Nội dung toàn văn Circular No. 177/2012/TT-BTC guiding the collection payment management and use

|

THE MINISTRY

OF FINANCE |

SOCIALIST REPUBLIC OF VIETNAM |

|

No. 177/2012/TT-BTC |

Hanoi, October 23rd 2012 |

CIRCULAR

GUIDING THE COLLECTION PAYMENT, MANAGEMENT, AND USE OF FEES AT INLAND WATERWAY PORT AUTHORITIES

Pursuant to the Law on Inland Waterway Navigation;

Pursuant to the Ordinance on Fees and Charges;

Pursuant to the Government's Decree No. 57/2002/NĐ-CP dated June 03rd 2002, and the Government's Decree No. 24/2006/NĐ-CP dated March 06th 2006, detailing the implementation of the Ordinance on Fees and Charges;

Pursuant to the Government's Decree No. 118/2008/NĐ-CP dated November 27th 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance ;

At the proposal of the Director of the Tax Policy Department;

The Minister of Finance promulgate this Circular to guide the collection payment, management, and use of fees at Inland Waterway Port Authorities as follows:

Article 1. Fee payers

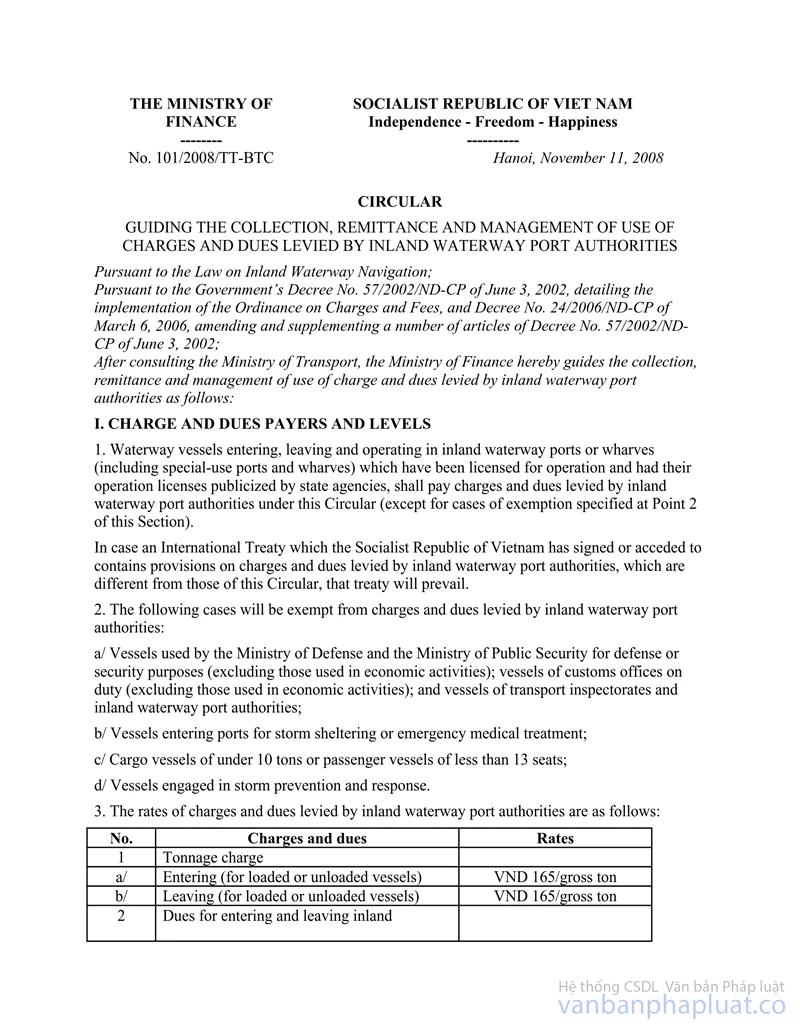

The watercraft entering, leaving, and working and inland ports and wharves (including specialized ports and wharves) licensed by the State must pay fees at Inland Waterway Port Authorities as prescribed in this Circular (except for the cases prescribed in Article 2 of this Circular).

In case the provisions on fees at the Inland Waterway Port Authority in an International Agreement to which the Socialist Republic of Vietnam is a signatory is inconsistent with this Circular, such International Agreement shall apply.

