Circular No. 05/2006/TT-BTC, guiding natural resource tax on natural water used for hydroelectricity generation, promulgated by the Ministry of Finance. đã được thay thế bởi Circular No. 42/2007/TT-BTC of April 27, 2007 guiding the implementation of The Governments Decree No. 68/1998/ND-CP of September 3, 1998, detailing the implementation of the ordinance on royalties (amended and Decree No. 147/2006/ND-CP of December 1, 2006, amending and supplementing a number of articles of Decree No. 68/1998/ND-CP và được áp dụng kể từ ngày 24/08/2007.

Nội dung toàn văn Circular No. 05/2006/TT-BTC, guiding natural resource tax on natural water used for hydroelectricity generation, promulgated by the Ministry of Finance.

|

THE

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

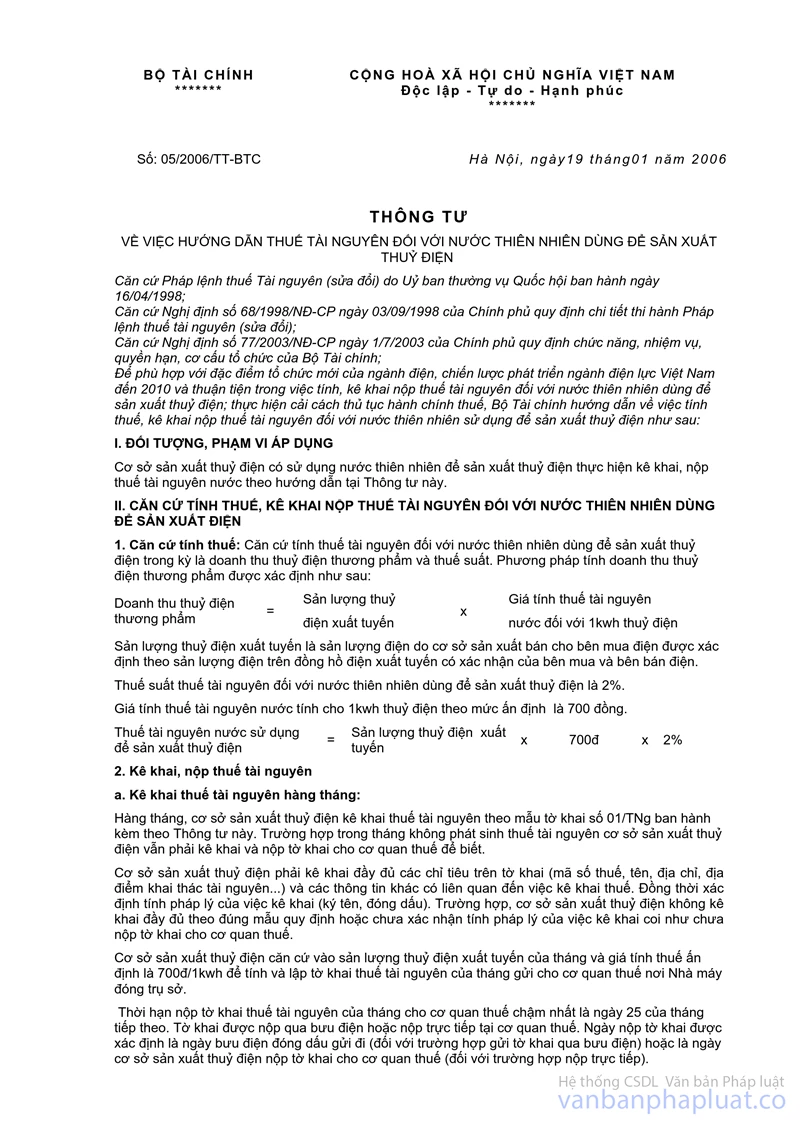

No. 05/2006/TT-BTC |

Hanoi, January 19, 2006 |

CIRCULAR

GUIDING NATURAL RESOURCE TAX ON NATURAL WATER USED FOR HYDROELECTRICITY GENERATION

Pursuant to the Ordinance on

Natural Resource Tax (amended) promulgated on April 16, 1998, by the National

Assembly Standing Committee;

