Circular No. 161/2009/TT-BTC of August 12, 2009, guiding personal income tax applicable to transfers of real property and receipt of inheritances and gifts being real property đã được thay thế bởi Circular No. 111/2013/TT-BTC on the implementation of the Law on personal income tax và được áp dụng kể từ ngày 01/10/2013.

Nội dung toàn văn Circular No. 161/2009/TT-BTC of August 12, 2009, guiding personal income tax applicable to transfers of real property and receipt of inheritances and gifts being real property

|

MINISTRY

OF FINANCE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 161/2009/TT-BTC |

Hanoi, August 12, 2009 |

CIRCULAR

GUIDING PERSONAL INCOME TAX APPLICABLE TO TRANSFERS OF REAL PROPERTY AND RECEIPT OF INHERITANCES AND GIFTS BEING REAL PROPERTY

Pursuant to the Law on

Personal Income Tax dated 21 November 2007;

Pursuant to Decree 100/2008/ND-CP of the Government dated 8 September 2008

implementing the Law on Personal Income Tax ("Decree 100");

Pursuant to Decree 118/2008/ND-CP of the Government dated 27 November 2008 on

functions, duties, powers and organizational structure of the Ministry of

Finance;

Pursuant to the opinion and directions of the Prime Minister of the Government

set out in Official Letters of the Government Office 657/VPCP-KTTH dated 3

February 2009 on guidelines for implementation of the Law on Personal Income

Tax; 3199/VPCP-KTTH dated 19 May 2009 on Personal Income Tax applicable to real

property transfers; and 3945/VPCP-KTTH dated 11 June 2009 on guidelines for

implementation of the Law on Personal Income Tax;

The Ministry of Finance hereby provides the following guidelines on

Personal Income Tax applicable to a number of cases of transfer of real

property, and receipt of an inheritance or gift being real property:

Article 1. Determining who is the taxpayer liable to pay tax

Which taxpayer must pay tax on a transfer of real property and on receipt of an inheritance or gift being real property shall be determined specifically as follows:

1. The individual transferor shall be the taxpayer liable to pay Personal Income Tax on a transfer of real property. If a transfer contract stipulates that the transferee must discharge tax obligations on behalf of the transferor, then the transferee shall be liable to declare and pay tax on behalf of the transferor.

2. The individual recipient of an inheritance or gift being real property shall be the taxpayer liable to pay Personal Income Tax on receipt of such inheritance or gift.

3. Each individual joint owner shall be the taxpayer liable to pay Personal Income Tax on a transfer of jointly owned real property, or on receipt of an inheritance or gift being jointly owned real property.

Each individual named in the official document of bequest or donation shall be the taxpayer liable to pay Personal Income Tax in a case of inheritance or receipt of a gift being real property.

The taxpayer liable to pay Personal Income Tax on a transfer of real property shall be determined in accordance with the name of the individual recorded on the land use right certificate [and/or] home ownership certificate. If real property is commonly owned by one group of people or by one family household for which there is a representative named on the land certificate, then the taxpayers liable to pay Personal Income Tax shall be the individual representative so named and also each individual providing a written authorization to such representative for the latter's name to be used (written authorizations certified by the commune people's committee at the place of residence or notarized), or all the people named in the list (if any) attached in accordance with law to the land certificate in the name of a representative. If there are no such written authorizations or if there is no list of people jointly named on a land certificate for which there is a representative, then the individual named in the land certificate shall be the taxpayer liable to pay tax.

Income to be used as the basis for assessing tax on each individual joint owner of real property shall be determined in accordance with the official document of bequest or donation, [or] the agreement between the joint owners in accordance with law at the time the real property was formed; and if one of the above bases do not exist, then [income] shall be divided on average between each individual joint owner.

4. If a land certificate has not yet been issued for real property which is transferred and the competent State administrative authority has consented [to the transfer], then other valid documents recognized by the competent State authority shall provide the basis for determining who is the taxpayer liable to pay Personal Income Tax.

