Nội dung toàn văn Circular No. 140/2012/TT-BTC guiding the Government's Decree No. 60/2012/ND-CP

|

THE MINISTRY OF

FINANCE |

SOCIALIST REPUBLIC

OF VIETNAM |

|

No. 140/2012/TT-BTC |

Hanoi, August 21, 2012 |

CIRCULAR

GUIDING THE GOVERNMENT'S DECREE NO. 60/2012/NĐ-CP DATED JULY 30, 2012, DETAILING THE IMPLEMENTATION OF THE NATIONAL ASSEMBLY’S RESOLUTION NO. 29/2012/QH13 PROMULGATING A NUMBER OF TAX POLICIES TO HELP ORGANIZATIONS AND INDIVIDUALS RESOLVE THEIR DIFFICULTIES

Pursuant to the Law on Tax administration No. 78/2006/QH11 dated November 29, 2006.

Pursuant to the Law on Personal income tax No. 04/2007/QH12 dated November 21, 2007;

Pursuant to the Law on Value-added tax No. 13/2008/QH12 dated June 03, 2008;

Pursuant to the Law on Enterprise income tax No. 14/2008/QH12 dated June 03, 2008;

Pursuant to the National Assembly’s Resolution No. 29/2012/QH13 dated June 21, 2012 promulgating a number of tax policies to help organizations and individuals resolve their difficulties

Pursuant to the Government's Decree No. 60/2012/NĐ-CP dated July 30, 2012, detailing the implementation of the National Assembly’s Resolution No. 29/2012/QH13 promulgating a number of tax policies to help organizations and individuals resolve their difficulties;

Pursuant to the Government's Decree No. 118/2008/NĐ-CP dated November 27, 2008 on defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

At the proposal of the Director of the General Department of Taxation;

The Minister of Finance promulgates the Circular guiding the Government's Decree No. 60/2012/NĐ-CP dated July 30, 2012, detailing the implementation of the National Assembly’s Resolution No. 29/2012/QH13 promulgating a number of tax policies to help organizations and individuals resolve their difficulties;

Chapter I

ENTERPRISE INCOME TAX

Article 1. Enterprise income tax reduction

1. Reducing 30% enterprise income tax in 2012 for:

a) Medium and small enterprises, including cooperatives (hereinafter referred to as medium and small enterprises).

a) Intensive-labor enterprises that produce or process agricultural products, forestry products, aquatic products, textile and garment, leather and footwear, electronic components, or build socio-economic infrastructure (hereinafter referred to as intensive-labor enterprises).

2. The medium and small enterprises prescribed in Point a Clause 1 this Article are enterprises that satisfy the standards of capital or labor as prescribed in Clause 1 Article 3 of the Government's Decree No. 56/2009/NĐ-CP dated June 30, 2009 of development support for medium and small enterprises.

a) The amount of capital for calculating the reduction of the enterprise income tax amount payable in 2012 of medium and small enterprises is the total capital shown in the Balance sheet made on December 31, 2011 of the enterprise. For enterprises of which the tax period in the fiscal year 2011 is different from the calendar year, the amount of capital for calculating the reduction of the enterprise income tax amount payable in 2012 of medium and small enterprises is the total capital shown in the Balance sheet made on the last day of the tax period in the fiscal year.

For medium and small enterprises established on January 01, 2012 or later, the amount of capital for calculating the reduction of the enterprise income tax amount payable in 2012 of medium and small enterprises is the charter capital written in the Enterprise registration certificate or the First investment certificate.

b) The annual average number of employees (including the employee of the branches and affiliated units) for determining whether the enterprise is eligible for tax reduction prescribed in Point a Clause 1 this Article is the total number of employees that the enterprise regularly employs in 2011, excluding employees signing short-term contracts under 3 months

