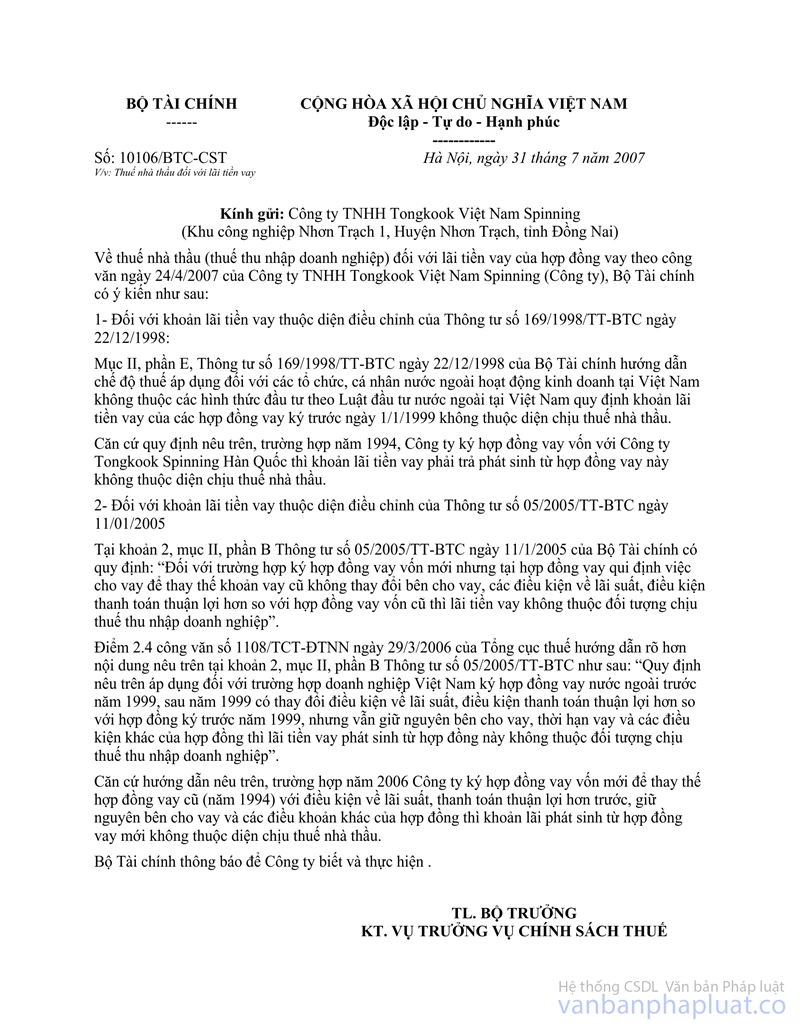

Nội dung toàn văn Official Dispatch No. 10106/BTC-CST of July 31, 2007 Regarding Contractor Tax On Loan Interests

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 10106/BTC-CST |

Hanoi, July 31, 2007 |

To:

Tongkook Vietnam Spinning Limited Liability Company

(Nhon Trach 1 Industrial Park, Nhon Trach district, Dong Nai province)

Regarding contractor tax (business income tax) on loan interests under the loan contract according to the April 24, 2007 Official Letter of Tongkook Vietnam Spinning Limited Liability Company (the Company), the Ministry of Finance gives the following opinions:

1. For loan interests governed by Circular No. 169/1998/TT-BTC of December 22, 1998:

Section II, Part F of the Finance Ministry’s Circular No. 169/1998/TT-BTC of December 22, 1998, guiding the tax regime applicable to foreign organizations and individuals having business operations in Vietnam without investment forms under the Law on Foreign Investment in Vietnam, stipulates that loan interests under loan contracts signed before January 1, 1999, are not liable to contractor tax.

Accordingly, if in 1994 the Company signed a loan contract with South Korea Tongkook Spinning Company, the payable loan interests under this contract are not liable to contractor tax.

2. For loan interests governed by Circular No. 05/2005/TT-BTC of January 11, 2005:

Clause 2, Section II, Part B of the Finance Ministry’s Circular No. 05/2005/TT-BTC of January 11, 2005, stipulates: “In case a newly signed loan contract states that a new loan is provided to replace the old one without changing the lenders, with interest rate and payment conditions are more favorable than those in the old contract, the loan interests are not liable to business income tax.”

Point 2.4 of the General Department of Taxation’s Official Letter No. 1108/TCT-DTNN of March 29, 2006, gives more explicit guidance as follows: “The above stipulation applies to cases in which Vietnamese enterprises signed foreign loan contracts before 1999, then, after 1999 the interest rate terms and payment conditions changed and became more favorable than the loan contracts signed before 1999, while the lenders, the loan terms and other contractual terms remain the same, the loan interests arise under these contracts are not liable to business income tax.”

Based on the above guidance, if in 2006 the Company signed a new loan contract in replacement of the old one (signed in 1994) with more favorable interest rate and payment conditions, without changing lenders and other contractual terms, the interests under the new contract are not liable to contractor tax.

The Ministry of Finance notifies its above opinions to the Company for information and compliance.

|

|

FOR

THE MINISTER OF FINANCE |