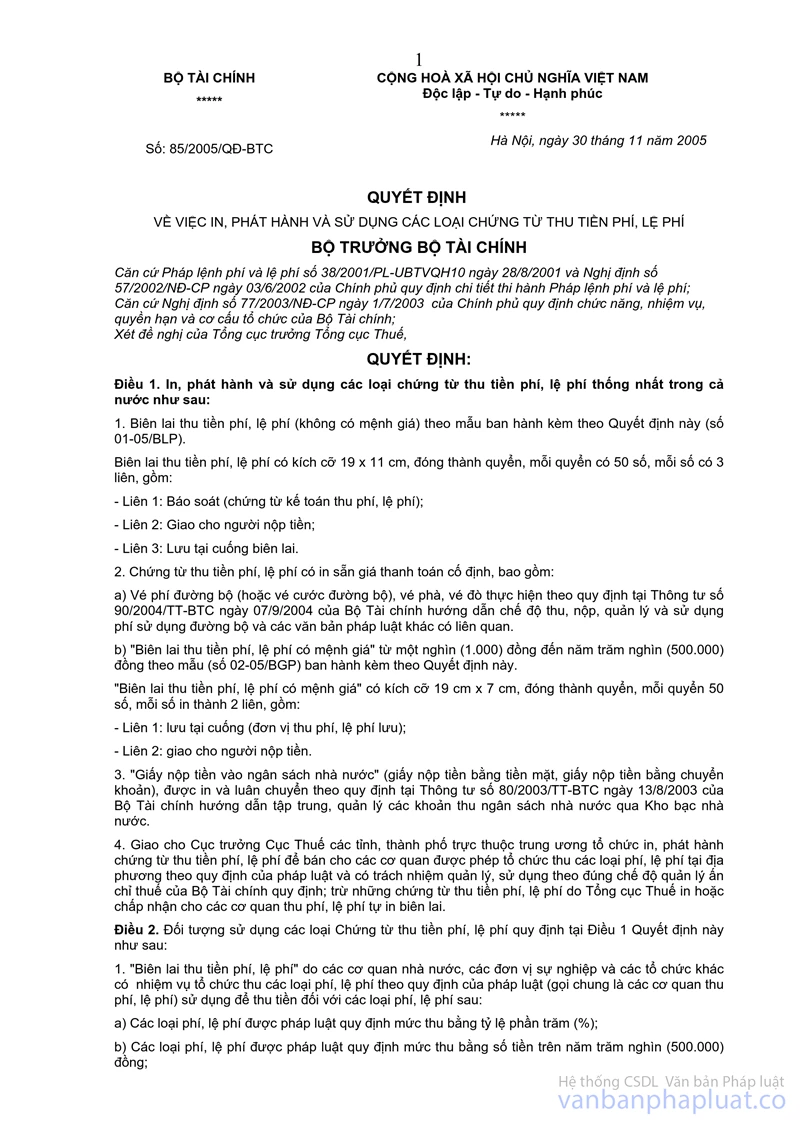

Nội dung toàn văn Decision No. 85/2005/QD-BTC, on printing, distribution and use of fee and charge receipts of all kinds, promulgated by the Ministry of Finance.

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 85/2005/QD-BTC |

Hanoi, November 30, 2005 |

DECISION

ON PRINTING, DISTRIBUTION AND USE OF FEE AND CHARGE RECEIPTS OF ALL KINDS

THE FINANCE MINISTER

Pursuant to Ordinance No.

38/2001/PL-UBTVQH10 of August 28, 2001 on Fees and Charges and the Government's

Decree No. 57/2002/ND-CP of June 3, 2002, detailing the implementation of the

Ordinance on Fees and Charges;

Pursuant to the Government's Decree No. 77/2003/ND-CP of July 1, 2003, defining

the functions, tasks, powers and organizational structure of the Finance

Ministry;

At the proposal of the General Director of the General Department of Taxation,

DECIDES:

Article 1.- To print, distribute and use fee and charge receipts of the following kinds in a unified manner throughout the country:

1. Fee and charge receipts (without par value), made according to the form enclosed herewith (No. 01-05/BLP).

These fee and charge receipts are of a size of 19 cm x 11 cm, and bound into books, each comprising 50 numbers. Each number is shown on triplicate originals, including:

- Original 1: To be used for checking (fee and charge collection accounting documents);

- Original 2: To be handed to the payer;

- Original 3: Not to be torn off from the receipt book.

