Nội dung toàn văn Circular No. 60/2015/TT-BTC amending 152/2011/TT-BTC guidance 67/2011/ND-CP

|

THE MINISTRY OF FINANCE |

THE SOCIALIST REPUBLIC OF VIETNAM |

|

No. 60/2015/TT-BTC |

Hanoi, April 27, 2015 |

CIRCULAR

AMENDING AND SUPPLEMENTING CLAUSE 2 ARTICLE 5 OF THE CIRCULAR NO. 152/2011/TT-BTC DATED NOVEMBER 11, 2011 ON PROVIDING GUIDANCE ON IMPLEMENTATION OF THE GOVERNMENT’S DECREE NO. 67/2011/ND-CP DATED AUGUST 8, 2011 ON PROVIDING SPECIFIC PROVISIONS AND GUIDANCE ON IMPLEMENTATION OF SEVERAL ARTICLES OF THE LAW ON ENVIRONMENTAL PROTECTION TAX

Pursuant to the Law on Environmental Protection Tax No. 57/2010/QH12 dated November 15, 2010;

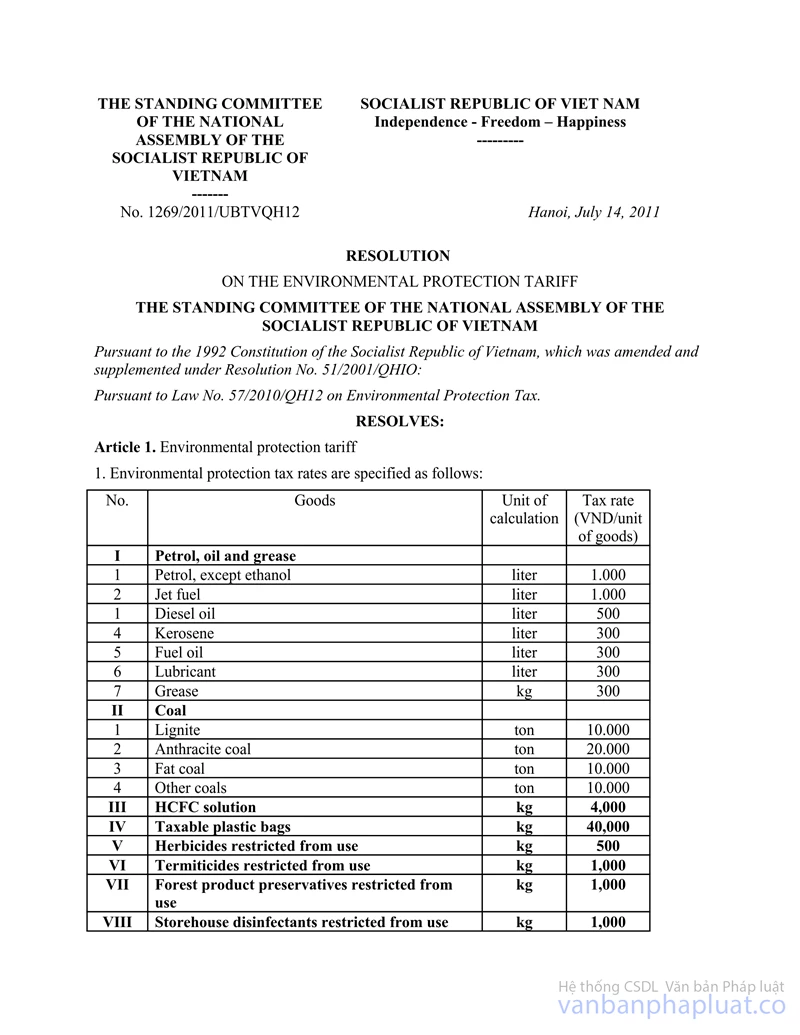

Pursuant to the Resolution No. 1269/2011/UBTVQH12 of the National Assembly Standing Committee dated July 14, 2011 on environmental protection tax schedule and the Resolution No. 888a/2015/UBTVQH13 of National Assembly Standing Committee dated March 10, 2015 on amendments and supplements to the Resolution No. 1269/2011/UBTVQH12 on environmental protection tax schedule;

Pursuant to the Government’s Decree No. 67/2011/ND-CP dated August 8, 2011 on providing specific provisions and guidance on implementation of several articles of the Law on Environmental Protection Tax and the Government's Decree No. 69/2012/ND-CP dated September 14, 2012 on amendments and supplements to Clause 3 Article 2 of the Government’s Decree No. 67/2011/ND-CP dated August 8, 2011;

Pursuant to the Government's Decree No. 215/2013/ND-CP dated December 23, 2013 defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

After considering the request of the Director of the Tax Policy Department,

The Minister of Finance hereby promulgates the Circular on amending and supplementing Clause 2 Article 5 of the Circular No. 152/2011/TT-BTC dated November 11, 2011 on providing guidance on implementation of the Government’s Decree No. 67/2011/ND-CP dated August 8, 2011.

Article 1. Amending and supplementing Clause 2 Article 5 as follows:

The absolute duty rate that serves as the basis for assessment of environmental protection tax on specific commodities is the tax rate stipulated in the environmental protection tax schedule issued together with the Resolution No. 1269/2011/UBTVQH12 of the National Assembly Standing Committee dated July 14, 2011 and the Resolution No. 888a/2015/UBTVQH13 of National Assembly Standing Committee dated March 10, 2015 on amendments and supplements to the Resolution No. 1269/2011/UBTVQH12 on environmental protection tax schedule.

Article 2. Effect

This Circular shall enter into force as from the effective date of the Resolution No. 888a/2015/UBTVQH13 of the National Assembly Standing Committee dated March 10, 2015.

In the course of implementation, if there is any difficulty that may arise, organizations or individuals concerned shall be advised to send timely feedbacks to the Ministry of Finance for further study and possible resolution./.

|

|

PP. THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed