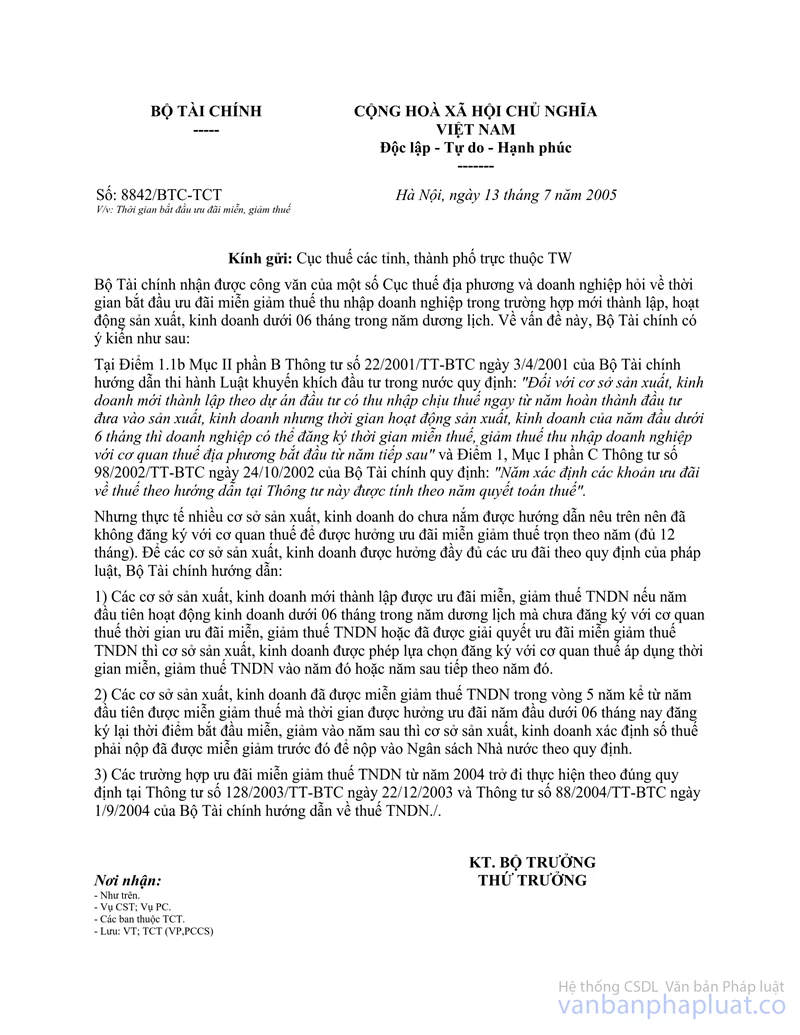

Nội dung toàn văn Official Dispatch No. 8842/BTC-TCT of July 13, 2005, on the starting time of tax exemption or reduction preferences

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIET NAM |

|

No. 8842/BTC-TCT |

Hanoi, July 13, 2005 |

To: Provincial/municipal Tax Departments

The Finance Ministry has received official letters from some Provincial/ Municipal Tax Departments and enterprises questioning about the starting time of business income tax exemption or reduction preferences in case the enterprises have been newly set up and carried out production and/or business operations for less than 6 months of a calendar year. Concerning this matter, the Ministry hereby expresses its opinions as follows:

Point 1.1b, Section II, Part B of the Finance Ministry’s Circular No. 22/2001/TT-BTC of April 3, 2004 guiding the Domestic Investment Promotion Law stipulates: “With regard to production and/or business establishments which have been newly set up under investment projects and generate taxable income right in the year of completing their investment and starting their production and/or business, but their production and/or business time in the first year is less than 6 months, they can register the time to enjoy business income tax exemption or reduction preferences with local tax offices from the subsequent year.” Meanwhile, Point 1, Section I, Part C of its Circular No. 98/2002/TT-BTC of October 24, 2002, states: “The year for determination of tax preferences under the guidance in this Circular shall be the tax-finalization year.”

However, due to the fact that many production and/or business establishments fail to fully grasp the above instructions, they have not registered with tax offices to enjoy tax reduction and exemption preferences for the whole year (12 months). In order to help such establishments enjoy every preference provided for by law, the Finance Ministry provides the following guidance:

1. Newly-set up production and/or business establishments eligible for business income tax reduction and exemption preferences, which in the first calendar year operate for less than 6 months and have not yet registered the time to enjoy business income tax exemption or reduction with tax offices or have already enjoyed such preferences, shall be permitted to register this time in either that year or the year following that year.

2. If production and/or business establishments have enjoyed business income tax reduction and exemption preferences for 5 years since the first year they are entitled thereto but this first year’s period of preferences was less than 6 months, and they now wish to reregister the time to start enjoying such preferences from the next year, they shall have to define the already exempted or reduced tax amounts for remittance to the state budget in accordance with the provisions of law.

3. Cases eligible for business income tax exemption or reduction from the year 2004 onwards shall have to strictly comply with the provisions of the Finance Ministry’s Circular No. 128/2003/TT-BTC of December 22, 2003 and Circular No. 88/2004/TT-BTC of September 1, 2004 guiding the business income tax.

|

|

Truong Chi Trung |