Nội dung toàn văn Circular No. 154/2011/TT-BTC guiding the government’s Decree No. 101/2011/ND-CP

|

THE

MINISTRY OF FINANCE |

THE

SOCIALIST REPUBLIC OF VIETNAM |

|

No. 154/2011/TT-BTC |

Hanoi, November 11, 2011 |

CIRCULAR

GUIDING THE GOVERNMENT’S DECREE NO. 101/2011/ND-CP OF NOVEMBER 4, 2011, DETAILING THE NATIONAL ASSEMBLY’S RESOLUTION NO. 08/2011/QH13, ADDITIONALLY PROVIDING A NUMBER OF TAX-RELATED SOLUTIONS FOR ENTERPRISES AND INDIVIDUALS TO OVERCOME THEIR DIFFICULTIES

Pursuant to June 3, 2008 Law No. 14/2008/QH12 on Enterprise Income Tax;

Pursuant to June 3, 2008 Law No. 13/2008/QH12 on Value-Added Tax; Pursuant to November 21, 2007 Law No. 04/2007/QH12 on Personal Income Tax;

Pursuant to November 29, 2006 Law No. 78/2006/QH11 on Tax Administration;

Pursuant to the National Assembly’s Resolution No. 08/2011/QH13 of August 6, 2011, additionally providing a number of tax-related solutions for enterprises and individuals to overcome their difficulties;

Pursuant to the Government’s Decree No. 101/2011/ND-CP of November 4, 2011, detailing the National Assembly’s Resolution No. 08/2011/QH13, additionally providing a number of tax-related solutions for enterprises and individuals to overcome their difficulties;

Pursuant to the Government’s Decree No. 118/2008/ND-CP of November 27, 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

The Ministry of Finance guides the implementation as follows:

