Law No. 08/2003/QH11 of June 17, 2003, amending and supplementing a number of articles of the law on special consumption tax đã được thay thế bởi Law No. 27/2008/QH12 of November 14, 2008, on Excise Tax và được áp dụng kể từ ngày 01/04/2009.

Nội dung toàn văn Law No. 08/2003/QH11 of June 17, 2003, amending and supplementing a number of articles of the law on special consumption tax

|

THE NATIONAL ASSEMBLY |

SOCIALIST REPUBLIC OF VIET NAM |

|

No: 08/2003/QH11 |

Hanoi, June 17, 2003 |

LAW

AMENDING AND SUPPLEMENTING A NUMBER OF ARTICLES OF THE LAW ON SPECIAL

CONSUMPTION TAX

(No. 08/2003/QH11 of

June 17, 2003)

Pursuant to the 1992 Constitution of

the Socialist Republic of Vietnam, which was amended and supplemented under

Resolution No. 51/2001/NQ-QH10 bổ sung điều của Hiến pháp nước cộng hoà xã hội chủ nghĩa Việt Nam năm 1992">51/2001/QH10 of December 25, 2001 of the 10th session of the Xth

National Assembly;

This Law amends and supplements a number of articles of the May 20, 1998 Law

on Special Consumption Tax.

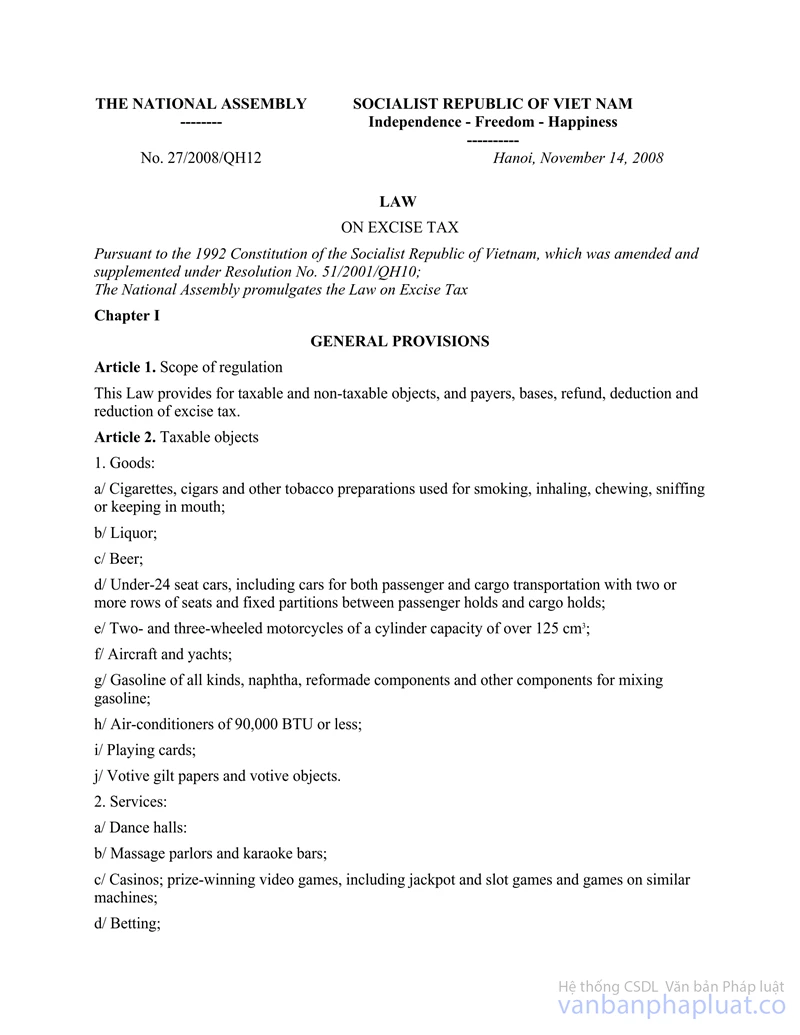

Article 1.- To amend and supplement a number of articles of the Law on Special Consumption Tax:

1. Article 1 is amended and supplemented as follows:

"Article 1.- Taxable objects

The following goods and services shall be subject to the special consumption tax:

1. Goods:

a/ Cigarettes, cigars;

b/ Liquors;

c/ Beers;

d/ Under-24-seat cars;

e/ Gasoline of various kinds, naphtha, reformade components and other components for mixing gasoline;

f/ Air conditioners of a capacity of 90,000 BTU or less;

g/ Playing cards;

h/ Votive gilt paper, votive objects;

2. Services:

a/ Dancing halls, massage parlors, karaoke bars;

b/ Casinos, jackpot games;

c/ Entertainment with bet tickets;

d/ Golf business: sale of golf club membership cards, golf playing tickets;

e/ Lottery business."

2. Clause 6 of Article 6 is amended and supplemented as follows:

"6. For home-made liquors and beers, casinos, jackpot games and golf business, the special consumption tax calculation prices shall be specified by the Government.

The special consumption tax calculation prices of goods and services defined in this Article shall also include surcharges enjoyed by business establishments.

In cases where the tax payers have sale and purchase turnovers in foreign currencies, they must convert such foreign currency amounts into Vietnam dong at the exchange rates announced by Vietnam State Bank at the time such turnovers are generated to determine the tax calculation prices."

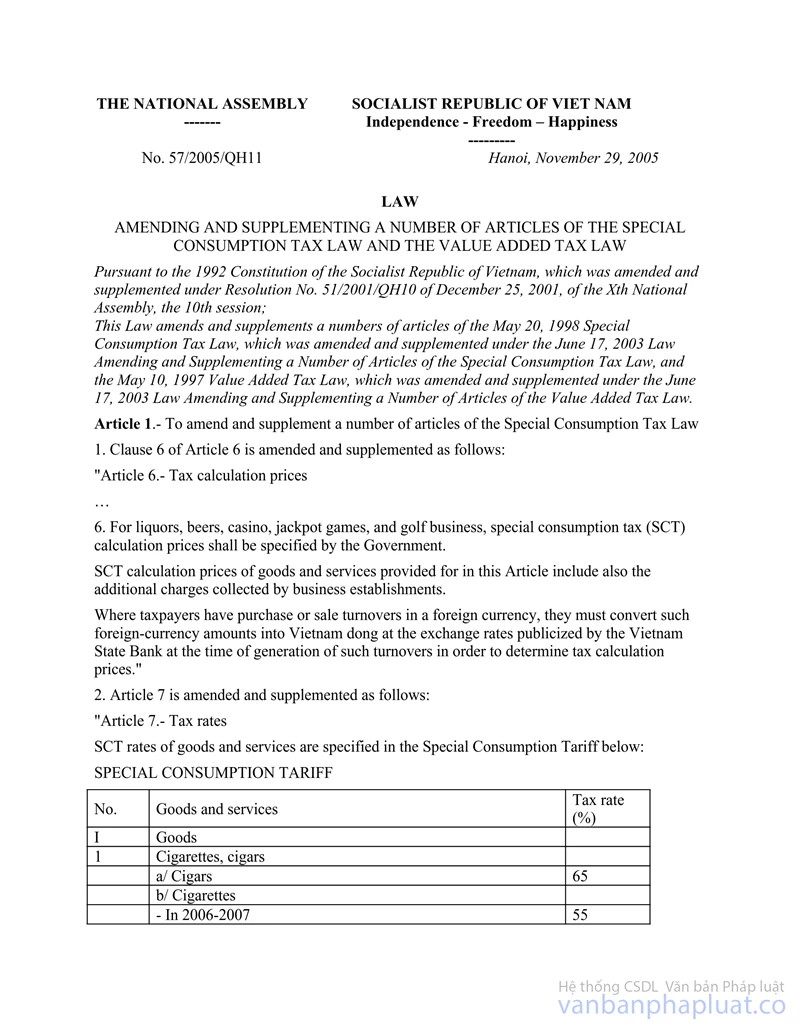

3. Article 7 is amended and supplemented as follows:

"Article 7.- Tax rates

The special consumption tax rates for goods and services are specified in the following special consumption tax table:

The special consumption tax table

|

Ordinal number |

Goods and services |

Tax rates (%) |

|

I. |

Goods |

|

|

1. |

Cigarettes, cigars |

|

|

|

a/ Filter cigarettes produced mainly from imported raw materials, cigars |

65 |

|

|

b/ Filter cigarettes produced mainly from domestic raw materials |

45 |

|

|

c/ Non-filter cigarettes |

25 |

|

2. |

Liquors |

|

|

|

a/ Of 40% proof or higher |

75 |

|

|

b/ Of 20% to under 40% proof |

30 |

|

|

c/ Of under 20% proof, fruitwines |

20 |

|

|

d/ Medicated liquors |

15 |

|

3. |

Beers |

|

|

|

a/ Bottled beers, canned beers, fresh beers |

75 |

|

|

b/ Draught beers |

30 |

|

4. |

Cars |

|

|

|

a/ Cars of 5 seats or less |

80 |

|

|

b/ Cars of between 6 and 15 seats |

50 |

|

|

c/ Cars of between 16 and under 24 seats |

25 |

|

5. |

Gasoline of various kinds, naphtha, reformade components and other components for mixing gasoline |

10 |

|

6. |

Air conditioners of a capacity of 90,000 BTU or less |

15 |

|

7. |

Playing cards |

40 |

|

8. |

Votive gilt paper, votive objects |

70 |

|

II. |

Services |

|

|

1. |

Dancing halls, message parlors, karaoke bars |

30 |

|

2. |

Casinos, jackpot games |

25 |

|

3. |

Entertainment with bet tickets |

25 |

|

4 |

Golf business: sale of golf club membership cards, golf playing tickets |

10 |

|

5. |

Lottery business |

15 |

4. Clause 1 of Article 11 is amended and supplemented as follows:

"1. Establishments engaged in the production of goods and/or provision of services, which are subject to the special consumption tax, shall have to pay special consumption tax into the State budget at the places where they conduct their production and/or business activities.

The deadline for monthly tax payment shall be the 25th day of the subsequent month;"

5. To add the following Clause 4 to Article 11:

"4. The Government shall specify the procedures for tax declaration and payment, suitable to the requirements of administrative reform, raising business establishments sense of responsibility before law, and at the same time enhancing the work of examination, inspection and handling of law violations by tax agencies in order to ensure the strict and effective management of tax collection."

6. Clause 2 of Article 14 is amended and supplemented as follows:

"2. To notify the tax payers prescribed by the Government of the payable tax amounts, to urge the tax payers to pay tax on time; if past the tax payment time limits, the tax payers still fail to pay tax, to notify them of the payable tax amounts and fines for late tax payment according to the provisions in Clause 2 and Clause 3, Article 17 of this Law; if the tax payers still fail to fully pay the tax amounts and fines stated in the notices, the handling measures prescribed in Clause 4, Article 17 of this Law may be applied so as to ensure the full collection of tax and fines; if the above-mentioned handling measures have been applied, but the tax payers still fail to fully pay the amounts of tax and fines, the dossiers of the cases shall be transferred to the competent State agencies for handling according to law provisions."

7. To add the following Point e to Clause 1 of Article 15:

"e/ Declaring the selling prices for use as basis for determining the special consumption tax calculation prices as 10% lower than the market selling prices of such goods and/or services."

8. Article 16 is amended and supplemented as follows:

"Article 16.- Cases eligible for consideration for special consumption tax reduction and/or exemption

1. Establishments producing goods subject to the special consumption tax, which meet with difficulties due to natural disasters, enemy sabotage and unexpected accidents, shall be considered for tax reduction or exemption.

2. Establishments engaged in the manufacture and/or assembly of automobiles shall enjoy a reduction of the tax rates defined in the Special Consumption Tax Table prescribed in Article 7 of this Law as follows:

- A reduction of 70% for 2004.

- A reduction of 50% for 2005.

- A reduction of 30% for 2006.

- From 2007 on, tax shall be paid at the prescribed rates.

The Government shall specify the tax reduction and exemption prescribed in this Article."

Article 2.- This Law takes effect as from January 1, 2004.

Article 3.- The Government shall detail and guide the implementation of this Law.

This Law was passed by the XIth National Assembly of the Socialist Republic of Vietnam on June 17, 2003 at its 3rd session.

|

|

CHAIRMAN OF THE NATIONAL ASSEMBLY |