Nội dung toàn văn Official Dispatch No. 9976/BTC-TCT 2013 on VAT refund examination

|

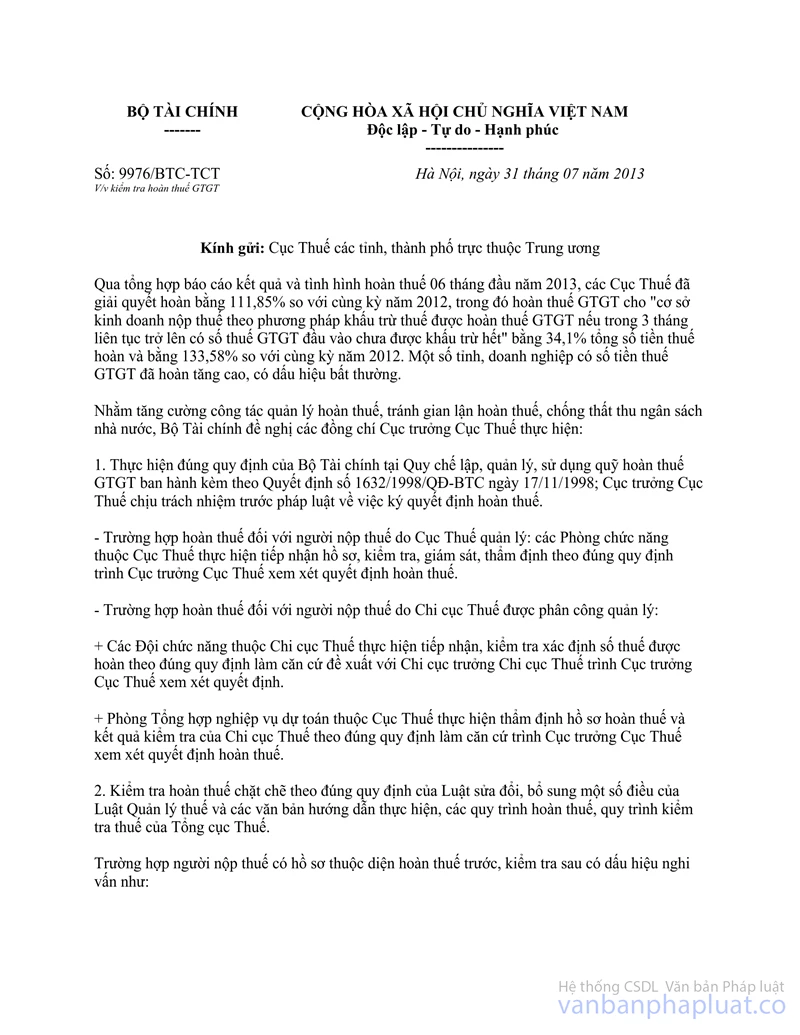

THE MINISTRY

OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 9976/BTC-TCT |

Hanoi, July 31, 2013 |

Respectfully to: Taxation Departments of provinces and central-affiliated cities

Through the summing report about results and status of tax refund in 06 first months of 2013, the Taxation Departments have solved equal to 111.85% in comparison with amount of the same period in 2012, in which the refunded VAT amounts of “facilities trading and paying tax under method of tax deduction and refunded VAT” if in 03 consecutive months or more, facilities have the input VAT amounts which have not yet been deducted entirely” are equal to 34.1% of total refunded taxation amounts and equal to 133.58% in comparison with the same period in 2012. Some provinces and enterprises had raised the refunded VAT amounts at high level, with irregular signs.

With the aim to strengthen management of tax refund, prevention of tax refund fraud, prevention of state budget revenue loss, the Ministry of Finance request Directors of Taxation Departments for implementing:

1. Complying with provisions of the Ministry of Finance at Regulations of establishment, management and use of VAT refund Fund promulgated together with Decision No. 1632/1998/QD-BTC dated November 17, 1998; Directors of Taxation Departments shall be responsible before law for signing on the tax refund decisions.

- Tax refund cases for taxpayer under management of Taxation Departments: Functional divisions under Taxation Departments shall receive dossiers, examine, supervise, appraise in accordance with regulations and submit them to the Directors of Taxation Departments for consideration and issue of tax refund decisions.

