Nội dung toàn văn Official Dispatch No. 958/TCT-TNCN on dealing with problems in personal income

|

GENERAL

DEPARTMENT OF TAXATION |

SOCIALIST REPUBLIC OF VIET NAM |

|

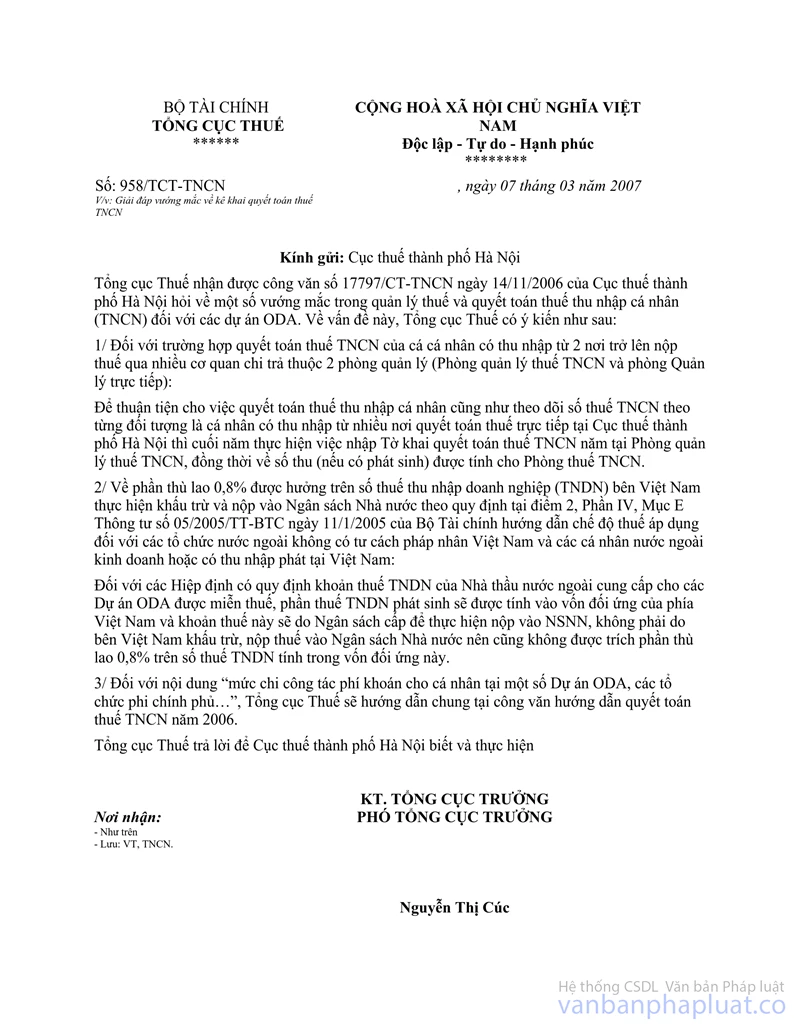

No. 958/TCT-TNCN |

Hanoi, March 07, 2007 |

OFFICIAL LETTER

ON DEALING WITH PROBLEMS IN PERSONAL INCOME TAX DECLARATION AND FINALIZATION

To: The Tax Department of Hanoi

The General Department of Taxation received Official Letter No. 17797/CT-TNCN of November 14, 2006, of the Tax Department of Hanoi, on problems in the management and finalization of personal income tax (PIT) for ODA-funded projects. Concerning this issue, the General Department of Taxation expresses the following opinions:

1. Finalization of PIT on individuals who have incomes generated in two or more places and pay PIT through many income-paying agencies under control of two management sections (the PIT Management Section and the Direct Management Section):

In order to facilitate the finalization of PIT and the monitoring of the PIT amount of each individual who has incomes generated in different places and finalizes PIT directly at the Tax Department of Hanoi, at year end, annual PIT finalization declarations shall be processed by the PIT Management Section and the collected PIT amounts (if any) shall be accounted for the PIT Section.

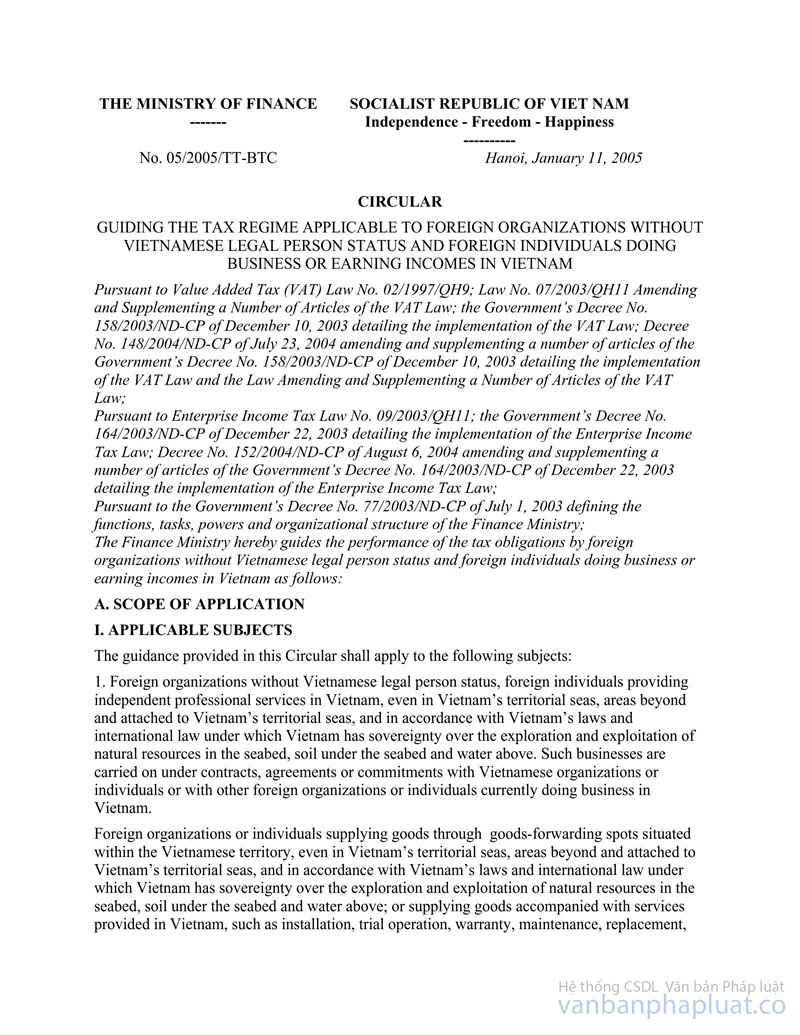

2. Regarding the remuneration equal to 0.8% of the business income tax (BIT) amount withheld and remitted by the Vietnamese party into the state budget under Point 2, Part IV, Section E of the Finance Ministry’s Circular No. 05/2005/TT-BTC of January 11, 2005, guiding the tax regulations applicable to foreign organizations without Vietnamese legal person status and foreign individuals doing business or earning incomes in Vietnam:

For ODA agreements which stipulate that foreign contractors supplying goods for ODA-funded projects are eligible for BIT exemption, the BIT amounts due shall be included in the contributed domestic capital of the Vietnamese party. These amounts shall be allocated from the budget for remittance into the state budget but not withheld or remitted by the Vietnamese party into the state budget. Therefore, the remuneration equal to 0.8% of the BIT amounts included in the domestic capital cannot be deducted.

3. For package working-mission allowances for individuals working for ODA-funded projects and in non-governmental organizations, the General Department of Taxation shall provide guidance in an official letter guiding PIT finalization for 2006.

The General Department of Taxation would like to give its reply to the Tax Department of Hanoi for information and compliance.

|

|

FOR THE GENERAL DIRECTOR OF

TAXATION |