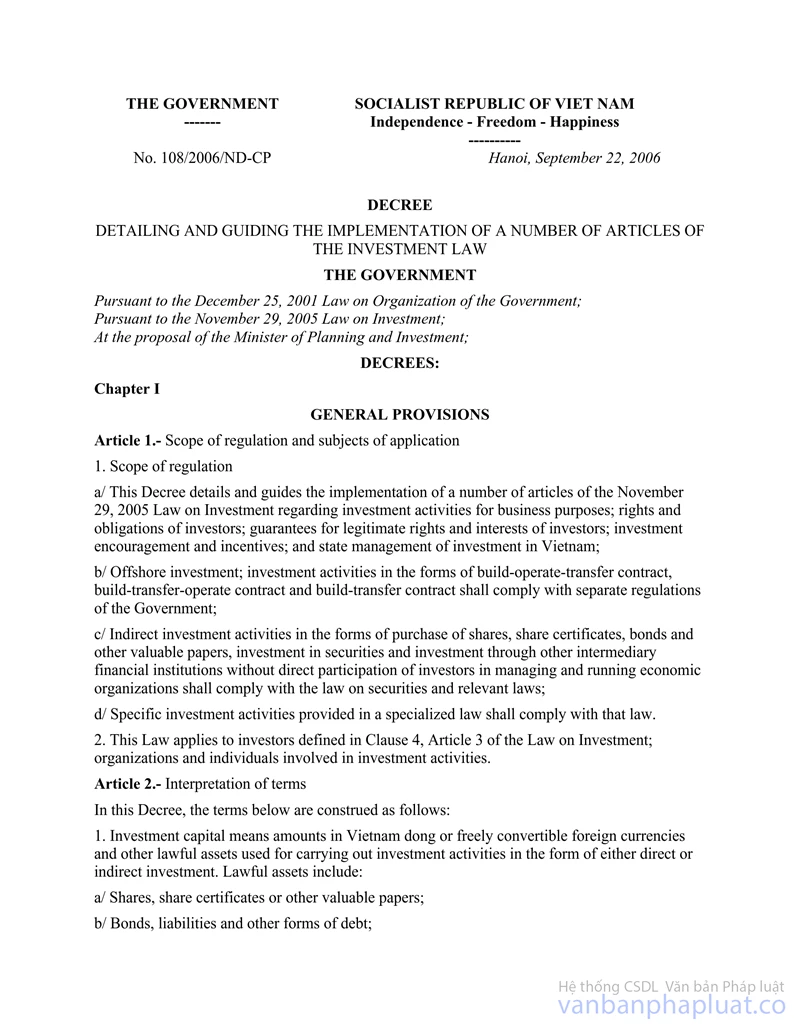

The annual average number of regular employees is calculated as guided in the Circular No. 40/2009/TT-BLĐTBXH dated December 03, 2012 of the Ministry of Labor, War Invalids and Social Affairs, on guiding the calculation of the number of regular employees as prescribed in the Government's Decree No. 108/2006/NĐ-CP dated September 22, 2006 on detailing and guiding the implementation of a number of articles of the Law on investment.

For the enterprises established on January 01, 2012 and later, the total number of employees, excluding employees signing short-term contracts under 3 months, is the average number of regular employees from the date of establishment until December 31, 2012.

c) For enterprises engaged in various sectors, the determination of whether they are medium and small enterprises to determine the capital or labor criteria as prescribed in the Decree No. 56/2009/NĐ-CP is based on the primary business line written in their Enterprise registration certificates. If the primary business line is not determined, one of the following criteria shall apply to determine its primary business line:

- The highest number of employees in each business of the enterprise in 2011; or

- The highest revenue in each business of the enterprise in 2011.

If the primary business line is not determined after applying the criteria above, it is required to take apply the criteria for capital or the lowest number of employees of the business line in the business lines that the enterprise engages in 2011 as prescribed in Clause 1 Article 3 of the Decree No. 56/2009/NĐ-CP

d) For enterprises following the model of parent companies – subsidiary companies that the parent companies are not medium and small enterprises holding more than 50% equity capital of subsidiary companies, if subsidiary companies are able to satisfy the capital or labor criteria prescribed in Clause 1 Article 3 of the Decree No. 56/2009/NĐ-CP and do not engage in the business lines ineligible for tax reductions, they are also eligible for 30% reduction of the enterprise income tax payable in 2012.

3. Intensive-labor enterprises (including the employees of branches and affiliated units) that engage in the business lines eligible for tax reduction guided in Point b Clause 1 this Article include:

a) Enterprises established before January 01, 2012, of which the annual average number of regular employees in 2012 is over 300 people, excluding employees signing short-term contracts under 3 months.

The annual average number of regular employees is calculated as guided in the Circular No. 40/2009/TT-BLĐTBXH dated December 03, 2012 of the Ministry of Labor, War Invalids and Social Affairs, on guiding the calculation of the number of regular employees as prescribed in the Government's Decree No. 108/2006/NĐ-CP dated September 22, 2006 on detailing and guiding the implementation of a number of articles of the Law on investment.

For the enterprises established on January 01, 2012 and later, the total number of employees, excluding employees signing short-term contracts under 3 months, is the average number of regular employees over 300 people from the date of establishment until December 31, 2012.

For enterprises following the model of parent companies – subsidiary companies, the number of employees for determining whether the parent company is eligible for tax reduction does not include the number of employees of subsidiary companies, and vice versa.

b) The reduced enterprise income tax is the tax on the income of the production and processing of agricultural products, forestry products, aquatic products, textile and garment, leather and footwear, electronic components, or the construction of socio-economic infrastructure.

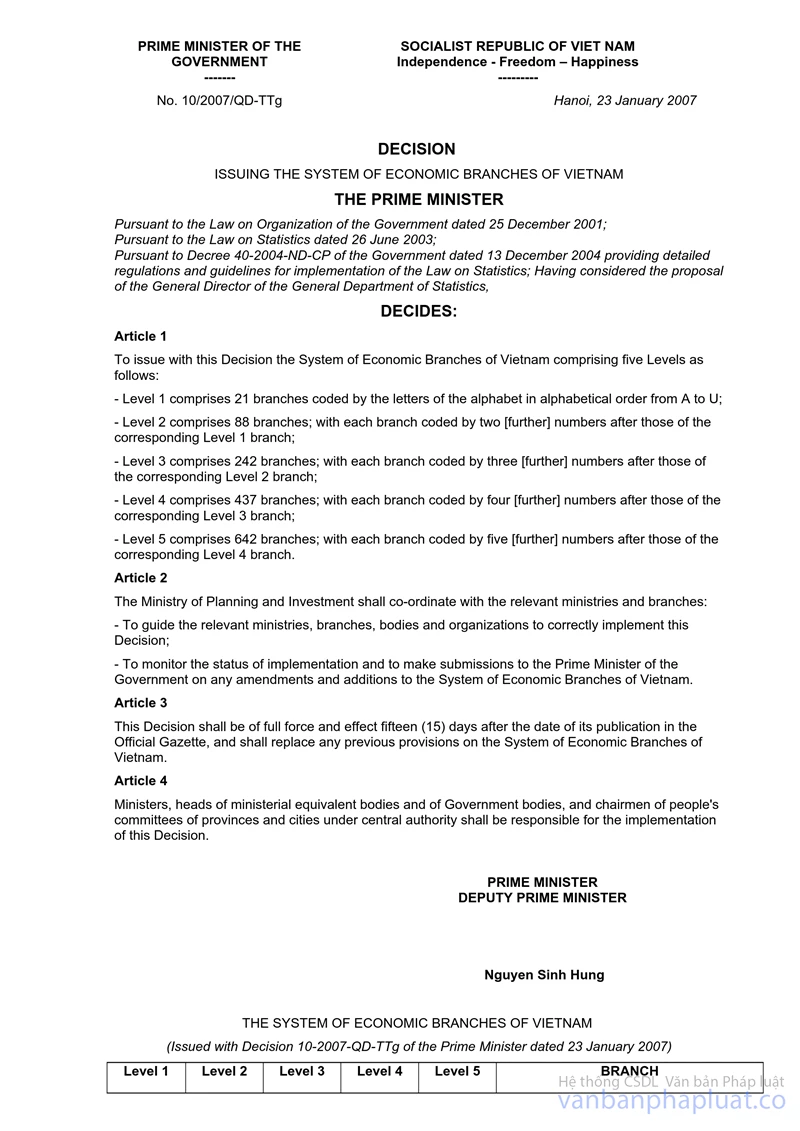

c) The production and processing of agricultural products, forestry products, aquatic products, textile and garment, leather and footwear (including leather shoes and slippers), electronic components are identified according to the Vietnam’s system of business lines, promulgated together with the Prime Minister’s Decision No. 10/2007/QĐ-TTg dated January 23, 2007.

d) The construction of socio-economic infrastructure includes the construction and installation of water plants, power plants, electricity distribution and transmission constructions, water supply and drainage system; roads, railroads, airports, sea ports, river ports, train stations, bus stations, schools, hospitals, cultural houses, cinemas, art performance centers, sports stadiums, sewage and solid waste treatment systems, communication constructions, irrigation serving agriculture, forestry and fishery.

4. Enterprise income tax reduction prescribed in Point a Clause 1 this Article is not applicable to the following subjects:

a) Medium and small enterprises engaged in lottery, real estate, securities, finance, banking, insurance, production and provision of goods and services subject to special excise duty.

Medium and small enterprises engages in various business lines, the enterprise income tax reduce does not include the tax on the income from the business of lottery, real estate, securities, finance, banking, insurance, production and provision of goods and services subject to special excise duty.

b) Enterprises ranked among the class I as prescribed in the Circular No. 23/2005/TTLT-BLĐTBXH-BTC dated August 31, 2005 by the Ministry of Labor, War Invalids and Social Affairs and the Ministry of Finance guiding the rating and salaries of members of the Board of Directors, General Directors, Directors, Deputy General Directors, Deputy Directors, Chief accountants of State-owned companies.

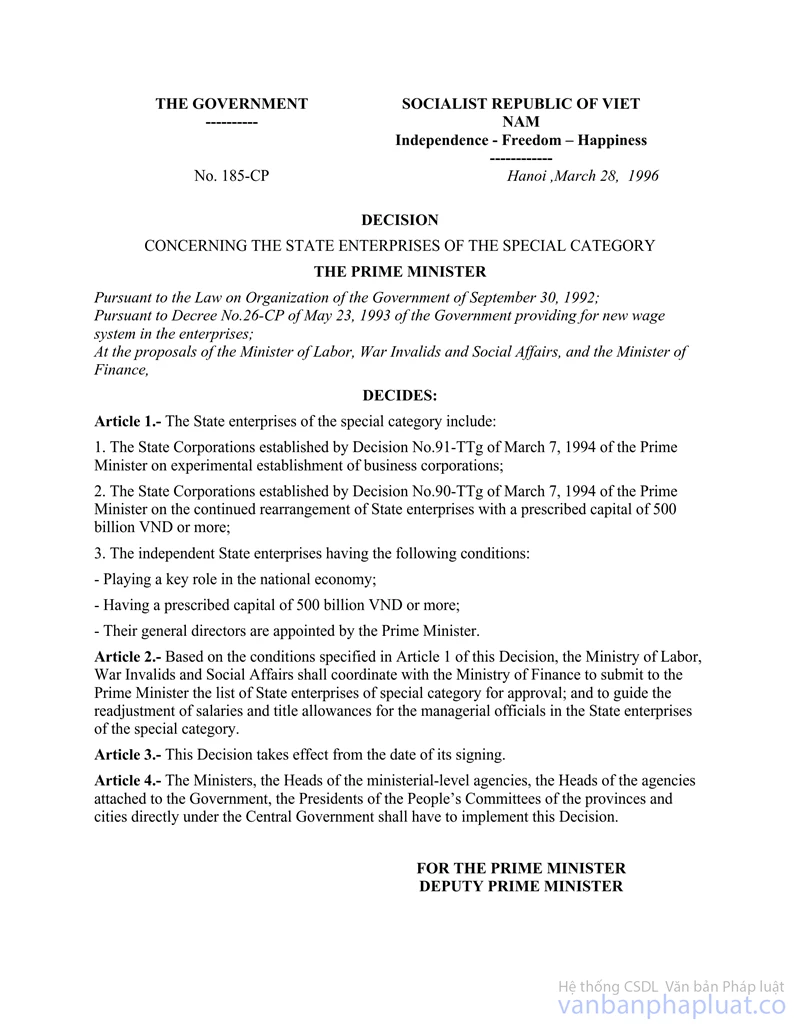

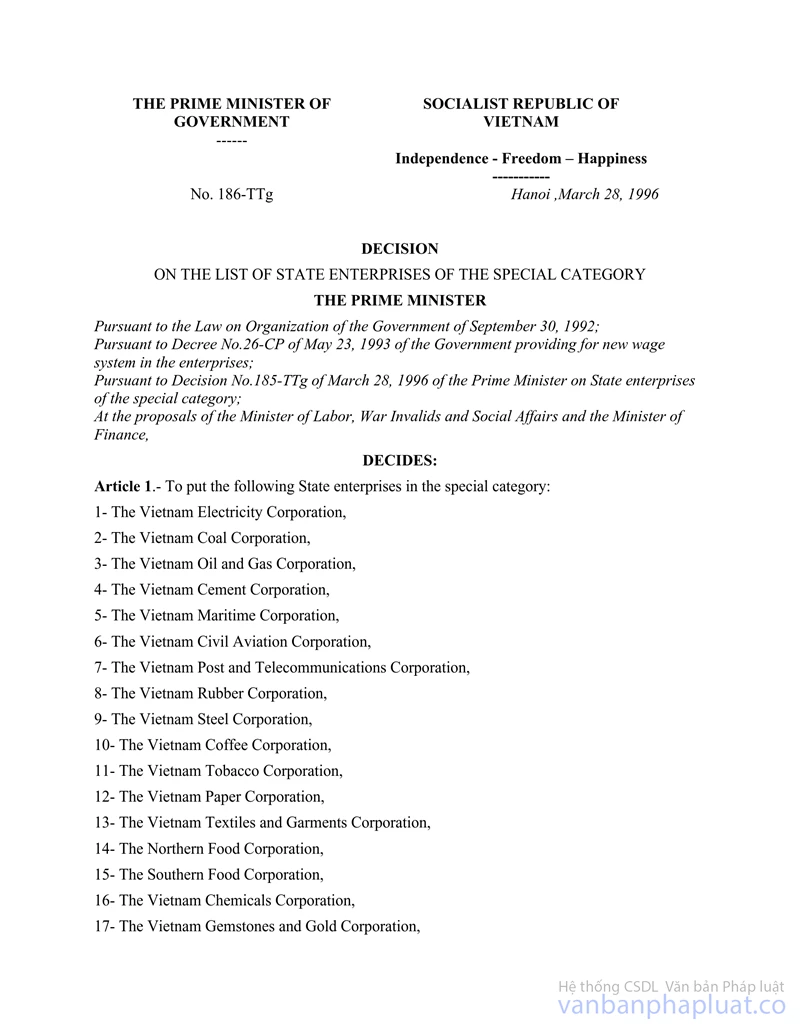

c) Enterprises ranked among the Special class under the Prime Minister’s Decision No. 185/TTg dated March 28, 1996 on Special-class State-owned enterprises, and the Prime Minister’s Decision No. 186/TTg dated March 28, 1996 of the list of Special-class State-owned enterprises.

d) Economic organizations being non-business units.

Article 2. Enterprise income tax exemption

The enterprise income tax payable in 2012 on the income from doing catering for workers by catering enterprises.

Article 3. Conditions for enterprise income tax reduction and exemption

1. Enterprises and organizations eligible for tax exemption and reduction as prescribed in Article 1 and Article 2 of this Circular are units being legally established and run under Vietnam’s law, following the regulations on accounting and invoices, and paying tax according to the declaration.

2. For enterprises enjoying enterprise income tax incentives as prescribed by the Law on Enterprise income tax or legal documents on enterprise income tax, the reduced enterprise income tax prescribed in Article 1 of this Circular is calculated on the remaining amount of enterprise income tax after deducting the amount enterprise income tax eligible for incentives as prescribed.

3. Enterprises, organizations doing catering for workers are eligible for tax exemption as prescribed in Article 2 of this Circular must commit to keep the catering prices during 2012 not higher than the prices in December 2011. If competent agencies find that the enterprise or organizations does not implement their commitment, they will be no longer eligible for tax exemption as prescribed in Article 2 of this Circular.

If an enterprise doing catering for workers also a medium or small enterprise that is both eligible for 30% reduction of the enterprise income tax payable in 2012 as prescribed in Point a Clause 1 Article 1 of this Circular, and eligible for the exemption of the enterprise income tax in 2012 on the income from the provision of catering services for workers, the enterprise may choose the most beneficial tax incentive.

Article 4. Determination of the tax amount reduced and exempted

1. Enterprises and organizations must separately record the incomes from the production or business eligible for the exemption and reduction of enterprise income tax, and the production or business ineligible for the exemption and reduction of enterprise income tax. If the income from the activities eligible for tax exemption and reduction is not identifiable, the income for calculating the tax reduced or exempted is calculated on the ratio (%) of the income from the activities eligible for tax exemption and reduction to the total income of the enterprise or organization in 2012.

2. The reduced enterprise income tax amount prescribed in Clause 1 Article 1 of this Circular is the enterprise income tax preliminarily calculated quarterly, and the outstanding difference of enterprise income tax payable under the tax finalization in 2012 of the enterprise compared to the total tax amount preliminarily calculated quarterly.

3. The exempted enterprise income tax amount prescribed in Article this Circular is calculated as follows:

a) In case the enterprise or organization can determine the receipts, expenses, and taxable income from the provision of catering services for workers in 2012, the exempted enterprise income tax in 2012 on catering for workers is calculated on the enterprise income tax amount payable in 2012 calculated by the enterprise or organization.

b) If in the tax period 2012, the enterprise or organization does not separate the income from doing catering for workers and the income from the production or business ineligible for tax incentives, the income eligible for tax exemption in 2012 equals the total taxable income from the production or business (excluding other incomes) multiplied by (x) the ratio (%) of the income from doing catering for workers to the total revenue of the enterprise or organization in 2012.

c) The exempted enterprise income tax on the income from doing catering for workers does not include the tax on the income from doing catering for transport and aviation enterprises to serve passengers, and the tax on the income from other business.

Article 5. Tax declaration

1. Enterprises and organizations eligible for tax exemption and reduction as prescribed in Article 1 and Article 2 of this Circular shall declare the reduced and exempted tax in accordance with the Law on Tax administration and its guiding documents.

Enterprises and organizations must make and send the Annex on enterprise income tax exemption and reduction (form No. 01/MGT-TNDN promulgated together with this Circular) to the direct tax authorities, specifying that the enterprise or organization is eligible for enterprise income tax exemption or reduction, and the reduced or exempted enterprise income tax amount. Declaring the total reduced and exempted tax in the item [31] on the declaration sheet No. 01A/TNDN, or the item [30] on the declaration sheet No. 01B/TNDN, or the item [C9] on the declaration sheet No. 03/TNDN (promulgated together with the Circular No. 28/2011/TT-BTC dated February 28, 2011 by the Ministry of Finance).

2. Enterprises and organizations that have make declaration as prescribed but have not made tax exemption and reduction declaration as prescribed in Article 1 and Article 2 of this Circular may make additional tax declaration.

If the enterprise or organization makes the additional declaration in Q1/2012 and Q2/2012, the additional declaration of enterprise income tax exemption and reduction including the preliminary declaration of enterprise income tax in Q1/2012 and Q2/2012 that has been added the reduced or exempted tax amount; the Annex of Enterprise income tax exemption and reduction in Q1/2012 and Q2/2012 stated above.

The additional tax declaration sheet is submit to tax authorities on any working day, not depending on the time limit for submitting the next tax declaration, but before the tax authorities or competent agencies announce the decision on carrying out tax inspection at the tax payer’s office.

3. If a enterprise eligible for tax reduction has declared and paid the reduced tax amount in Q1 and Q2/2012 to the State budget, such enterprise may deduct the reduced tax amount from the tax amount payable in Q3 and Q4/2012, and the difference payable according to the tax finalization in 2012. If the deduction is not complete after the tax finalization in 2012, the enterprise may request to deduct it from the amount payable in the succeeding year, or request tax refund as prescribed by the Law on Tax administration and its guiding documents.

4. If a enterprise eligible for tax exemption has declared and paid the reduced tax amount in Q1 and Q2/2012 to the State budget, such enterprise may deduct the exempted tax amount from the tax amount payable in Q3 and Q4/2012, and the difference payable according to the tax finalization in 2012 of other business. If the deduction is not complete after the tax finalization in 2012, the enterprise may request to deduct it from the amount payable in the succeeding year, or request tax refund as prescribed by the Law on Tax administration and its guiding documents

5. Settling the difference of the reduced enterprise income tax in the tax finalization compared to the preliminary calculation of the quarterly enterprise income tax declaration

a) When finalizing enterprise income tax in 2012, if the reduced enterprise income tax amount is larger than the total reduced tax amount preliminarily calculated in Q4, the enterprise is eligible for reducing the reduction of the difference amount between the reduced tax amount according to the tax finalization and the total reduced tax amount according to the preliminary calculation in Q4/2012.

b) When finalizing enterprise income tax in 2012, if the reduced enterprise income tax amount is smaller than the total reduced tax amount preliminarily calculated in Q4, reduce tax amount is calculated according to the tax finalization.

6. When competent agencies inspect and discover that the enterprise income tax during the tax exemption and reduction period prescribed in Article 1 and Article 2 of this Circular is larger than that declared by the unit (including enterprises and organizations eligible for enterprise income tax exemption and reduction prescribed in this Circular that have made declarations but have not determined the reduced or exempted enterprise income tax amount), the enterprises and organizations are eligible for the exemption and reduction of the enterprise income tax (including the additional enterprise income tax and the undetermined enterprise income tax amount eligible for tax exemption and reduction prescribed in this Circular).

When competent agencies inspect and discover that the enterprise income tax eligible for tax exemption and reduction as prescribed in Article 1 and Article 2 of this Circular is smaller than that declared by the unit, the enterprises and organizations are only eligible for the exemption and reduction of the enterprise income tax amount discovered during the inspection.

Competent agencies shall impose the sanctions against the violations of law provisions on tax depending on the seriousness of violations.

Chapter II

VALUE-ADDED TAX

Article 6. Exemption of flat value-added tax in 2012 for business households and individuals

1. Flat value-added tax in 2012 is exempted for:

a) Households and individuals renting houses and rooms to workers, employees, and students;

b) Households and individuals providing day care services;

c) Households and individuals doing catering for workers.

2. Conditions for tax exemption

Business households and individuals eligible for tax exemption as prescribed in Article 1 must satisfy the following conditions:

- Paying value-added tax at a flat rate;

- Committed to sustain the rents, day care charges, and catering charges in 2012 not exceeding that in December 2011. For business households and business individuals commencing their business in 2012, the rents, day care charges and catering charges must not exceed that in December 2011 of business households and individuals doing the same business in the same locality that have been operated before 2012.

- Publicly posting the rents, day care charges, and catering charges in the business establishments, and notify the local authorities and direct tax authorities before November 01, 2012 of the maintenance of the charges not exceeding that in December 2012 from January 01, 2012.

3. Depending on the approved Tax Register 2012, tax authorities must make and report the list of individuals and households leasing rooms, houses, providing day care, and doing catering for workers, and the exempted tax amount, to People’s Committees at the same level and the superior tax authorities for monitoring and inspecting. Posting it at the tax authorities office before November 15, 2012, and notify the business households and individuals.

The business households and individuals eligible for flat value-added tax exemption that have paid the flat value-added tax of the months in 2012 to the State budget shall have the paid VAT amount refunded, or deduct it from the flat value-added tax in the succeeding year.

Tax authorities shall make the list of business households and individuals eligible for tax refund in each commune or ward, and send the Decision on tax refund to every business household and individual.

Tax authorities must make and post the list of individuals and households leasing rooms, houses, providing day care, and doing catering for workers, that are eligible for tax refund at the tax authorities office before November 15, 2012.

4. When the business households and individuals are discovered that they do not keep the commitment on charges specified above, they are no longer eligible for tax exemption, and must pay the tax arrears and fines for late payment as prescribed by law provisions on tax administration.

Article 7. Exemption of value-added tax payable in 2012 on doing catering for workers by catering enterprises.

1. The value-added tax payable in 2012 on the income from doing catering for workers is exempted (not including the catering for transport and aviation enterprises to serve passengers and other business).

2. Enterprises and organizations doing catering eligible for value-added tax exemption as prescribed in Article 1 must satisfy the following conditions:

- Being established and run under Vietnam’s law, following the regulations on accounting and invoices, and paying tax according to the declaration;

- Paying value-added tax under deduction method;

- Committed to maintain the catering charges in 2012 not exceeding that in December 2011 (for enterprises and organizations that have run in 2011 and earlier). For enterprises and organizations that commence their business in 2012, the catering charges must not exceed that in December 2011 of a organization or enterprise doing catering that have run in 2011 or earlier in the same locality.

- Publicly posting catering charges at the business establishments, and notify the local authorities and direct tax authorities before November 01, 2012.

3. In case an enterprise or organization doing catering for workers engages in various business, such enterprise or organization must separately declare the revenue, input value-added tax, and output value-added tax on the catering services to calculate the exempted value-added tax in 2012 on catering for workers.

The exempted value-added tax amount in each month in 2012 is calculated as follows:

|

Value-added tax payable on catering for workers. |

= |

Output value-added tax on catering for workers. |

- |

Deducted input value-added tax on catering for workers. |

Including:

a) The output value-added tax on catering for workers equals (=) the total value-added tax amount on the provided catering written on the VAT invoices.

The value-added tax written on the VAT invoice equals (=) the taxable charge for the catering for workers being provided multiplied by (x) the VAT rate (10%).

b) Calculating the deducted input value-added tax

- The input value-added tax on goods and services used for doing catering for workers are all deducted.

- If the input VAT on fixed assets, goods and services used for doing catering for workers is recorded separately, the deducted input VAT is calculated according to the amount separately recorded. In case it is not separated, the input VAT shall be deducted according to the ratio (%) of the revenue from doing catering for workers to the total revenue subject to VAT from the sold goods and services.

In case an enterprise or organization doing catering for workers engages in various business, and does not separately record the revenue, input value-added tax, and output value-added tax on the provision of catering services and on the provision of other goods and services, that results in being unable to accurately calculate the exempted VAT in the month, the exempted VAT is calculated as follows:

|

Exempted VAT |

= |

VAT payable according to the monthly declaration |

x |

Revenue subject to VAT from doing catering |

|

Total revenue from goods and services subject to VAT. |

Including:

|

VAT payable |

= |

Total output VAT |

- |

Total deducted input VAT of the tax period (excluding the negative VAT transferred from the previous period) |

If the VAT payable according to the formula above does not arise (which means the VAT of the enterprise is negative), the enterprise is not eligible for VAT exemption.

4. Enterprises and organizations doing catering for workers that are eligible for tax exemption that have not declared the exemption of the VAT payable from January 01, 2012 must make additional declarations. After the declaration of the exempted tax, if the is excessive tax payment, the enterprise may deduct it from the VAT on other business, or from the VAT payable of the next tax period, or request tax refund as prescribed.

Enterprises and organizations doing catering for workers that are eligible for tax exemption must record the exempted VAT as other incomes when calculating enterprise income tax.

5. If an enterprise or organization doing catering for workers is discovered that they do not keep the commitment on charges, they are no longer eligible for tax exemption. If the unexempted tax is declared as exempted, the enterprise must pay the tax arrears and the fines for late payment as prescribed by law provisions on tax administration.

6. The procedures and dossiers on VAT declaration are made as prescribed in the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance, and the Annex of Value-added tax exemption (Form No. 02/MT-GTGT promulgated together with this Circular).

- The item 07 “Exempted VAT on catering for workers” in the form No. 02/MT-GTGT is summarized in item 38 “Reduction of VAT in previous periods” on the VAT declaration sheet No. 01/GTGT promulgated together with the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance.

- When adding the declaration of exempted VAT of the previous months and periods, the item 07 the Annex No. 02/MT-GTGT of the previous months shall be summarized in item 38 “Reduction of VAT in previous periods” on the VAT declaration sheet No. 01/GTGT promulgated together with the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance.

Chapter III

PERSONAL INCOME TAX

Article 8. The exemption and exemption period of personal income tax on the income from salaries, remunerations, and incomes from business (except for households and individuals leasing houses and rooms, providing day care, and doing catering for workers that are eligible for tax exemption as prescribed in Article 9 this Circular).

1. The personal income tax is exempted from July 01, 2012 until the end of December 31, 2012 for business households and individuals earning taxable income from salaries, remunerations and business at level 1 in the Progressive tariff in Article 22 of the Law on Personal income tax No. 04/2007/QH12 dated November 21, 2007

2. Business households and individuals earning taxable income from salaries, remunerations and business at level 2 in the Progressive tariff in Article 22 of the Law on Personal income tax No. 04/2007/QH12 dated November 21, 2007 must pay personal income tax from level 1 in the Progressive tariff.

Article 9. The exemption of personal income tax in 2012 applicable to households and individuals leasing houses and rooms, providing day care, and doing catering for workers

The flat personal income tax is exempted from January 01, 2012 until the end of December 31, 2012 for business households and individuals renting houses and rooms to employees and students, providing day care, doing catering for workers as long as they maintain the rents, day care charges and catering charges not exceeding that in December 2011.

For business households and business individuals commencing such business in 2012, the rents, day care charges and catering charges must not exceed that in December 2011 of business households and individuals doing the same business in the same locality that have been operated before 2012.

Article 10. Declaring and deducting personal income tax on salaries and remunerations

1. For organizations and individuals that pay salaries or remunerations (hereinafter referred to as salary payers):

From July 01, 2012 until the end of December 31, 2012, the salary payer must declare tax but shall not calculate and deduct personal income tax of individuals earning taxable income from salaries or remunerations at level 1 (taxable income ≤ 5 million VND/month) in the Progressive tariff in Article 22 of the Law on Personal income tax. Individuals earning taxable income from salaries or remunerations at level 2 or above (taxable income > 5 million VND/month), the salary payer must declare, deduct, and pay personal income tax from level 1 in the Progressive tariff in Article 22 of the Law on Personal income tax.

Salary payers shall write the deducted tax amount in the item [33] of the Declaration No. 02/KK-TNCN promulgated together with the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance.

Example 1. Mr. A earn his income from the salary of July 2012 being 9,200,000 VND. Mr. A is eligible for family circumstance reduction being 4,000,000 VND, the social insurance payable is 200,000 VND. Mr. A has no dependant and no contribution to charities.

The taxable income of Mr. A is:

9,200,000 VND - 4,000,000 VND - 200,000 VND = 5,000,000 VND.

Mr. A’s income is at level 1 of the Progressive tariff, so the personal income tax in July 2012 is temporarily not deducted from his income.

Example 2. Mr. B earn his income from the salary of July 2012 being 21,200,000 VND. Mr. B is eligible for family circumstance reduction being 4,000,000 VND, the social insurance payable is 318,000 VND. Mr. A has no dependant and no contribution to charities.

- The taxable income of Mr. B is:

21,200,000 VND - 4,000,000 VND - 318,000 VND = 16,882,000 VND.

Mr. B’s income is at level 2 of the Progressive tariff and higher, so he must pay tax as follows:

- The personal income tax payable by Mr. B is:

+ Level 1: 5,000,000 VND x 5% = 250,000 VND.

+ Level 2: (10,000,000 VND – 5,000,000 VND) x 10% = 500,000 VND.

+ Level 3: (16,882,000 VND – 10,000,000 VND) x 15% = 1,032,300 VND.

The total personal income tax payable by Mr. B is: 1,782,300 VND (250,000 VND + 500,000 VND + 1,032,300 VND).

2. For individuals directly declaring personal income tax:

From July 01, 2012 until the end of December 31, 2012, individuals earning monthly taxable income from salaries or remunerations at level 1 (taxable income ≤ 5 million VND/month) may not declare and pay personal income tax monthly.

Individuals earning taxable income from salaries or remunerations at level 2 or higher (taxable income > 5 million VND/month) must declare and pay personal income tax from level 1 in the Progressive tariff in Article 22 of the Law on Personal income tax.

Article 11. Declaring personal income tax of business households and individuals

1. Business households and individuals shall pay tax under tax declaration method as follows:

a) Business households and individuals earning monthly taxable income at level 1 in the Progressive tariff (taxable income > 5 million VND/month) must make declaration every month, and temporarily have the tax amount payable in the Declaration of Q3 and Q4/2012 exempted.

Business households and individuals must declare the tax payable (excluding the tax temporarily exempted) in the item [33] (Personal income tax preliminarily paid), in the declaration No. 08/KK-TNCN promulgated together with the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance.

Example 3: Mr. A earns taxable income of Q3/2012 being 22.8 million VND. Mr. A has 1 dependant and does not pay social insurance, health insurance, nor contribute to charities.

- Mr. A is eligible for reduction of family circumstance in Q3: (4 million VND x 3 months) + (1.6 million VND x 3 months) = 16.8 million VND

- The taxable income in Q3 of Mr. A is 6 million VND (22.8 million VND – 16.8 million VND).

- The preliminary monthly taxable income in Q3 of Mr. A is 2 million VND (6 million VND : 3 months).

Mr. A’s monthly taxable income is at level 1 of the Progressive tariff, so he is exempted from the preliminary tax in Q3.

