Circular No. 25/1998/TT-BTC of the Ministry of Finance, amending and supplementing Circular No.78/1997/TT-BTC of November 4, 1997 of the Ministry of Finance đã được thay thế bởi Circular No. 44/1999/TT-BTC of April 26, 1999, guiding tax preferences for cooperatives và được áp dụng kể từ ngày 01/01/1999.

Nội dung toàn văn Circular No. 25/1998/TT-BTC of the Ministry of Finance, amending and supplementing Circular No.78/1997/TT-BTC of November 4, 1997 of the Ministry of Finance

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

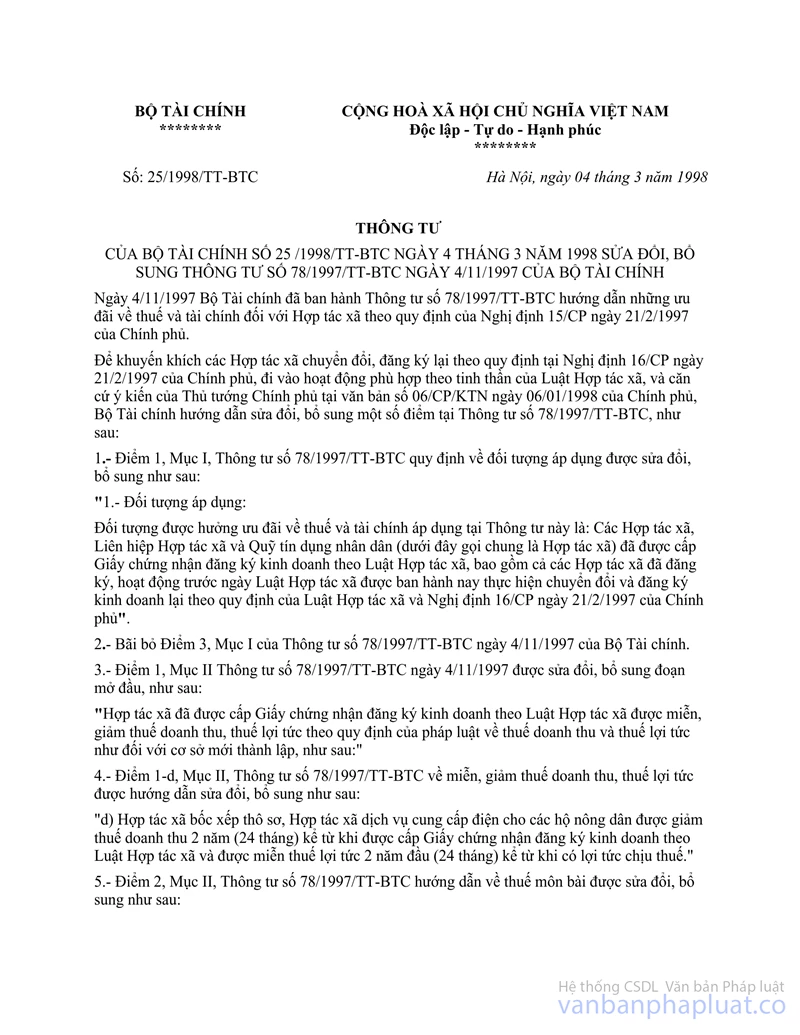

No. 25/1998/TT-BTC |

Hanoi, March 4, 1998 |

CIRCULAR

AMENDING AND SUPPLEMENTING CIRCULAR No.78/1997/TT-BTC OF NOVEMBER 4, 1997 OF THE MINISTRY OF FINANCE

On November 4, 1997 the Ministry of Finance issued Circular No.78/1997/TT-BTC to provide guidance on tax and financial preferences for cooperatives in accordance with Decree No.15-CP of February 21, 1997 of the Government.

In order to encourage cooperatives to transform and re-register as prescribed in Decree No.16-CP of February 21, 1997 of the Government and to operate in the spirit of the Law on cooperatives and proceeding from the Prime Minister's opinions in Document No.6-CP/KTN of January 6, 1998 of the Government, the Ministry of Finance hereby makes the following amendments and supplements to a number of points in Circular No.78/1997/TT-BTC of November 4, 1997:

1. Point 1, Section I of Circular No.78/1997/TT-BTC of November 4, 1997 on the scope of application is amended and supplemented as follows:

"1.- Scope of application:

"1.-The subjects that are entitled to the tax and financial preferences under this Circular include: cooperatives, unions of cooperatives and the people's credit funds (hereafter collectively referred to as cooperatives) which have been granted business registration certificates under the Law on Cooperatives, including cooperatives which were registered and operating before the effective date of the Law on Cooperatives and have been transformed and registered their business in accordance with the Law on Cooperatives and Decree No. 16-CP of February 21, 1997 of the Government."

