, the units shall base themselves on the petrol and oil volumes actually delivered and/or sold in the period (delivered for internal use; delivered for exchange for other products and goods; delivered back to the goods import entrustor; sold to other organizations, individuals, regardless of whether or not the payment therefor has been collected) to calculate and temporarily pay petrol and oil charges into the State budget.

Once a month, the units shall base themselves on the petrol and oil volumes delivered and sold in the month to calculate and make petrol and oil charge declarations according to set form and send them to the tax offices of the localities where they are headquartered within the first 10 days of the subsequent month. The tax offices shall check them and notify the units of the remaining petrol and oil charge amounts to be paid and the deadline for payment thereof into the State budget. Basing themselves on the tax offices� notices, the units shall carry out the procedures for paying the petrol and oil charges fully and on time into the State Treasury not later than the 25th of the subsequent month.

The petrol and oil charges paid into the State Treasury shall be accounted into the relevant chapter and clause, item and sub-item No. 032.01 of the current State budget content and transferred wholly into the central budget.

d/ Settle the amount of petrol and oil charges payable annually with the tax offices and submit, within 60 days after the end of the year, the petrol and oil charge settlement reports to the tax offices and pay fully the outstanding petrol and oil charges into the State budget within 10 days after the date of submission of the settlement reports; if the petrol and oil charges have been paid in excess, the excessive amount may be deducted from the amount of petrol and oil charges payable in the subsequent period.

2. The provincial/municipal Tax Departments of the localities where the petrol and oil charge payers are headquartered shall have to:

a/ Supervise, urge and guide organizations and individuals being payers of petrol and oil charges to pay such charges under the guidance of this Circular, ensuring that no charge payers and objects are omitted.

b/ Regularly coordinate with the customs offices and the managing bodies of the petrol and oil-producing, processing and/or trading units in the localities so as to know promptly the petrol and oil volumes imported, produced and/or processed by each unit, compare them with the actually-delivered and sold volumes, the volumes still left in stock and the waste volumes of petrol and oil (not exceeding the waste norms prescribed by the State) for calculation and collection of petrol and oil charges close to the arising volumes, thus avoiding loss to the State budget.

c/ Check the petrol and oil charge collection and payment declarations, calculate and notify the petrol and oil trading organizations and individuals of the monthly amount of petrol and oil charges payable into the State budget according to regulations. Regularly urge the units to pay petrol and oil charges fully and on time. Settle the annual payable petrol and oil charges with the petrol and oil charge payers according to the prescribed regime.

Where signs of breaching the petrol and oil charge management regulations by charge payers are detected and it is necessary to inspect and supervise the situation of the petrol and oil charge payment under decisions of competent bodies, the tax offices may request the petrol and oil charge payers to supply their accounting books, vouchers, dossiers and documents related to the petrol and oil charge calculation and payment in order to ensure the accurate and full calculation of petrol and oil charges payable into the State budget.

d/ Handle petrol and oil charge-related administrative violations according to their competence prescribed in Article 21 of the Governments Decree No. 04/1999/ND-CP of January 30, 1999 on charges and fees belonging to the State budget and guided at Point 6, Section V of the Finance Ministrys Circular No. 54/1999/TT-BTC of May 10, 1999 guiding the implementation of the said Decree.

3. Organizations and individuals that buy petrol and oil from units which have calculated and inscribed the petrol and oil charges on the sale invoices may account such petrol and oil charges into the costs and circulation fees for determining the reasonable expenses when calculating their incomes subject to enterprise income tax (for organizations and individuals engaged in business activities) or for determining reasonable expenses when settling the State budget funding (for administrative and public-service activities funded with the State budget allocations).

4. If organizations and individuals being payers of petrol and oil charges violate the provisions of the Governments Decree No. 78/2000/ND-CP of December 26, 2000 and the guidance in this Circular, they shall be sanctioned according to the provisions of Articles 18 and 20 of the Governments Decree No. 04/1999/ND-CP of January 30, 1999 and under the guidance at Points 3 and 5, Section V of the Finance Ministrys Circular No. 54/1999/TT-BTC of May 10, 1999.

IV. ORGANIZATION OF IMPLEMENTATION

1. This Circular takes effect as from January 1, 2001. To annul all documents guiding the Governments Decree No. 186/CP of December 7, 1994 on the collection of traffic fees through the petrol and oil prices.

2. Organizations and individuals that import, produce and/or process petrol and oil shall have to declare and pay petrol and oil charges according to the provisions of this Circular to the tax offices of the localities where they are headquartered for the volumes actually delivered and sold to other organizations and individuals as from January 1, 2001.

|

|

FOR THE

MINISTER OF FINANCE |