Nội dung toàn văn Official Dispatch No. 11684/BTC-TCT of September 16, 2005, guiding the business income tax

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 11684/BTC-TCT |

Hanoi, September 16, 2005 |

|

To: |

- Ministries,

ministerial-level agencies, Government-attached agencies; |

Proceeding from the problems reported by localities and enterprises in the course of implementation of the Finance Ministry’s Circular No. 128/2003/TT-BTC of December 22, 2003 and Circular No. 88/2004/TT-BTC of September 1, 2004, guiding the implementation of enterprise income tax, the Finance Ministry hereby provides additional specific guidance on a number of contents on business income tax as follows:

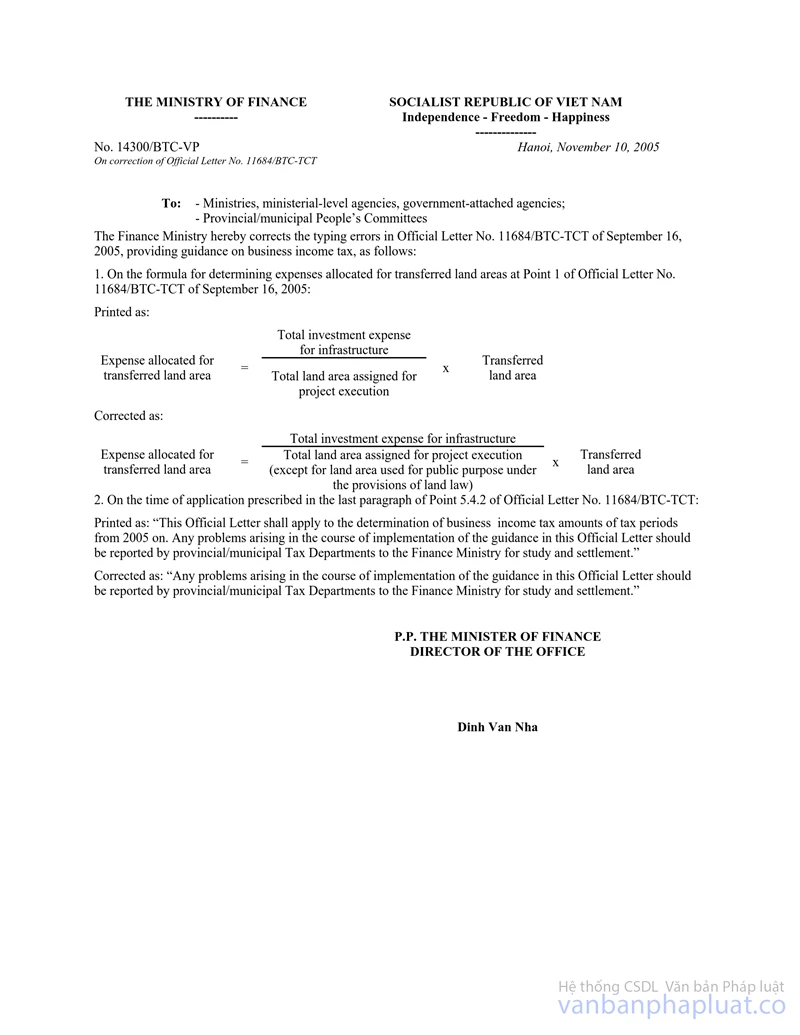

1. The determination of expenses for land use right transfer, land lease right transfer

The expenses for land use right transfer, land lease right transfer shall be determined under the guidance at Point 2.1, Section IV, Part C of the above-said Circular No. 128/2003/TT-BTC which is now guided in detail regarding the distribution of expenses for land use right transfer, land lease right transfer according to square meters of the transferred land for investment projects to be completed part by part as follows:

