Nội dung toàn văn Circular No. 37/2001/TT-BTC promulgated by The Ministry of Finance, supplementing a number of points to the Finance Ministry's Circular No. 42/1999/TT-BTC of April 20, 1999 guiding the implementation of finance, accounting and tax regimes applicable to duty-free shops in Vietnam.

|

THE

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No: 37/2001/TT-BTC |

Hanoi, May 28, 2001 |

CIRCULAR

SUPPLEMENTING A NUMBER OF POINTS TO THE FINANCE MINISTRY�S CIRCULAR No. 42/1999/TT-BTC OF APRIL 20, 1999 GUIDING THE IMPLEMENTATION OF FINANCIAL, ACCOUNTING AND TAX REGIMES APPLICABLE TO DUTY-FREE SHOPS IN VIETNAM

Pursuant to the Law on Export Tax and Import

Tax; the Law on Enterprise Income Tax and the Law on Value Added Tax;

Pursuant to the Prime Ministers Decision No.205/1998/QD-TTg of October 19,

1998 promulgating the Regulation on duty-free shops; Decision

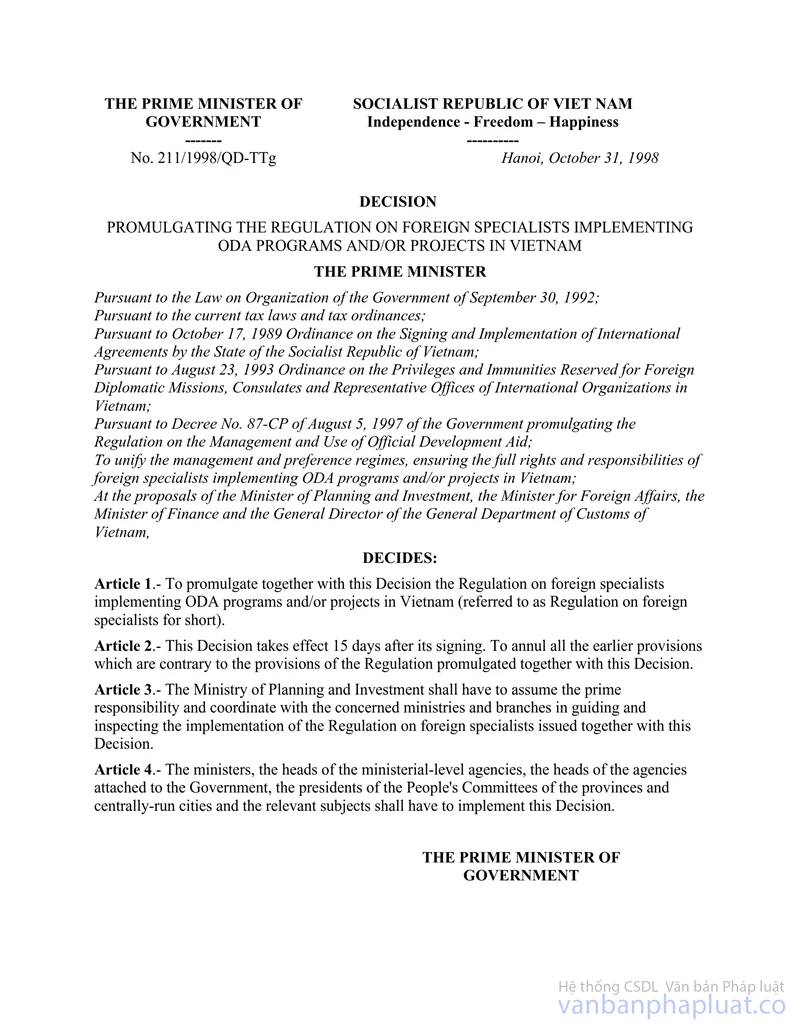

No.211/1998/QD-TTg of October 31, 1998 promulgating the Regulation on foreign

specialists implementing ODA programs and projects in Vietnam; and Decision

No.210/1999/QD-TTg of October 27, 1999 on a number of policies towards overseas

Vietnamese;

Pursuant to the Finance Ministrys Circular No.172/1998/TT-BTC of December

22, 1998 guiding the implementation of the Governments Decree No.54/CP of

August 28, 1993 and Decree No.94/1998/ND-CP of November 17, 1998 detailing the

implementation of the Export Tax and Import Tax Law and the laws amending and

supplementing a number of articles of the Export Tax and Import Tax Law as well

as the Finance Ministrys Circular No.42/1999/TT-BTC of April 20, 1999 guiding

the implementation of financial, accounting and tax regimes applicable to

duty-free shops in Vietnam;

Pursuant to the Prime Ministers directing opinions in the Government Offices

Official Dispatch No.246/VPCP-KTTH of February 16, 2001 on the expansion of

goods items and subjects buying duty-free goods;

After consulting the Trade Ministry, the Ministry of Planning and

Investment, the Ministry for Foreign Affairs and the General Department of

Customs, the Finance Ministry hereby provides additional guidance on a number

of points in above-said Circular No.42/1999/TT-BTC of April 20, 1999 as

follows:

I. TO ADD THE FOLLOWING TO SECTION I (OBJECTS OF APPLICATION) OF CIRCULAR NO.42/1999/TT-BTC:

Duty-free shops are allowed to sell goods to foreign specialists implementing ODA projects in Vietnam (according to the Prime Ministers Decision No.211/1998/QD-TTg of October 31, 1998 promulgating the Regulation on foreign specialists implementing ODA programs and projects in Vietnam) and overseas Vietnamese returning home to work at the invitation of Vietnamese State agencies (according to the Prime Ministers Decision No.210/1999/QD-TTg of October 27, 1999 on a number of policies towards overseas Vietnamese).

