Law No. 05/1998/QH10 of May 20, 1998, on Special Consumption Tax. đã được thay thế bởi Law No. 27/2008/QH12 of November 14, 2008, on Excise Tax và được áp dụng kể từ ngày 01/04/2009.

Nội dung toàn văn Law No. 05/1998/QH10 of May 20, 1998, on Special Consumption Tax.

|

THE NATIONAL ASSEMPLY --------- |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 05/1998/QH10 |

Hanoi, May 20, 1998 |

THE LAW

ON SPECIAL CONSUMPTION TAX

To direct the production and

social consumption, to rationally regulate the consumers' incomes for the State

budget and to enhance the management over production of and trading in a number

of goods and services;

Pursuant to the 1992 Constitution of the Socialist Republic of Vietnam;

This Law prescribes the special consumption tax,

Chapter I

GENERAL PROVISIONS

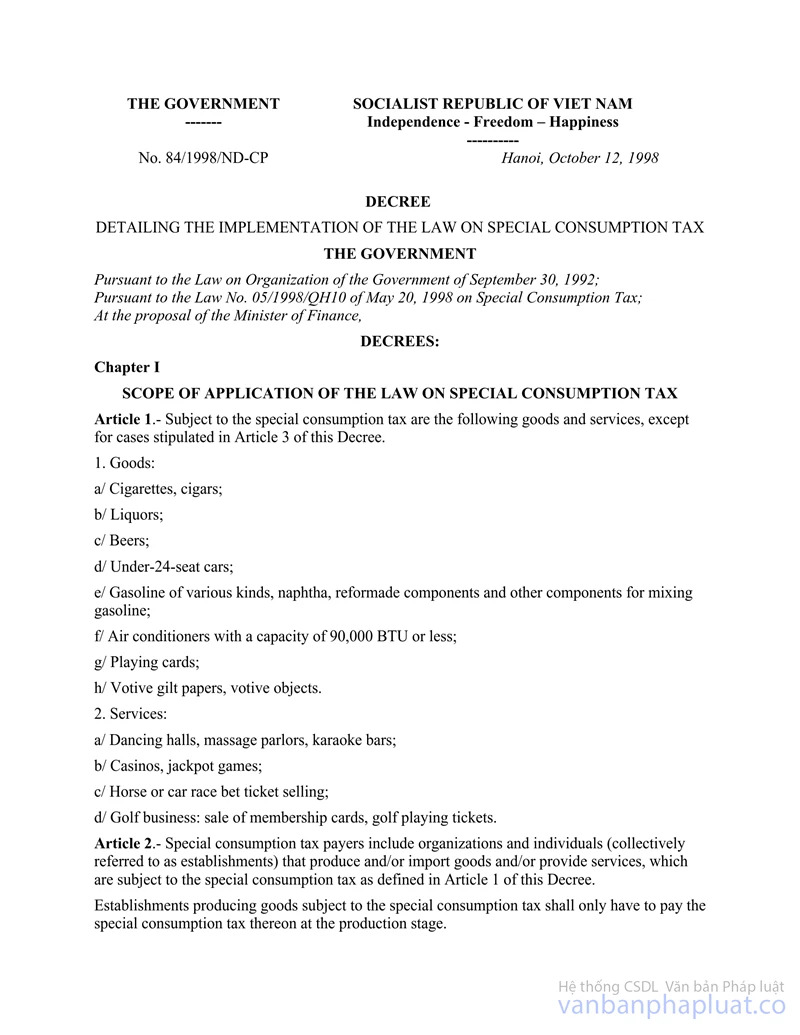

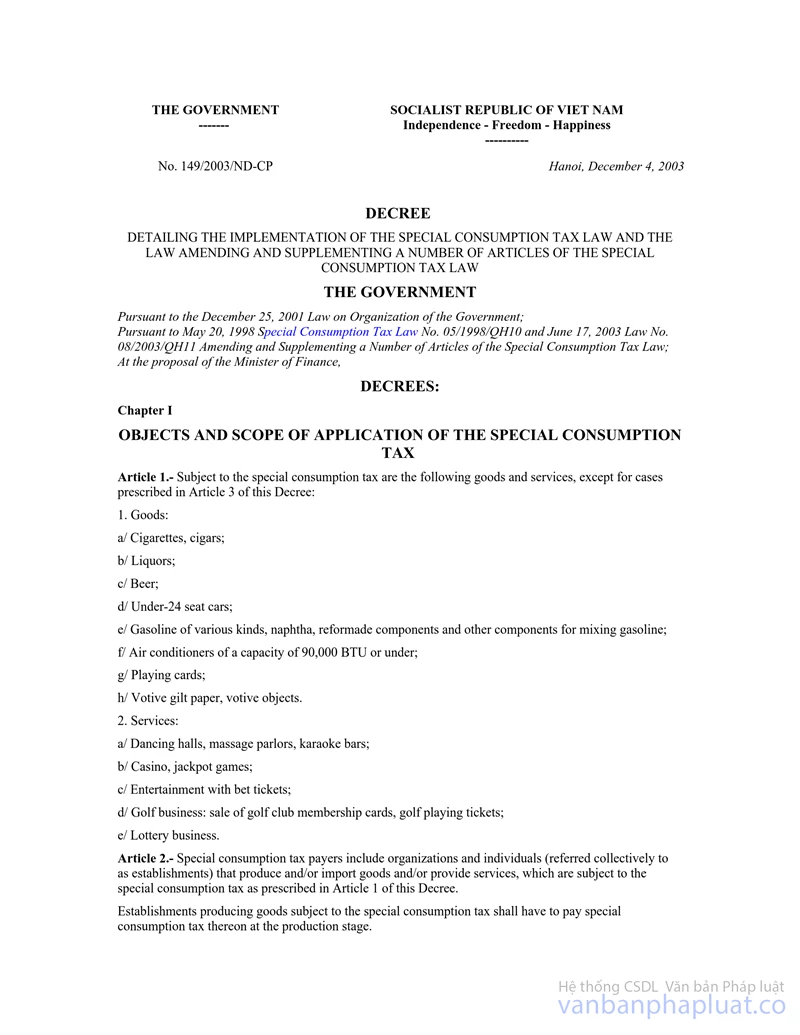

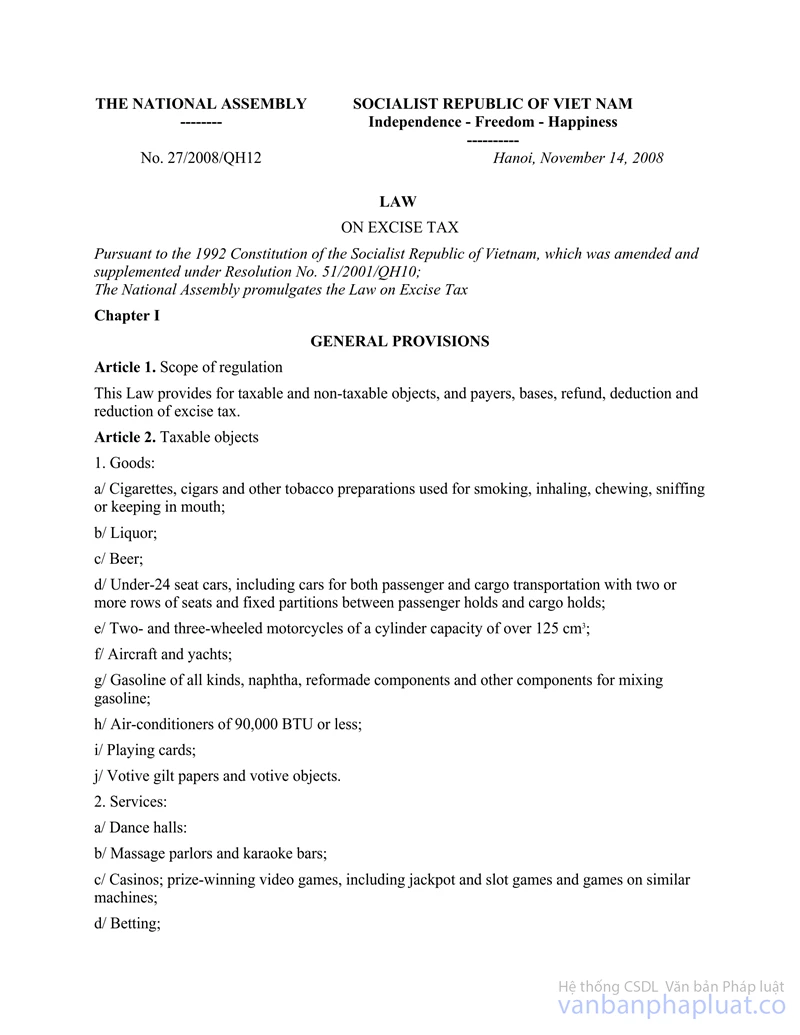

Article 1.- Taxable objects:

The following goods and services shall be subject to the special consumption tax:

1. Goods:

a) Cigarettes, cigars;

b) Liquors;

c) Beers;

d) Under-24-seat cars;

e) Gasoline of various kinds, naphtha, reformate components and other compounds for mixing gasoline;

f) Air conditioners with a capacity of 90,000 BTU or less;

g) Playing cards;

h) Votive gilt paper, votive objects.

2. Services:

a) Dancing halls, massage parlors, karaoke bar;

b) Casinos, jackpot games;

c) Horse race or car race bet tickets;

d) Golf business: sale of membership cards, golf playing tickets.

Article 2.- Tax payers

Organizations and individuals (hereafter collectively referred to as establishments) that produce and/or import goods and provide services, which are subject to the special consumption tax, shall be special consumption tax payers.

Article 3.- Goods not subject to the special consumption tax

Goods defined in Clause 1, Article 1 of this Law shall not be subject to the special consumption tax in the following cases:

1. Goods which are directly exported, sold or consigned to export business establishments for export by production or processing establishments;

2. Goods which are imported in the following cases:

a) Humanitarian aid or non-refundable aid goods; gifts for State agencies, political organizations, socio-political organizations, social organizations, socio-professional organizations, people's armed forces units; belongings of foreign organizations and/or individuals that enjoy diplomatic immunities; personal effects within the duty-free luggage limit;

b) Goods which are transshipped, transited or transported through Vietnam's border;

c) Goods temporarily imported for re-export, or temporarily exported for re-import during the tax-free period;

d) Goods imported for duty-free sale under the prescribed regulations.

Article 4.- Obligations and responsibilities for implementing the Law on Special Consumption Tax

1. Those who are liable to the special consumption tax shall have obligation to pay tax fully and within the time limit prescribed by this Law.

2. The tax authorities shall, within their respective tasks and powers, have to strictly comply with the provisions of this Law.

3. State agencies, political organizations, socio-political organizations, social organizations, socio-professional organizations and people's armed forces units shall, within their respective functions and powers, have to supervise the observance of this Law and coordinate with the tax authorities in enforcing this Law.

4. Vietnamese citizens shall have to help the tax authorities and tax officials to enforce this Law.

Chapter II

THE TAX CALCULATION BASES AND TAX RATES

Article 5.- The tax calculation bases

The bases for calculating the special consumption tax are the tax calculation prices of taxable goods or services and tax rates.

Article 6.- Tax calculation prices

1. For goods produced in the country, they shall be the sale prices set by the production establishments at the production places, not yet including the special consumption tax.

2. For imported goods, they shall be the import tax calculation price plus (+) the import tax.

3. For processed goods, they shall be the tax calculation prices of the produced goods of the same or equivalent types at the time of goods delivery.

4. For services, they shall be service provision prices, not yet including the special consumption tax.

5. For goods or services used for purposes of exchange or internal consumption, gift or donation, they shall be the special consumption tax calculation prices of goods and services of the same or equivalent type at the time such activities are conducted.

6. For liquors made in the country, casinos, jackpot games and golf business, the special consumption tax calculation prices shall be specified by the Government.

The special consumption tax calculation prices of goods and/or services defined in this Article shall also include surcharges enjoyed by the establishments.

In cases where the production and business establishments purchase and sell goods and/or services in foreign currency(ies), they must convert such foreign currency(ies) into Vietnam Dong at the exchange rate(s) announced by the State Bank of Vietnam at the time such turnovers are generated to determine the special consumption tax calculation prices.

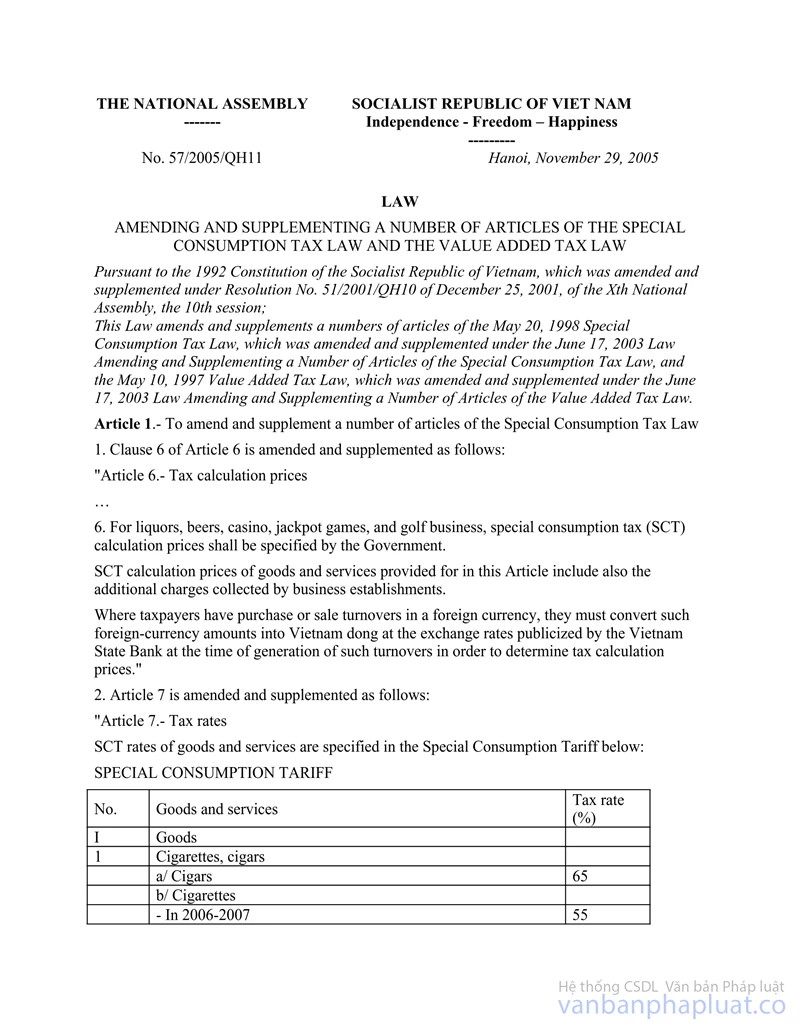

Article 7.- Tax rates

The special consumption tax rates for goods and services are specified in the following special consumption tax table.

THE SPECIAL CONSUMPTION TAX TABLE

|

No. |

Goods and services |

Tax rates (%) |

|

I. |

Goods |

|

|

1. |

Cigarettes, cigars |

|

|

|

a) Filter cigarettes produced mainly from imported raw materials, cigars |

65 |

|

|

b) Filter cigarettes produced mainly from domestic raw materials |

45 |

|

|

c) Non-filter cigarettes |

25 |

|

2. |

Liquors |

|

|

|

a) Of over 40% proof. |

70 |

|

|

b) Of from 30% to 40% proof. |

55 |

|

|

c) Of from 20 % to under 30 % proof. |

25 |

|

|

d) Of under 20 % proof, including fruitwines |

20 |

|

|

e) Medicated liquors |

15 |

|

3. |

Beers |

|

|

|

a) Bottled beer, fresh beer |

75 |

|

|

b) Canned beer |

65 |

|

|

c) Draught beer |

50 |

|

4 |

Automobiles |

|

|

|

a) Cars of 5 seats or less |

100 |

|

|

b) Cars of from 6 to 15 seats |

60 |

|

|

c) Cars of from 16 to under 24 seats |

30 |

|

5 |

Gasoline of various kinds, naphtha, reformate components and other compounds for mixing gasoline |

15 |

|

6 |

Air conditioners of a capacity of 90,000 BTU or less |

20 |

|

7 |

Playing cards |

30 |

|

8 |

Votive gilt paper, votive objects |

60 |

|

II |

Services |

|

|

1 |

Dancing halls, massage parlors, karaoke bars |

20 |

|

2 |

Casinos, jackpot games |

25 |

|

3 |

Horse race and car race bet tickets |

20 |

|

4 |

Golf business: sale of membership cards, golf playing tickets |

20 |

In case of necessity, the National Assembly Standing Committee shall make amendments and supplements to the list of goods and services subject to the special consumption tax and/or the special consumption tax rates, then propose them to the National Assembly for adoption at its nearest session.

Chapter III

TAX REGISTRATION, DECLARATION, PAYMENT AND FINAL SETTLEMENT

Article 8.- Tax registration

An establishment which produces goods or provides services subject to special consumption tax shall have to register the tax payment with the tax authority of the locality where it conducts production or service activities under the regulations on tax registration and guidance of the tax authority.

The time limit for tax registration is ten days from the date it is granted the business registration certificate.

In case of a merger, amalgamation, division, splitting, dissolution, bankruptcy or change in its business line or its business operation is terminated, the production or business establishment shall have to make a declaration thereof with the tax authority within five days before such change occurs.

Article 9.- Registration for use of trademarks, invoices and vouchers

1. An establishment which produces goods items subject to the special consumption tax and uses the trademarks thereof shall have to register such trademarks with the tax authority of the locality where it conducts production or business activities within five days from the date it uses such trademarks. When changing the trademarks, the establishment shall have to notify the tax authority thereof within five days from the date of changing such trademarks.

2. The purchase and sale of goods and services as well as the transportation of goods, which are subject to the special consumption tax, must have invoices and vouchers as prescribed by law.

Article 10.- Tax declaration

1. An establishment that produces goods and/or provides services which are subject to the special consumption tax, shall have to make monthly special consumption tax declaration and submit it to the concerned tax authority within the first ten days of the following month. For a production or business establishment with a large special consumption tax amount, the special consumption tax declaration shall be made once every five days or every ten days in accordance with the regulations of the tax authority.

Even if there is no payable special consumption tax in the month, a production or business establishment shall still have to make its tax declaration and submit it to the tax authority.

2. A goods importing establishment shall have to make a special consumption tax declaration and submit it upon each importation together with the import tax declaration with the import tax collecting agency.

3. An establishment that produces goods items subject to the special consumption tax from raw materials for which the special consumption tax has already been paid, when making special consumption tax declaration for the production process, shall be entitled to deduct the special consumption tax amount already paid for such materials if it can produce valid vouchers.

4. An establishment that produces and/or deals in different kinds of goods and/or services, which are subject to the special consumption tax with different tax rates, shall have to declare the special consumption tax according to the tax rate applicable to each kind of goods or service; if such establishment fails to determine payable tax amount according to each tax rate, it shall have to calculate and pay tax at the highest rate applicable to a certain kind of goods or service it produces and/or deals in.

The establishments producing or importing goods and/or providing services which are subject to the special consumption tax, shall have to fully declare the tax according to the set form and take responsibility for the accuracy of their declarations.

The Ministry of Finance shall set the tax declaration form and guide the declaration.

Article 11.- Tax payment

The special consumption tax shall be paid into the State budget according to the following regulations:

1. Establishments producing goods and/or providing services, which are subject to the special consumption tax, shall have to pay the special consumption tax into the State budget at their places of production or business according to the tax payment notices issued by the tax authorities.

The deadline for tax payment for a month as stated in a tax notice shall not be later than the 20th of the following month;

2. Establishments importing goods subject to the special consumption tax shall have to pay the special consumption tax upon each importation.

The deadline for issuing a notice and the deadline for payment of special consumption tax on imported goods shall be the deadlines for the import tax notice and payment;

3. The special consumption tax shall be paid into the State budget in Vietnam Dong.

Article 12.- Tax final settlement

Establishments producing goods and/or providing services, which are subject to the special consumption tax, shall have to make the annual final settlement of special consumption tax with the tax authorities. A year of tax final settlement shall be the solar calendar year. Within 60 days from the end of a year, the establishments shall have to submit tax final settlement reports to the tax authorities and fully pay the outstanding tax amounts to the State budget within 10 days from the date of submitting the final settlement reports; in case of overpayment, such overpaid amounts shall be deducted from the payable tax amount of the following period.

In case of a merger, amalgamation, division, splitting, dissolution, bankruptcy or change in its business line, an establishment shall have to make the tax final settlement and submit the report thereon to the tax authority within 45 days from the date of issuance of the decision on such merger, amalgamation, division, splitting, dissolution or bankruptcy, and fully pay the outstanding tax amount into the State budget within ten days from the date of submitting the final settlement report; in case of overpayment, the overpaid amount shall be deducted from the payable tax amount of the following period or reimbursed in accordance with Article 13 of this Law.

Article 13.- Tax reimbursement

An establishment producing and/or importing goods subject to the special consumption tax shall have its paid special consumption tax reimbursed in the following cases where:

1. Goods are temporarily imported for re-export;

2. Goods are raw materials imported for the production or processing of export goods;

3. It has an overpaid tax amount in the tax final settlement upon a merger, amalgamation, division, splitting, dissolution or bankruptcy;

4. It has a tax reimbursement decision issued by the competent agency as prescribed by law.

The Ministry of Finance shall define the procedures and competence for tax reimbursement as prescribed in this Article.

Article 14.- Duties, powers and responsibilities of the tax authorities

The tax authority shall have the following duties, powers and responsibilities:

1. To guide the tax payers in implementing the regulations on tax registration, declaration and payment as prescribed by this Law;

2. To send the tax payers notices on the payable tax amounts and the tax payment deadlines as prescribed; to issue another notice on the payable tax amount and fine for late tax payment under Clauses 2 and 3, Article 17 of this Law if past the deadline stated in the first notice, a tax payer fails to pay tax; if such tax payer still fails to fully pay tax and fine for late tax payment stated in the second notice, coercive measures prescribed in Clause 4, Article 17 of this Law shall be applied to guarantee full collection of tax and fine; If such tax payer once again fails to pay full amount of tax and fine even after such coercive measures have been taken, the dossier of the case shall be transferred to the competent State agency for handling as prescribed by law;

3. To examine and inspect the tax declaration, payment and final settlement by tax payers in order to ensure the strict observance of law;

4. To handle tax-related administrative violations and settle complaints about tax;

5. To request the tax payers to provide accounting books, invoices, vouchers and other records and documents related to the tax calculation and payment;

6. To keep and use data and documents provided by the tax payers and other subjects in accordance with the prescribed regime.

Article 15.- The right to determine tax

1. The tax authority shall determine the payable special consumption tax amount for a tax payer in the following cases when the latter:

a) Fails to implement or has improperly implemented the regulations on accounting, invoices and vouchers;

b) Fails to declare tax or to submit the tax declaration within the notified time limit; or has submitted the tax declaration but falsely declared the bases for determining the special consumption tax amount;

c) Refuses to produce accounting books, invoices, vouchers and necessary documents relating to the calculation of special consumption tax;

d) Is found to have conducted business without any business registration.

2. The tax authority shall base itself on documents related to investigation of production and business activities of concerned tax payers or on the payable tax amounts of other production and business establishments with the same business line and scale, to determine the payable tax amounts.

Chapter IV

SPECIAL CONSUMPTION TAX REDUCTION AND EXEMPTION

Article 16.- Cases eligible to be considered for special consumption tax reduction or exemption

1. Establishments producing goods subject to the special consumption tax, which meet difficulties due to natural calamities, enemy sabotage or unexpected accidents, shall be considered for tax reduction or exemption.

2. Small beer-making establishments, which are operating, have fully paid tax according to the special consumption tax table prescribed in Article 7 of this Law but suffered from losses, shall be considered for special consumption tax reduction corresponding to the loss incurred in the tax reduction year(s); the tax reduction duration shall not exceed five years from the effective date of this Law.

3. If a domestic establishment engaged in the automobile assembly and/or manufacture which has enjoyed a reduction of from 60%-100% of the tax rate in the special consumption tax table stipulated in Article 7 of this Law in the first five years from the effective date of this Law continues to suffer from losses, the tax reduction duration may be extended for one to five more years.

4. A golf business establishment shall be entitled to a 30% tax rate reduction according to the special consumption tax table stipulated in Article 7 of this Law for three years from the effective date of this Law.

The Government shall specify the tax reduction and exemption prescribed in this Article.

Chapter V

HANDLING OF VIOLATIONS, REWARDS

Article 17.- Handling of violations committed by tax payers

A tax payer who violates the Law on Special Consumption Tax shall be handled as follows:

1. A tax payer who fails to strictly comply with the regulations on tax registration, declaration, payment and final settlement, the regime of accounting and keeping of invoices and vouchers as prescribed in Articles 8, 9, 10, 11 and 12 of this Law shall, depending on the nature and seriousness of his/her violation, be administratively sanctioned for tax violations;

2. A tax payer who fails to pay tax or fine on time as prescribed or as stated in a sanctioning decision shall, in addition to the full payment of such tax and fine amounts, be subject to a fine of to 0.1% (one thousandth) of the belated payment amount per late day;

3. A tax payer who falsely declares or evades tax shall, in addition to the full tax payment under this Law, be subject to a fine equal to one to five times of the fraudulent tax amount, depending on the nature and seriousness of his/her violation. A tax payer who evades a large amount of tax or repeats a tax violation for which he/she was administratively sanctioned, or commits another serious violation, shall be examined for penal liability as prescribed by law;

4. A tax payer who fails to pay tax or fine according to the notice or the tax sanctioning decision shall be subject to the following coercive measures:

a) The deduction of his/her deposit at the bank, credit institution or treasury for the payment of such tax or fine.

The bank, credit institution or treasury shall have to deduct an amount of money from the tax payer's deposit account for payment of tax or fine into the State budget according to the tax handling decision of the tax authority or the competent State agency before the collection of debts;

b) The seizure of goods and material evidences to guarantee the full collection of tax or fine;

c) The inventory of his/her property as prescribed by law so as to ensure the full collection of outstanding tax or fine.

Article 18.- The competence of the tax authorities to handle tax violations

1. The heads of the tax authorities that directly manage the tax collection shall be entitled to handle violations committed by tax payers as defined in Clauses 1, 2 and 3, Article 17 of this Law.

2. The heads of the tax departments or sub-departments that directly manage the tax collection shall be entitled to apply handling measures prescribed in Clause 4, Article 17 of this Law, and forward dossiers to the competent agencies for handling according to the provisions of criminal law with regard to the violations described in Clause 3, Article 17 of this Law.

Article 19.- Handling of violations committed by tax officials and other individuals

1. A tax official or an individual who abuses his/her position and power to illegally use or appropriate tax money or fines shall have to return to the State the whole tax amount or fines he/she has illegally used or appropriated and shall, depending on the nature and seriousness of his/her violation, be disciplined or examined for penal liability as prescribed by law.

2. A tax official or an individual who, due to irresponsibility or mishandling, causes damage to tax payers, shall have to make compensation in accordance with the provisions of the civil legislation; and he/she shall, depending on the nature and seriousness of his/her violation, be disciplined or examined for penal liability as prescribed by law.

3. A tax official or an individual who abuses his/her position and power to act in complicity with or cover up violator(s) of the special consumption tax law or commits other acts of violating the provisions of this Law shall, depending on the nature and seriousness of his/her violation, be disciplined or examined for penal liability as prescribed by law.

4. Those who hinder or incite other people to hinder the enforcement of the Law on Special Consumption Tax shall, depending on the nature and seriousness of their violations, be administratively sanctioned or examined for penal liability as prescribed by law.

Article 20.- Rewards

Tax authorities or tax officials that well perform their assigned tasks; organizations or individuals that record achievements in implementing the Law on Special Consumption Tax; and tax payers who fulfill their tax obligations shall be rewarded.

The Government shall stipulate in detail the reward.

Chapter VI

COMPLAINTS, THE INITIATION OF LAWSUITS AND THE STATUTE OF LIMITATIONS

Article 21.- The rights and responsibilities of tax payers in making complaints about tax

1. Tax payers shall have the right to complain about acts of tax officials and tax authorities they deem violating the Law on Special Consumption Tax.

Complaints shall be lodged to the tax authority that directly manages the tax collection within 30 days from the date of receipt of notices or handling decisions of tax officials or tax authorities.

Pending the settlement of complaints, the complainants shall still have to strictly comply with the notices or the decisions of the tax officials or tax authorities.

2. In cases where a complainant disagrees with a decision of the agency in charge of handling complaints, or his/her complaints is not settled within the time limit prescribed in Article 22 of this Law, he/she shall be entitled to lodge complaint to the immediate higher tax authority or initiate a lawsuit at the court as prescribed by law.

Article 22.- The responsibilities and powers of tax authorities in settling tax complaints

1. Within 15 days from the date of receipt of a tax complaint, a tax authority shall have to settle such complaint; for complicated cases, such time limit may be extended but must not exceed 30 days; if the case is beyond its jurisdiction, the tax authority shall have to forward the dossier or send a report to a competent agency for settlement and inform the complainant thereof within ten days from the date of receipt of the complaint.

2. The complaint-receiving tax authority shall have the right to request complainants to provide dossiers and documents relating to their complaints; if the complainants refuse to do so, the tax authority shall be entitled to decline the consideration and settlement of such complaints.

3. The tax authority shall have to return to tax payers the amounts of tax or fines improperly collected within 15 days from the date of receipt of decisions from the superior tax authority or the competent agency as prescribed by law.

4. Upon the discovery of and conclusion on a false tax declaration, tax evasion or errors, the tax authority shall have to collect the tax or fine arrears or reimburse tax payment dating back 5 years from the date of discovery of false tax declaration, tax evasion or tax errors. In cases where tax payers fail to register, declare and pay tax, the duration for collection of tax or fine arrears shall be dated back to the date such tax payers commenced their operation.

5. The head of a superior tax authority shall have to settle tax complaints lodged by tax payers against the subordinate tax authorities.

The Minister of Finance's decisions on the settlement of tax complaints shall be final.

Chapter VII

ORGANIZATION OF IMPLEMENTATION

Article 23.- The Government shall direct the organization of the implementation of the Law on Special Consumption Tax throughout the country.

Article 24.- The Minister of Finance shall have to organize and inspect the implementation of the Law on Special Consumption Tax throughout the country.

Article 25.- The People's Committees at all levels shall, within their respective tasks and powers, direct the implementation and inspect the observance of the Law on Special Consumption Tax in their respective localities.

Chapter VIII

IMPLEMENTATION PROVISIONS

Article 26.- This Law takes effect from January 1st, 1999.

This Law replaces the Law on Special Consumption Tax of June 30, 1990, the Law on the Amendments and Supplements to a Number of Articles of the Law on Special Consumption Tax of July 5, 1993, and the Law on the Amendments and Supplements to a Number of Articles of the Law on Special Consumption Tax of October 28, 1995.

To annul the stipulations on special consumption tax in other legal documents as from the effective date of this Law.

The settlement of all remaining problems relating to tax, tax final settlement, tax exemption and reduction and the handling of special consumption tax violations before January 1st, 1999 shall comply with relevant stipulations of the Law on Special Consumption Tax, the Laws on the Amendments and Supplements to a Number of Articles of the Law on Special Consumption Tax and the stipulations on special consumption tax in other legal documents.

Article 27.- In cases where an international agreement which the Socialist Republic of Vietnam has signed or acceded to contains provision(s) different from those of this Law, the special consumption tax shall be applied in accordance with the provision(s) of such international agreement.

Article 28.- The Government shall stipulate in detail and guide the implementation of this Law.

This Law was passed by the Xth National Assembly of the Socialist Republic of Vietnam, on May 20, 1998 at its 3rd session.

|

|

NATIONAL ASSEMBLY |