The common expenses for the entire projects of establishments dealing in houses or infrastructures shall be distributed according to square meters of the transferred land in order to determine the taxable incomes from activities of transferring the land use rights, transferring the land lease rights, which include expenses for traffic roads, greenery premises; expenses for investment in construction of water supply and drainage systems, transformer stations; expenses for land damage compensation. The above expense distribution shall be determined in the following formula:

|

Expense distributed for transferred land acreage |

= |

Total investment expense for infrastructure construction |

x |

Transferred land area |

|

Total land area assigned for project execution |

2. Declaration and payment of tax on land use right transfer before the annual tax finalization:

Organization dealing in houses, land, infrastructures, architectures on land shall declare, pay and settle tax on incomes from land use right transfer, land lease right transfer under the guidance at Point 2.2, Section VII, Part C of Circular No. 128/2003/TT-BTC which is now guided in detail as follows:

a. In cases where business organizations transfer the land use rights or land lease rights before the annual tax finalization while the purchasers demand the completion of procedures for grant of land use right certificates, the tax offices shall carry out procedures to notify, inspect and certify the payable tax amounts on declaration form No. 02C/TNDN under the guidance at Point 2.1, Section VII, Part C of the above-said Circular No. 128/2003/TT-BTC The business organizations shall pay the tax amounts determined in the tax declaration forms and provide tax payment vouchers to the land use right registration offices for carrying out the procedures to grant the land use right certificates.

The tax amounts paid by business organizations for the transferred land shall be subtracted from the business income tax amounts temporarily paid in the quarter according to the business income tax declaration (Form 02A/TNDN) or according to amounts fixed by the tax offices. At the end of a tax year, the business organizations shall carry out procedures for business income tax finalization according to regulations.

b. In cases where business organizations transfer the land use rights or land lease rights in localities (provinces, centrally run cities) other than the localities where their head-offices are based (including organizations with land use right transfer activities arising not frequently), they must carry out procedures to declare tax on incomes from land use right transfer, land lease right transfer. If business organizations fail to set up their management sections in localities where exist the transferred land, they must declare tax with tax offices and pay tax at localities where exist the transferred land.

The dossiers on tax declaration and payment and vouchers on payment of tax on incomes from land use right transfer, land lease right transfer arising in localities where exist the transferred land shall serve as bases for finalization of tax at the head-offices.

3. Regarding procedures for declaration, deduction of business income tax paid for agents being individual business households by business establishment being principals:

At point 3 of Circular No. 88/2004/TT-BTC and Official Letter No. 13692/TC-TCT of November 23, 2004 on income tax of individuals acting as agents, the following guidance was provided: Business establishments assigning agency to individual business households with business registration certificates but failing to fully comply with the regime of accounting, invoices, sale of goods or provision of services at the set prices must pay business income tax at the fixed rate of 5% of the enjoyed agency commission, including support amounts from the principals. The business establishments being principals shall have to declare and withhold business income tax of the above-said business households being agents and pay them into the state budget together with the annual declaration and payment of value added tax of the establishments and shall enjoy royalties being equal to 0.8% of the actually collected tax amount of the agents for payment into the state budget. Such royalty amounts shall be subtracted from the business income tax amounts collected from the agents before remittance into the budget.

To unify the criteria upon declaration and payment of business income tax according to the contents guided above, the Finance Ministry promulgates declaration form (Form No. 02/TNDN-KT) together with this Official Letter to facilitate the tax declaration and monitoring of tax collection, payment, accounting and statistics.

4. On loss carried forward:

Business establishments that suffer losses after tax settlement shall be entitled to subtract their loss amounts from their taxable incomes of the subsequent years under the guidance at Point 8, Section III, Part C of the above-said Circular No. 128/2003/TT-BTC which is now further guided in detail as follows:

a. The loss amount subtracted from the taxable income of the tax settlement year shall be determined as equal to the negative difference of the turnover calculated according to enterprise income tax minus (-) reasonable expenses plus (+) amounts of damage caused to goods by objective reasons in the tax calculation period.

Business establishments shall themselves determine their loss amounts to be subtracted from taxable incomes according to the above principle and register their loss carried forward plans with tax offices. Where the bodies competent to examine, inspect and finalize the business income tax determine that loss amounts to be eligibly carried forward by the business establishments, which are different from the loss amounts determined by the business establishments themselves, the loss amounts to be subtracted from the taxable incomes shall be determined according to the conclusions of competent bodies.

b. Business establishments suffering losses must draw up plans on loss carried forward immediately after the year when the losses arose and inscribe them in Section I of Appendix No. 1 promulgated together with the declaration on self-finalization of business income tax and send them to the tax offices for registration of the loss carried forward plans in any fiscal year in the prescribed loss carrying period. In cases where business establishments suffer losses in land use right or land lease right transfer activities, they must register separate loss carried forward plans.

Business establishments are not allowed to carry forward losses if they fail to register their loss carried forward plans with tax offices or transfer losses outside the loss carried forward plans already registered with tax offices.

c. Annually when finalizing the business income tax, business establishments shall base on their loss carried forward plans registered with the tax offices of the previous tax calculation periods to determine the carried forward loss amounts to be subtracted from the taxable incomes of the tax finalization period and inscribe them in Section II, Appendix 1 to the declaration on self-finalization of business income tax. Where the taxable income of the tax finalization period is lower than the loss amount in their registered loss carried forward plans, the remaining loss amount shall be added to the loss amount registered in the loss carried forward plan of the following year and inscribe it in Section I of Appendix 1 to the declaration of self-finalization of business income tax without having to re-register the loss carried forward plan; the time limit for accumulation of loss amount not yet fully transferred to the following year shall not exceed the prescribed loss carried forward time limit.

d. The loss amounts carried forward from 2003 backward but within the five- year time limit shall be handled as follows:

- The business establishments are entitled to continue carrying forward losses to the remaining years of the loss transfer time limit without having to re-register their loss carried forward plans with tax offices. Where the loss carried forward have been registered, the registered loss carried forward plans and the above-mentioned guidances shall be complied with.

- Foreign-invested enterprises that have registered their loss carried forward plans with tax offices under the guidance in the Finance Ministry’s Circular No. 13/2001/TT-BTC of March 8, 2001 shall continue to carry forward their losses under the registered plans; where the loss amounts are not yet registered for carry forward while the loss carries forward time limit has not yet expired, the establishments shall be entitled to register their plans for carry forward of losses to the remaining years under the guidance at this Point.

5. On business income tax preference:

Point 3, Part I of Circular No. 128/TT-BTC (amended at Point 8 of Circular No. 88/2004/TT-BTC) guided preferences for cases already granted investment licenses, investment preference certificates before February 1, 2004, is now additionally guided in detail as follows:

5.1. Domestic business establishments already granted investment preference certificates before January 1, 2004 are entitled to shift to the preferential business income tax rates as follows:

a. Domestic business establishments currently applying the preferential business income tax rates under the investment preference certificates granted before January 1, 2004 and still satisfying the investment preference conditions stated in the investment preference certificates shall be entitled to shift to apply the preferential business income tax rates for the remaining preference duration as follows:

- The tax rate of 25% under the investment preference certificates is, as from January 1, 2004, changed to the tax rate of 20% for the remaining preference duration.

- The tax rate of 20% under the investment preference certificates is, as from January 1, 2004, changed to the tax rate of 15% for the remaining preference duration.

- The tax rate of 15% under the investment preference certificates is, as from January 1, 2004, changed the tax rate of 10% for the remaining preference duration.

b. Domestic business establishments currently enjoying the preferential business income tax rates under the investment preference certificates granted before January 1, 2004 and now satisfying additional preference conditions guided in Section I, Part E of Circular No. 128/2003/TT-BTC as compared with the investment preference certificates already granted shall, as from January 1, 2004, be entitled to enjoy the preferential business income tax rates guided in Section II, Part E of Circular No. 128/2003/TT-BTC for the remaining preference duration, depending on the extent of satisfying the investment preference conditions.

c. Domestic business establishments currently enjoying the preferential business income tax rates under the investment preference certificates granted before January 1, 2004 but now failing to satisfy the conditions to enjoy the preferential business income tax rates guided in Section II, Part E of Circular No. 128/2003/TT-BTC shall continue to enjoy the preferential tax rates under the granted investment preference certificates for the remaining preference duration.

The remaining preference duration stated in Items a and b of this Point shall be determined as equal to the duration of enjoying the preferential tax rates as guided at Point 2, Section II, Part E of Circular No. 128/2003/TT-BTC minus (-) the duration from the time the business establishments commenced their production and/or business operations to January 1, 2004.

5.2. Foreign-invested enterprises and foreign parties to business cooperation contracts, that had been granted the investment licenses before January 1, 2004 and satisfy the conditions inscribed in the investment licenses, shall continue to enjoy the preferential business income tax rates until the end of the period of enjoying the preferential tax rates under the investment licenses; after the period of enjoying the preferential tax rates under the investment licenses, they shall shift to apply the enterprise income tax rate of 25%; in cases where they are paying the business income tax at the tax rate of 25%, they shall continue applying the tax rate of 25% till the expiry of the investment licenses. For foreign-invested enterprises and foreign parties to business cooperation contracts, that have applied for extension of investment licenses as from January 1, 2004 on, the applicable preferential enterprise income tax rates shall comply with the guidance in Sections I and II, Part E of Circular No. 128/2003/TT-BTC.

5.3. The business income tax rates for incomes from activities of transferring contributed capital, stock capital shall be applied as follows:

a. Business establishments with incomes arising from activities of transferring contributed capital, stock capital, which have been already invested in other business establishments (income is equal (=) to the revenue from transfer of contributed capital, stock capital minus (-) the contributed capital amount, stock capital amount), shall have to pay business income tax for the incomes from activities of transferring the contributed capital, stock capital at the tax rate applicable to their principal business activities.

b. Foreign investors or foreign parties to business cooperation contracts, that transfer their contributed capital portions or stock capital portions within the foreign-invested enterprises or the business cooperation contracts shall have to pay enterprise income tax at the tax rate of 28% for the income from the transfer of contributed capital or stock capital.

5.4. Regarding the enterprise income tax exemption or reduction duration

5.4.1. Where the enterprise income tax preference levels inscribed in the granted investment licenses or investment preference certificates granted to business establishments before January 1, 2004 are lower than the enterprise income tax preference levels guided in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC (with the same enterprise income tax preference conditions inscribed in the investment licenses or investment preference certificates), the business establishments shall be entitled to enjoy the enterprise income tax preference levels under the guidance in the above-said Circulars for the remaining preference duration counting from the 2004 tax calculation period.

The tax preference levels for comparison in this case shall be determined on the basis of tax preference percentages (tax exemption; 50% reduction of payable tax amounts) and the tax exemption or reduction duration (the number of years of tax exemption or tax reduction according to the prescribed regime).

The remaining preference duration is equal to the number of years for which business establishments still enjoy tax exemption or reduction under the guidance in Circular No. 128/2003/TT-BTC Circular No. 88/2004/TT-BTC minus (-) the number of years for which the business establishments have already enjoyed tax exemption or reduction under their investment licenses or investment preference certificates granted to the end of 2003. The determination of the above-mentioned remaining preference duration must follow the principles:

- At the end of the 2003 tax period, the business establishments that are being in the tax exemption period under the granted investment licenses or investment preference certificates shall continue to enjoy the remaining tax exemption or reduction years under the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC.

- At the end of the 2003 tax period, the business establishments that have just gone through the tax exemption period under their granted investment licenses or investment preference certificates shall only be entitled to enjoy the complete number of tax reduction years under the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC.

- At the end of the 2003 tax period, if the business establishments are being in the tax reduction period under their granted investment licenses or investment preference certificates, the remaining number of tax reduction years is equal to the number of tax reduction years under the guidance in Circular No. 128/2003/TT-BTC Circular No. 88/2004/TT-BTC minus (-) the number of years for which the business establishments have enjoyed the tax reduction to the end of the 2003 tax calculation period.

- At the end of the 2003 tax period, the business establishments that have just gone through the tax exemption period and the tax reduction period under their granted investment licenses or investment preference certificates shall not be entitled to enjoy tax exemption and/or tax reduction under the guidance in Circular No. 128/2003/TT-BTC Circular No. 88/2004/TT-BTC.

5.4.2. For a number of specific cases, the remaining preference duration shall be determined as follows:

a. Where the tax exemption or reduction duration under investment licenses or investment preference certificates granted before January 1, 2004 is shorter than that guided in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC the business establishments shall be entitled to enjoy tax exemption or reduction for the remaining preference period as follows:

Example 1: Under investment licenses granted before January 1, 2004, a production enterprise set up from a project on investment in an industrial park shall enjoy business income tax exemption for two years and 50% business income tax reduction for three subsequent years counting from the time the taxable income is generated. At the end of 2003, this enterprise had enjoyed tax exemption for only one year. Under the guidance in Circular No. 88/2004/TT-BTC production enterprises set up from projects on investment in industrial parks shall enjoy business income tax for three years and 50% business income tax reduction for seven subsequent years. Compared with the above guidance, as from the 2004 tax calculation period, such enterprise shall still be entitled to enjoy tax exemption for two more years and the 50% business income tax reduction for seven subsequent years.

Example 2: According to the above-cited example 1, if by the end of the 2003 tax period, an enterprise had already enjoy tax exemption for two years under the granted license, as from the 2004 tax period, the enterprise shall still be entitled to enjoy tax reduction for seven years.

Example 3: According to the above-cited example 1, if by the end of the 2003 tax period, the enterprise had fully enjoyed the tax exemption duration and the tax reduction for one year under the granted license, as from the 2004 tax period, the enterprise shall continue enjoying the tax reduction for 6 more years.

Example 4: According to the above-cited example 1, if by the end of the 2003 tax period, the enterprise had fully enjoyed the tax exemption duration and the tax reduction duration under the granted license, as from the 2004 tax period, the enterprise shall not be entitled to enjoy the tax reduction under the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC.

b. Where the business income tax exemption duration inscribed in the investment licenses or investment preference certificates granted before January 1, 2004 is longer than that under the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC while the tax reduction duration is shorter, the tax exemption or reduction for the remaining preference duration shall be determined as follows:

Example 1: Under the investment license granted before January 1, 2004, an enterprise under a special investment project is entitled to enjoy business income tax exemption for 4 years and 50% business income tax reduction for 4 subsequent years counting from the time the taxable income is generated. Under the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC such enterprise is entitled to enjoy business income tax exemption for three years and 50% business income tax reduction for seven subsequent years.

If by the end of 2003, the enterprise had enjoyed the business income tax exemption for two years, as from the 2004 tax calculation period, the enterprise may opt to enjoy the tax exemption and reduction under the granted license or to follow the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC:

- Under the granted license: tax exemption for two years and 50% reduction of the payable tax amount for 4 subsequent years.

- Under the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC: tax exemption for one year and 50% reduction of the payable tax amount for seven subsequent years.

Example 2: For the same case mentioned in Example 1 above, but by the end of the 2003 tax period, the enterprise had enjoyed tax exemption for 4 years, it is entitled to tax reduction under the granted investment license, specifically: as from the 2004 tax period, the enterprise shall still be entitled to 50% reduction of the payable tax amount for 4 subsequent years.

Example 3: For the same case mentioned in Example 1 above, by the end of the 2003 tax period, the enterprise had fully enjoyed the four-year tax exemption duration and the four-year tax reduction duration under the granted license, so as from the 2004 tax period, the enterprise shall not be entitled to tax reduction under the guidance in Circular No. 128/2003/TT-BTC and Circular No. 88/2004/TT-BTC.

This Official Letter shall apply to determine the business income tax amounts of the tax calculation periods from 2005 on. If problems arise in the course of implementation of the guidance in this Official Letter, the provincial/municipal Tax Departments are requested to report them to the Finance Ministry for study and settlement.

Form No. 01/TNDN-KT

BUSINESS INCOME TAX DECLARATION FORM

To be used by business establishments being agency principals and submitting them on behalf of individual business households with business registration, that do not fully implement the accounting, invoice and voucher regime

(enclosed with Official Letter No. 11684/BTC-TCT of September 16, 2005 of the Finance Ministry)

Month.............. year..............

Tax identification number:................................................................................................................

Name of the business establishment:...............................................................................................

Address:........................................................................................................................................

Urban district/Rural district:..................................... Province, city:..................................................

Telephone:................................................ Fax:............................... Email:...................................

Main business lines:.......................................................................................................................

Calculation unit: VNdong

|

Ordinal number |

Name of individual business household |

Tax identification number |

Agency contract (No...date..) |

Commission and other revenues to be taxed under contract |

Set percentage |

Payment EIT amount |

|

1 |

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

The total BIT amount

Percentage of remuneration to be enjoyed by entrusted collecting organizations (if any)

Remuneration amount to enjoy (if any)

The total BIT payable in this period:

(In words:..........)

I swear that the above declarations are truthful and bear responsibility therefor.

|

|

Day.......

Month..... year..... |