Circular No. 64/2010/TT-BTC amending and supplementing the Finance Ministry's đã được thay thế bởi Circular No. 60/2012/TT-BTC guiding the executing of tax liability applicable và được áp dụng kể từ ngày 27/05/2012.

Nội dung toàn văn Circular No. 64/2010/TT-BTC amending and supplementing the Finance Ministry's

|

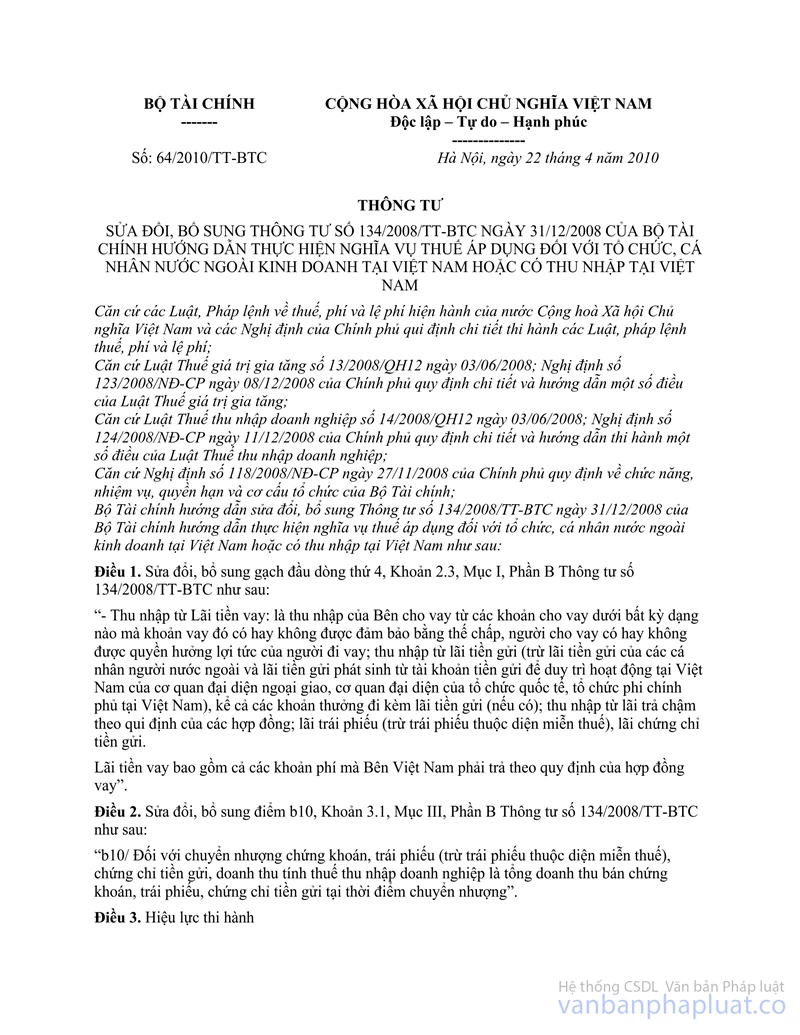

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 64/2010/TT-BTC |

Hanoi, April 22, 2010 |

CIRCULAR

AMENDING AND SUPPLEMENTING THE FINANCE MINISTRY'S CIRCULAR NO. 134/ 2008/TT-BTC OF DECEMBER 31, 2008, GUIDING THE PERFORMANCE OF THE TAX OBLIGATION BY FOREIGN ORGANIZATIONS AND INDIVIDUALS DOING BUSINESS OR EARNING INCOMES IN VIETNAM

THE MINISTRY OF FINANCE

Pursuant to the Socialist Republic of Vietnam's current laws and ordinances on taxes, fees and charges and the Government's decrees detailing laws and ordinances on taxes, fees and charges;

Pursuant to June 3, 2008 Law No. 13/2008/ QH12 on Value-Added Tax; and the Government's Decree No. 123/2008/ND-CP of December 8, 2008, detailing and guiding a number of articles of the Value-Added Tax Law;

Pursuant to June 3, 2008 Law No. 14/2008/ QH12 on Enterprise Income Tax; and the Government's Decree No. 124/2008/ND-CP of December 11, 2008, detailing and guiding a number of articles of the Law on Enterprise Income Tax;

Pursuant to the Government's Decree No. 118/2008/ND-CP of November 27, 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

The Ministry of Finance amends and supplements Circular No. 134/2008/TT-BTC of December 31, 2008, guiding the performance of the tax obligation by foreign organizations and individuals doing business or earning incomes in Vietnam as follows:

Article 1. To amend and supplement the forth em rule of Clause 2.3, Section I, Part B of Circular No. 134/2008/TT-BTC as follows:

"- Incomes from loan interests, which are a lender's incomes earned from loans provided in any form, whether or not those loans are guaranteed with mortgage and lenders are entitled to borrower rights over revenues; incomes from deposit interests (other than those of foreigners and those arising on deposit accounts to maintain operation in Vietnam of diplomatic missions and representative offices of international organizations and non-governmental organizations in Vietnam), including also bonuses accompanying deposit interests (if any); incomes from interests for deferred payment under contracts, of interests bonds (other than tax-free bonds) and deposit certificates.

Loan interests include fees payable by Vietnamese parties under loan contracts."

Article 2. To amend and supplement Point b10, Clause 3.1, Section III, Part B of Circular No. 134/2008ATT-BTC as follows:

"MO/ For the transfer of securities, bonds (other than tax-free bonds) and deposit certificates, turnover for enterprise income tax calculation is the total sales of those securities, bonds and deposit certificates at the time of transfer."

Article 3. Effect

This Circular takes effect 45 days from the date of its signing.

In the course of implementation, units and businesses should promptly report arising problems to the Ministry of Finance for settlement.-

|

|

FOR

THE MINISTER OF FINANCE |