Decision no. 18/2006/QD-BTC of March 28, 2006 providing for the rates and regime of collection, remittance, management and use of the charge for evaluation of technology transfer contracts đã được thay thế bởi Circular No. 200/2009/TT-BTC of October 15, 2009, providing for charge rates and the collection, remittance, management and use of for evaluation of technology transfer contracts và được áp dụng kể từ ngày 29/11/2009.

Nội dung toàn văn Decision no. 18/2006/QD-BTC of March 28, 2006 providing for the rates and regime of collection, remittance, management and use of the charge for evaluation of technology transfer contracts

|

THE

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 18/2006/QD-BTC |

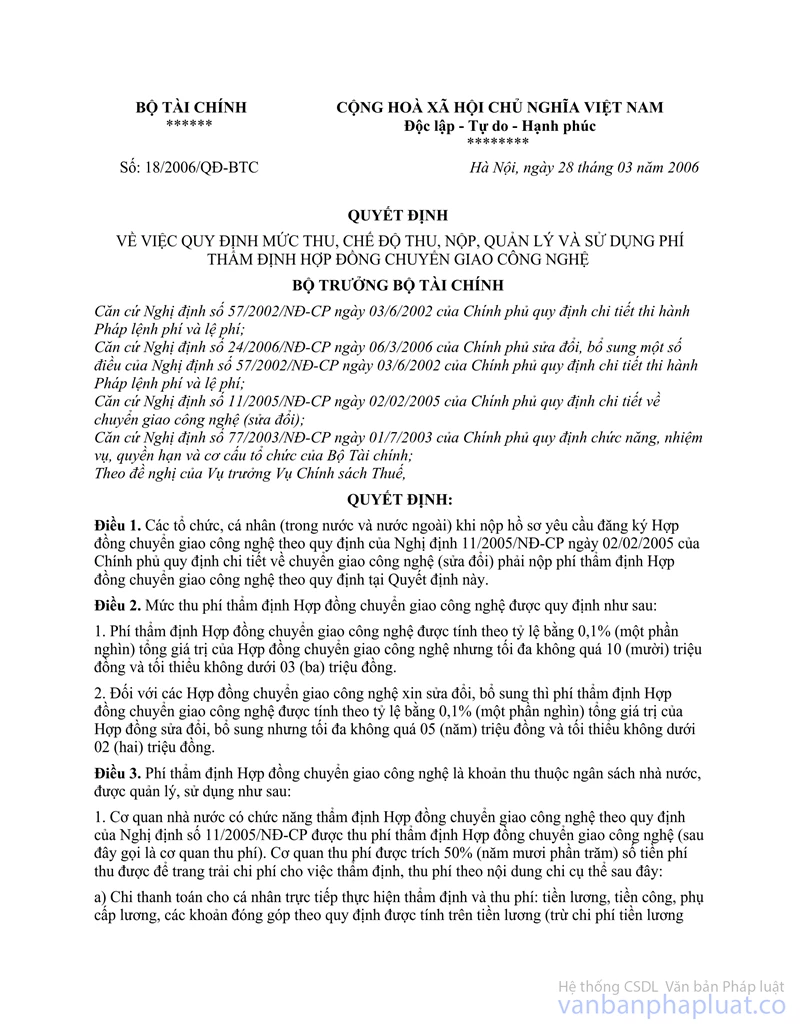

Hanoi, March 28, 2006 |

DECISION

PROVIDING FOR THE RATES AND REGIME OF COLLECTION, REMITTANCE, MANAGEMENT AND USE OF THE CHARGE FOR EVALUATION OF TECHNOLOGY TRANSFER CONTRACTS

THE MINISTER OF FINANCE

Pursuant to the Government's

Decree No. 57/2002/ND-CP of June 3, 2002, detailing the implementation of the

Charge and Fee Ordinance;

Pursuant to the Government's Decree No. 24/2006/ND-CP of March 6, 2006,

amending and supplementing a number of articles of the Government's Decree No.

57/2002/ND-CP of June 3, 2002, which details the implementation of the Charge

and Fee Ordinance;

Pursuant to the Government's Decree No. 11/2005/ND-CP of February 2, 2005,

detailing technology transfer (amended);

Pursuant to the Government's Decree No. 77/2003/ND-CP of July 1, 2003, defining

the functions, tasks, powers and organizational structure of the Finance

Ministry;

At the proposal of the Director of the Tax Policy Department,

DECIDES:

Article 1.- When submitting dossiers of request for registration of technology transfer contracts under the provisions of the Government's Decree No. 11/2005/ND-CP of February 2, 2005, detailing technology transfer (amended), domestic and foreign organizations and individuals shall pay a charge for evaluation of technology transfer contracts in accordance with this Decision.

Article 2.- Rates of charge for evaluation of technology transfer contracts are specified as follows:

1. The charge for evaluation of a technology transfer contract is equal to 0.1% (one thousandth) of the total value of that contract but must be between VND 3 (three) million and 10 (ten) million.

2. The charge for evaluation of a modified technology transfer contract is equal to 0.1% (one thousandth) of the total value of that contract but must be between VND 2 (two) million and 5 (five) million.

Article 3.- The charge for evaluation of technology transfer contracts is a state budget revenue and is managed and used as follows:

1. State agencies with the function of evaluating technology transfer contracts defined in Decree No. 11/2005/ND-CP (below referred to as charge-collecting agencies) may collect the charge for evaluation of technology transfer contracts and retain 50% (fifty per cent) of the collected charge amount to cover expenses for the evaluation and charge collection, specifically as follows:

a/ Payments to individuals directly involved in the evaluation and charge collection, including salaries, wages, salary-based allowances and contributions (except cadres and civil servants who are salaried by the state budget according to regulations), over-time allowances for cadres and laborers of charge-collecting agencies;

b/ Evaluation expenses, including:

- Expense for inspection and evaluation of technologies under technology transfer contracts and for inspection of technology transfer under projects;

- Remuneration paid to specialists hired to conduct inspection or evaluation, give comments, and assess evaluation reports;

- Expense for conferences, workshops or meetings of the council for evaluation of technology transfer contracts.

c/ Expense in direct service of the evaluation and charge collection, including stationery, office supplies, communication, electricity, water, working-trip allowances, etc., according to current criteria and norms;

d/ Expense for regular repair and overhaul of assets, machinery or equipment directly used in the evaluation and charge collection; depreciation of fixed assets used in the evaluation and charge collection;

e/ Expense for procurement of supplies or materials, and other expenses directly related to the evaluation or charge collection;

f/ Expense for rewards and welfare benefits for the agencies' staff members directly involved in the evaluation or charge collection on the principle that the average annual expense per person must not exceed 3 (three) months' paid salaries if the revenue of the current year is higher than that of the previous year, or 2 (two) months' paid salaries if the revenue of the current year is lower than or equal to that of the previous year, after the expenses specified at Points a, b, c, d and e of this Clause have been covered.

Annually, charge-collecting agencies shall make revenue-expenditure finalization according to actually collected charge amounts and actually paid expenses. After making finalization according to regulations, the charge amount which has not yet been spent in the year may be carried forward to to the subsequent year for further spending according to regulations. The charge amount retained by charge-collecting agencies to cover expenses for the evaluation and charge collection shall not be accounted into the state budget.

2. After subtracting the amount at the percentage specified in Clause 1 of this Article, charge-collecting agencies shall remit the remainder (50%) of the actually collected charge amount into the state budget according to corresponding chapters, categories or clauses, Section 042, Sub-section 21 of the current State Budget Index.

Article 4.-

1. This Decision takes effect 15 days after its publication in "CONG BAO."

2. To annul Joint Circular No. 139/1998/TTLT/BTC-BKHCNMT of October 23, 1998, of the Ministry of Finance and the Ministry of Science, Technology and Environment, guiding the collection and use of the evaluation charge and registration fee for technology transfer contracts.

3. Other matters related to the charge collection, remittance, management and use, charge receipts, and the publicization of the charge collection regime which are not mentioned in this Decision shall comply with the Finance Ministry's Circular No. 63/2002/TT-BTC of July 24, 2002, guiding the implementation of legal provisions on charges and fees.

4. Any problems arising in the course of implementation should be promptly reported to the Finance Ministry for study and additional guidance.

|

|

FOR THE MINISTER OF FINANCE |