Nội dung toàn văn Circular 24/2017/TT-BTC accounting for cooperatives and cooperative unions

|

MINISTRY OF

FINANCE |

THE SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 24/2017/TT-BTC |

Hanoi, March 28, 2017 |

CIRCULAR

ACCOUNTING FOR COOPERATIVES AND COOPERATIVE UNIONS

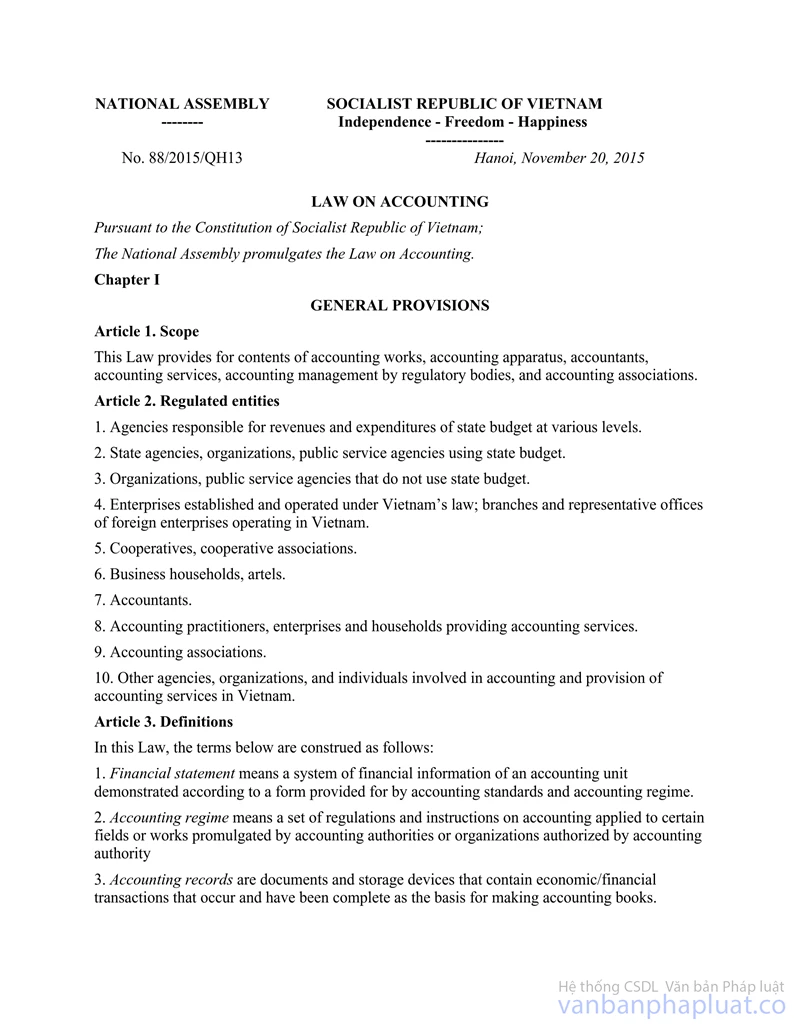

Pursuant to the Law on Accounting No. 88/2015/QH13 dated November 20, 2015;

Pursuant to the Government's Decree No. 215/2013/ND-CP dated December 13, 2013 defining the functions, tasks, entitlements and organizational structure of the Ministry of Finance;

At the request of Director of Department of Audit and Accounting,

The Minister of Finance promulgates a Circular on accounting for cooperatives and cooperative unions.

Chapter I

GENERAL PROVISIONS

Article 1. Scope

This Circular provides guidelines for bookkeeping, preparation of financial statements of cooperatives and cooperative unions (hereinafter referred to as CCU) and does not apply to determination of cooperatives’ tax liability.

Article 2. Regulated entities

1. This Circular applies to all CCU in every field and every line of producing and trading

2. Large-scale CCU with a lot of transactions that are not regulated in this Circular may choose the accounting policy for small and medium enterprises promulgated under the Ministry of Finance’s Circular No. 133/2016/TT-BTC dated August 26, 2016 on accounting for small and medium enterprises (hereinafter referred to as Circular No. 133/2016/TT-BTC) and amendment or replacement document (if any). The choice of application of accounting policy must ensure consistency in the fiscal year and must be notified to the tax authority in charge.

Article 3. General rules

1. If CCU chooses to apply Circular No. 133/2016/TT-BTC they must comply with all regulations specified in this Circular on invoices, accounting journals, accounts, financial statements and other regulations. If CCU has accounting events related to internal credit activities, benefits and additional supports from the State and other contents that are not regulated in Circular No. 133/2016/TT-BTC the provisions in this Circular shall apply.

2. A CCU that wishes to turn back to applying the accounting policies specified this Circular must do it in the beginning of the fiscal year and inform its supervisory tax authority.

Chapter II

SPECIFIC PROVISIONS

Article 4. Chart of accounts

1. Accounts are used for classification and systematization of financial and economic transactions according to economic contents.

2. The accounts applied for CCU consists of the accounts in the balance sheet accounts (includes accounts of type 1 to 6 and 9) and off-balance account (accounts of type 0). Accounts in the balance sheet shall be applied double entry bookkeeping (accounting transactions are recorded in the debit column of at least one account and recorded in the credit column of another account). Off-balance accounts shall be applied the single entry accounting (accounting transactions are only recorded in one side of one account).

3. Adjustments of chart of accounts

a) If the CCU wishes to supplement 1st and 2nd grade accounts or adjust names, codes, contents and accounting methods of particular economic transactions of accounts 1st and 2nd grade, they must gain a written approval from the Ministry of Finance before implementation.

b) CCU may open additional accounts of the 3rd and 2nd grades for the accounts not being specified as the accounts of 3rd and 2nd grades in the list system of accounting accounts prescribed in Section I Annex 1 issued together with this Circular for requirements for CCU’s management without the proposal for approval from the Ministry of Finance.

4. The chart of accounts and the contents, structures, accounting principles and accounting methods are specified in Annex 1 issued together herewith.

Article 5. Accounting records

1. Accounting records are documents and storage devices that contain economic/financial transactions that occur and have been complete as the basis for making accounting books.

2. Accounting records must be made in a clear, complete, timely and accurate manner.

3. CCU may design its own accounting records as long as they are conformable with provisions of the Law on Accounting and suitable for its operation, unless otherwise prescribed by law.

4. Other contents related to accounting records shall be applied the provisions in the Law on Accounting, guiding documents on the Law on accounting and other legal documents related to accounting records and provisions in this Circular.

5. The list of accounting records, forms of accounting records and the methods of making accounting records are specified in Annex 2 issued together herewith.

Article 6. Accounting books

1. Accounting books are used for recording economic/financial transactions that occurred and are related to the CCU.

2. Each accounting book must specify the name of the CCU; name, opening date, closing date of the book; signature of the book maker, chief accountant, legal representative of the CCU, page numbers and overlapping seals.

3. Other contents related to accounting books shall be applied the provisions in the Law on Accounting, guiding documents on the Law on accounting and other legal documents related to accounting books and provisions in this Circular.

4. The list of accounting books, forms of accounting books and the methods of making entries in accounting books are specified in Annex 3 issued together herewith.

Article 7. Financial statement

1. Financial statements of an accounting unit are used for aggregating and describing its financial conditions and performance.

2. Other contents related to financial statements shall be applied the provisions in the Law on Accounting, guiding documents on the Law on accounting and other legal documents related to financial statements and provisions in this Circular.

3. Financial statement system, forms of accounting books, contents and the methods of preparation and presentation of financial statements are specified in Annex 4 issued together herewith.

Chapter III

IMPLEMENTATION

Article 8. Transfer of balances in accounting books

1. Agricultural, forestry, fishery and salt production CCU shall apply the accounting policy promulgated under the Ministry of Finance’s Circular No. 24/2010/TT-BTC dated February 23, 2010 on transferring balances in accounting books as follows:

- Short term deposits recorded in Account 121 – Short term financial investments and long term deposits recorded in Account 2218 - Other long-term financial investments are transferred to Account 1211 – Term deposits. Other short term financial investments recorded in Accounts 121 – Short term financial investments and other long term financial investments recorded in Account 2212 - Capital contribution for joint venture, Account 2213 - Investment in associates and Account 2218 - Other long term financial investments are transferred to Account 1218 - Other financial investments;

- Balance of loan receivables recorded in the detailed account of Account 122 – Lending cooperative members (Account 1221, Account 1222, and Account 1223) is transferred to Account 13211 - Loan receivables. Balance of receivables from loan interests recorded in Account 1318 is transferred to Account 13212 – Receivables from loan interests;

- Balance of receivables recorded in Account 1311 – Receivable from cooperative members, Account 1312 – Receivable from customers outside the cooperatives is transferred to Account 131 - Receivables.

- The detailed balance recorded in Account 1318 - Other receivables (Excluding receivables from loan interests of internal credit activity) is transferred to Account 138 – Other receivables.

- Balances of Account 142 – Short term prepaid expense and Account 242- Long term prepaid expense are transferred to Account 2421 – Prepaid expense;

- Balances of detailed accounts of Account 241- Capital work in progress (Account 2411, Account 2412, Account 2413) are transferred to Account 2422- Capital work in progress;

- Balance of Account 153- Tool is transferred to Account 152- Materials. Balances of detailed accounts of Account 155- Finished goods (Account 1551, Account 1552) are transferred to Account 156- Merchandise.

- The provisions in Account 159 – Provisions (Account 1592, Account 1593) are transferred to Account 229- Provisions against impairment of assets;

- The balances of detailed accounts of Account 311 – Borrowings (Account 3111, Account 3112) are transferred to Account 341- Loans payable

- Balance of Account 322 – Deposit of cooperative members is transferred to Account 33211 - Loan payable; balance of payable to loan interests recorded in Account 3388- Other payable is transferred to Account 33212 – Payable to loan interests;

- Balances of Account 33311- Output VAT, Account 33312- VAT on imports are transferred to Account 3331- VAT payable;

- Balances of Account 3332- Special excise tax, Account 3333- Export and import duties, Account 3335- Personal income tax, Account 3336- Resource royalty, Account 3337- Real property levies and land rents, Account 3339- Fees, charges and other payable are transferred to Account 3338- Other taxes, fees, charges and payable;

- Balance of Account 3341- Payable to cooperative members and Account 3348- Payable to other employees are transferred to Account 334- Payable to employees;

- Balances of Account 3383- Social insurance, Account 3384- Health insurance, Account 3389- Unemployment insurance and other income-based payable (if any) in Account 3388 – Other payables are transferred to Account 335- Income-based payable;

- Balances in Account 3386- Received deposits, Account 3387- Unearned revenues, Account 3388- Other payable (excluding payable to loan interests of internal credit activities and other income-based payable) are transferred to Account 338- Other payables;

- Balances of Account 4111- Capital contributed by cooperative members and Account 4113- Capital received from joint venture are transferred to Account 4111- Capital contributed by members;

- Balances of Account 4112- Capital accumulated by cooperative and Account 4118- Other capital are transferred to Account 4118- Other capital;

- Balance of Account 4114- Capital of investment support of the State is transferred to Account 442- Non-refundable subsidies and investment support of the State;

- Balances of Account 4181- Fund of development of production and business, Account 4182- Reserve fund and Account 4188- Other funds are transferred to Account 418- Funds of equity

- Balances of Account 4211- Previous years’ after-tax profit and Account 4212- Current year’s after-tax profit are transferred to Account 421- Undistributed after-tax profits

2. Non-agricultural CCU shall apply the accounting policy promulgated under the Ministry of Finance’s Decision No. 48/2006/QĐ-BTC dated September 14, 2006 and Circular No. 138/2011/TT-BTC dated April 10, 2011 on transferring balances in accounting books as follows:

- Balances of Account 1113- Gold, silver, valuable metals, gemstones and Account 1123- Gold, silver, valuable metals, gemstones are transferred to Account 152- Inventory, Account 156- Merchandise (for those classified as inventory) and Account 1218- Other financial investment (for those classified as investment).

- Short term deposits recorded in Account 121 – Short term financial investments and long term deposits recorded in Account 2218 - Other long-term financial investments are transferred to Account 1211– Term deposits. Other short term financial investments recorded in Accounts 121 – Short term financial investments and other long term financial investments recorded in Account 2212 - Capital contribution for joint venture, Account 2213 - Investment in associates and Account 2218 - Other long term financial investments are transferred to Account 1218 - Other financial investments;

- Balance in Account 1381- Unresolved asset losses, short term deposit, other receivables recorded in Account 1388- Other receivable and the balance in Account 244- Long term deposit are transferred to Account 138- Other receivable;

- Balances of Account 142 – Short term prepaid expense and Account 242- Long term prepaid expense are transferred to Account 2421- Prepaid expense;

- Balance of Account 241- Capital work in progress is transferred to Account 2422- Capital work in progress;

- Balance of tools and equipment in Account 153- Tool is transferred to Account 152- Materials. The balance of Account 155- Finished goods is transferred to Account 156- Merchandise.

- The provisions in Account 159- Provisions (Account 1591, Account 1592, and Account 1593), provision for devaluation of long term financial investment are transferred to Account 229- Provisions against impairment of assets;

- Balances of Account 311- Short term borrowings, Account 315- Long term debt come due, Account 3411- Long term borrowings and Account 3412- Long term debt are transferred to Account 341- Loans payable;

- Balances of Account 33311- Output VAT, Account 33312- VAT on imports are transferred to Account 3331- VAT payable;

- Balances of Account 3332- Special excise tax, Account 3333- Export and import duties, Account 3335- Personal income tax, Account 3336- Resource royalty, Account 3337- Real property levies and land rents, Account 3339- Fees, charges and other payable are transferred to Account 3338- Other taxes, fees, charges and payable;

- Balances of Account 335- Expenses payable and Account 352- Provisions for payables are transferred to Account 338- Other payable;

- Balances in Account 3381- Assets in surplus pending resolution, Account 3387- Unearned revenues, Account 3388- Other payable (excluding income-based payable) are transferred to Account 338- Other payables;

- Balances of Account 3382- Union expenses, Account 3383- Social insurance, Account 3384- Health insurance, Account 3389- Unemployment insurance and other income-based payable recorded in Account 3388 – Other payables are transferred to Account 335- Income-based payable;

- Balances in Account 3386- Received short term deposits and Account 3414- Received long term deposits are transferred to Account 338- Other payable;

- Balance in account 351- Allowance reserve funds for unemployment (if any) is transferred to Account 418- Funds of equity;

- Balance of Account 3353- Welfare fund formed fixed asset is transferred to Account 3532- Welfare; balance of Account 3534- Manager reward fund is transferred to Account 3531- Reward fund.

- Balance of Account 356- Scientific and technological development fund is transferred to Account 338- Other payable;

- Balance of Account 4111- Capital contributed by owners is transferred to Account 4111- Capital contributed by members;

- Balances of Account 4211- Previous years’ after-tax profit and Account 4212- Current year’s after-tax profit are transferred to Account 421 - Undistributed after-tax profits

- If balances of other Accounts related to internal credit activities of the non-agricultural CCU remains, the CCU shall apply the policy on transfer of balances in accounting books as specified in Clause 1 this Article.

3. Other contents that are not conformable with this Circular must be adjusted to this Circular.

4. Difficulties that arise during the transfer of balances in accounting books shall be reported to the Ministry of Finance for consideration and settlement.

Article 9. Effect

1. This Circular applies to the fiscal year beginning on or after January 01, 2018. All provisions that contravene this Circular are annulled. This Circular supersedes the provisions applied to CCU in the Minister of Finance’s Decision No. 48/2006/QD-BTC dated September 14, 2006 on promulgating the accounting regime applicable to small and medium-sized enterprises, the Ministry of Finance’s Circular No. 138/2011/TT-BTC of October 04, 2011 on amendment, supplementation Decision No.48/2006/QD-BTC and the Ministry of Finance’s Circular No. 24/2010/TT-BTC dated February 23, 2010 on guiding accounting applicable to cooperatives of agriculture, forestry, fishery and salt occupation.

2. Ministries, the People’s Committees, Departments of Finance, Provincial Departments of Taxation shall instruct cooperatives to implement this Circular.

3. Difficulties that arise during the implementation of this Circular shall be reported to the Ministry of Finance for consideration and settlement./.

|

|

PP MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed