Nội dung toàn văn Official Dispatch No. 1199/BTC-TCT environmental protection tax

|

MINISTRY OF

FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 1199/BTC-TCT |

Ha Noi, January 30, 2012 |

|

To: |

- Provincial-level Tax Departments; |

On November 11, 2011, the Ministry of Finance issued Circular No. 152/2011/TT-BTC to guide the implementation of Government’s Decree No. 67/2011/ND-CP of August 8, 2011, detailing and guiding the implementation of a number of articles of the Law on Environmental Protection Tax, which took effect on January 1, 2012. However, the Ministry of Finance has received some recommendations through the program on law dissemination among enterprises. In order to implement the environmental protection tax policies, the Ministry of Finance provides the following guidance:

1. Regarding tax declarers and payers:

- Article 3 of Circular No. 152/2011/TT-BTC stipulates: “Environmental protection tax payers are organizations, households and individuals that produce or import goods liable to the tax specified in Article 1 of this Circular…”

- Clauses 1 and 2, Article 10 of Circular No. 152/2011/TT-BTC stipulate: “1. This Circular takes effect on January 1, 2012…

2. Organizations and individuals that produce or trade in petrol and oil are not required to declare and pay environmental protection tax for petrol and oil volumes for which they have declared and paid the petrol and oil charge before January 1, 2012.”

Therefore, organizations, households and individuals producing or importing of goods liable to environmental protection tax that import, sell, exchange, donate or give as gifts these goods from January 1, 2012, on shall declare and pay environmental protection tax in accordance with law (except petrol and oil for which the petrol and oil charge has been declared and paid before January 1, 2012). Particularly, organizations, households and individuals that purchase coal exploited on a small scale shall produce environmental protection tax payment receipts for coal amounts actually purchased from January 1, 2012, on. In case they have no environmental protection tax payment receipt, coal-purchasing organizations, households and individuals shall declare and pay the tax.

2. Regarding lubricating oil and grease imported together with imported aircraft supplies and spare parts or imported machinery and equipment:

- Articles 3 and 5 of the Law on Environmental Protection Tax stipulate:

“Article 3. Tax-liable objects

1. Petrol, lubricating oil and grease, including:

…

f/ Lubricating oil;

g/ Lubricating grease.”

“Article 5. Taxpayers

1. Environmental protection tax payers are organizations, households and individuals that produce or import goods liable to the tax specified in Article 3 of this Law.”

- Item b, Clause 1.2, Article 7 of the Ministry of Finance’s Circular No. 152/2011/TT-BTC of November 11, 2011, stipulates: “b/ For imported goods (except petrol and oil imported for sale), taxpayers shall submit tax declaration dossiers to customs offices where customs procedures are carried out.”

According to the above provisions, lubricating oil and grease are liable to environmental protection tax. Enterprises that import aircraft supplies and spare parts or machinery and equipment, which are accompanied by lubricating oil and grease (in separate boxes), shall declare and pay environmental protection tax in accordance with law.

For petrol, lubricating oil and grease imported not for sale, customs offices shall base themselves on tax declaration dossiers of taxpayers to collect environmental protection tax and import duty on these goods like other environmental protection tax-liable imported goods.

Particularly for petrol and oil imported by major petrol and oil companies for sale, these companies do not have to declare environmental protection tax at the same time with declaring and paying import duty but shall declare and pay the tax at the time of delivery for sale or consumption.

3. Regarding environmental protection tax on goods imported into non-tariff zones:

- Point 2.4, Clause 2, Article 2 of Circular No. 152/2011/TT-BTC specifies objects not liable to environmental protection tax as follows:

“2.4. Goods exported abroad directly by their producers (including processors) or by export businesses as entrusted by their producers, except for organizations, households or individuals that purchase goods liable to environmental protection tax for export.”

- Item b, Point 1.2 and Item b, Point 1.3, Clause 1, Article 7 of Circular No. 152/2011/TT-BTC stipulate:

“1.2. Place for submission of tax declaration dossiers:…

b/ For imported goods (except petrol and oil imported for sale), taxpayers shall submit their tax declaration dossiers to customs offices where they carry out customs procedures.

1.3. Environmental protection tax declaration:

b/ For imported goods and goods imported under import entrustment which are liable to environmental protection tax, taxpayers shall make declare, calculate and pay tax for each time of importation (except petrol and oil imported for sale).

The declaration, calculation and payment of environmental protection tax shall be made at the same time with the declaration and payment of import duty for imported goods, except imported petrol and oil which comply with Clause 2, Article 7 of this Circular.

The time limit for payment of environmental protection tax in this case is that for payment of import duty prescribed in the Law on Tax Administration and guiding documents.”

- Clause 3, Article 6 of Circular No. 152/2011/TT-BTC stipulates:

“3. For imported goods, the time of tax calculation is the time of registration of the customs declaration, except petrol and oil imported for sale specified in Clause 4 of this Article.”

Accordingly:

- For goods imported from abroad into non-tariff zones and domestic goods exported into non-tariff zones for consumption in these zones without being exported abroad which are liable to environmental protection tax in accordance with Article 3 of the Law on Environmental Protection Tax, environmental protection tax shall be declared and paid in accordance with regulations.

Customs offices shall base themselves on customs dossiers of goods to determine whether these goods are liable to environmental protection tax. In case imported goods are liable to environmental protection tax, customs dossiers are their environmental protection tax declaration dossiers.

- For imported goods which are exempt from import duty but liable to environmental protection tax, environmental protection tax declaration dossiers are their customs dossiers and the time limit for declaration and payment of environmental protection tax is that for declaration and payment of import duty for these goods which are liable to import duty in accordance with the Law on Tax Administration and the Law on Import Duty, Export Duty.

- Goods imported for processing and then exported abroad are not liable to environmental protection tax in accordance with Point 2.4 of Circular No. 152/2011/TT-BTC mentioned above. Customs offices shall not collect environmental protection tax on these goods upon their importation. For goods being consumable materials and liable to environmental protection tax, after the liquidation of processed goods in accordance with the Ministry of Finance’s Circular No. 117/2011/TT-BTC of August 15, 2011, environmental protection tax shall be collected in accordance with regulations.

4. Regarding environmental protection tax receipts to be issued to taxpayers

- Clauses 1 and 3, Article 44 of the Law on Tax Administration stipulate: “1. Taxpayers shall remit tax amounts into the state budget:

a/ At the State Treasury;

b/ At tax administration agencies which receive tax declaration dossiers;” and “3. When receiving or deducting tax amounts, agencies and organizations shall issue tax payment receipts to taxpayers.”

- Pursuant to Clause 4, Article 20 of the Ministry of Finance’s Circular No. 194/2010/TT-BTC of December 6, 2010, customs offices shall issue receipts, made according to the form set by the Ministry of Finance, to duty payers in case of collecting duty in cash.

- Points 2.2 and 2.4, Section I, Part B of Circular No. 128/2008/TT-BTC of December 24, 2008, guiding the collection and management of state budget revenues through the State Treasury, stipulate:

“2.2. State budget remittance papers:

- State budget remittance papers are state budget revenue receipts, made according to a form set by the Ministry of Finance;

- State budget remittance papers are used in the following cases:

+ Payers of taxes, charges, fees and other revenues (below collectively referred to as taxpayers) remit money amounts into the State Treasury or commercial banks, other credit institutions or agencies authorized to collect state budget revenues;

+ Collecting agencies or authorized organizations or individuals collect and remit collected money amounts into the State Treasury or banks where the State Treasury opens accounts.

+ Taxpayers remit money amounts into temporary collection and custody accounts of collecting agencies (before making state budget remittances as prescribed).”

“2.4. State budget revenue receipts:

2.4.1. Cases in which state budget revenue receipts are used:

- Collecting agencies are assigned to directly collect state budget revenues in cash; organizations and individuals are authorized by collecting agencies to collect taxes, charges, fees and fines;

- Competent state agencies that issue decisions on sanctioning administrative violations directly collect fines;

- The State Treasury directly collect some charges, fees and fines; organizations are authorized by the State Treasury to collect charges, fees and fines.”

Accordingly, environmental protection tax payers, when remit tax amounts into the state budget shall use state budget remittance papers. These papers, with contents on environmental protection tax according to the state budget index, the tax period and the certification of the State Treasury or bank or credit institution of the permitted tax amount, serve as written evidence of environmental protection tax payment by taxpayers.

For imported goods for which environmental protection tax is paid in cash directly to customs offices, customs offices shall issue tax receipts to taxpayers. Receipts of environmental protection tax on imported goods comply with the General Department of Customs’ guidance.

5. Regarding value-added tax (VAT) calculation prices of petrol and oil for which petrol and oil charges have been declared and paid before January 1, 2012:

Clause 4, Article 7 of the Ministry of Finance’s Circular No. 152/2011/TT-BTC of November 11, 2011, guiding the implementation of Decree No. 67/2011/ND-CP on environmental protection tax, guides as follows:

“For organizations and individuals that sell goods liable to environmental protection tax, value-added tax calculation prices are those inclusive of environmental protection tax.”

Clauses 1 and 2, Article 10 of Circular No. 152/2011/TT-BTC stipulate:

“1. This Circular takes effect on January 1, 2012…

2. Organizations and individuals that produce or trade in petrol and oil are not required to declare and pay environmental protection tax for petrol and oil volumes for which they have declared and paid the petrol and oil charge before January 1, 2012.

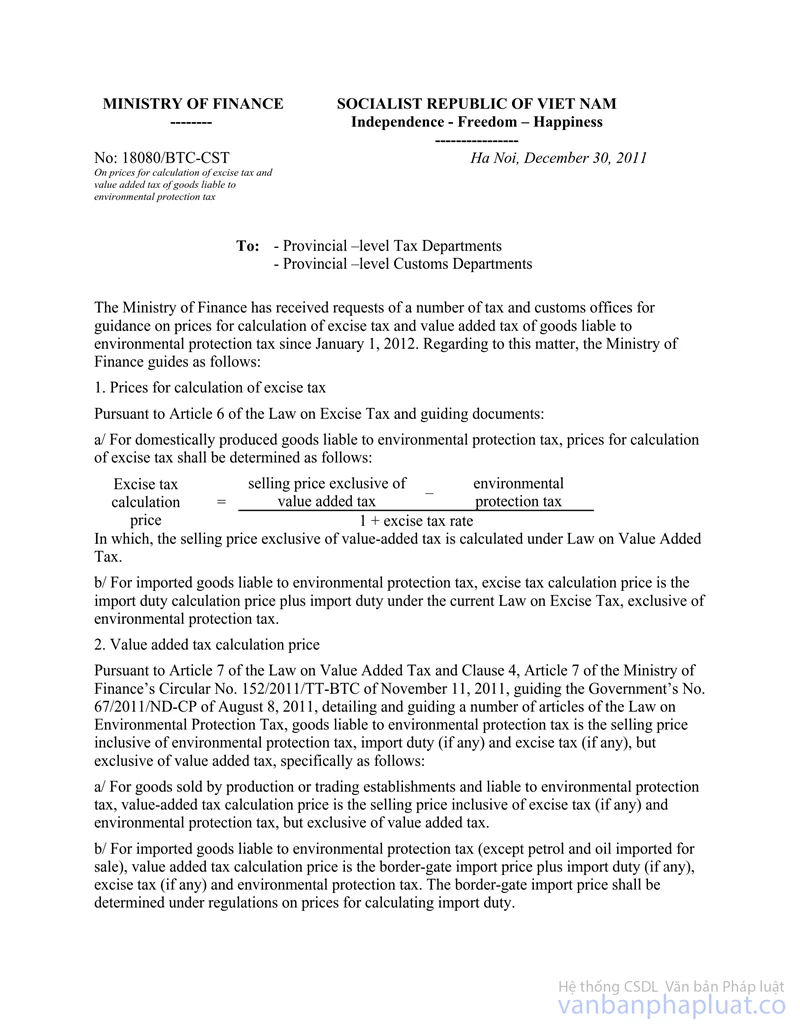

Point 2 of Official Letter No. 18080/BTC-CST of December 30, 2011, guiding value-added tax calculation prices of goods liable to environmental protection tax from January 1, 2012, as follows:

“For goods liable to environmental protection tax and sold by their producers or traders, value-added tax calculation prices are sale prices inclusive of excise tax (if any) and environmental protection tax but exclusive of value-added tax.”

According to the above guidance, for petrol and oil volumes for which the petrol and oil charge has been paid by petrol and oil traders before January 1, 2012, VAT calculation prices from January 1, 2012, are sale prices inclusive of the petrol and oil charge but exclusive of VAT.

6. Regarding the method of writing value-added invoices for goods liable to environmental protection tax

From January 1, 2012, for goods liable to environmental protection tax and petrol and oil for which the petrol and oil charge has been declared and paid before January 1, 2012, the line for sale price in value-added invoices shall be written with a VAT-exclusive price, VAT rate and payable amount, tax-inclusive payment price (without specifying the environmental protection tax or the petrol and oil charge for petrol and oil for which the charge has been declared and paid before January 1, 2012).

Any problems arising in the course of implementation should be reported by provincial-level Tax Departments and Customs Departments to the Ministry of Finance for study and settlement.

|

|

FOR THE

MINISTER OF FINANCE |