- Tax refund cases for taxpayer under management of Taxation Sub-Departments:

+ Functional teams under Taxation Sub-Departments shall receive dossiers, examine, and define the tax amount of refund in accordance with regulations as the basis for proposing them to the Directors of Taxation Sub-Departments for submission to Directors of Taxation Departments for consideration and decision.

+ The division of summing estimation operations under Taxation Departments shall appraise dossiers of tax refund and examination result of Taxation Sub-Departments in accordance with regulations as the basis for submitting them to the Directors of Taxation Departments for consideration and decision of tax refund.

2. Strictly examining tax refund in accordance with provisions of Law on amending and supplementing a number of articles of Law on tax administration, and documents guiding implementation, processes of tax refund, process of tax examination of the General Department of Taxation.

If a taxpayer with dossier in condition of tax refund prior to examination has doubtful signs as follows:

- It is an enterprise with charter capital, equity capital less than scale of business turnover, in comparison with the tax amounts requested for refund.

- It is a facility of production and trading newly established within 24 months backwards.

- It is a trading enterprise without material facilities (factories, production workshops, warehouses, means of transport, system of stores…)

- Enterprise is established in a locality but activities of product and goods purchase and sale (especially agricultural goods) produced in other locality with irregular signs.

- It is an enterprise which trade in and purchase goods in serve of export mainly from trading enterprises, enterprises just established, organizations and individuals collecting goods which are agricultural, forest and fishery products not subject to input VAT.

- It is an enterprise conducting payment of export goods and services from current accounts.

- Enterprises of the buyer and the seller which have relationships of spouse, brothers and sisters, linkage relationship with irregular signs.

For the above cases, taxation agencies must have written request to the taxpayer for providing explanations, supplementations as the basis for the tax refund decision; if the taxpayer fails to provide explanations, supplementations, or provides explanations, supplementations which fail to prove that the declared tax amounts are right, has tax refund fraudulent signs, dossiers must be transferred into subject of examination prior to tax refund.

Dossiers of VAT refund must remove the input VAT amounts not eligible for deduction, tax refund due to failing payment via bank and provided that decision of tax refund is issued in accordance with provisions of Law on VAT.

Examining and defining properly refunded tax amounts (case where “business facilities paying tax under method of tax deduction are eligible for VAT refund, if in 3 consecutive months or more, they have input VAT amounts which have not yet been deducted entirely” as specified in Clause 1 Article 18 of the Circular No. 06/2012/TT-BTC dated January 11, 2012 of the Ministry of Finance, guiding the implementation of a number of articles of the Law on value-added tax, guiding the implementation of the Decree No. 123/2008/ND-CP of December 08, 2008 and the Decree No. 121/2011/ND-CP of December 27, 2011 of the Government, defining the refunded tax amounts in accordance with guide of the General Department of Taxation at the Official dispatch No. 1027/TCT-KK dated March 23, 2012, excluding content “input VAT of goods purchased for export not processed, produced, such goods will be considered for tax refund after goods have been exported in reality”).

3. For taxpayers with the refunded tax amounts rising suddenly (over 10% in comparison with the same period of previous year), there is risky sign in tax refund, taxation agencies should clarify reason, focus on examination before and after tax refund, in combination with examination and inspection wholly over all activities of production and trading as well as obligations of paying other tax kinds of taxpayer, preventing status of misusing, conducting frauds in tax refund, preventing the state budget's revenue lost.

(According to tax refund result report of 06 first months in 2013, some enterprises have the refunded tax amounts for case of “facilities trading and paying tax under method of tax deduction and refunded VAT if in 03 consecutive months or more, facilities have the input VAT amounts which have not yet been deducted entirely” rising suddenly such as enterprises under localities managed by Taxation Departments of: Hung Yen, Ha Noi city, Ho Chi Minh city, Dong Nai,…)

4. Strengthening the tax examination, inspection according to guide of the Ministry of Finance at the Official dispatch No. 7527/BTC-TCT dated June 12, 2013 with the aim to remove tax amounts not eligible for tax deduction and refund.

5. During the course of tax refund management in localities, monthly, quarterly, biannually, and annually, taxation agencies shall monitor, assess the tax refund result and status, detect cases of tax refund rising suddenly, with risky sign so as to apply measures to strengthen inspection, examination, supervision, concurrently report to superior taxation agencies for information and summing in general assessment.

The Ministry of Finance notifies Taxation Departments for information and execution.

|

|

FOR THE

MINISTER OF FINANCE |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments