Nội dung toàn văn Official Dispatch No. 1820/TCT-TNCN, on personal income tax policy for profits

|

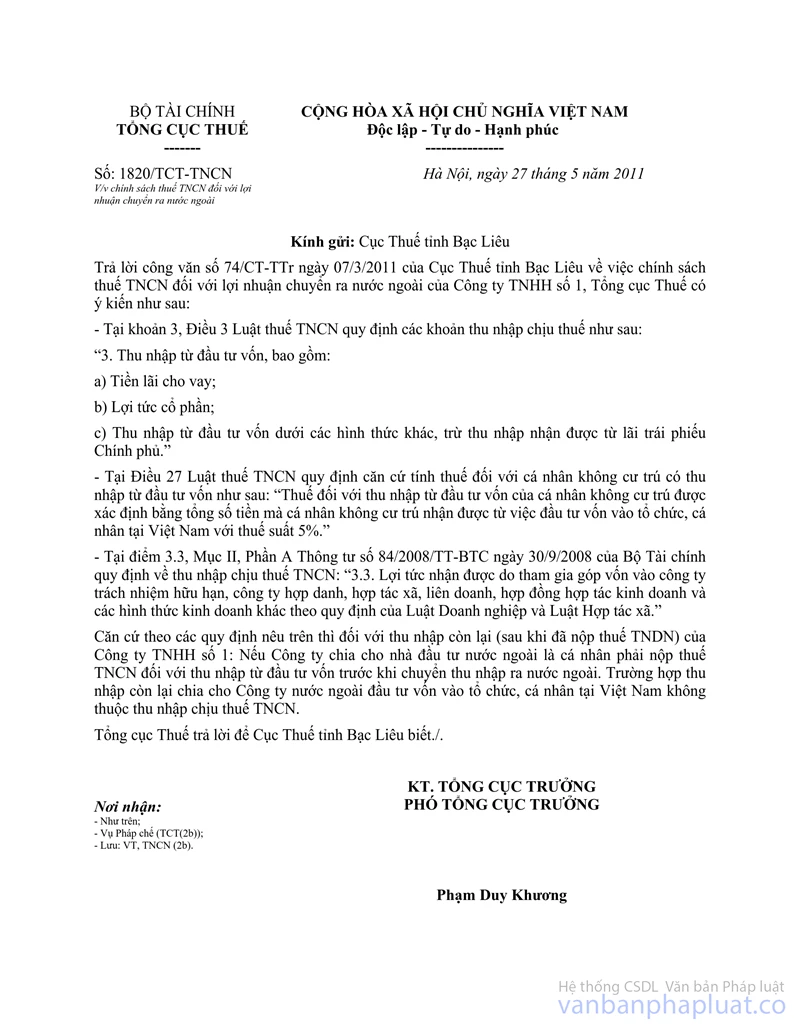

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 1820/TCT-TNCN |

Hanoi, May 27, 2011 |

OFFICIAL DISPATCH

ON PERSONAL INCOME TAX POLICY FOR PROFITS TRANSFERRED OVERSEAS

To: Bac Lieu Department of Tax

On answer the Official Dispatch No. 74/CT-TTr dated March 07, 2011 of Bac Lieu Department of Tax on Personal Income Tax Policy for profits transferred overseas of No.1 Limited Company, the General Department of Tax has following opinions:

- The Article 3.3 of the Law on Personal Income Tax regulates taxable incomes as following:

“3. Incomes from capital investment, including: a/ Interests;

b/ Dividends;

c/ Incomes from capital investment in other forms, except for government bond interests.”

- The Article 27 of the Law on Personal Income Tax regulates the

calculation base for non-residents who earn incomes from capital investment as following: “Tax on income from capital investment of a nonresident is determined to be equal to the total sum of money earned by a non-resident from his/her capital investment in organizations or other individuals in Vietnam, multiplied by the tax rate of 5%.” - At the point 3.3, Section II, Part A of the Circular No. 84/2008/TT-BTC dated September 30, 2008 of the Ministry of Finance regulating incomes liable to personal income tax: “Profits received for contribution of capital to limited liability companies, partnerships, cooperatives, joint ventures, business cooperation contracts and other business forms under the Enterprise Law and the Cooperative Law.”

Pursuant to above regulations, the remained income of No.1 Limited Company (after paying enterprise income tax): If the Company shares foreign investors who have to pay personal income tax for Incomes from capital investment before transferring incomes overseas. The remaining incomes are shared with foreign company investing in organizations, individuals in Vietnam and not in the list of Incomes liable to personal income tax.

The General Department of Tax responds to Bac Lieu Departments of Tax for full understanding./.

|

|

FOR THE GENERAL DIRECTOR |