II. TAX EXEMPTION CRITERIA, PROCEDURES AND DOSSIERS

1. Duty-free shops are allowed to sell goods in service of foreign specialists implementing ODA projects in Vietnam strictly according to the tax-exemption criteria prescribed in the Prime Ministers Decision No.211/1998/QD-TTg of October 31, 1998 promulgating the Regulation on foreign specialists implementing ODA programs and projects in Vietnam and Circular No.01/2001/TT-TCHQ of February 9, 2001 of the General Department of Customs guiding the implementation of above-said Decision No.211/1998/QD-TTg The tax-exemption procedures and dossiers include:

- For the sale of duty-free goods valued at not more than USD 300 as prescribed in the Governments Decree No.17/CP of February 6, 1995 and Decree No.79/1998/ND-CP of September 29, 1998:

+ The specialists original passport, which must be produced when he/she buys goods. The shop shall have to fully inscribe his/her name, passport number, date of issuance, the issuing body in the sale invoice.

+ The Vietnam entry-exit declaration (original).

- For the sale of duty-free goods being household appliances to specialists allowed to stay in Vietnam for 183 days or more:

+ The Planning and Investment Ministrys certification (copy affixed with stamp of the project management agency) that the concerned foreign specialist is participating in the ODA program and/or project implementation, clearly stating his/her name, nationality, passport number, stay duration in Vietnam and list of his/her dependents.

+ The specialists original passport, which must be produced when he/she buys goods. The shop shall have to fully inscribe his/her name, passport number, date of issuance and the issuing body in the sale invoice.

2. Duty-free shops are allowed to sell duty-free goods in service of overseas Vietnamese who return home to work at the invitation of Vietnamese State agencies strictly according to the tax-exemption criteria stipulated in Joint Circular No.03/2000/TTLT-TCHQ-BNG of June 6, 2000 of the General Department of Customs and the Ministry for Foreign Affairs guiding the implementation of Article 4 of the Prime Ministers Decision No.210/1999/QD-TTg of October 27, 1999 on a number of policies towards overseas Vietnamese. The tax-exemption procedures and dossiers include:

- For the sale of duty-free goods valued at not more than USD 300 as prescribed in the Governments Decree No.17/CP of February 6, 1995 and Decree No.79/1998/ND-CP of September 29, 1998:

+ The goods buyers original passport, which must be produced when he/she buys goods. The shop shall have to fully inscribe his/her name, passport number, date of issuance and the issuing body in the sale invoice.

+ The Vietnam entry-exit declaration (original).

- For the sale of goods being household appliances to overseas Vietnamese who return home to work at the invitation of Vietnamese State agencies as prescribed in Joint Circular No.03/2000/TTLT-TCHQ-BNG of June 6, 2000 of the General Department of Customs and the Ministry for Foreign Affairs:

+ The host Vietnamese State agencys certification that the goods buyer is an overseas Vietnamese returning home to work at its invitation, clearly stating his/her name, nationality, passport number, stay duration in Vietnam, specific jobs, project(s) or plan(s) in which he/she is involved.

+ The goods buyers original passport, which must be produced when he/she buys goods. The shop shall have to fully inscribe his/her name, passport number, date of issuance and the issuing body in the sale invoice.

3. Particularly for goods being household appliances, the eligible subjects can buy them strictly according to the set quota, meaning that each subject can buy only one piece of a duty-free item; If the above-said subjects have bought goods according to the quotas prescribed in the Governments Decree No.17/CP of February 6, 1995 and Decree No.79/1998/ND-CP of September 29, 1998, they shall not be allowed to buy the corresponding duty-free goods as stipulated in the Prime Ministers Decision No.211/1998/QD-TTg of October 31, 1998 and Joint Circular No.03/2000/TTLT-TCHQ-BNG of June 6, 2000 of the General Department of Customs and the Ministry for Foreign Affairs.

III. THE TAX PAYMENT, COLLECTION AND EXEMPTION REGIME; THE ACCOUNTING AND REPORTING REGIME AS WELL AS THE INSPECTION AND HANDLING OF VIOLATIONS:

shall strictly comply with the provisions in the Finance Ministrys Circular No.42/1999/TT-BTC of April 20, 1999 and this Circular.

IV. Implementation effect and organization:

This Circular takes effect 15 days after its signing. The General Department of Customs shall have to guide the procedures to sell goods to subjects eligible for tax exemption as well as the tax exemption procedures and the management of goods traded in duty-free shops according to current regulations.

In the course of implementation, the concerned ministries, branches and units are requested to report arising problems to the Finance Ministry for timely settlement.

|

|

FOR THE FINANCE MINISTER |