Pursuant to the Government’s Decree No. 68/1998/ND-CP of September 3, 1998,

detailing the implementation of the Ordinance on Natural Resource Tax

(amended);

Pursuant to the Government’s Decree No. 77/2003/ND-CP of July 1, 2003, defining

the functions, tasks, powers and organizational structure of the Finance

Ministry;

In order to suit the new organizational characteristics of the power industry

and the strategy for development of Vietnam’s power industry; make the

calculation and declaration for payment of natural resource tax on natural

water used for hydroelectricity generation easier; and further reform

administrative procedures in taxation, the Finance Ministry hereby guides the

calculation and declaration for payment of natural resource tax on natural

water used for hydroelectricity generation as follows:

I. SUBJECTS AND SCOPE OF APPLICATION

Hydroelectricity generation establishments which use natural water for hydroelectricity generation shall declare and pay water resource tax under this Circular’s guidance.

II. BASES FOR CALCULATION, DECLARATION AND PAYMENT OF NATURAL RESOURCE TAX ON NATURAL WATER USED FOR POWER GENERATION

1. Tax bases: Bases for calculation of natural resource tax on natural water used for hydroelectricity generation in a tax period are commodity hydroelectricity revenue and tax rate. The method of calculating commodity hydroelectricity revenue is as follows:

Price of 1 kWh

Commodity

Hydroelectricity

of

hydroelectricity

hydroelectricity = output

on x

for calculating

revenue

outgoing feeder

water

resource tax

Hydroelectricity output on outgoing feeder means the electricity volume sold by the generation establishment to an electricity purchaser and determined according to the electricity volume figure indicated in the outgoing feeder meter and certified by the electricity purchaser and seller.

The natural resource tax rate applicable to natural water used for hydroelectricity generation is 2%.

The price of 1 kWh of hydroelectricity for calculating water resource tax is fixed at VND 700.

Natural

resource

tax

Hydroelectricity

on water used for

=

output on

x VND

700 x

2%

hydroelectricity

outgoing feeder

generation

2. Declaration and payment of natural resource tax

a/ Monthly declaration of natural resource tax

Monthly, hydroelectricity generation establishments shall declare natural resource tax according to declaration form No. 01/TNg promulgated together with this Circular (not printed herein). Even when no natural resource tax amount arises in a month, hydroelectricity generation establishments shall have to fill in and submit declarations to tax offices for information.

Hydroelectricity generation establishments shall have to fill in all elements of the declaration form (tax identification number, address, location of natural resource exploitation, etc.) and declare other information relating to the tax calculation, and concurrently certify the legality of their declarations (by signing and sealing). Where hydroelectricity generation establishments fail to fully fill in the set declaration form or certify the legality of their declarations, they shall be considered having not yet submitted declarations to tax offices.

Hydroelectricity generation establishments shall base themselves on the hydroelectricity output on outgoing feeder in a month and the fixed tax calculation price of VND 700/kWh to calculate natural resource tax amounts and make natural resource tax declarations for the month, then submit them to the tax offices of the localities where they are located.

The time limit for submitting natural resource tax declarations for a month to tax offices shall be the 25th day of the following month. Declarations may be sent via mail or submitted directly to the tax offices. The date a declaration is submitted shall be the date the sending post office affixes its postmark thereon (for declarations sent via mail) or the date the hydroelectricity generation establishment submits its declaration to the tax office (for those submitted directly to tax offices).

Hydroelectricity generation establishments shall be held before law for the truthfulness and accuracy of the declaration of natural resource tax on natural water used for hydroelectricity generation and keep all written evidence on the declared natural resource tax amounts.

b/ Making of declarations on self-settlement of natural resource tax

Hydroelectricity generation establishments shall have to make declarations on self-settlement of natural resource tax according to a form promulgated together with this Circular (not printed herein).

