Nội dung toàn văn Circular 302/2016/TT-BTC on guidelines for license fees

|

MINISTRY OF

FINANCE |

THE SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 302/2016/TT-BTC |

Hanoi, November 15, 2016 |

CIRCULAR

ON GUIDELINES FOR LICENSE FEES

Pursuant to the Law on fees and charges No. 97/2015/QH13 dated November 25, 2015;

Pursuant to the Law on Tax administration No. 78/2006/QH11 dated November 29, 2006; the Law No. 21/2012/QH13 dated November 20, 2012 on amendments to the Law on Tax administration; the Law No. 71/2014/QH13 dated November 26, 2014 on amendments to the Laws on taxation; the Law No. 106/2016/QH13 dated April 6, 2016 on amendments to the Law on Value-added tax, the Law on special excise duty and the Law on Tax administration;

Pursuant to the Government's Decree No. 139/2016/ND-CP dated October 4, 2016 on license fees;

Pursuant to the Government's Decree No. 215/2013/ND-CP dated December 23, 2013 defining the functions, tasks, entitlements and organizational structure of the Ministry of Finance;

At the request of the Director of the General Department of Taxation,

The Minister of Finance promulgates a Circular on guidelines for license fees as follows:

Article 1. Scope

This Circular deals with licensing fee payers; exemption from licensing fees; amounts of license fees, and declaration and payment of licensing fees.

Article 2. Licensing fee payers

Licensing fee payers are the organizations and individuals engaging in business operation as prescribed in Article 2 of the Government's Decree No. 139/2016/ND-CP dated October 4, 2016 on license fees, except for the cases specified in Article 3 of this Decree and guidance in Article 3 of this Circular.

Article 3. Exemption from licensing fees

Cases of exemption from license fees shall be consistent with Article 3 of the Government's Decree No. 139/2016/ND-CP dated October 4, 2016 on license fees. With regard to cases of exemption from license fees prescribed in Clause 1, Clause 2 Article 3 of Decree No. 139/2016/ND-CP the exempt license fees shall be determined as follows:

1. The individuals, groups of individuals and households engaging in business with annual revenues of less than or equal to VND 100 million. The annual revenue of less than or equal to VND 100 million used to determine an individual, a group of individuals, or a household eligible for exemption from license fees is the total assessable revenue with regard to personal income tax in accordance with regulations of law on personal income tax.

2. The individuals, groups of individuals and households engaging in irregular business or business without fixed locations.

The engaging in irregular business or business without fixed locations shall be consistent with guidance in Point a Clause 1 Article 3 of Circular No. 92/2015/TT-BTC dated June 15, 2015 of the Ministry of Finance on guidelines for value-added tax and personal income tax in terms of residents engaging in business; on guidelines for personal income tax in the Law on amendments to Laws on taxation No. 71/2014/QH13 and Decree No. 12/2015/ND-CP dated February 12, 2015 on guidelines for Law on amendments to Laws on taxation and amendments to Decrees on taxation.

The individuals, groups of individuals, and households without fixed locations in this Clause include individuals being members of cooperatives and cooperatives that have paid license fees as prescribed in regulations on cooperative; individuals who directly conclude contracts to act as lottery agents, insurance agents, or agents charging designated selling prices to withhold tax; individuals entering into business cooperation contracts with organizations as prescribed in law on personal income tax.

Article 4. Amounts of licensing fees

1. The amounts of annual licensing fees for organizations engaging in business as follows:

a) Organizations with charter capital and investment capital of greater than VND 10 billion: VND 3,000,000;

b) Organizations with charter capital and investment capital of less than or equal to VND 10 billion: VND 2,000,000;

c) Branches, representative offices, business premises, public service providers, other business entities: VND 1,000,000.The amounts of licensing fees for the organizations specified in this Clause is based on the charter capital written in the certificate of business registration, the certificate of enterprise registration, or the charter of cooperatives. In case of absence of charter capital, it is based on the investment capital written in the certification of investment registration or decision on investment policies.

If the organizations prescribed in Point a, b of this Clause change their charter capital or investment capital, the ground for determining the amount of licensing fees is their charter capital or investment capital of the year preceding the year of calculation of licensing fees.

Where the charter capital or investment capital written in the certificate of business registration or certificate of investment registration is in foreign currency, it shall be converted into Vietnamese dong as a basis for determining the amount of licensing fees in accordance with the buying rate of commercial banks or credit institutions where the licensing fee payers open their accounts at the time they make payment to the state budget.