2. Fee and charge receipts pre-printed with fixed rates, including:

a/ Road toll (or road freight) tickets, ferry or river-crossing boat fare tickets, which comply with the provisions of the Finance Ministry's Circular No. 90/2004/TT-BTC of September 7, 2004, guiding the regime of collection, remittance, management and use of road tolls and other relevant legal documents.

b/ Fee and charge receipts with a par value of between VND 1,000 and VND 500,000, made according to the set form (No. 02-05/BGP) enclosed herewith.

"Fee and charge receipts with par value" are of a size of 19 cm x 7 cm, bound into volumes, each comprising of 50 numbers. Each number is shown on duplicate originals, including:

- Original 1: Not to be torn off from the receipt book (kept as a record by the fee or charge-collecting unit);

- Original 2: To be handed to the payer.

3. "State budget remittance papers" (papers for remittances in cash and papers for remittances by account transfer), which are printed and circulated according to the provisions of the Finance Ministry's Circular No. 80/2003/TT-BTC of August 13, 2003, guiding the centralized remittance and management of state budget revenues through the State Treasury.

4. To assign the directors of the Provincial/Municipal Departments of Tax to organize the printing and distribution of fee and charge receipts to be sold to local agencies permitted to organize the collection of fees and charges of all kinds according to the provisions of law and to be responsible for managing and using such receipts in strict compliance with the Finance Ministry's regulations on management of tax forms, except for fee and charge receipts printed or permitted by the General Department of Taxation to be printed by fee and charge-collecting agencies themselves.

Article 2.- Users of fee and charge receipts of the kinds defined in Article 1 of this Decision shall be as follows:

1. "Fee and charge receipts" shall be used by state agencies, non-business units and other organizations tasked to organize the collection of fees and charges according to the provisions of law (hereinafter collectively referred to as fee and charge-collecting agencies) to collect the following fees and charges:

a/ Fees and charges, the rates of which are prescribed by law in percentage (%);

b/ Fees and charges, the rates of which are prescribed by law in specific amounts of over VND 500,000;

c/ Particular fees and charges in international transactions, and those with receipts printed by collecting agencies themselves after getting approval of the Finance Ministry (the General Department of Taxation). Procedures for collecting agencies to register for printing fee and charge receipts are specified in the Appendix to this Decision.

2. Road toll (or freight) tickets, ferry or river-crossing boat fare tickets shall be used by organizations or individuals to collect road tolls or ferry or river-crossing boat fares according to the relevant provisions of law.

3. "Fee and charge receipts with par value" shall be used by agencies permitted to collect fees and/or charges, the rates of which are prescribed by law in specific amounts being their par values of between VND 1,000 and VND 500,000.

4. "State budget remittance papers" (papers for remittances in cash or papers for remittances by account transfer) shall be used in the following cases:

a/ Fee and charge payers use "state budget remittance papers" to remit fee and charge amounts into the state budget at the State Treasury;

b/ The State Treasury uses "state budget remittance papers" to collect fee and charge amounts into the state budget according to the provisions of law.

Article 3.- Fee and charge receipts defined in Article 1 of this Decision shall be managed and used according to the Finance Minister's Decision No. 30/2001/QD-BTC of April 13, 2001, promulgating the regime of printing, distribution, management and use of tax receipts. Particularly, "fee and charge receipts with par value" shall also be managed and used according to the following provisions:

1. Fee and charge-collecting agencies, before circulating "fee and charge receipts with par value" for use, must affix their seals on the upper right corner of original 2 of each receipt (to be handed to the payer). Fee and charge collectors, when collecting money, must sign and clearly write their full names in original 2 of fee and charge receipts with par value.

2. Organizations and individuals that pay a fee or a charge of between VND 1,000 and VND 500,000 shall be issued a "fee and charge receipt with par value" according to the provisions of this Decision.

a/ "Fee and charge receipts with par value" distributed by Provincial/Municipal Tax Departments of, affixed with seals of fee and charge-collecting agencies and completely filled in compliance with the provisions of this Decision shall be valid for payment, financial accounting and settlement.

b/ "Fee and charge receipts with par value" not distributed by Provincial/Municipal Tax Departments, not affixed with seals of fee and charge-collecting agencies and not containing signatures (with full names) of fee or charge collectors shall neither be valid for payment nor eligible for financial accounting and settlement.

Article 4.- This Decision takes effect 15 days after its publication in "CONG BAO"; all fee and charge receipts not specified in this Decision shall be annulled. Quantities of fee and charge receipts and tickets already printed according to the previously set forms may continue to be used up till the end of December 31, 2006. As from January 1, 2007, the printing, distribution and use of fee and charge receipts shall comply with this Decision.

Article 5.- The director of the Office of the Finance Ministry, the General Director of the General Department of Taxation, the General Director of the State Treasury, the directors of the Provincial/Municipal Tax Departments, organizations and individuals that manage and use fee and charge receipts shall have to implement this Decision.

|

|

FOR THE MINISTER OF

FINANCE |

|

District Tax

Department........ FEE AND CHARGE RECEIPT(Original 1: To be used for checking) Name of payer:......................................................................................................................... Address:.................................................................................................................................... Payment reason (name of fee or charge):................................................................................. Amount:..................................................................................................................................... (In words): ................................................................................................................................. ................................................................................................................................................... Payment mode:.......................................................................................................................... ...................................................................................................................................................

|

|||||

|

District Tax

Department........

FEE AND CHARGE RECEIPT(Original 2: To be handed to payer) Name of payer:........................................................................................................................... Address:..................................................................................................................................... Payment reason (name of fee or charge):.................................................................................. Amount:...................................................................................................................................... (In words): .................................................................................................................................. ..................................................................................................................................................... Payment mode:........................................................................................................................... .....................................................................................................................................................

|

|

District Tax

Department........

FEE AND CHARGE RECEIPT(Original 3: Not to be torn off from the receipt book) Name of payer:........................................................................................................................... Address:..................................................................................................................................... Payment reason (name of fee or charge):.................................................................................. Amount:....................................................................................................................................... (In words): ................................................................................................................................... ..................................................................................................................................................... Payment mode:............................................................................................................................ ….................................................................................................................................................

|

GENERAL DEPARTMENT

Form No. 02-05/BGP FEE

AND CHARGE RECEIPT Series: AA/ - Amount: ............................. - In words:............................

Original 1: To be kept as a record |

TCT * TCT * TCT * TCT |

GENERAL DEPARTMENT

SOCIALIST REPUBLIC OF

VIETNAM Form No. 02-05/BGP

FEE AND CHARGE RECEIPT WITH PAR VALUE- Amount: (Pre-printed par value in figures) - In words: (Pre-printed par value in words)

Original 2: To be handed to payer |

For example:

|

GENERAL DEPARTMENT

Form No. 02-05/BGP FEE

AND CHARGE RECEIPT Series: AA/ - Amount: VND 100,000 - In words: One hundred thousand dong only

Original 1: To be kept as a record |

TCT * TCT * TCT * TCT |

GENERAL DEPARTMENT

SOCIALIST REPUBLIC OF

VIETNAM Form No. 02-05/BGP

FEE AND CHARGE RECEIPT WITH PAR VALUE- Amount: VND 100,000 - In words: One hundred thousand dong only

Original 2: To be handed to payer

|

PROCEDURES

OF REGISTRATION FOR USE OF SELF-PRINTED

FEE AND CHARGE RECEIPTS

(Promulgated together with the Finance Minister's Decision No.

85/2005/QD-BTC of November 30, 2005)

1. Subjects eligible for registration for printing fee and charge receipts (called receipts for short) by themselves are agencies performing the task of collecting particular fees and charges in international transactions which require the use of bilingual receipts (printed in Vietnamese and a foreign language), and other fee and charge-collecting agencies defined by law.

2. Agencies which print, distribute and use fee and charge receipts shall have the following responsibilities:

a/ To print receipts in strict compliance with the following provisions:

- Receipts must be printed according to the forms already approved and registered with competent tax authorities. Heads of fee and charge-collecting agencies must sign for certification in the forms of receipts ordered to be printed.

- For receipt printing, there must be printing contracts with printing units, clearly stating quantities, signs and serial numbers of receipts ordered to be printed. After each printing batch or upon expiration of each printing contract, such contract must be liquidated by the printing-ordering party and the printing party. It is prohibited to order the printing of receipts without contract.

- Agencies which themselves order the printing of receipts may select appropriate and convenient printing houses on the list of printing houses registered with the General Department of Taxation.

b/ Distribution of receipts:

- Five days after registering for circulation of self-printed receipts, fee and charge-collecting agencies must send written notices on distribution (enclosed with the receipt form) to their managing tax authorities and post up such notices at their head offices where fees and charges are collected or transactions are conducted. A receipt distribution notice must clearly specify the receipt form, kind, presentation, size, pattern, logo, structural specifications and valid term of the receipt form.

- When changing receipt forms, fee and charge-collecting agencies must publicly notify the kind, sign, series of receipts, and date of expiration of their validity to tax authorities and post up the receipt form and notices on receipts which are no longer valid for use at their head offices where fees and charges are collected or transactions are conducted, make payment, settlement and return unused quantities of receipts to their managing tax offices.

3. Procedures of registration for use of self-printed receipts:

3.1. Procedures of registration of self-printed receipt forms:

Fee and charge collecting agencies shall register for use of self-printed receipts with the General Department of Taxation according to the form enclosed herewith. Procedures of registration of self-printed receipt forms shall be as follows:

a/ A written request for registration for use of self-printed receipts (made according to the form enclosed herewith).

b/ The receipt form designed by the collecting agency. This receipt form must contain all the following details: Name of the collecting agency, its address and tax identification number, sign and serial number of receipt; name, address and tax identification number of fee or charge-paying organization or individual; total amount paid (in case of various kinds of fees and charges), printed according to document No., dated..., of the tax authority, and name of the receipt-printing house; specifications or logo of the collecting unit may be presented on the receipt form. For bilingual receipts, Vietnamese words shall be printed above foreign-language words.

c/ Copy(ies) (not required to be notarized) of the legal document(s), defining the function, tasks and powers to perform services or state management jobs for which fees or charges are collected.

Tax authority, within ten (10) working days after receiving dossiers for registration for use of self-printed receipts of fee and charge-collecting agencies, shall verify such dossiers and compare them with current fee and charge law before carrying out procedures for approving the registration of self-printed receipt forms. In case of refusal to approve the registration of a self-printed receipt form, they must reply in writing within seven (07) working days. When changing their self-printed receipt forms, fee and charge-collecting agencies must make re-registration.

3.2. Registration for circulation of self-printed receipts

For circulation, forms of receipts printed by fee and charge-collecting agencies must be registered with tax authorities where such receipts have been registered for use, regarding receipt signs, quantity and serial numbers (from number ... to number...). Tax authorities shall base themselves on receipt use demands of such agencies to determine the quantity of self-printed receipts which may be registered for circulation and use in each period of between one month and three months. Before the printing of receipts of a new batch, the use of previously printed receipts must be reported and the new printing batch must be registered with tax offices regarding receipt signs, quantity and serial numbers.

The managing tax authorities shall open a book for monitoring the registration for circulation of self-printed receipt forms by a fee and charge-collecting agency and give one copy of such book to this agency, such a book shall be made according to the form set in the Finance Ministry's Circular No. 120/2002/TT-BTC of December 30, 2002, guiding the implementation of the Government's Decree No. 89/2002/ND-CP of November 7, 2002 on printing, distribution, use and management of invoices.

FORM

OF WRITTEN REQUEST FOR REGISTRATION FOR

SELF-PRINTING OF FEE AND CHARGE RECEIPTS

(Promulgated together with the Finance Minister's Decision No.

85/2005/QD-BTC of November 30, 2005)

|

Unit:...... |

SOCIALIST REPUBLIC OF VIETNAM |

|

On registration for

use of |

Date........................ |

To: The General Department of Taxation

1. Name of agency registering for self-printing of receipts:..............................

- Tax identification number.....................................Telephone number.................

- Transaction Contact..............................................................................................

- For collection of fee or charge:............................................................................

- Place of collection of fee or charge:....................................................................

2. Name of head of fee and charge-collecting agency:..........................................

- People's identity card No..............., granted on day....month.......year....., in......

- Telephone number:..............................................................................................

Pursuant to Circular/Decision No......dated.........issued by............, stipulating the regime of collection, remittance, management and use of fees and charges..............;

After thoroughly studying the Finance Minister's Decision No... /2005/QD-BTC of dated.......... 2005 on printing, distribution and use of fee and charge receipts;

To suit the branch's management particularities as well as specific fees or charges to be collected by our agency, and satisfy demands of fee and charge-paying organizations and individuals, we would like to request the General Department of Taxation to permit us to print and use fee and charge receipts, including the following kinds: (specifying each kind, number of originals of each kind, use purpose of each original). This quantity of receipts will be registered for use in ...........................

We hereby undertake that our declarations are accurate. If the General Department of Taxation permits us to use self-printed fee and charge receipts, we will print, distribute, manage and use such receipts in strict compliance with the State's and the Finance Ministry's current regulations. We shall take responsibility before law for any mistakes and violations.

|

|

Head of the fee and charge-collecting agency (Signature and stamp) |