Nội dung toàn văn Official Dispatch No. 13293/TC-CST of November 16, 2004, on the value added tax rate applicable to malt

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

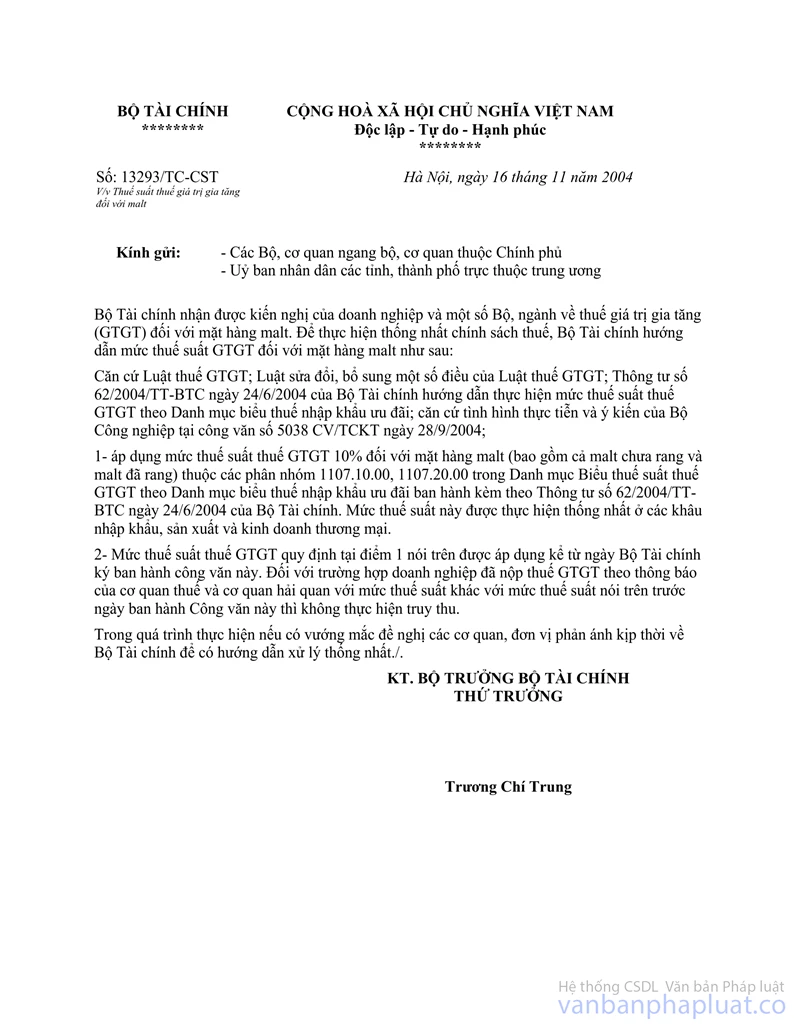

No. 13293/TC-CST |

Hanoi, November 16, 2004 |

|

To: |

- Ministries, ministerial-level agencies, government-attached

agencies |

The Ministry of Finance has received proposals from enterprises and several ministries and branches on the value added tax (VAT) imposed on malt. In order to implement tax policies in a uniform manner, the Ministry of Finance guides the VAT rate applicable to malt as follows:

Pursuant to the VAT Law; the Law Amending a Number of Articles of the VAT Law; the Finance Ministry’s Circular No. 62/2004/TT-BTC of June 24, 2004, guiding the application of VAT rates according to the Preferential Import Tariffs; on the basis of the practical situation and opinions of the Ministry of Industry in Official Letter No. 5038CV/TCKT of September 28, 2004:

1. The VAT rate of 10% shall apply to malt (whether or not roasted) under sub-headings 1107.10.00 and 1107.20.00 in the VAT Tariffs according the Preferential Import Tariffs, issued together with the Finance Ministry’s Circular No. 62/2004/TT-BTC of June 24, 2004. This tax rate shall apply uniformly at the stages of importation, production and trading.

2. The VAT rate defined at Point 1 above shall apply as from the date the Ministry of Finance signs this Official Letter. Where enterprises have paid VAT at a rate other than the aforesaid VAT rate according to notices issued by tax offices and customs offices before the date of issuance of this Official Letter, any unpaid VAT shall not be collected.

Agencies and units are requested to report any problems arising in the course of implementation to the Ministry of Finance for uniform guidance and settlement.

|

|

FOR THE MINISTER OF FINANCE |