2. The amounts of annual licensing fees for individuals, groups of individuals, households engaging in business as follows:

a) Individuals, groups of individuals, households with annual revenues of greater than VND 500 million: VND 1,000,000;

b) Individuals, groups of individuals, households with annual revenues of greater than VND 300 million to less than and equal to VND 500 million: VND 500,000;

c) Individuals, groups of individuals, households with annual revenues of greater than VND 100 million to less than and equal to VND 300 million: VND 300,000.The annual revenue used to determine the amount of license fees an individual, a group of individuals, or a household eligible for exemption from license fees is the total assessable revenue with regard to personal income tax in accordance with regulations of law on personal income tax.

If the individuals, groups of individuals and households specified in this Clause change their revenues, the ground to determine the amounts of licensing fees is the revenues of the year preceding the year of calculation of licensing fees.

With regard to individuals, groups of individuals, or households engaging new business within the year, the revenue used to determine the amount of license fees shall be the revenue of the tax year as prescribed in law on personal income tax.

3. Organizations, individuals, groups of individuals, or households engaging in business or newly-incorporated that are issued with tax registration and TINs, business identification numbers within the first six months shall pay license fees for the whole year; those are incorporated or issued with tax registration and TINs, business identification numbers within the last six months shall pay 50% of license fees for the whole year.

If any organization, individual, group of individuals, or household engaging in business without declaration of license fees, it must pay the amount of license fee for the whole year, irrespective of the time of detection which is in the first 6 months or the last 6 months.

When any organization, individual, group of individuals, or household engaging in business notifies a tax authority of the business suspension for the full calendar year, it is not required to pay the license fee for year of business suspension. If the business is not suspended for the full calendar year, it must the license fee for the whole year.

Article 5. Declaration and payment of licensing fees

1. Declaration and payment of license fees regarding organizations engaging in business.

a) Declaration of license fees

a.1) Declaration of lump sum payment of license fees when the organization has just engaged in business, no later than the last date of the month in which the business commences;

a.2) If a license fee payer has an affiliated entity (branch, representative office, business premises) engaging in business in the same province, the license fee payer must submit declaration of license fees of such affiliated entity to its supervisory tax authority;

a.3) If a license fee payer has an affiliated entity (branch, representative office, and business premises) engaging in business in a province different from the province where the license fee payer is headquartered, such affiliated entity must submit declaration of its license fee to its supervisory tax authority.

a.4) If a license fee payer which has just incorporated has not engaged in business, it must make a declaration of license fees within 30 days from the date on which it is issued with a business registration certificate or certificate of registration for investment and tax registration or enterprise registration certificate; or certificate of registration for branch operation; or the date on which the approval for investment policies is issued.

b) Payment of license fees

Deadline for paying license fees is every January 30. If an organization has just engaged in business or has just established a business facility, the deadline for paying license fees is the deadline for submitting declaration for license fees prescribed in Clause 1 Article 5 of Decree No. 139/2016/ND-CP dated October 4, 2016 on license fees.

2. Declaration and payment of license fees regarding individuals, groups of individuals, households engaging in business

a) Declaration of license fees

a.1) Individuals, groups of individuals, households engaging in business which pay fixed taxes shall not required to pay license fees. The tax authority shall, according to database of total revenues of the individual, group of individuals, household, determine the amount of license fee for each business premises.

a.2) Individuals, groups of individuals, households leasing real estate that declare lump sum payment of license fees upon every contract of real estate lease. If the contract of real estate lease lasts multiple years, license fees shall be paid annually corresponding to number of years which the individual, group of individuals, household making statement of value-added tax, personal income tax. If the individual, group of individuals, household makes statement and lump-sum payment of value-added tax, personal income tax with respect to the contract of real estate lease which lasts multiple years, it shall pay the amount of license fee for one year.

a.3) If the individual, group of individuals, household engaging in business does not make direct tax statement and payment to the tax authority but has an authorized entity to make tax statement and payment on its behalf, the authorized entity shall pay an amount of license fee in case where such individual, group of individuals, household fails to pay such license fee.

b) Payment of license fees

Each individual, group of individuals, household shall pay license fees no later than every January 30.

If a license fee payer being an individual, group of individuals, or a household that has just engaged in business pays fixed tax*, the deadline for paying license fee is no later than the last date of the month succeeding the month in which the tax statement obligation arises* in accordance with law on personal income tax.

Article 6. Entry into force

1. This Circular comes into force from January 1, 2017.

2. This Circular repeals Article 17 of Circular No. 156/2013/TT-BTC dated November 6, 2013 of the Ministry of Finance on guidelines for the Law on Tax administration; Law on amendments to the Law on Tax administration and the Decree No. 83/2013/ND-CP dated July 22, 2013 of the Government and replaces the following Circulars:

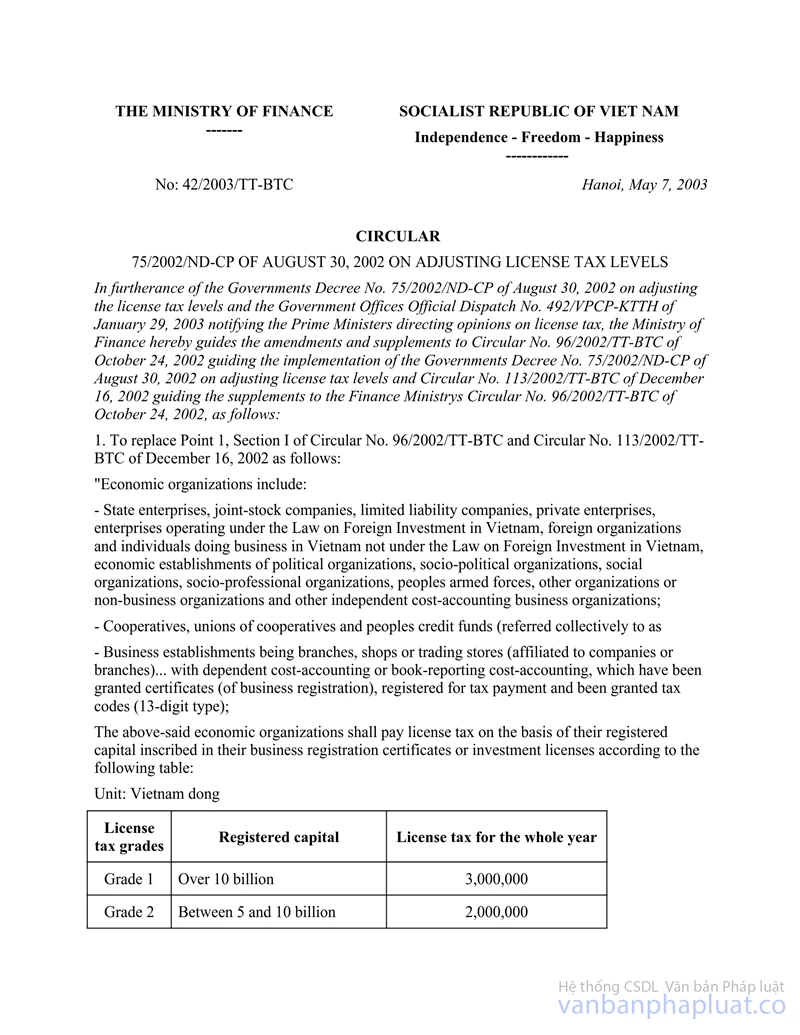

a) Circular No. 96/2002/TT-BTC dated October 24, 2002 of the Ministry of Finance on guidelines for the Government's Decree No. 75/2002/ND-CP dated August 30, 2002 on adjustments to amounts of business license tax*;

b) Circular No. 113/2002/TT-BTC dated December 16, 2002 of the Ministry of Finance on guidelines for Circular No. 96/2002/TT-BTC dated October 24, 2002 of the Ministry of Finance;

c) Circular No. 42/2003/TT-BTC dated May 7, 2003 of the Ministry of Finance on guidelines for amendments to Circular No. 96/2002/TT-BTC dated October 24, 2002.

Article 7. Implementation

1. Annually, Departments of Taxation of provinces/cities shall direct Sub-departments of Taxation in the provinces/cities to:

a) Make and approve the registers, announce annual license fees payable by individuals, groups of individuals, households engaging in business in the same time in which registers of fixed taxes are made and approved and amounts of fixed taxes are announced in accordance with law on personal income tax;

b) Review organizations, individuals, groups of individuals, households engaging in business in the administrative divisions to classify taxpayers operating stably and taxpayers having just engaged in business; determine amounts and the collection of license fees as prescribed.

2. Tax authorities shall propagate and instruct organizations, individuals, groups of individuals, and households engaging in business implement this Circular.

3. Organizations, individuals, groups of individuals, households engaging in business shall make declaration and payment of license fees as prescribed.

4. During the implementation of this Circular, if any document referred to in this Circular is amended or replaced, the amending or replacing document shall prevail.

Difficulties that arise during the implementation of this Circular should be reported to the Ministry of Finance for consideration./.

|

|

PP. MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed