Circular No. 35/1998/TT-BTC of March 21, 1998, guiding the import tax exemption procedures applicable to organizations and individuals engaged in oil and gas activities under the law on petroleum đã được thay thế bởi Circular No. 48/2001/TT-BTC, promulgated by the Ministry of Finance, guiding the implementation of tax provisions applicable to organizations and individuals conducting oil and gas prospection, exploration and exploitation activities under the Petroleum Law. và được áp dụng kể từ ngày 10/07/2001.

Nội dung toàn văn Circular No. 35/1998/TT-BTC of March 21, 1998, guiding the import tax exemption procedures applicable to organizations and individuals engaged in oil and gas activities under the law on petroleum

|

THE MINISTRY

OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

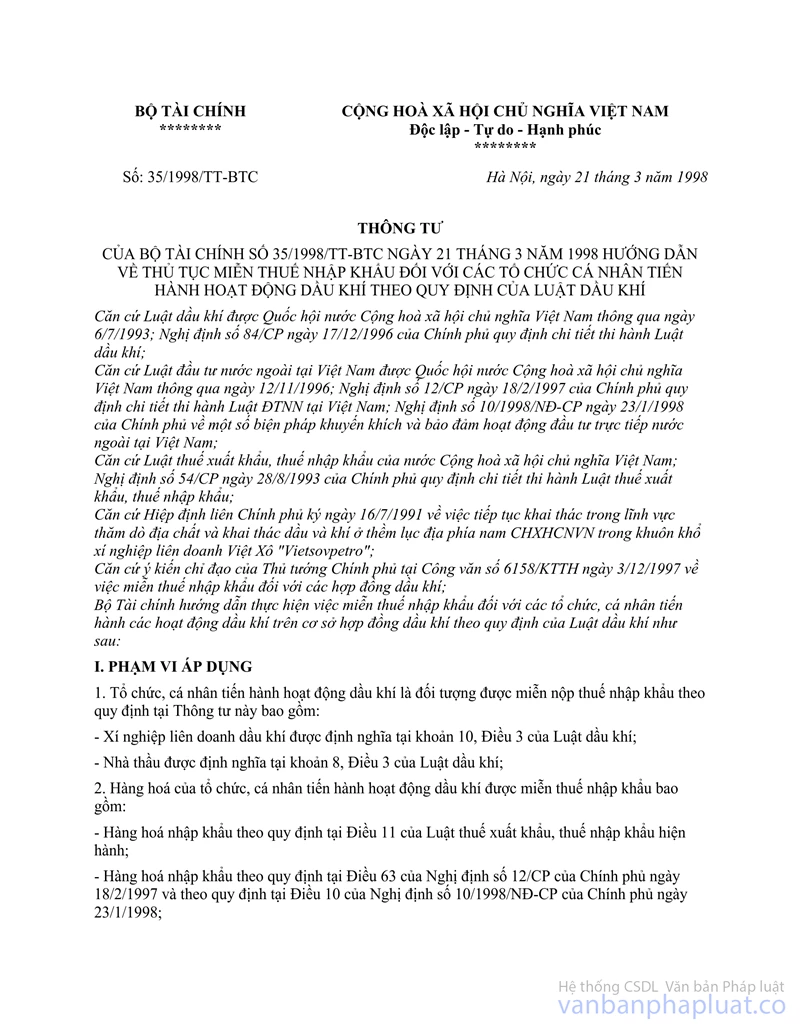

No. 35/1998/TT-BTC |

Hanoi, March 21, 1998 |

CIRCULAR

GUIDING THE IMPORT TAX EXEMPTION PROCEDURES APPLICABLE TO ORGANIZATIONS AND INDIVIDUALS ENGAGED IN OIL AND GAS ACTIVITIES UNDER THE LAW ON PETROLEUM

Pursuant

to the Law on Petroleum adopted by the National Assembly of the Socialist

Republic of Vietnam on July 6, 1993 and Decree No. 84-CP of December 17, 1996

of the Government detailing the implementation of the Law on Petroleum.

Pursuant to the Law on Foreign Investment in Vietnam adopted by the National

Assembly of the Socialist Republic of Vietnam on November 12, 1996; Decree No.

12-CP of February 12, 1997 of the Government detailing the implementation of

the Law on Foreign Investment in Vietnam and Decree No. 10/1998/ND-CP of

January 23, 1998 of the Government on a number of measures to encourage and

guarantee foreign direct investment activities in Vietnam;

Pursuant to the Law on Import Tax and Export Tax of the Socialist Republic of

Vietnam and Decree No. 54-CP of August 28, 1993 of the Government detailing the

implementation of the Law on Import Tax and Export Tax;

Pursuant to the Inter-Governmental Agreement signed on July 16, 1991 on the continued

geological surveys and oil and gas exploitation in the southern continental

shelf of the Socialist Republic of Vietnam within the framework of the

Vietsovpetro joint venture enterprise;

Proceeding from the Prime Minister's direction in Official Dispatch No.

6158/KTTH of December 3, 1997 on the import tax exemption for oil and gas

contracts;

The Ministry of Finance hereby provides the following guidance on the import

tax exemption for organizations and individuals conducting oil and gas

activities under oil and gas contracts in accordance with the Law on Petroleum:

I. SCOPE OF REGULATION

1. Organizations and individuals that conduct oil and gas activities and are eligible for import tax exemption as prescribed in this Circular include:

- Oil and gas joint ventures defined in Clause 10, Article 3 of the Law on Petroleum.

- Contractors defined in Clause 8, Article 3 of the Law on Petroleum.

2. Goods of organizations and individuals conducting oil and gas activities which are exempt from import tax include:

- Goods imported under Article 11 of the Law on Import Tax and Export Tax currently in force;

- Goods imported in accordance with Article 63 of Decree No. 12-CP of February 18, 1997 of the Government and Article 10 of Decree No. 10/1998/ND-CP of January 23 of the Government;

- Materials, equipment and fuel imported in service of oil and gas activities under Clause 5, Article 28 of the Law on Petroleum and Article 41 of Decree No. 84-CP of December 17, 1996;

- Materials and equipment imported by the mode of "temporary import for re-export" in service of oil and gas activities under Clause 5, Article 28 of the Law on Petroleum and Article 41 of Decree No. 84-CP of December 17, 1996;

- Consumer goods, being foodstuff and medicines imported in service of workers working on offshore oil rigs, which have not yet been manufactured in Vietnam.

3. Organizations and individuals conducting oil and gas activities shall have to pay import tax and other taxes and fees (if any) on imported automobiles of various kinds (except for specialized means of transport as part of the technological lines and means used for the transport of workers including automobiles of over 24 seats and waterway means) as well as other taxes and/or fees (if any) on import tax-free goods stated in Point 2, Section I of this Circular.

II. IMPORT TAX EXEMPTION PROCEDURES

Basing itself on the proposal of the Vietnam Oil and Gas Corporation (PetroVietnam) and the operational scope of each oil and gas contract, the Ministry of Trade shall approve the list of import tax-free materials, equipment, fuel, foodstuff and medicines of various kinds in service of offshore oil rig activities for each oil and gas contract. For consumer goods which are foodstuff and medicines of various kinds they must be those goods which have not yet been manufactured in Vietnam and approved by the specialized management agencies.

Basing itself on the list of import tax-free materials, equipment and fuel already approved by the Ministry of Trade, the Customs Departments of the provinces and cities directly under the Central Government shall oversee the importation of such tax-free goods by organizations and individuals conducting oil and gas activities.

In cases where subcontractors import goods under the authorization of organizations and individuals conducting oil and gas activities under oil and gas service contracts on the basis of the list of import tax-free goods approved by the Ministry of Trade for such organizations and individuals, the Customs Departments of the provinces and cities directly under the Central Government shall oversee the import tax exemption for such organizations and individuals.

III. COLLECTION OF IMPORT TAX ARREARS

1. Organizations and/or individuals that wish to use goods, materials, equipment and means of transport which are exempt from import tax and special consumption tax (if any) for any purpose other than serving the oil and gas activities or sell them in Vietnam, shall have to obtain the Trade Ministry's permission, to declare and pay import tax and special consumption tax (if any) arrears as well as other related taxes within two working days after the reason for tax exemption is altered.

For materials and equipment imported free of tax by the mode of "temporary import for re-export", if they are not re-exported out of Vietnam after the termination of the contracts or are sold in Vietnam, they must be declared for payment of import tax arrears within two working days after the reason for tax exemption is altered.

In cases where organizations and/or individuals conducting oil and gas activities transfer automobiles which are exempt from import tax and special consumption tax (if any) to the Vietnam Oil and Gas Corporation as committed in the oil and gas contracts, the Vietnam Oil and Gas Corporation shall have to pay import tax and special consumption tax (if any) arrears.

The declaration and payment of import tax and special consumption tax (if any) arrears shall comply with the guidance in the Law on Import Tax and Export Tax and the Law on Special Consumption Tax, their guiding legal documents currently in force and Circular No. 65-TC/TCT of September 24, 1996 of the Ministry of Finance guiding the determination of prices for the calculation of import tax and special consumption tax on import tax-free goods for which the tax-exemption reason is now altered.

2. Organizations and individuals conducting oil and gas activities shall not have to pay import tax and other related tax arrears in the following cases:

They transfer materials and equipment imported free of tax to the Vietnam Oil and Gas Corporation as agreed upon in the oil and gas contracts in service of oil and gas activities.

They assign automobiles imported free of tax to other organizations or individuals conducting oil and gas activities in cases where they assign the rights and obligations defined in the oil and gas contracts. This provision shall apply only to automobiles which are entitled to import tax exemption before the issuance of this Circular.

3. Organizations and individuals conducting oil and gas activities shall not have to pay import tax arrears but other related taxes in cases where they assign materials and equipment imported free of tax to other organizations or individuals for conducting oil and gas activities.

IV. IMPLEMENTATION PROVISIONS

This Circular applies to customs declarations as from January 1st, 1998. The previous provisions which are contrary to this Circular are hereby annulled.

This Circular replaces Circular No. 75-TC/TCT of October 20, 1995 of the Ministry of Finance.

If any problems arise in the course of implemen-tation, agencies are requested to report to the Ministry of Finance for timely additional guidance.

|

THE MINISTRY OF

FINANCE |