Article 2. Fee exemption

The following cases are exempted from paying fees at Inland Waterway Port Authorities:

1. The vessels serving National defense and security of belonging to the Ministry of National Defense and the Ministry of Public Security (except for the vessels used for economic purposes); the vessels on duty of the customs (except for the vessels used for economic purposes); the vessels of traffic inspectors or Inland Waterway Port Authorities;

2. The vessels taking shelter from storms, and the rescuing vessels;

3. The cargo vessels of which the total weight is less than 10 tonnes, or passenger vessels having fewer than 13 seats;

4. The vessels serving storm and flood fighting.

Article 3. The fee rates

The fee rates at Inland Waterway Port Authorities are provided as follows:

1. The fee rates

|

No. |

Content |

Fee rate |

|

1 |

Tonnage fees |

|

|

a) |

Entrance (loaded or unloaded) |

165 VND/tonne |

|

b) |

Exit (loaded or unloaded) |

165 VND/tonne |

|

2 |

Fees for entrance and exit of inland ports and wharves |

|

|

a) |

Cargo vessel of which the gross tonnage is from 10 – 50 tonnes |

5,000 VND/time |

|

b) |

Cargo vessel of which the gross tonnage is from 51 – 200 tonnes, or passenger vessels that have 13 - 50 seats |

5,000 VND/time |

|

c) |

Cargo vessel or tugging group of which the gross tonnage is from 201 – 500 tonnes, or passenger vessels that have 51 - 100 seats |

20,000 VND/time |

|

d) |

Cargo vessel or tugging group of which the gross tonnage is from 501 – 1,000 tonnes, or passenger vessels that have 101 seats or more. |

30,000 VND/time |

|

dd) |

Cargo vessel or tugging group of which the gross tonnage is from 1,001 – 1,500 tonnes |

40,000 VND/time |

|

c) |

Cargo vessel or tugging group of which the gross tonnage is 1,501 tonnes or more |

50,000 VND/time |

2. The ocean-going vessels entering and leaving inland ports and wharves must pay nautical fees as prescribed by the Ministry of Finance.

3. In case the vessel enters and exits multiples inland ports and wharves under the management of a representative of the Inland Waterway Port Authority in one trip, it only pays fee once as prescribed in Clause 1 this Article.

4. The vessels entering and leaving the port not for loading or unloading goods and passenger must pay 70% of the tonnage fee prescribed in Clause 1 this Article.

5. The vessels other than cargo vessels shall be converted to calculate tonnage fees as follows:

a) Specialized vessels: 01 horsepower is equivalent to 01 tonne of the total tonnage;

b) Passenger vessel: 01 bed is equivalent to 06 seats or 06 tonnes of the total tonnages; 01 seat is equivalent to 01 tonne of the total tonnage.

6. The fees at the Inland Waterway Port Authority are collected in VND. Foreign organizations and individuals shall pay fees in USD at the exchange rates announced by the State bank of Vietnam at the time of payment.

Article 5. The management and the use

1. The fee-collecting agencies at the Inland Waterway Port Authority are the Inland Waterway Port Authorities as prescribed by to the Law on Inland Waterway Navigation. The fee-collecting agencies must make registration, declaration, and pay the fees to the State budget as prescribed by the Ministry of Finance in the Circular No. 28/2011/TT-BTC dated February 28th 2011 of the Ministry of Finance, guiding the implementation of a number of articles of the Law on Tax administration, guiding the Government's Decree No. 85/2007/NĐ-CP dated May 25th 2007 and the Government's Decree No. 106/2010/NĐ-CP dated October 28th 2010.

2. The fees at the Inland Waterway Port Authority are the State budget revenues. Fee-collecting agencies may extract from the money collected to defray the operation cost of the Port Authority as prescribed in Clause 3 this Article in the following proportion:

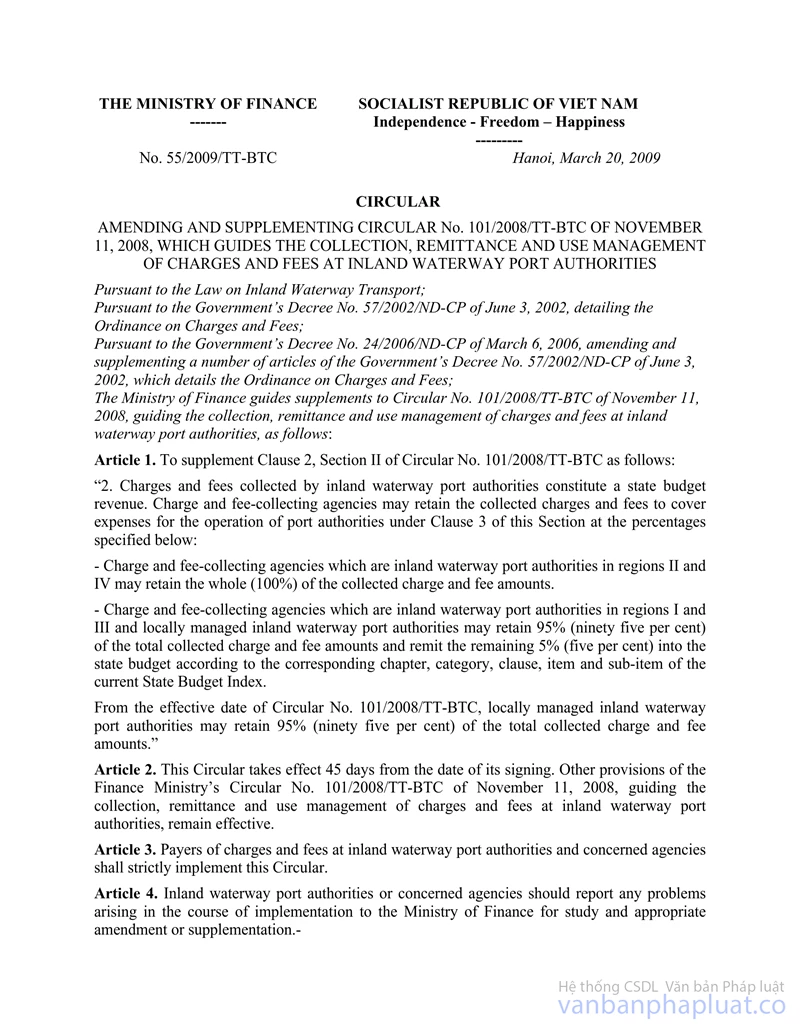

- The fee-collecting agencies being the Inland Waterway Port Authorities in area II and area IV may keep all (100%) the fee collected.

- The fee-collecting agencies being the Inland Waterway Port Authorities in area I and III, and the Inland Waterway Port Authorities under the management of local authorities may extract 95% of the fee collected before paying to the State budget, and pay 5% of the collected amount to the State budget in accordance with the current List of the State budget.

3. The spending of the Inland Waterway Port Authority:

a) Regular spending

- Spending on wages and salaries, benefits, and contributions according to wages and salaries under the current regime.

- Direct spending: stationery, office supplies, telephone, electricity, water, business trip allowance according to the current standards and norms.

- Spending on maintaining and repairing property, machinery and equipment.

- Special spending: spending on the labor protection or uniform; spending on buying receipts and stamps serving the fee collection, spending on the fuel serving the operation of the port authority, and other special spending.

- Other regular spending as prescribed by law.

b) Irregular spending

- Spending on office lease of representatives of the Inland Waterway Port Authority and teams of the Inland Waterway Port Authority (if any).

- Spending on rescuing humans, cargo, and vessels; doing jobs related to the prevention of environment pollution within the water of the inland port and wharf.

- Spending on enhancing professional skills.

- Spending on purchasing and repairing vehicles, devices, and the office building.

c) Spending on performing the State management of inland waterway navigation at the inland port or wharf in order to ensure the adherence to the law provisions on inland waterway safety and order, and prevent environment pollution according to the plan for financial autonomy given by competent authorities.

- In case the money extracted is not sufficient, the State budget shall support.

- If the actual collected amount is higher than the estimate, the fee-collecting agency may use it to give reward to its employees and managers. The total amount of the reward fund and benefit fun in a year of a person must not exceed 3 months of salaries. The residual amount shall be transferred to the succeeding year to cover the operation cost after reaching an agreement with a financial agency at the same level.

4. Annually, the fee-collecting agency must finalize the use of fee receipts and fee amount collected, the amount kept, the amount payable to the State budget, the amount paid and going to be paid to the State budget. Finalize the kept amount with the financial agency at the same level in accordance with current law provisions.

Article 5. Implementation organization

1. This Circular takes effect on December 10th 2012, and annuls the Circular No. 101/2008/TT-BTC dated November 11th 2008 and the Circular No. 55/2009/TT-BTC dated March 20th 2009, amending and supplementing the Circular No. 101/2008/TT-BTC dated November 11th 2008 of the Ministry of Finance, on the regime for collecting, paying, managing, and using fees at Inland Waterway Port Authorities.

2. Other contents related to the collection, payment, management, use, and announcement of fees not being guided in this Circular must comply with the Circular No. 63/2002/TT-BTC dated July 24th 2002 and the Circular No. 45/2006/TT-BTC dated May 25th 2006, amending and supplementing the Circular No. 63/2002/TT-BTC dated July 24th 2002 of the Ministry of Finance, guiding the implementation of law provisions on fees and charges; the Circular No. 28/2011/TT-BTC dated February 28th 2011 of the Ministry of Finance, guiding the implementation of a number of articles of the Law on Tax administration, guiding the implementation of the Government's Decree No. 85/2007/NĐ-CP dated May 25th 2007 and the Government's Decree No. 106/2010/NĐ-CP dated October 28th 2010.

3. The organizations and individuals that pay fees at the Inland Waterway Port Authorities and relevant agencies are responsible for the implementation of this Circular. Organizations and individuals are recommended to send feedbacks on the difficulties arising during the course of implementation to the Ministry of Finance for guidance./.

|

|

FOR THE

MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments