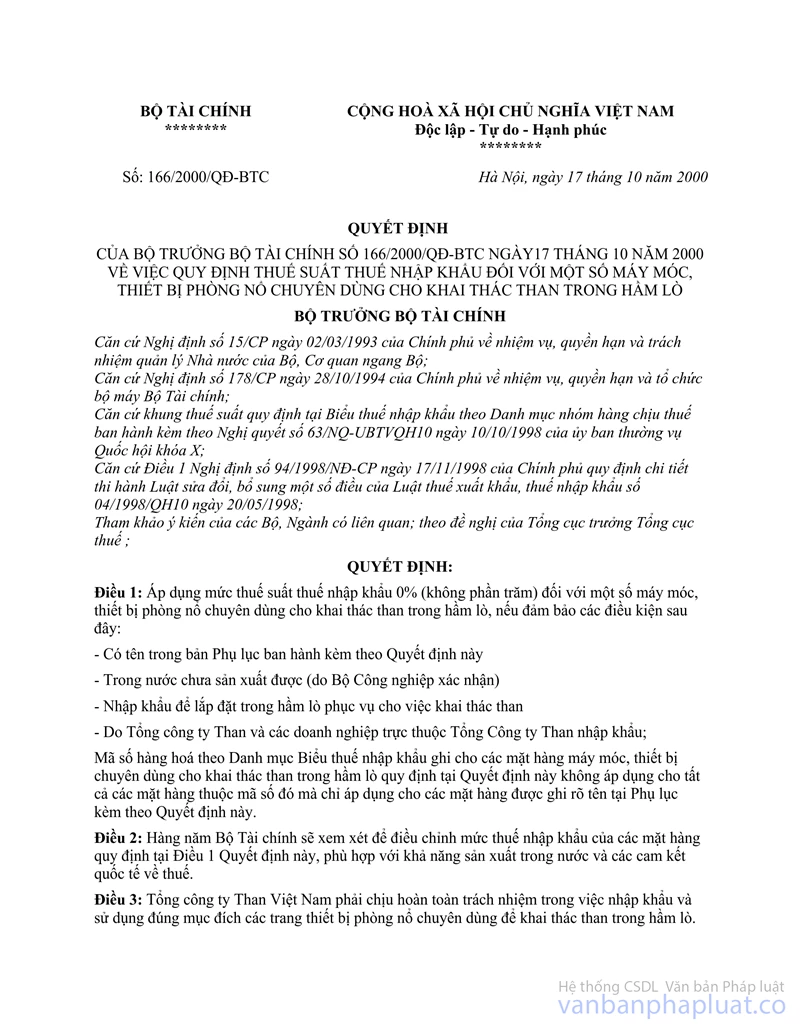

Decision No. 166/2000/QD-BTC of October 17, 2000 stipulating the import tax rates for a number of explosion-preventionmachinery and equipment used exclusively for coal pit extraction đã được thay thế bởi Decision No. 04/2002/QD-BTC of prescribing the preferential import tax rate for a number of explosion-preventing machinery and equipment for exclusive use in pit coal mining as well as a number of supplies and equipment for manufacture and assembly thereof và được áp dụng kể từ ngày 01/02/2002.

Nội dung toàn văn Decision No. 166/2000/QD-BTC of October 17, 2000 stipulating the import tax rates for a number of explosion-preventionmachinery and equipment used exclusively for coal pit extraction

|

THE

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No.166/2000/QD-BTC |

Hanoi, October 17, 2000 |

DECISION

STIPULATING THE IMPORT TAX RATES FOR A NUMBER OF EXPLOSION-PREVENTIONMACHINERY AND EQUIPMENT USED EXCLUSIVELY FOR COAL PIT EXTRACTION

THE MINSITER OF FINANCE

Pursuant

to the Government’s Decree No.15/CP dated March 2, 1993on the tasks, powers and

State management responsibility of the ministries andministerial-level

agencies;

Pursuant to the Government’s Decree No.178/CP dated October 28,1994 on the

tasks, powers and organizational apparatus of the Ministry of Finance;

Pursuant to the tax brackets prescribed in the Import Tariff accordingto the

List of taxable commodity groups, issued together with Resolution

No.63/NQ-UBTVQH10dated October10, 1998 of the Xth National Assembly

Standing Committee;

Pursuant to Article 1 of the Government’s Decree No.94/1998/ND-CPdated November

17, 1998 detailing the implementation of the Law Amending and Supplementinga

Number of Articles of Law No.04/1998/QH10 on Import Tax and Export Tax dated

May 20,1998;

After consulting the concerned ministries and branches; and at theproposal of

the General Director of Tax,

DECIDES

Article 1.- To apply the import tax rate of 0% (zero per cent) to a number ofexplosion-prevention machinery and equipment exclusively used for coal pit extraction, ifthey fully meet the following conditions:

- They are included in the Appendix issued together with this Decision;

- They have not yet been produced in the country (with certification bythe Ministry of Industry);

- They are imported for installation in pits in service of coalexploitation;

- They are imported by the Coal Corporation or its attachedenterprises.

The goods headings on the List of Import Tariff inscribed for themachinery and equipment used exclusively for coal pit exploitation stipulated in thisDecision shall not apply to all commodities of such headings, but only to those which areclearly named in the Appendix enclosed herewith.

Article 2.- Annually, the Ministry of Finance shall consider theadjustment of import tax rates of commodities prescribed in Article 1 of this Decision, inconformity with domestic production capability and international tax commitments.

Article 3.- Vietnam Coal Corporation shall have to bear fullresponsibility for the import and proper use of explosion-prevention equipment and devicesused exclusively for coal pit exploitation. The stipulation of specific import tax ratesfor machinery and equipment used exclusively for coal pit exploitation shall be effectedby December 31, 2005 at the latest.

By March 31 of next year at the latest, the Coal Corporation shall haveto report to the Ministry of Industry and the customs office (where such goods areimported) the situation on the use of such machinery and equipment for coal pitexploitation already imported in the previous year. All cases of use for wrong purposesshall be subject to payment of import tax arrears and be sanctioned in strict accordancewith the provisions of the Import Tariff and the Law on Import Tax and Export Tax.

Article 4.- This Decision takes effect and applies to import goodsdeclarations already submitted to the customs offices as from October 25, 2000.

|

|

FOR THE MINISTER OF

FINANCE |