Circular No. 97/2012/TT-BTC of June 18, 2012, guiding the collection, transfer and management of fees for issuing working holiday licenses to New Zealand’s citizens đã được thay thế bởi Circular 140/2016/TT-BTC collection payment fees issuance working holiday permits new zealand australia và được áp dụng kể từ ngày 01/01/2017.

Nội dung toàn văn Circular No. 97/2012/TT-BTC of June 18, 2012, guiding the collection, transfer and management of fees for issuing working holiday licenses to New Zealand’s citizens

|

THE MINISTRY OF

FINANCE |

THE SOCIALIST REPUBLIC OF VIETNAM |

|

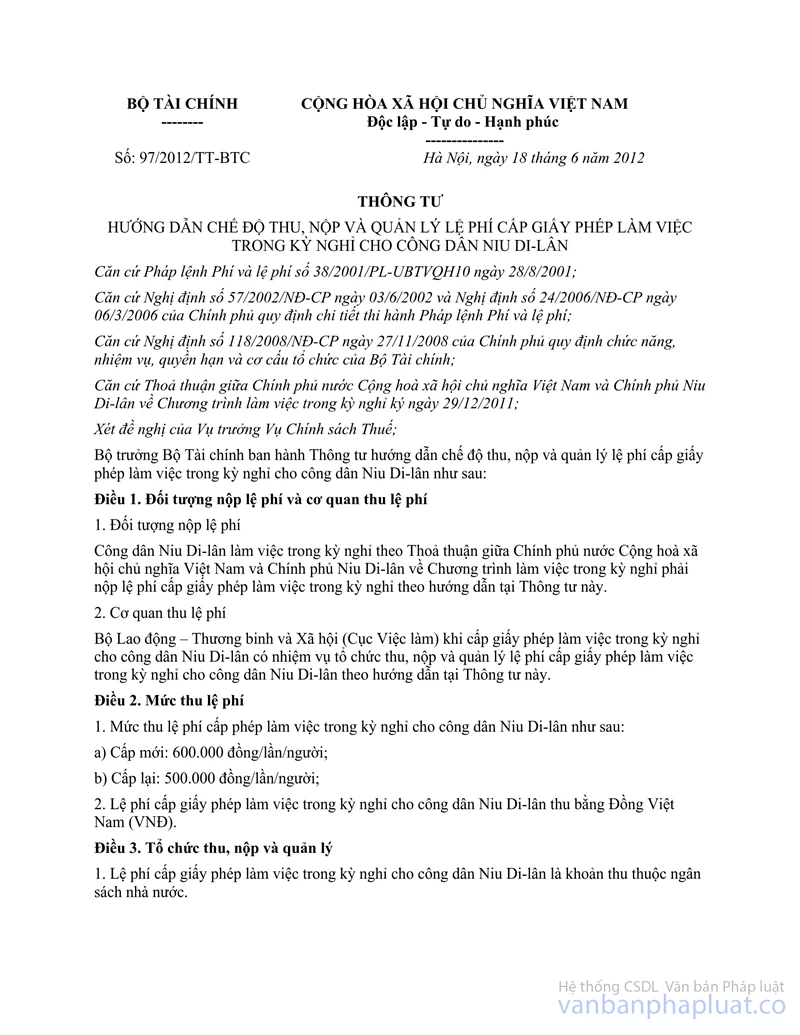

No. 97/2012/TT-BTC |

Hanoi, June 18, 2012 |

CIRCULAR

GUIDING THE COLLECTION, TRANSFER AND MANAGEMENT OF FEES FOR ISSUING WORKING HOLIDAY LICENSES TO NEW ZEALAND’S CITIZENS

Pursuant to the Ordinance on Fees and Charges No. 38/2001/PL-UBTVQH10 dated August 28, 2001;

Pursuant to the Government's Decree No. 57/2002/ND-CP dated June 03, 2002, and Decree No. 24/2006/ND-CP dated March 06, 2006, detailing the implementation of the Ordinance on Fees and charges;

Pursuant to the Government's Decree No. 118/2008/ND-CP dated November 27, 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

Pursuant to the Agreement between the Government of the Socialist Republic of Vietnam and the Government of New Zealand on the Working Holiday Scheme signed on December 29, 2011;

At the proposal of the Director of the Tax Policy Department;

The Minister of Finance promulgates the Circular guiding the collection, transfer and management of fees for issuing working holiday licenses to New Zealand’s citizens.

Article 1. Fee payers and fee-collecting agencies

1. Fee payers

New Zealand’s citizens who work during their holidays according to the Agreement between the Government of the Socialist Republic of Vietnam and the Government of New Zealand on the Working Holiday Scheme must pay the fee for issuing the working holiday license as guided in this Circular.

2. Fee-collecting agencies

When issuing working holiday licenses to New Zealand’s citizens, the Ministry of Labor, War Invalids and Social Affairs (The Bureau of Employment) must collect, transfer and manage of the fees for issuing the licenses as guided in this Circular.

Article 2. Fee rates

1. The fee rates for issuing working holiday licenses to New Zealand’s citizens::

a/ New issuance: VND 600,000 VND/time/ person;

b/ Re issuance: VND 500,000 VND/time/person;

2. Fees for issuing working holiday licenses to New Zealand’s citizens shall be collected in Vietnam dong (VND).

Article 3. Fee collection, transfer and management

1. Fees for issuing working holiday licenses to New Zealand’s citizens are State budget receipts.

2. The agencies that collect fee for issuing working holiday licenses to New Zealand’s citizens must register, declare and transfer the collected amount to the State budget in accordance with the Ministry of Finance's Circular No. 63/2002/TT-BTC dated July 24, 2002, and Circular No. 45/ 2006/TT-BTC dated May 25, 2006, amending and supplementing Circular No. 63/2002/TT-BTC of July 24, 2012, guiding the law provisions on fees and charges.

3. Fee-collecting agencies shall transfer 100% (one hundred percent) of collected amount to the State budget according to the corresponding chapter, category, clause, item and sub-item of the current State Budget Index.

4. Central budget shall be allocated to regular expenditure estimates of the Ministry of Labor, War Invalids and Social Affairs to defray the expenses on the fee collection and the issuance of working holiday licenses to New Zealand’s citizens. At the time of making annual State budget estimates, the Ministry of Labor, War Invalids and Social Affairs shall make the expenditure estimates for the fee collection and the issuance of working holiday licenses to New Zealand’s citizens, include them in the state budget expenditure estimates and send it to the Ministry of Finance as prescribed.

Article 4. Implementation organization

1. This Circular takes effect on August 2, 2012.

2. Other matters related to fee collection, transfer, management and announcement of the fee collection regime not being specified in this Circular must comply with the Ministry of Finance's Circular No. 63/2002/TT-BTC dated July 24, 2012, and Circular No. 45/2006/TT-BTC dated May 25,2006, amending and supplementing Circular No. 63/2002/TT-BTC dated July 24,2002, guiding the law provisions on fees and charges; Circular No. 28/2011/TT-BTC dated February 28, 2011, guiding a number of articles of the Law on Tax Administration, and the Government's Decree No. 85/2007ND-CP dated May 25, 2007, and the Decree No. 106/2010/ND-CP dated October 28, 2010.

3. Fee payers and other relevant agencies are responsible for implementing this Circular. Organizations and individuals are recommended to send feedbacks on the difficulties arising during the course of implementation to the Ministry of Finance for consideration and settlement./.

|

|

FOR THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments