Nội dung toàn văn Circular No. 152/2011/TT-BTC guiding the Government's Decree No. 67/2011/ ND-CP

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 152/2011/TT-BTC |

Hanoi, November 11, 2011 |

CIRCULAR

GUIDING THE GOVERNMENT'S DECREE NO. 67/2011/ ND-CP OF AUGUST 8, 2011, DETAILING AND GUIDING A NUMBER OF ARTICLES OF THE LAW ON ENVIRONMENTAL PROTECTION TAX

Pursuant to November 15, 2010 Law No. 57/20I0/QHI2 on Environmental Protection Tax;

Pursuant to November 29, 2006 Law No. 78/2006/QH11 on Tax Administration and government decrees detailing the implementation of the Law on Tax Administration;

Pursuant to the National Assembly Standing Committee's Resolution No. 1269/2011/NQ-UBTVQH12 of July 14, 2011, on the Environmental Protection Tariff;

Pursuant to the Government's Decree No. 67/2011/ND-CP of August 8, 2011, detailing and guiding a number of articles of the Law on Environmental Protection Tax;

Pursuant to the Government's Decree No. 118/2008/ND-CP of November 27, 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

The Ministry of Finance guides the implementation as follows:

Chapter I

SCOPE OF APPLICATION

Article 1. Taxable objects

Taxable objects defined in Article 3 of the Law on Environmental Protection Tax and Article 2 of the Government's Decree No. 67/2011/ND-CP of August 8, 2011, are specified as follows:

1. Petrol, oil and grease, including:

1.1. Petrol, except ethanol;

1.2. Jet fuel;

1.3. Diesel fuel;

1.4. Kerosene;

1.5. Fuel oil;

1.6. Lubricants;

1.7. Grease.

Petrol, oil and grease specified in this Clause include all kinds of petrol, oil and grease (below collectively referred to as petrol and oil) of fossil origin which are sold in Vietnam, excluding bio-preparations (such as ethanol, vegetable oil, animal fat, etc.).

For mixed fuel containing bio-fuel and petrol and oil of fossil origin, environmental protection tax shall be calculated and collected only for the volume of petrol and oil of fossil origin.

2. Coals, including:

2.1. Lignite (brown coal);

2.2. Anthracite coal;

2.3. Fat coal;

2.4. Other coals.

3. Hydrochlorofluorocarbon (HCFC) solution, meaning a group of the ozone layer-depleting substances used as refrigerant in cooling equipment and semi-conductor industry, which are domestically produced, imported separately or in imported refrigeration electric equipment.

4. Taxable plastic bags (soft plastic bags), meaning thin plastic bags and packings made of high density polyethylene (HPDE), low density polyethylene (LDPE) or linear low density polyethylene (LLDPE) resin, excluding environmentally friendly ready-made goods packings and plastic bags complying with the environmental protection law and the guidance of the Ministry of Natural Resources and Environment.

5. Herbicides restricted from use.

6. Termiticides restricted from use.

7. Forest product preservatives restricted from use.

8. Storehouse disinfectants restricted from use.

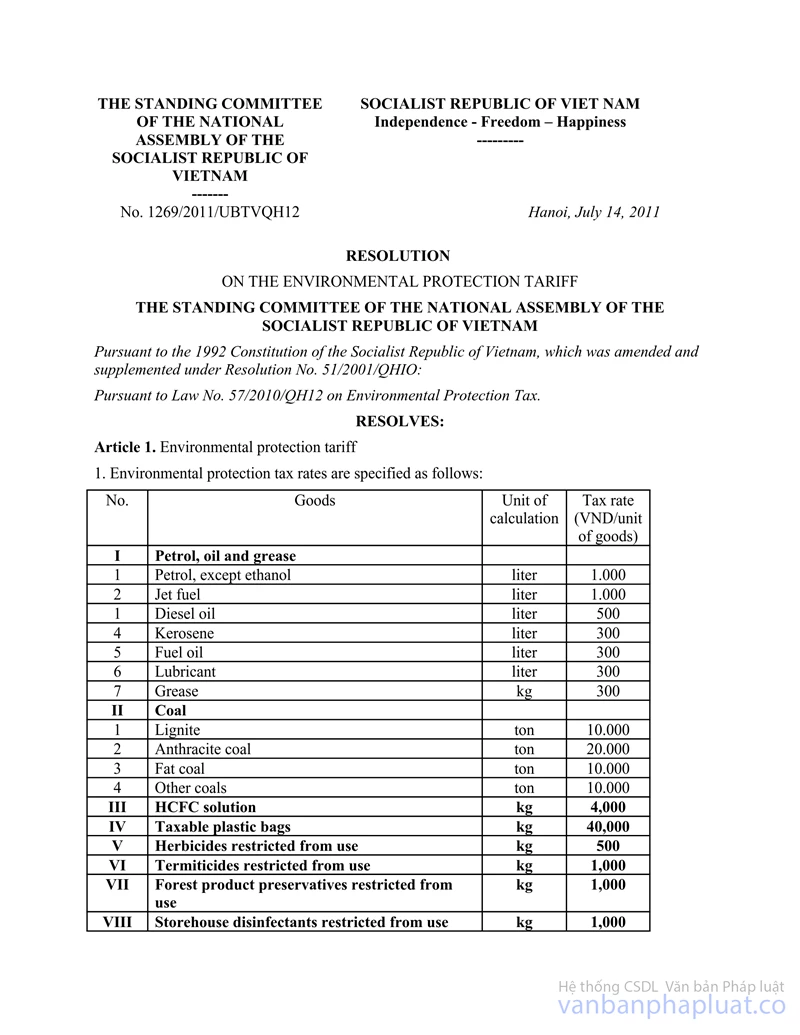

Details of herbicides restricted from use, termiticides restricted from use, forest product preservatives restricted from use and storehouse disinfectants restricted from use are specified in the National Assembly Standing Committee's Resolution No. 1269/2011/NQ-UBTVQH12 of July 14, 2011, on the Environmental Protection Tariff.

Article 2. Objects not liable to tax

1. Goods not specified in Article 3 of the Law on Environmental Protection Tax and guided in Article 2 of Decree No. 67/2011/ND-CP and Article 1 of this Circular are not liable to environmental protection tax.

2. Goods specified in Article 3 of the Law on Environmental Protection Tax and guided in Article 2 of Decree No. 67/2011/ND-CP and Article 1 of this Circular arc not liable to tax in the following cases:

2.1. Goods transported from exporting countries to importing countries via Vietnamese border gates (transited or transported via border gates, including goods already brought into bonded warehouses) for which procedures for import into or export out of Vietnam are not carried out.

2.2. Goods transited via border gates or the border of Vietnam under agreements concluded between the Vietnamese Government and a foreign government or between agencies or representatives authorized by the Vietnamese Government and a foreign government under law.

2.3. Goods temporarily imported for re-export within the time limit specified by law.

2.4. Goods exported abroad directly by producers (including processors) or exporters as entrusted, unless organizations, households and individuals purchase goods subject to environmental protection tax for export.

Based on goods' customs dossiers, customs clearance offices shall determine goods not liable to environmental protection tax specified in this Clause.

Article 3. Taxpayers

1. Environmental protection tax payers include organizations, households and individuals producing and importing taxable goods specified in Article 1 of this Circular.

2. Environmental protection tax payers are defined in some cases as follows:

2.1. Entrusted importers shall pay environmental protection tax, regardless of the form of entrustment and of whether goods are exported and delivered to entrusting parties or entrusted parties.

2.2. Producing and processing organizations, households and individuals that are concurrently entrusted to sell goods into the Vietnamese market shall pay environmental protection tax. In case processing organizations, households and individuals are not entrusted to sell goods, processing-ordering organizations, households and individuals shall pay environmental protection tax when selling goods in Vietnam.

2.3. Organizations, households and individuals that act as principal procurers of coal exploited on a small and scattered scale but fail to produce documents evidencing that environmental protection tax has been paid for the goods shall pay tax.

Chapter II

TAX BASES AND TAX CALCULATION METHOD

Article 4. Tax calculation method

Payable environmental protection tax shall be calculated according to the following formula:

|

Payable environmental protection tax |

= |

Quantity of taxed goods units |

x |

Specific tax amount on a goods unit |

Article 5. Tax bases

Environmental tax bases include quantity of taxed goods and specific tax amount.

1. The quantity of taxed goods is specified as follows:

1.1. For domestically produced goods, it is the quantity of produced goods which are sold, exchanged, used for internal consumption, donated, or used for sales promotion or advertising.

1.2. For imported goods, it is the quantity of imported goods.

In case the quantity of goods subject to environmental protection tax sold and imported is calculated in a unit of measurement other than the unit of tax calculation specified in the Environmental Protection Tariff issued by the National Assembly Standing Committee, the former unit must be converted into the latter for tax calculation.

1.3. For mixed fuel containing petrol, oil or grease of fossil origin and bio-fuel, the quantity of taxed goods in a period is the quantity of petrol, oil or grease of fossil origin contained in the quantity of mixed fuel imported or produced which is sold, exchanged, donated or used for internal consumption, converted into the unit of measurement specified for tax calculation applicable to relevant goods. The method of determination is as follows:

|

Quantity of taxed petrol, oil or grease of fossil origin |

= |

Quantity of mixed fuel imported or produced which : is sold, used for internal consumption, exchanged, donated |

x |

Percentage (%) of petrol, oil or grease of fossil origin contained in mixed fuel |

Pursuant to competent agencies' technical standards on processing of mixed fuel (even in case of change in the percentage (%) of petrol, oil or grease of fossil origin contained in mixed fuel), taxpayers shall themselves calculate, declare and pay environmental protection tax for the quantity of petrol, oil or grease of fossil origin; and concurrently notify tax offices of the percentage (%) of petrol, oil or grease of fossil origin contained in mixed fuel and submit such notices together with tax declaration forms of the month following the month in which mixed fuel is sold (or which sees change in the percentage of petrol, oil or grease of fossil origin contained in mixed fuel).

2. Specific tax amount used as a basis for calculating environmental protection tax for each kind of goods is the tax amount specified in the Environmental Protection Tariff issued together with the National Assembly Standing Committee's Resolution No. 1269/2011/NQ-UBTVQH 12 of July 14, 2011.

Chapter III

TAX DECLARATION, PAYMENT AND REFUND

Article 6. Tax calculation time

1. For produced goods sold, exchanged, donated, used for sales promotion or advertising, the tax calculation time is the time of transfer of the goods ownership or use right.

2. For produced goods used for internal consumption, the tax calculation time is the time goods are put into use.

3. For imported goods, the tax calculation time is the time of registration of customs declarations, except petrol and oil imported for sale as specified in Clause 4 of this Article.

4. For petrol and oil produced or imported for sale, the tax calculation time is the time principal petrol and oil traders sell petrol and oil.

Article 7. Tax declaration and payment

1. Tax declaration and payment comply with the Law on Environmental Protection Tax, the Law on Tax Administration and guiding documents, specifically as follows:

1.1. Environmental protection tax declaration dossiers shall be made according to form 01/TBVMT attached to this Circular (not printed herein) and documents related to tax declaration and calculation.

For goods exported, imported, transited or temporarily imported for re-export, their customs dossiers may be used as environmental protection tax declaration dossiers.

Goods producers and traders shall be accountable for their declaration of environmental protection tax. Any detected cases of false tax declaration, tax fraud or tax evasion shall be handled under the law on tax administration.

1.2. Places for submission of tax declaration dossiers:

a/ For domestically produced goods (except locally sold coals of Vietnam Coal-Mineral Industries Group, and petrol and oil), environmental protection tax payers shall submit environmental protection tax declaration dossiers to managing tax offices.

A taxpayer that has an establishment producing goods subject to environmental protection tax in a province or centrally run city other than his/her/its head office shall submit environmental protection tax declaration dossiers to the managing tax office in the locality in which such establishment is based.

b/ For imported goods (except petrol and oil imported for sale), taxpayers shall submit tax declaration dossiers to customs clearance offices.

1.3. Declaration of environmental protection tax:

a/ For produced goods sold, exchanged, used for internal consumption, donated, used for sales promotion or advertising, tax shall be declared, calculated and paid on a monthly basis under the Law on Tax Administration and guiding documents.

In case there is no payable environmental protection tax amount in a month, taxpayers are still required to make and submit tax declarations to tax administration agencies for monitoring.

b/ For imported goods and goods imported under entrustment which are subject to environmental protection tax, taxpayers shall declare, calculate and pay tax each time when there is an environmental protection tax amount (except petrol and oil imported for sale).

Environmental protection tax on imported goods shall be declared, calculated and paid simultaneously with declaration and payment of import duty, except imported petrol and oil which comply with Clause 2, Article 7 of this Circular.

In this case, the time limit for environmental protection tax payment is the time limit for import duty payment under the Law on Tax Administration and guiding documents.

2. Environmental protection tax declaration and payment in some cases are specified as follows:

2.1. Producers and traders importing HCFC-containing plastic bags and refrigeration electric equipment shall, pursuant to quality standards on produced and imported goods and relevant documents and dossiers, declare and pay environmental protection tax under regulations.

2.2. For petrol and oil:

Principal petrol and oil traders shall register, declare and remit environmental protection tax into the state budget at tax offices in localities in which they declare and pay value-added tax, specifically as follows:

- Principal petrol and oil traders that directly import, produce and process petrol and oil (collectively referred to as principal units) shall declare and pay tax in localities in which they are headquartered for the quantity of petrol and oil they directly sell, including the quantity of petrol and oil sold for use for internal consumption, sold for exchange for other products and goods, sold for return of goods imported under entrustment, or sold to other organizations and individuals outside the system of principal units (even enterprises in which principal traders hold 50% shares or less), except the quantity of petrol and oil sold and imported under entrustment to other principal petrol and oil traders.

- Independent cost-accounting member units attached to principal units; branches attached to principal units; joint-stock companies whose dominating shares (over 50% of shares) are held by principal units or branches attached to the above member units or joint-stock, companies (collectively referred to as member units) shall declare and pay tax in localities in which member units are headquartered for the quantity of petrol and oil sold by member units to other organizations and individuals outside the system.

- Other organizations directly importing, producing and processing petrol and oil shall declare and pay tax at tax offices in localities in which they declare and pay value-added tax when selling petrol and oil.

- For petrol and oil used as raw materials for mixing bio-petrol for which environmental protection tax has not yet been declared and paid, when selling bio-petrol, sellers shall declare and pay environmental protection tax under regulations.

2.3. For domestically exploited and sold coal:

2.3.1. For coal managed by Vietnam Coal-Mineral Industries Group (Vinacomin) and assigned to member units for exploitation, processing and sale, environmental protection tax shall be declared and paid as follows:

a/ Monthly, companies acting as principal units in selling Vinacomin's coal shall allocate payable environmental protection tax amounts to localities in which coal is exploited in proportion to the quantities of coal procured by local coal production and mining companies and make tables for calculating environmental protection tax according to the form provided in Appendix 02/TBVMT to this Circular (not printed herein).

Environmental protection tax amounts to be allocated to localities in which coal is exploited shall be determined based on the percentage (%) of domestically sold coal to the total quantity of coal sold and the quantity of locally exploited coal sold to principal coal consumers of Vinacomin, according to the following formula:

|

Percentage (%)of the output of domestically consumed coal in a period |

= |

Output of domestically consumed coal in a period |

|

Total quantity of consumed coal in a period |

|

Environmental Protection tax amount to be paid to the locality in which coal is exploited in a period |

= |

Percentage (%) of domestically consumed coal in a period |

x |

Output of coal procured from units in the locality in which coal is exploited in a |

x |

Specific tax amount on one ton of consumed coal |

b/ The principal coal-consuming company shall declare and pay the whole environmental protection tax on domestically exploited and consumed coal according to form 01/TBVMT and Appendix 02/TBVMT to this Circular to the tax office managing the principal company, and concurrently send a copy of Appendix 02/TBVMT to the tax office managing the mining company.

c/ Based on the environmental protection tax amount calculated to be paid by each locality in Appendix 02/TBVMT in a tax period, the principal coal-consuming company shall make a document for payment of environmental protection tax to the locality in which it is headquartered (if there is a payable tax amount) and localities in which coal is exploited.

A tax payment document must indicate that the tax is remitted into the state budget revenue account at the state treasury of the same level with the tax office in the locality in which the principal company registers tax declaration and the tax office in the locality in which the coal mining company is based.

The state treasury in the locality in which the principal coal-consuming company is headquartered shall transfer money and state budget collection documents to the concerned state treasury for accounting as state budget revenue the tax amount of the coal mining company.

2.3.2. Other coal producers and traders (including coal used for internal consumption) shall declare and pay environmental protection tax at tax offices of localities in which coal is exploited.

2.3.4. Taxpayers that are organizations, households or individuals acting as principal procurers of coal exploited on a small and scattered scale shall declare environmental protection tax to managing tax offices.

3. For imported coal: Taxpayers shall make declaration under Item b, Point 1.3, Clause 1 of this Article. If importing crude coal containing anthracite coal, taxpayers must separately declare the quantity of imported anthracite coal in order to pay environmental protection tax at the rate applicable to anthracite coal. If the actual quantity of imported anthracite coal is different from the quantity of coal declared upon import, taxpayers shall make additional declaration and adjustment.

4. Environmental protection tax shall be paid only once for produced or imported goods. In case environmental protection tax has been paid for exported goods which must be re-imported into Vietnam, environmental protection tax needs not to be paid upon import.

For organizations and individuals that purchase goods for production and business purposes for which environmental protection tax has been paid, environmental protection tax on purchased goods shall be accounted as cost of goods or cost price of products. For organizations and individuals that sell goods subject to environmental protection tax, value-added taxed price is the price inclusive of environmental protection tax.

Article 8.Tax refund

Environmental protection taxpayers may have the paid environmental protection tax amount refunded in the following cases:

1. Imported goods which are still in warehouses or storing yards at border gates and under customs supervision and allowed to be re-exported abroad.

2. Goods imported for transfer and sale to foreign parties via Vietnam-based agents; petrol and oil sold to foreign firms' vehicles on routes via Vietnamese ports or to Vietnamese vehicles on international routes under law.

3. For goods temporarily imported for re-export by the mode of temporary import for re-export, the paid environmental protection tax amount shall be refunded for the quantity of re-exported goods.

4. For imported goods re-exported abroad by importers (including returned goods), the paid environmental protection tax amount shall be refunded for the quantity of re-exported goods.

5. For goods temporarily imported for display at fairs, exhibitions or product shows. the paid environmental protection tax amount shall be refunded for the quantity of re-exported goods.

Refund of environmental protection tax under this Article applies only to actually exported goods. Procedures, dossiers, order and competence for environmental protection tax refund for exported goods comply with regulations applicable to refund of import duty under the law on import duty and export duty.

Chapter IV

ORGANIZATION OF IMPLEMENTATION

Article 9. Distribution of state budget revenues

State budget distribution with regard to environmental protection tax revenues complies with regulations of competent state agencies.

Article 10. Effect

1. This Circular takes effect on January 1, 2012. To annul the Finance Ministry's Circular No. 06/2001/TT-BTC of January 17, 2001, guiding the Government's Decree No. 78/2000/ ND-CP of December 26, 2000, on petrol and oil charges, Circular No. 63/2001/TT-BTC of August 9, 2011, Circular No. 70/2002/TT-BTC of August 19, 2002, amending and supplementing Circular No. 06/2001/TT-BTC and the provisions on tax administration of petrol and oil charges in the Finance Ministry's Circular No. 28/2011/TT-BTC of February 28, 2011.

2. Petrol and oil producers and traders are not required to declare and pay environmental protection tax on the quantities of petrol and oil for which petrol and oil charges had been declared and paid before January 1, 2012.

3. Violations related to environmental protection tax shall be handled under the Law on Tax Administration and guiding documents.

4. Ministries, ministerial-level agencies, government-attached agencies, provincial-level People's Committees and related organizations and individuals shall implement this Circular.

Any problems arising in the course of implementation should be promptly reported to the Ministry of Finance for study and settlement.-

|

|

FOR

THE MINISTER OF FINANCE |