Nội dung toàn văn Official Dispatch No. 3559/TCT-CS, on Enterprise income tax rates

|

MINISTRY

OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No.

3559/TCT-CS |

Hanoi, September 23, 2008 |

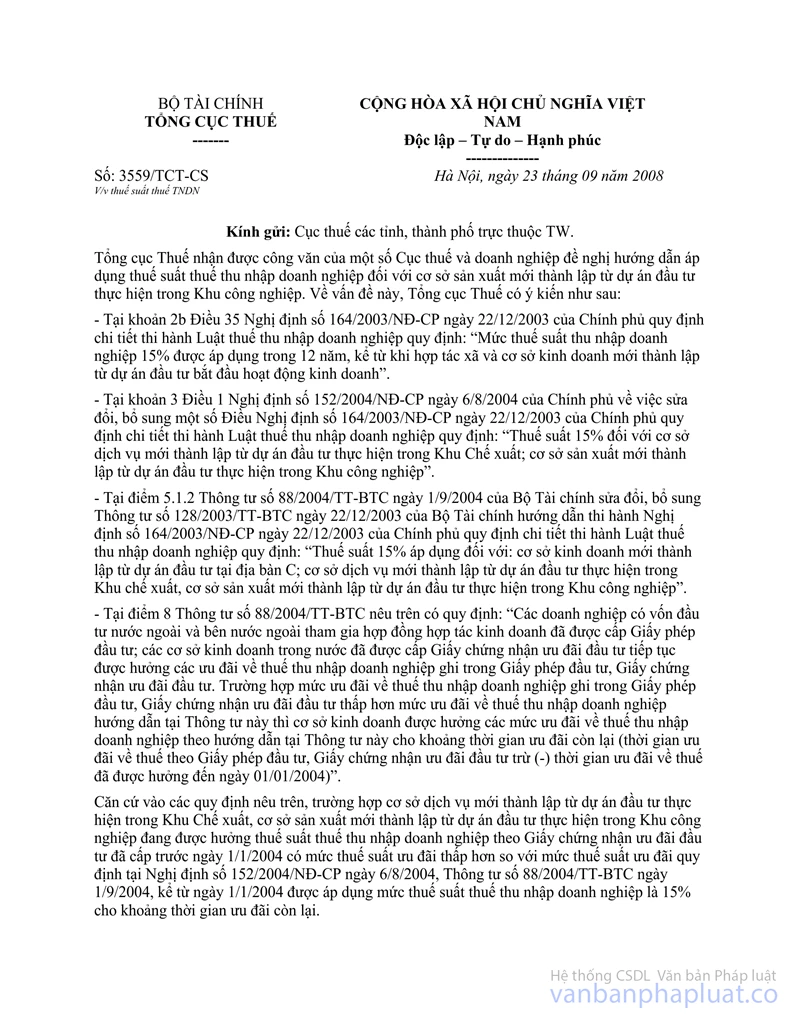

To: Tax Offices of provinces and centrally run cities

The General Department of Taxation has received requests from some Provincial Tax Offices and enterprises for guidance on enterprise income tax rates applicable to production establishments newly set up under investment projects in industrial parks. Regarding this issue, the General Department of Taxation gives the following opinions:

- Clause 2b, Article 35 of the Government's Decree No. 164/2003/ND-CP of December 22, 2003, detailing the implementation of the Law on Enterprise Income Tax, stipulates: “The enterprise income tax rate of 15% shall be applied for 12 years after newly-established cooperatives and business establishments newly set up under investment projects start their business operations”

- Clause 3, Article 1 of the Government's Decree No. 152/2004/ND-CP of August 6, 2004, amending and supplementing a number of articles of the Government's Decree No. 164/2003/ND-CP of December 22, 2003, detailing the implementation of the Law on Enterprise Income Tax, stipulates: “The tax rate of 15% shall be applicable to service establishments newly set up under investment projects executed in export processing zones; production establishments newly set up under investment projects executed in industrial parks.”

- Point 5.1.2 of the Ministry of Finance’s Circular No. 88/2004/TT-BTC of September 1, 2004, amending and supplementing the Ministry of Finance’s Circular No. 128/2003/TT-BTC of December 22, 2003, guiding the implementation of the Government's Decree No. 164/2003/ND-CP of December 22, 2003, detailing the implementation of the Law on Enterprise Income Tax, stipulates: “The tax rate of 15% shall be applicable to: business establishments newly set up under investment projects in grade-C localities, service establishments newly set up under investment projects executed in export processing zones; and production establishments newly set up under investment projects executed in industrial parks.”

- Point 8 of Circular No. 88/2004/TT-BTC stipulates: “Foreign-invested enterprises and foreign parties to business cooperation contracts having obtained investment licenses; domestic businesses establishments having obtained investment preference certificates may continue enjoying preferential enterprise income taxes under their investment licenses or investment preference certificates. When the preferential enterprise income tax rate under an investment license or investment preference certificate is lower than the preferential enterprise income tax rate under this Circular, a business establishment may enjoy the preferential enterprise income tax rate under this Circular for its remaining time of tax preference (the tax preference period under the investment license or investment preference certificate minus (-) the time of having enjoyed preferential taxes till January 1, 2004).”

Under the above regulations, when service establishments newly set up under investment projects executed in export processing zones; production establishments newly set up under investment projects executed in industrial parks currently enjoying enterprise income tax rates under investment preference certificates granted prior to January 1, 2004, which are lower than the preferential tax rate specified in Decree No. 152/2004/ND-CP of August 6, 2004, and Circular No. 88/2004/TT-BTC of September 1, 2004, are entitled to the enterprise income tax rate of 15% for their remaining time of tax preference from January 1, 2004, .

The remaining time of tax preference is determined as 12 years minus the period from the time a business establishment starts its production and business activities to January 1, 2004.

The General Department of Taxation informs Provincial Tax Offices for information and guidance to taxpayers for implementation.

|

|

FOR

THE DIRECTOR GENERAL OF TAXATION |