Nội dung toàn văn Official Dispatch No. 4468/TCT-CS on value-added tax (VAT) for international

|

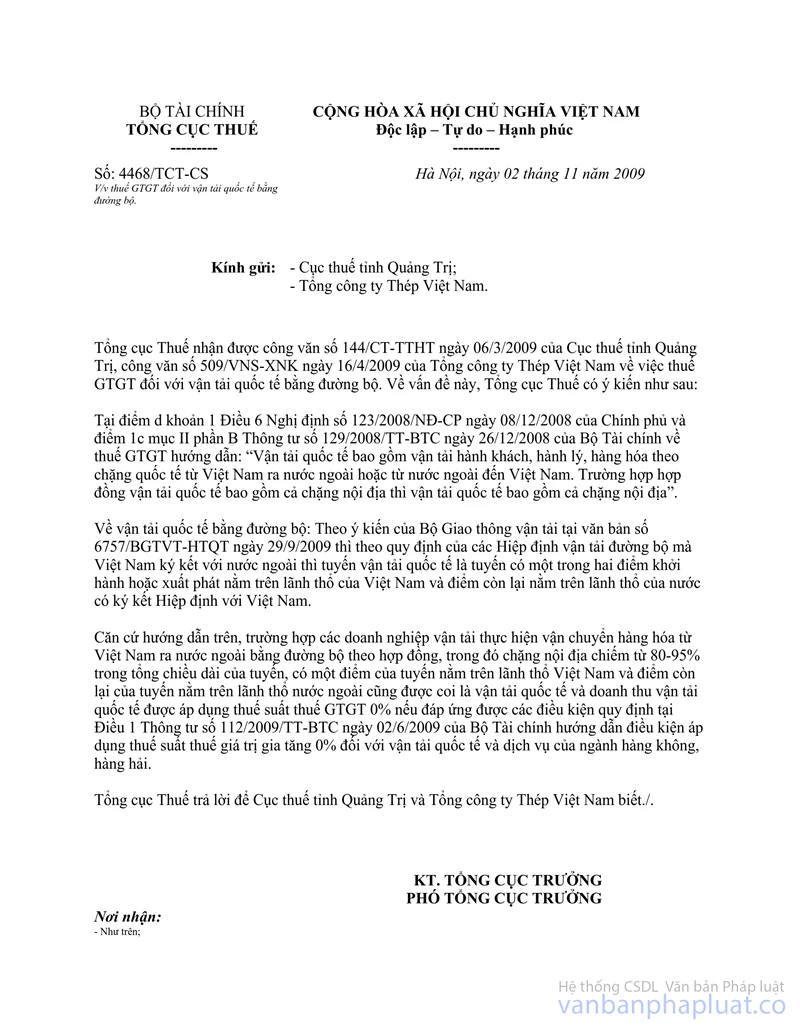

THE

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 4468/TCT-CS |

Hanoi, November 02, 2009 |

OFFICIAL LETTER

ON VALUE-ADDED TAX (VAT) FOR INTERNATIONAL TRANSPORTATION BY ROAD

|

To: |

- The Tax Department of Quang

Tri province |

The General Department of Taxation has received Official Letter No. 144/CT-TTHT of March 6, 2009, of the Tax Department of Quang Tri province, and Official Letter No. 509/VNS-XNK of April 16, 2009, of the Vietnam Steel Corporation, inquiring about VAT for international transportation by road. Regarding this mater, the General Department of Taxation gives the following opinions:

Point d, Clause 1, Article 6 of the Government’s Decree No. 123/2008/ND-CP of December 8, 2008, and Point 1c, Section II, Part B of the Finance Ministry’s Circular No. 129/2008/TT-BTC of December 26, 2008, on VAT, guide: “International transportation means transportation of passengers, luggage and cargoes along international routes from Vietnam to abroad or vice versa. In case an international transportation contract covers also a domestic stage, international transportation covers also domestic routes.”

For international transportation by road: According to the Transport Ministry’s opinions in Document No. 6757/BGTVT-HTQT of September 29, 2009, under the provisions of road transportation agreements which Vietnam has signed with foreign countries, an international transportation route means a route has a departing or a starting point on the Vietnam’s territory and the remaining point of the route on the territory of the country which has signed the agreement with Vietnam.

Under the above provisions, in case a transportation enterprise transports cargoes from Vietnam to aboard by road under contracts, of which domestic stage accounts for 80-95% of the entire route length and one point of the route lying on the Vietnam’s territory and the remaining point lying on the territory of a foreign country, its transportation is also regarded as international transportation and its international transportation turnover is eligible for the VAT rate of 0% if satisfying the conditions specified in Article 1 of the Finance Ministry’s Circular No. 112/2009/TT-BTC of June 2, 2009, guiding the conditions for application of the VAT rate of 0% on international transportation, aviation and maritime services.

Above is the General Department of Taxation’s reply to the inquiry of the Tax Department of Quang Tri province and the Vietnam Steel Corporation.

|

|

FOR

THE GENERAL DIRECTOR OF TAXATION |