Article 2. Cases where Personal Income Tax is exempt or shall temporarily not be collected

In addition to the cases of Personal Income Tax exemption on income from a transfer of real property and from receipt of an inheritance or gift being real property as stipulated in clauses 1 to 5 inclusive of Section III of Part A of Circular 84-2008-TT-BTC of the Ministry of Finance dated 30 September 2008 ["Circular 84"], the following cases shall be Personal Income Tax exempt or Personal Income Tax shall temporarily not be collected:

1. Personal Income Tax shall temporary not be collected from any individual or family household with a land use right [and/or] who owns a house when making capital contribution by such real property in order to establish an enterprise or to increase production and business capital of an enterprise in accordance with law.

The value of real property as capital contribution to an enterprise shall be determined in accordance with the Law on Enterprises. Any individual contributing capital by real property must attach to his or her tax declaration, documents proving the capital contribution by real property pursuant to the Law on Enterprises and its implementing guidelines.

If profit is distributed to an individual who contributed capital to an enterprise in the form of real property, then such individual must pay Personal Income Tax on such capital investment activity; and if the individual transfers his or her capital contribution portion to another entity3, then the former individual must pay

Personal Income Tax on income from the capital transfer, and must also pay Personal Income Tax on the earlier transfer of the real property as capital contribution to the enterprise.

2. Income being compensation received when the State recovers land, including income paid by economic organizations and being compensation or assistance received when one's land is recovered by the State pursuant to Decrees of the Government 197-2004-ND-CP dated 3 December 2004 and 17-2006-ND-CP dated 27 January 2006 regulating compensation and financial assistance when the State recovers land.

3. Personal Income Tax shall also be exempt on income from the transfer of a residential house [and/or] right to use residential land and assets on the land by an individual who has only one sole residential house [and/or] residential land use right in Vietnam, pursuant to clause 2 of Section III of Part A of Circular 84. A transferor shall be liable to make a self-declaration specifying that Personal Income Tax is exempt pursuant to article 4.2 of the Law on Personal Income Tax, and shall be legally liable for the declaration that he or she has only one sole residential house [and/or] residential land use right in Vietnam.

All cases of incorrect tax declaration which are discovered shall be deemed to be tax fraud, and a transferor in breach shall be obliged to pay tax arrears and shall be fined for tax fraud in accordance with the law on tax management.

Article 3. Obligation to declare and pay tax on transfer of real property

1. If an individual has a land use right [and/or] owns a house which he or she uses to mortgage, to guarantee loan capital or to make payment at a bank or credit institution; but then at the due date for repayment such individual is unable to repay and the bank or credit institution conducts procedures to realize the property by selling it, then the bank or credit institution must declare and pay Personal Income Tax on behalf of the individual prior to conducting accounting finalization of the debt to such individual.

If an individual has a land use right [and/or] owns a house which he or she mortgages in order to borrow capital or to make payment to another entity which then transfers all or a part of such property in order to recover the debt, then the former individual must declare and pay Personal Income Tax or else the latter entity when conducting procedures to transfer the property must declare and pay Personal Income Tax on behalf of such former individual prior to conducting accounting finalization of the debt.

The individual named on the land use right certificate shall be Personal Income Tax exempt when a bank conducts a realization sale of the asset being the sole residential house [and/or] residential land use right of such individual, pursuant to article 4 of the Law on Personal Income Tax.

2. If real property is transferred by an individual transferor to another entity pursuant to an execution judgement of a court, then such transferor must declare and pay tax or else the entity holding the auction must declare and pay Personal Income Tax on behalf of the transferor. Personal Income Tax need not be declared and paid in a case where real property owned by an individual is confiscated by a competent State authority and then auctioned and the proceeds paid into the State budget in accordance with law.

3. If individuals exchange land as between themselves (apart from a case of conversion of agricultural land for production within the category of Personal Income Tax exempt pursuant to article 4.6 of the Law on Personal Income Tax) then each individual exchanging land must declare and pay Personal Income Tax.

4. If an individual contributes capital to an entity to construct a house in order for the former individual to have the right to purchase an apartment or the house foundations, but during the process of contractual performance such individual transfers his or her capital contribution and right to purchase an apartment or the house foundations to another entity, then such individual must declare and pay Personal Income Tax on such activity being a transfer of real property.

5. Any declarant making a Personal Income Tax declaration on behalf of another entity regarding a transfer of real property must record that the declaration is made on behalf of such entity at the end of the declaration and specifically prior to the words 'individual having income' and also add the words 'declared on behalf of', and then write the declarant's full name and sign the declaration, and if the declarant is an organization it must also affix its seal after the signature. The file on tax assessment and the vouchers regarding collection of tax must correctly express that the true taxpayer is the individual having income from the transfer of the real property.

Article 4. Determining tax obligation on income from a transfer of real property accruing before year 2009 and on which financial obligations owing to the State have not yet been discharged

1. Cases of an individual with a contract for the transfer of real property in accordance with law who lodged a valid file with the competent State administrative authority prior to 1 January 2009 shall be dealt with as follows:

1.1. If the amount of tax payable as assessed under the Law on Tax on Assignment of Land Use Rights is less than the amount payable as assessed under the Law on Personal Income Tax, then the transferor shall pay tax in accordance with the provisions of the Law on Tax on Assignment of Land Use Rights; but if the amount of tax payable as assessed under the Law on Tax on Assignment of Land Use Rights is greater than the amount assessed under the Law on Personal Income Tax, then tax may be paid in accordance with the Law on Personal Income Tax. If a taxpayer paid tax into the State budget prior to the date on which this Circular takes effect and such amount was higher than the amount payable, then the tax office shall make a reimbursement in accordance with law.

The Law on Personal Income Tax shall apply to all cases of lodging valid files with the competent State authority after 1 January 2009.

1.2. If the transferor of an apartment lodged a valid file with the competent State authority prior to 1 January 2009, then Personal Income Tax shall not be collected on the value of the house; but regarding the value of the land (if any), Personal Income Tax or tax on transfer of the land use right must be paid in accordance with the guidelines in clause 1.1 above.

2. If an individual has been granted a land use right certificate which records the tax obligations as a debt, then the tax policy effective at the date when the land use right certificate was granted shall apply.

3. In a case of current land use with one of the documents prescribed in article 50.1 of the Law on Land (a document deemed to be valid as proving the land use right) which records the name of some other person pursuant to a transfer of the land use right and the document has been signed by the parties concerned but the actual transfer of the land use right has not been effected in accordance with law, and a valid file was lodged with the competent State authority prior to 1 January 2009, then tax shall be payable as follows:

3.1. If the competent State administrative body issued a land use right certificate prior to 1 January 2009 and recorded tax on the transfer of the land use right as a debt, then the individual must pay tax on the transfer of the land use right.

3.2. If the file was lodged with the competent State body prior to 1 January 2009 but the tax office has not yet assessed and notified the amount of tax payable, then either tax shall be paid on the transfer of the land use right or else Personal Income Tax shall be paid in accordance with the guidelines in clause 1 above.

Article 5. Price of a transfer of real property to be used as the basis for assessing Personal Income Tax

The price of a transfer of real property to be used as the basis for assessing Personal Income Tax shall be the price in accordance with the transfer contract. If the land price in the transfer contract is less than the price level stipulated by the provincial people's committees at the time of lodging a valid file with the competent State body, then the basis for calculating the land price shall be the regulations of the provincial people's committee for purposes of assessing tax; if the land price in the contract is greater than the land price stipulated by the provincial people's committee, then the land price in the contract shall be used for the [tax] assessment.

In cases of receipt of an inheritance or gift being real property, the basis for assessing tax shall be the value of the property at the time of lodging a valid file with the competent State administrative body. The value of a land use right shall be determined on the basis of land prices stipulated by the provincial people's committee; and the value of houses and buildings [including engineering works] on the land shall be the values for assessing registration fees as stipulated by the provincial people's committee.

Article 6. Applicable tax rates

The Law on Personal Income Tax and Decree 100 stipulate that the Personal Income Tax rate on transfers of real property shall be either of the following two rates:

1. Twenty five (25) per cent of taxable income.

If the prime cost and relevant expenses as the basis for determining assessable income are indeterminable, then the tax rate of two (2) per cent of the price of the transfer shall apply.

2. The tax rate of 25% on taxable income shall only apply where the individual transferor of real property has a complete and valid file and vouchers providing the basis for determining the transfer price, the prime cost and relevant expenses; and if the prime cost and relevant expenses are indeterminable, then the tax rate of 2% of the price of the transfer shall apply.

If a land transfer price is less than the land price stipulated by the provincial people's committee at the time of assessing tax, then the tax rate of 2% of the land price stipulated by the provincial people's committee shall apply.

3. The tax office must, in order to select and apply the [correct] tax rates when taxpayers declare tax, co-ordinate with the body managing land and housing to publicly list legal guidelines showing the basis for assessing tax, the method of determining taxable income, and the method of assessing tax and the other guidelines in this Circular; and shall also provide specific guidance to taxpayers to conduct Personal Income Tax declaration and payment either in accordance with the rate of 25% of taxable income or the rate of 2% of the price of the transfer.

Article 7. Organization of implementation

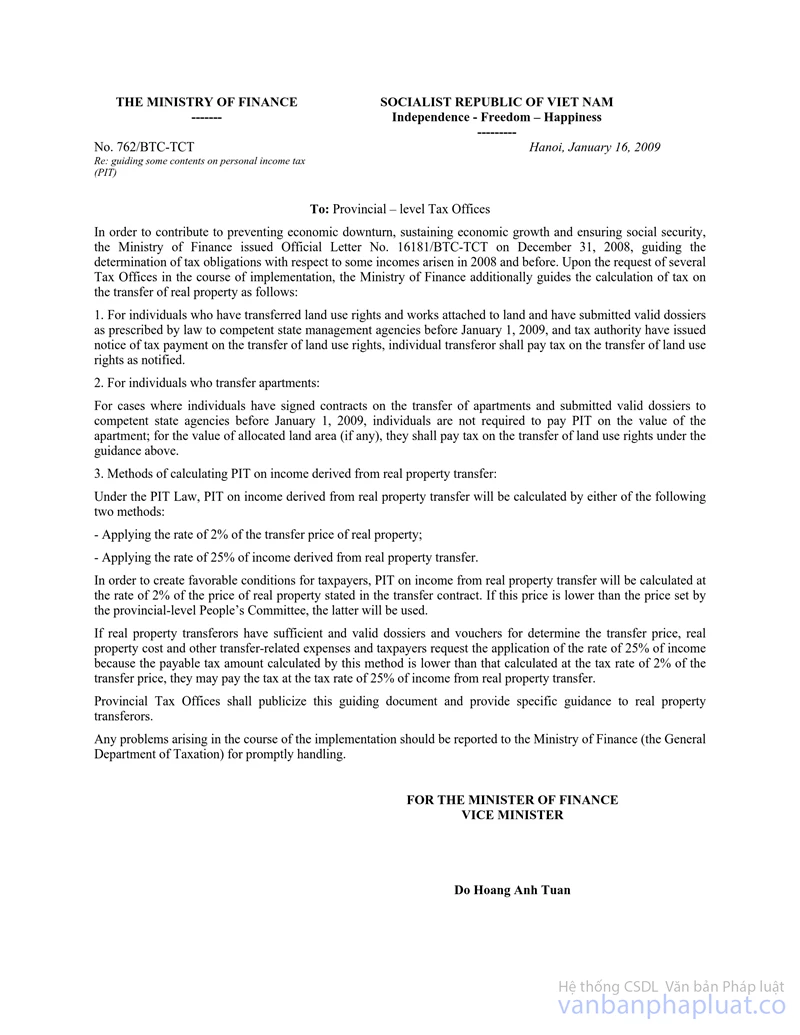

1. This Circular shall be of full force and effect after forty-five (45) days from the date of its signing. The contents of the guidelines in Official Letters of the Ministry of Finance 16181-BTC-TCT dated 31 December 2008 and 762-BTC-TCT dated 16 January 2009 on Personal Income Tax applicable to transfers of real property are hereby repealed.

2. Other matters not guided in this Circular shall be implemented in accordance with the provisions of Circular 84 as amended by Circular 62-2009-TT-BTC of the Ministry of Finance dated 27 March 2009.

Any problems arising during implementation should be reported to the Ministry of Finance for prompt resolution.

|

|

FOR

THE MINISTER OF FINANCE |