Declarations on self-settlement of natural resource tax on water used for hydroelectricity generation shall be made and submitted to tax offices within 60 days after the end of a calendar year or a fiscal year, which aim to determine the natural resource tax amount actually arising in the year, payable amount, overpaid amount or exempted or reduced amount (if any).

In case of merger, consolidation, separation, division, dissolution, bankruptcy, ownership conversion, assignment, sale, contracting or lease of state enterprises, concerned business establishments shall have to make and send declarations on self-settlement of natural resource tax to tax offices within 45 days after the date of termination of exploitation contracts or the date of issue of decisions on merger, consolidation, separation, division, dissolution, bankruptcy, ownership conversion, assignment, sale, contracting or lease.

c/ For a hydroelectricity generation establishment which is headquartered in a locality but has its natural resource tax amount distributed to other localities according to the Finance Ministry’s regulations, the tax office managing such hydroelectricity generation establishment shall have to make and send copies of the tax declaration and the declaration on self-settlement of natural resource tax to concerned tax offices which enjoy such natural resource tax for knowledge.

d/ Payment of natural resource tax:

Monthly, hydroelectricity generation establishments shall pay natural resource tax into the state budget according to the declared tax amounts. The deadline for paying natural resource tax shall be the 25th day of the month following the month when the payable natural resource amount arises. Where a payable natural resource tax amount arises according to the declaration on self-settlement of natural resource tax, the hydroelectricity generation establishment shall pay it into the state budget within 60 days after the end of the calendar year or the fiscal year.

In case of merger, consolidation, separation, division, dissolution, bankruptcy, ownership conversion, assignment, sale, contracting or lease of state enterprises, hydroelectricity generation establishments shall have to fully pay the outstanding natural resource tax amount within 45 days after the termination of exploitation contracts or the issue of competent authorities’ decisions on merger, consolidation, separation, division, dissolution, bankruptcy, ownership conversion, assignment, sale, contracting or lease. After tax offices check declarations on self-settlement of natural resource tax and identify overpaid tax amounts, such overpaid tax amounts shall be cleared against payable tax amounts of the subsequent period. For business establishments which have become bankrupt, been dissolved or have terminated their operation, they shall have overpaid tax amounts refunded by tax offices according to current regulations.

For hydroelectricity generation establishments which pay tax by account transfer via banks or other credit institutions, the date of tax payment into the state budget shall be the date banks or other credit institutions remit paid tax amounts to the State Treasury according to business establishments’ vouchers on payment of money into the state budget. For business establishments which pay tax in cash, the date of tax payment into the state budget shall be the date written in tax payment vouchers by tax-collecting agencies or the State Treasury (in cases where tax is collected via the State Treasury).

Hydroelectricity generation establishments shall fill in all elements of payment vouchers under the guidance of tax offices and the State Treasury. They must clearly state in payment vouchers payable tax amount and late payment fine amounts for each tax period. Where business establishments have, apart from tax and fine amounts payable in the current period, tax arrears and unpaid fines from the previous tax periods which, however, are unspecified, tax offices shall clear tax arrears and unpaid fines in the previous periods before clearing tax and fine amounts payable in the current period.

The State Treasury where power generation establishments pay natural resource tax amounts shall have to distribute water resource tax amounts paid by such establishments to localities according to percentages (%) prescribed by the Finance Ministry.

III. ORGANIZATION OF IMPLEMENTATION

1. This Circular takes effect 15 days after its publication in “CONG BAO.”

2. All previous provisions guiding the natural resource tax bases, declaration and payment applicable to hydroelectricity generation establishments which are contrary to this Circular are hereby annulled.

Particularly, the guidance on tax exemption and reduction, handling of violations, commendation, complaints and statute of limitations shall continue complying with the Finance Ministry’s Circular No. 153/1998/TT-BTC of November 26, 1998, guiding the implementation of the Government’s Decree No. 68/1998/ND-CP of September 3, 1998, detailing the implementation of the Ordinance on Natural Resource Tax (amended).

Any problems arising in the course of implementation should be promptly reported by concerned localities and units to the Finance Ministry for study and solution.

|

|

FOR THE

FINANCE MINISTER |