Assuming in Q4/2012, Mr. A’s monthly taxable income is similar to that in Q3, he is exempted from the preliminary tax in Q4.

b) For groups of business individuals

Groups of business individuals must declare the tax payable (excluding the tax temporarily exempted) prescribed in Point a this Clause in the item [35] (Personal income tax preliminarily paid), in the declaration No. 08A/KK-TNCN, promulgated together with the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance.

2. Tax declaration applicable to business households and individuals eligible for tax exemption that pay tax at a flat rate:

a) Business households and individuals paying tax at a flat rate (except for households and individuals leasing houses and rooms, providing day care, and doing catering for workers that are eligible for tax exemption as prescribed in Article 9 this Circular) that earn annual taxable income at level 1 in the Progressive tariff (the taxable income ≤ 60 million VND/year) are exempted from the tax payable in Q3 and Q4/2012 according to the tax notification from tax authorities.

b) Business households and individuals renting houses and rooms to employees and students, providing day care, doing catering for workers that are eligible for tax exemption as prescribed in Article 9 of this Circular, are exempted from paying the tax payable in 2012.

The business households and individuals eligible for tax exemption as prescribed in Point b this Clause must publicly post the rents, charges for day care and catering for workers at the business establishments that do not exceed that in December 2011. Business households and individuals must notify the direct tax authorities and local authorities at the commune or ward level in writing before November 01, 2012 about the charges not exceeding that in December 2011 right on January 01, 2012.

Business households and individuals eligible for tax exemption may not remake the tax declaration. Tax authorities must make and report the list of individuals and households leasing rooms, houses, providing day care, and doing catering for workers, and the exempted tax amount, to People’s Committees at the same level and the superior tax authorities for monitoring and inspecting. Posting it at the tax authorities office before November 15, 2012, and notify the business households and individuals.

If the business households or individuals are discovered that they do not collect the appropriate charges, they are no longer eligible for tax exemption or for the refund of the tax paid to the State budget. The exempted or refunded tax shall be collected. The violations of tax shall be fined as prescribed by law provisions on tax administration.

Article 12. Finalizing personal income tax

1. Finalizing personal income tax on taxable income from salaries, remunerations, and business at level 1 in the Progressive tariff.

a) The exempted tax amount for the whole year for individuals earning taxable income from salaries, remunerations and business at level 1 in the Progressive tariff is calculated as follows:

|

Exempted tax |

= |

The taxable income in 2012 at level 1 |

x |

The tax rate according to the progressive tariff |

x |

6 months |

|

12 months |

||||||

b) Business households and individuals shall declare personal income tax after subtracting the exempted tax in the item [32] “Total personal income tax in the period) on the Personal income tax declaration No. 09/KK-TNCN promulgated together with the Circular No. 28/2011/TT-BTC dated February 28, 2011 of the Ministry of Finance.

2. Households and individuals leasing houses and rooms, providing day care, and doing catering for workers that are eligible for tax exemption as prescribed in Article 9 this Circular) that have paid the personal income tax in Q1 and Q2/2012 (or even Q3/2012 for not being notified of the tax exemption by tax authorities) to the State budget shall be refunded the paid tax. The direct tax authorities shall make the list of business households and individuals eligible for tax refund in each commune or ward, and send the Decision on tax refund to every business household and individual.

Tax authorities must make and post the list of individuals and households leasing rooms, houses, providing day care, and doing catering for workers, that are eligible for tax refund at the tax authorities office before November 15, 2012.

3. When finalizing personal income tax, individuals earning income from salaries, remunerations, or business that are eligible for tax exemption must fill and submit the form No. 26/MT-TNCN (promulgated together with this Circular) to the tax authorities; salary payers authorized to finalize tax by salary receivers must fill and submit the form No. 27/MT-TNCN (promulgated together with this Circular) to the tax authorities.

Chapter IV

IMPLEMENTATION ORGANIZATION

Article 13. Effects

This Circular takes effect on October 05, 2012.

Article 14. Implementation responsibilities

1. People’s Committees of central-affiliated cities and provinces shall guide functional agencies to implement the Government’s provisions and the Ministry of Finance’s guidance.

2. Tax authorities at all level must disseminate and guide organizations and individuals to implement this Circular.

3. Organizations and individuals being subjects of application of this Circular must comply with this Circular.

Organizations and individuals are recommended to send feedbacks on the difficulties arising during the course of implementation to the Ministry of Finance for consideration and settlement./.

|

|

FOR THE MINISTER |

|

|

Form No.: 01/MGT-TNDN (Promulgated together with the Circular No. 140/2012/TT-BTC, of August 21, 2012 of the Ministry of Finance) |

SOCIALIST REPUBLIC OF

VIETNAM

Independence - Freedom - Happiness

----------------------------

ANNEX

ENTERPRISE INCOME TAX EXEMPTION AND REDUCTION

[01] Tax period: Quarter.../year.... (or year...)

[02] Name of taxpayer:..................................................................................

|

[03] Tax Code: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[04] Name of tax agent (if any):.............................................................................

|

[05] Tax Code: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

[06] The payable EIT amount :....................................................................................................

In words: …………………………………………………………………………….......

[07] The exempted or reduced EIT amount:........................................................................................

In words: …………………………………………………………………………….......

[08] Cases of exemption or reduction:

Small and medium-size enterprises

Labor-intensive enterprises

Enterprises providing shift meal for workers

(Enterprises may mark in only 1 in 3 reasons above)

I hereby commit that the declared content is right and I am responsible before law for the declared content.

|

STAFF

OF TAX AGENT |

Date .............................

|

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed