Nội dung toàn văn Official Dispatch 44/NHNN-TCKT of January 05, 2009 providing guidance on accounting of investment interests to be received before purchase.

|

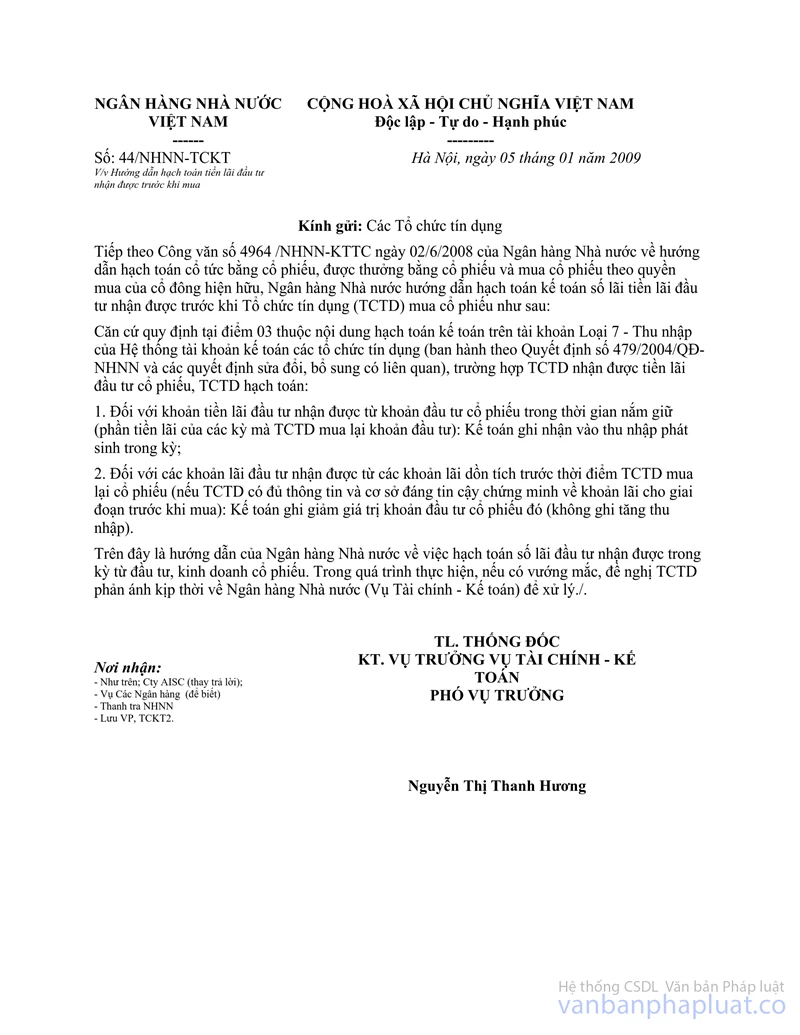

STATE

BANK OF VIETNAM |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 44/NHNN-TCKT |

Hanoi, January 05, 2009 |

To: Credit institutions

Following the Official Dispatch No. 4964/NHNN-KTTC dated 2 June 2008 of the State Bank of Vietnam on providing guidance on accounting of dividends by stocks, reward by stocks and stock purchase in accordance with purchase right of existing shareholders, the State Bank provides guidance on accounting of investment interests to be received before stock purchase by the Credit Institutions (CI) as follows:

Pursuant to provisions at point 03 belonging to the content of accounting in the account of type 7 – Income of Accounts System of credit institutions (issued in conjunction with the Decision No. 479/2004/QD-NHNN and related supplement, amendment decisions), in the event the CI received interests from stock investment, the CI shall account as follows:

1. For investment interests to be received from the stock investment during the holding time (interests of periods where the CI repurchased the investment): The accountant shall record them as income arising in the period;

2. For investment interests to be received from accumulated interests before the time of repurchase of stock by the CI (if the CI has full information and reliable evidence about the interests of the period before purchase): The accountant shall write down value of that stock investment (do not write up income).

The above is the guidance of the State Bank on the accounting of investment interests to be received in the period from the stock investment, business. During the process of implementation, any obstacle that may arise should be timely reported by the CI to the State Bank (Finance – Accounting Department) for settlement.

|

|

AUTHORIZED

BY THE GOVERNOR OF THE STATE BANK OF VIETNAM |