2. To annul Point 3, Section I of Circular No. 78/1997/TT-BTC of November 4, 1997 of the Ministry of Finance.

3. The first paragraph of Point 1, Section II of Circular No. 78/1997/TT-BTC of November 4, 1997 is amended and supplemented as follows:

"Cooperatives which have been granted business registration certificates under the Law on Cooperatives shall enjoy turnover tax and profit tax exemption and/or reduction like newly established units as prescribed by the legislation on turnover tax and profit tax, as follows:"

4. Point 1-d, Section II of Circular No. 78/1997/TT-BTC of November 4, 1997 on turnover tax and profit tax exemption and/or reduction is amended and supplemented as follows:

"d/ Cooperatives engaged in manual loading and unloading of merchandises and cooperatives engaged in the provision of power supply services for farmers' households shall be entitled to turnover tax reduction for two years (24 months) from the time they are granted business registration certificates under the Law on Cooperatives and to profit tax exemption for the first two years (24 months) from the time the taxable profit is generated."

5. Point 2, Section II of Circular No. 78/1997/TT-BTC providing guidance on license tax is supplemented and amended as follows:

"The imposition of license tax on cooperatives should depend on the degree of the production relationship and the business and production organization of each cooperative.

Specifically:

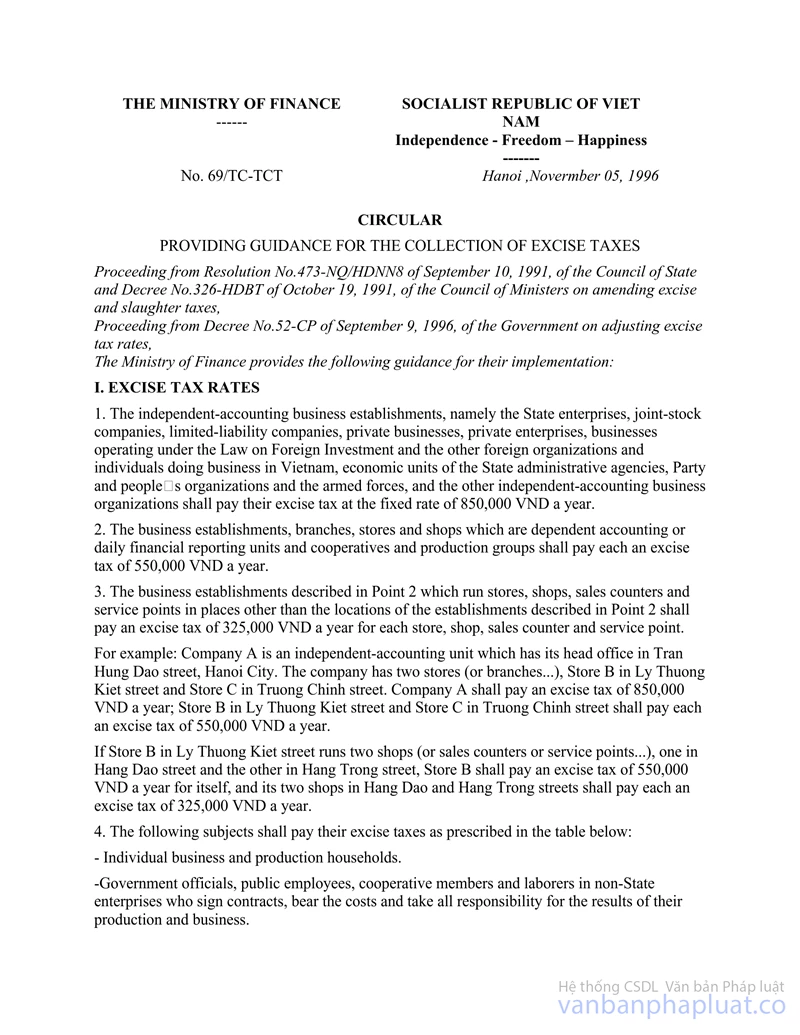

Cooperatives shall pay license tax according to Point 2, Section I of Circular No. 69-TC-TCT of November 5, 1996 of the Ministry of Finance;

Shops, stores and dependent cost-accounting business units of cooperatives shall pay license tax according to Point 3, Section I of Circular No. 69-TC/TCT of November 5, 1996 of the Ministry of Finance;

Cooperative members who perform the tasks assigned by their cooperatives (including transportation or construction cooperatives) shall not have to pay license tax. In cases where individual cooperative members or groups of cooperative members do business mainly on their own and their relationship with the cooperatives is merely nominal, they shall have to pay license tax according to Point 4. Section I of Circular No. 69-TC/TCT of November 5, 1996 of the Ministry of Finance."

6. Point 3, Section II of Circular No. 78/1997/TT-BTC providing guidance on registration fee is supplemented and amended as follows:

"Cooperative members' production means (subject to registration fee) for which registration fee has been paid and which are contributed as capital to cooperatives, shall be exempt from registration fee when the cooperatives register their right to own or use these means;

Production means which the cooperatives have registered their right to own or use shall not be subject to registration fee when they are transferred among the cooperative members for use;

In cases where a cooperative returns production means to its members, these members shall have to pay registration fee when registering their right to own or use them.

7. This Circular takes effect from the effective date of Circular No. 78/1997/TT-BTC of November 4, 1997 of the Ministry of Finance

|

|

FOR THE MINISTER OF

FINANCE |