Nội dung toàn văn Official Dispatch No. 6905/TC-TCHQ of June 8, 2005, on taxes on transferred diplomatic automobiles

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 6905/TC-TCHQ |

Hanoi, June 8, 2005 |

|

To: |

- Ministries,

ministerial-level agencies and government-attached agencies |

In order to solve problems arising in the course of implementation of Circular No. 87/2004/TT-BTC of August 31, 2004, the Finance Ministry hereby guides the provincial/municipal Customs Departments in uniformly implementing the following contents:

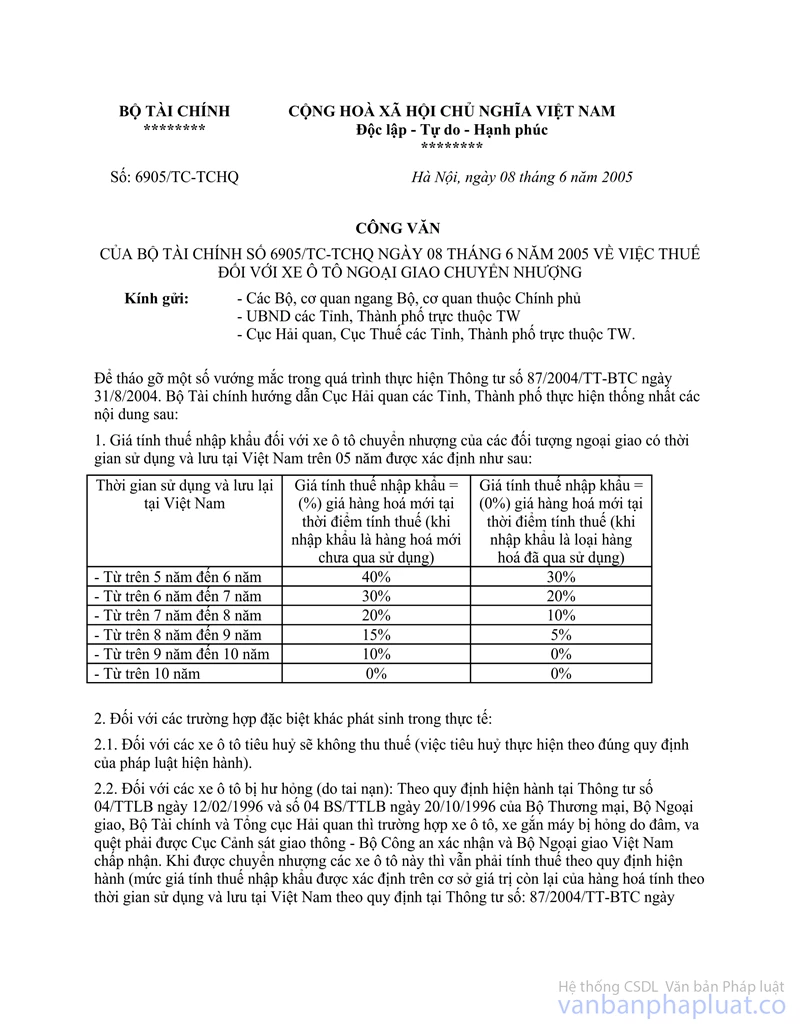

1. Prices for calculation of import duties on transferred automobiles of diplomats which have been used and retained in Vietnam for more than 5 years are determined as follows:

|

Period of use and retention in Vietnam |

Import duties calculation prices = (%) prices of brand-new commodities at the time of tax calculation (when being imported they are unused commodities) |

Import duties calculation prices = (0%) prices of brand-new commodities at the time of tax calculation (when being imported they are used commodities) |

|

- Between over 5 years and 6 years |

40% |

30% |

|

- Between over 6 years and 7 years |

30% |

20% |

|

- Between over 7 years and 8 years |

20% |

10% |

|

- Between over 8 years and 9 years |

15% |

5% |

|

- Between over 9 years and 10 years |

10% |

0% |

|

- Over 10 years |

0% |

0% |

2. For other special cases which may occur in reality:

2.1. For to be-destroyed automobiles, no tax shall be imposed (the destruction shall strictly comply with the current provisions of law).

2.2. For damaged automobiles (due to accidents): According to the current provisions of Joint Circulars No. 04/TTLB of February 12, 1996 and No. 04/BS/TTLB of October 20, 1996 of the Trade Ministry, the Foreign Affairs Ministry, the Finance Ministry and the Customs General Department, cases where automobiles and motorbikes are damaged due to collisions and crashes must be certified by the Traffic Police Department of the Public Security Ministry and accepted by the Foreign Affairs Ministry. When being transferred, these automobiles must still be taxed according to the current regulations (the import duties calculation prices are determined on the basis of the remaining values of commodities calculated according to their use and retention durations in Vietnam in compliance with the provisions of Circular No. 87/2004/TT-BTC of August 31, 2004 and the duties calculation prices additionally specified in Section 1 of this Official Letter applicable to automobiles used and retained in Vietnam for more than 5 years).

Payable tax amounts (including import duties, special consumption tax and VAT) shall be reduced according to extent of accident-caused damage. The provincial/municipal Customs Departments shall base themselves on accident-caused damage extents already assessed by the Vietnam Superintendence and Inspection Joint-Stock Company (Vinacontrol) and the relevant dossiers to consider tax reduction.

3. Bases for tax calculation and retrospective collection include the tax rate and tax calculation prices at the time of transfer (the time when involved parties carry out transfer procedures at customs offices). For cases where the transfer has been permitted by the competent state agency but the involved parties fail to come to customs offices to carry out procedures for transfer and tax payment declaration within 2 days according to the provisions of Point 3, Section II, Part E of Circular No. 87/2004/TT-BTC of August 31, 2004, they shall be sanctioned according to the provisions of the Import Duties and Export Duties Law and guiding documents.

4. This Official Letter takes effect on the effective date of the Finance Ministry's Circular No. 87/2004/TT-BTC of August 31, 2004.

The Finance Ministry notifies the provincial/municipal Customs Departments thereof for knowledge and implementation.

|

|

Truong Chi Trung |