Chapter I

ENTERPRISE INCOME TAX

Article 1. General provisions

1. To reduce 30% of payable enterprise income tax amounts in 2011 for small- and medium-sized enterprises.

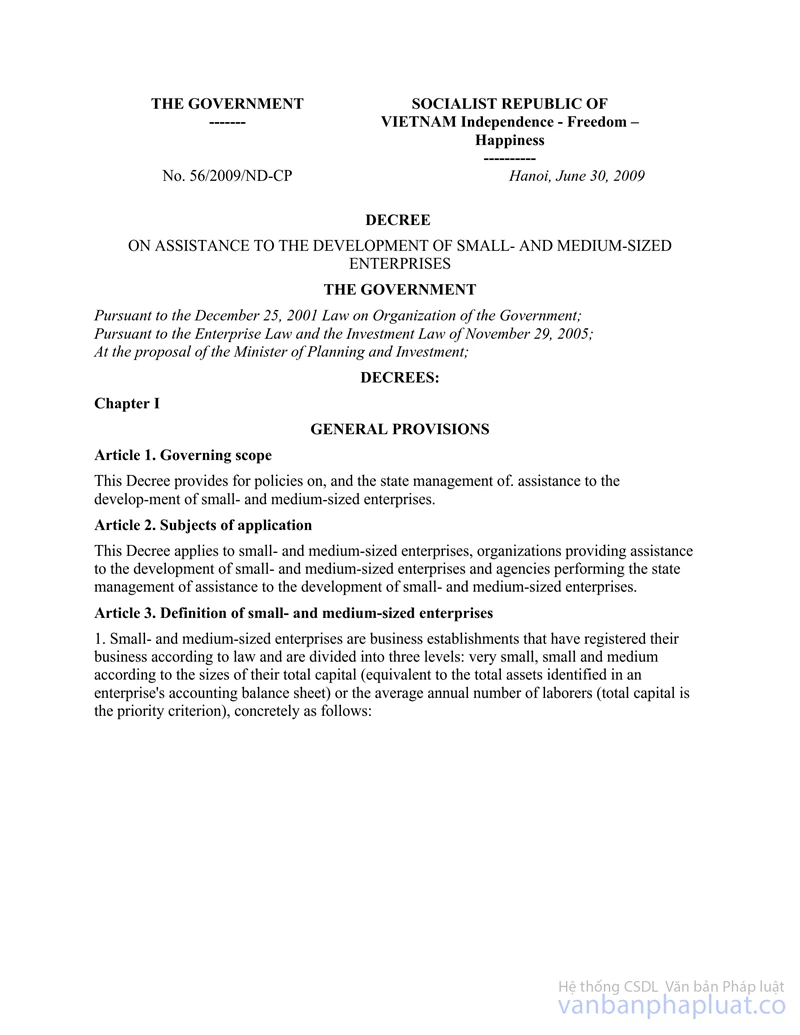

a/ Small- and medium-sized enterprises provided in this Clause are those satisfying the criterion on capital or labor under Clause 1, Article 3 of the Government’s Decree No. 56/2009/ND-CP of June 30, 2009, on support for development of small- and medium-sized enterprises;

b/ The capital as the basis for identifying an enterprise eligible for enterprise income tax reduction in 2011 is the total capital indicated in the enterprise’s accounting balance sheet made on December 31, 2010. For a small- or medium-sized enterprise established on January 1, 2011, or later, the capital as the basis for identifying a small- or medium-sized enterprise eligible for enterprise income tax reduction in 2011 is the charter capital stated in the enterprise’s business registration certificate or first investment certificate;

c/ For an enterprise with multiple business lines, it shall be determined as a small- or medium-sized enterprise based on the main business line stated in its business registration certificate. When it is unable to identify the enterprise’s main business line, one of the following indicators may be used to identify the enterprise’s main business line in 2011:

- The highest number of employees working in a business line of the enterprise.

- The highest revenues from a business line of the enterprise.

When it is unable to identify the enterprise’s main business line using the above indicators in order to determine the enterprise’s size, to base on the capital criterion or the business line with the lowest number of employees of which the enterprise actually operated in 2011 under Clause 1, Article 3 of Decree No. 56/2009/ND-CP.

d/ Enterprise income tax reduction is not applicable to the following small- and medium-sized enterprises:

- Grade-1 enterprises under Joint Circular No. 23/2005/TTLT-BLDTBXH- BTC of August 31, 2005, of the Ministry of Labor, War Invalids and Social Affairs and the Ministry of Finance, guiding the ranking and salarying of full-time members of boards of directors, general directors, directors, deputy general directors, deputy directors and chief accountants of state companies.

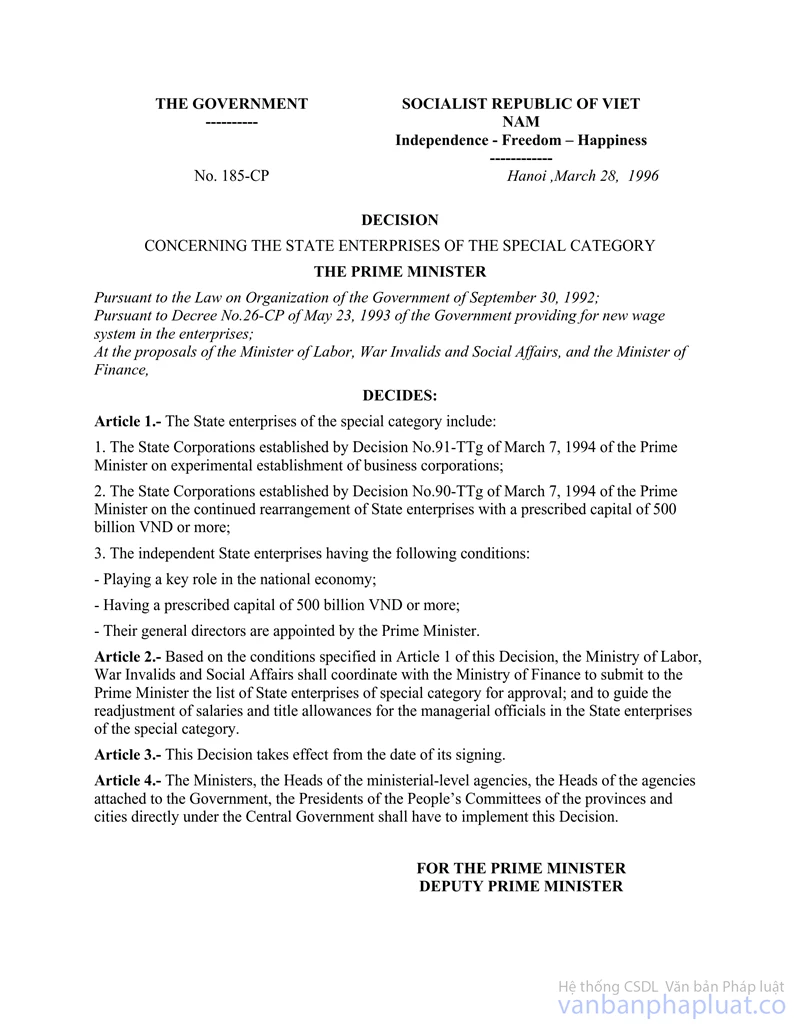

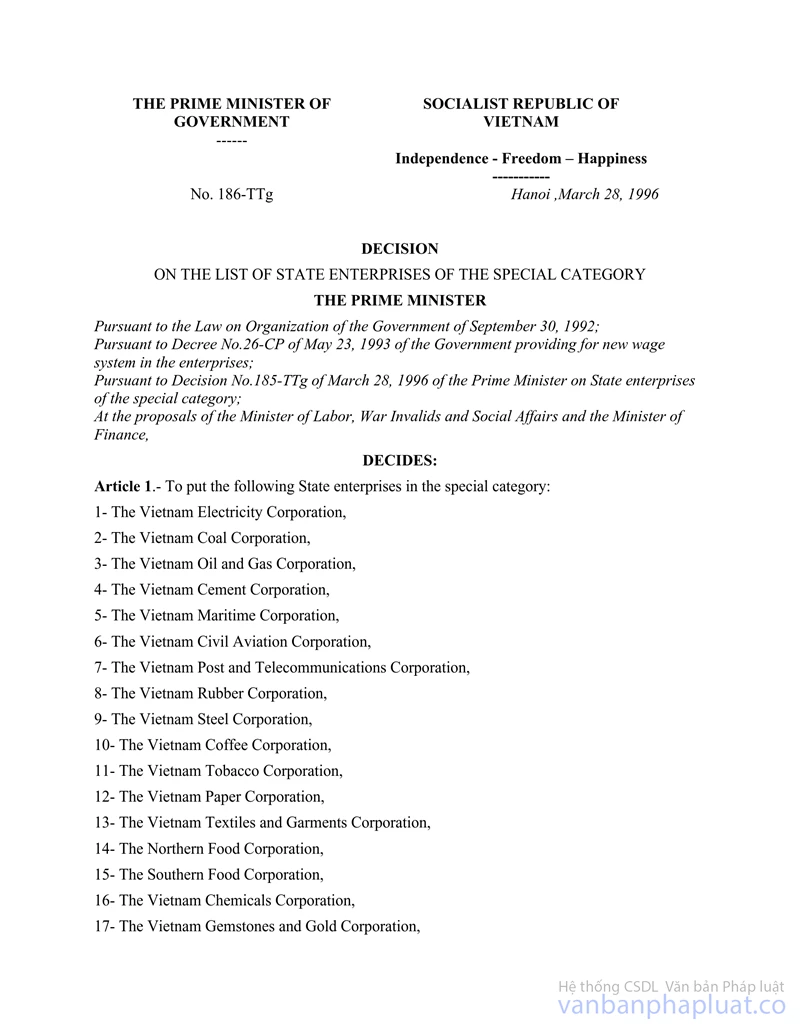

- Special-grade enterprises under the Prime Minister’s Decision No.185/TTg of March 28, 1996, on special-grade state enterprises, and Decision No. 186/TTg of March 28, 1996, listing special-grade state enterprises.

- Enterprises organized after the parent company-subsidiary company model whose parent companies are not small- or medium-sized enterprises and hold over 50% of their equity.

- Economic organizations being non-business units.

e/ Small- or medium-sized enterprises’ income tax amounts to be reduced under this Clause exclude tax amounts on revenues from lottery, real estate, securities, finance, banking and insurance business activities, production and provision of excise tax-liable goods and services, and mineral exploitation and processing.

2. To reduce 30% of payable enterprise income tax amounts in 2011 for labor-intensive enterprises engaged in production, sub-contract production and processing of agricultural, forest and aquatic products, textile and garment, leather footwear and electronic parts; and in construction of socio- economic infrastructure works.

- Labor-intensive enterprises eligible for tax reduction under this Clause are those frequently employing over 300 people on average in 2011, excluding employees working under short-term labor contracts of under 3 months.

- Reduced enterprise income tax amounts are the tax amounts on revenues from the production, sub-contract production and processing of agricultural, forest and aquatic products, textile and garment, leather footwear and electronic parts; and construction of socio-economic infrastructure works.

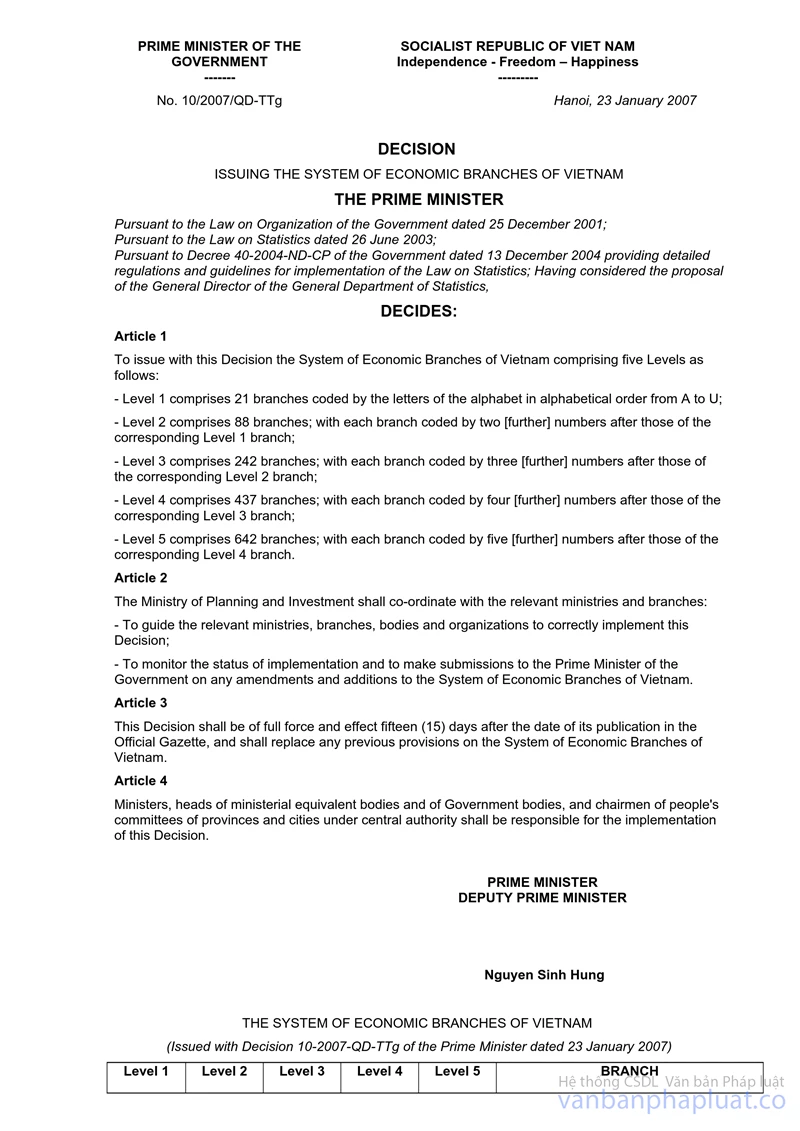

The production, sub-contract production and processing of agricultural, forest and aquatic products, textile and garment, leather footwear and electronic parts under this Clause shall be determined based on Vietnam’s system of industries promulgated together with the Prime Minister’s Decision No. 10/2007/QD-TTg of January 23, 2007.

Construction of socio-economic infrastructure works under this Clause covers construction and installation of water and power plants, electricity transmission and distribution works; water supply and drainage systems; roads, railways; airports, seaports, river ports; airfields, railway stations, car terminals; schools, hospitals, cultural houses, cinemas, art performance facilities, sports training and competition facilities; wastewater and solid waste treatment systems; communication works and irrigation works for agricultural, forestry and fishery production.

3. To reduce 50% of payable enterprise income tax amounts arising from July 1 through December 31, 2011 (payable enterprise income tax amounts in the 3rd and 4th quarters of 2011) for enterprises with revenues from commercial supply of shift meals to workers.

For a shift meal supplier which is a small- or medium-sized enterprise eligible for both a 30% reduction of the payable enterprise income tax amount in 2011 under Clause 1, Article 1 of this Circular, and a 50% reduction of the payable enterprise income tax amount arising from July 1 through December 31, 2011, for revenues from commercial supply of shift meals under Clause 3, Article 1 of this Circular, for the same income, the enterprise may opt for the most beneficial tax reduction.

Article 2. Conditions for receiving tax incentives

1. Enterprises eligible for tax reduction under Article 1 of this Circular are those established and operating under the Vietnamese law; and implementing the regime of accounting, invoices, and vouchers under regulations and paying tax by declaration.

To enjoy tax reduction under this Circular, when submitting its 2011 enterprise income tax finalization dossier under regulations, a small- or medium-sized enterprise organized after the parent company-subsidiary company model must additionally include in the dossier papers evidencing the parent-subsidiary relation and the rate of equity of the subsidiary company held by the parent company such as the subsidiary company’s business registration certificate (certified copy), the parent company’s charter (certified copy) or the subsidiary company’s charter (certified copy).

2. The average annual number of employees as the basis for an enterprise to enjoy tax reduction under Clauses 1 and 2, Article 1 of this Circular is the average number of employees frequently employed by the enterprise in 2011, excluding those working under short-term contracts of under 3 months.

The average annual number of permanent employees shall be determined under the Labor, War Invalids and Social Affairs Ministry’s Circular No.40/2009/TT-BLDTBXH of December 3, 2009, guiding calculation of the number of permanent employees under the Government’s Decree No.108/2006/ND-CP of September 22, 2006, detailing and guiding a number of articles of the Investment Law.

For an enterprise organized after the parent company-subsidiary company model, the number of employees as the basis for the parent company to receive tax reduction does not include the number of employees of subsidiary companies.

3. Shift meal suppliers eligible for tax reduction shall keep the 2011 shift meal price stable at the average price applied in December 2010, post up the shift meal price at their business offices and send to their managing tax offices a notice of the posted price when submitting enterprise income tax finalization dossiers under regulations. An enterprise which is detected by a competent examination or inspection agency to fail to keep its price commitment may not enjoy tax reduction.

4. For an enterprise currently enjoying enterprise income tax incentives under the Enterprise Income Tax Law or legal documents on enterprise income tax, the enterprise income tax amount to be reduced under this

Circular is that subtracted from the enterprise income tax amount eligible for tax incentives under regulations.

Article 3. Determination of to-be-reduced tax amounts

An enterprise shall separately account incomes from production and business activities eligible, from those ineligible, for enterprise income tax reduction. If it is impossible to separately account incomes from activities eligible for tax reduction, incomes used for calculating to-be-reduced tax amounts shall be determined according to the percentage (%) of revenues from tax reduction-eligible activities to the enterprise’s total revenues in 2011.

1. The enterprise income tax amount to be reduced under Clause 1 or 2, Article 1 of this Circular is the one temporarily calculated for quarterly payment and the payable enterprise income tax difference according to the tax finalization report of 2011 against the total temporarily calculated amount for quarterly payment.

An enterprise eligible for tax reduction under regulations having declared and paid tax amounts for the 1st, 2nd and 3rd quarters of 2011 which are eligible for reduction may clear the tax reductions against the payable tax amount for the 4th quarter of 2011 and the payable tax difference according to the annual tax finalization report. If still exists an overpaid tax amount, the enterprise may request to clear this amount against other payable tax amounts or request tax refund under the Tax Administration Law and its guiding documents.

2. The enterprise income tax amount to be reduced under Clause 3, Article 1 of this Circular shall be determined as follows:

a/ For an enterprise which can determine revenues, expenses and taxable incomes of the 3rd and 4th quarters of 2011, the enterprise income tax amount to be reduced for the 3rd and 4th quarters of 2011 shall be determined based on the payable enterprise income tax amounts actually arising in the 3rd and 4th quarters of 2011 determined by the enterprise.

b/ For an enterprise which cannot determine revenues, expenses and taxable incomes of the 3rd and 4th quarters of 2011, the enterprise income tax amount to be reduced for the 3rd and 4th quarters of 2011 shall be determined by the following principle:

|

Reduced enterprise income tax amount for the 3rd and 4th quarters of 2011 |

= |

Payable enterprise income tax amount for activities eligible for tax reduction in 2011 |

x (quarters) x 2 x 50% |

|

4 |

c/ For an enterprise applying the enterprise income tax period other than the calendar year, the enterprise income tax amount to be reduced by the calendar year shall be specifically determined as follows:

+ If it is possible to determine revenues, expenses and taxable incomes of the quarters of 2011 according to the calendar year, to base on actual declarations.

+ If it is impossible to separately determine revenues, expenses and taxable incomes of the quarters of 2011 according to the calendar year, to evenly divide by 12 months (if the enterprise operates for full 12 months) or by the number of months the enterprise actually operates (if the enterprise operates for less than 12 months) based on which to determine the enterprise income tax amount to be reduced corresponding to the period from July 1 through December 31, 2011.

The reduced enterprise income tax amount for incomes from the commercial supply of shift meals to workers exclude the tax amount for incomes from the supply of meals for transport enterprises and airlines and from other business activities.

Article 4. Tax declaration

Enterprises eligible for tax reduction under Article 1 of this Circular shall declare reduced tax amounts under the Tax Administration Law and its guiding documents.

Enterprises shall add the following phrase below the line of undertaking in the declaration of temporarily calculated enterprise income tax amount for quarter payment or the enterprise income tax finalization declaration (according to the forms promulgated together with the Finance Ministry’s Circular No. 28/2011/TT-BTC of February 28, 2011):

Enterprise income tax amount reduced under Resolution No.08/2011/QH13.

Enterprises shall concurrently declare the reduced tax amount in Item [31] of declaration 01A/TNDN or Item [30] of declaration 01B/TNDN, Item [C9] of declaration 03/TNDN, Item [09] of Exemption and Reduction Appendix 03-3A and additionally mark on Item “other incentives.”

An enterprise which has made tax declaration under regulations but has not made declaration for tax reduction under Article 1 of this Circular may additionally make tax declaration. The supplemented tax declaration dossier may be submitted to the tax office on any working day regardless of the deadline for submission of the tax declaration dossier for the subsequent period but before the tax office announces a decision on tax examination or inspection at the taxpayer’s head office.

Article 5. Tax finalization

1. Handling of the reduced enterprise income tax difference between tax finalization declaration and temporarily calculated enterprise income tax for quarterly payment

- For an enterprise making 2011 enterprise income tax finalization itself which has a reduced enterprise income tax amount higher than the total temporarily calculated tax amount of 4 quarters, the enterprise may enjoy tax reduction for the tax amount difference between the finalized tax amount and the temporarily calculated amount for 4 quarters of 2011.

For example: Company A has the temporarily calculated enterprise income tax declaration for quarterly payment in 2011 as follows:

Unit of calculation: million VND

|

Quarter |

Temporarily declared tax amount |

Amount eligible for 30% reduction |

|

I |

200 |

60 |

|

II |

100 |

30 |

|

III |

300 |

90 |

|

IV |

400 |

120 |

|

Total |

1,000 |

300 |

When making a tax finalization, Company A has the following statistics:

Unit of calculation: million VND

|

Tax finalization year |

Arising tax amount |

Amount eligible for 30% reduction |

|

2011 |

1,200 |

360 |

So:

The difference of the enterprise income tax amount eligible for 30% reduction between the finalized tax amount and the temporarily declared amounts of 4 quarters is (360-300) = 60 (million VND)

In this case, Company A may further enjoy reduction of enterprise income tax amount of VND 60 million when making a tax finalization for 2011.

- For an enterprise making 2011 enterprise income tax finalization itself which has a reduced enterprise income tax amount lower than the total temporarily calculated tax amount of 4 quarters, the reduced tax amount shall be determined based on the finalized tax amount.

2. When an enterprise is detected by a competent examination or inspection agency to have an enterprise income tax amount for the tax reduction period under Article 1 of this Circular higher than the tax amount declared by itself (even in case the enterprise is eligible for enterprise income tax reduction under this Circular but has not made declaration of the reduced enterprise income tax), it may enjoy enterprise income tax reduction under regulations for such enterprise income tax amount. Depending on the severity of the enterprise’s violation, the competent examination or inspection agency shall impose sanctions on violations of the tax law under regulations.

3. When an enterprise is detected by a competent examination or inspection agency to have a reduced enterprise income tax amount under Article 1 of this Circular lower than the tax amount declared by itself, the enterprise may enjoy reduction of only the enterprise income tax amount detected through examination or inspection. Depending on the severity of the enterprise’s violation, the competent examination or inspection agency shall impose sanctions on violations of the tax law under regulations.

Chapter II

VALUE-ADDED TAX

Article 6. Reduction of 50% of presumptive value-added tax

1. To reduce 50% of the presumptive value-added tax from July 1 through December 31, 2011, for:

- Households and individuals leasing houses or rooms to workers, students or pupils;

- Households and individuals supplying shift meals to workers.

2. Business households and individuals eligible for a 50% reduction of the presumptive value-added tax under Clause 1 of this Article shall:

- Keep stable charge rates and making written commitments to keeping rent rates or shift meal prices at the level applied in December 2010, for households and individuals commencing business in 2010 or earlier; keep rent rates or shift meal prices not higher than those applied in December 2010 by households and individuals commencing business in the same localities in 2010 or earlier, for households and individuals commencing business in 2011 or later.

- Post up rent rates or shift meal prices at their business offices and send notices of posted rent rates or prices to their managing tax offices before December 31, 2011, and concurrently to the People’s Committees of communes or wards in which they do business.

Managing tax offices shall coordinate with commune-level People’s Committees in scrutinizing business households and individuals to find out those eligible for tax reduction under Clause 1 of this Article which have made commitments to keeping stable charge rates and posted up charge rates (as mentioned above), coordinate with commune-level tax counseling councils in making list of these households and individuals, publicize this list at the offices of commune-level People’s Committees and tax teams and send notices of the 50% reduction of presumptive value-added tax to these households and individuals.

A household or an individual detected through inspection or examination to fail to keep its/his/her charge rate commitment may not enjoy tax reduction.

3. Business households and individuals eligible for the 50% reduction of presumptive value-added tax under Clause 1 of this Article that have paid 100% of the presumptive value-added tax amount from July through December 2011 are regarded as overpaying value-added tax and may have the overpaid tax amount handled under the tax administration law.

Article 7. 50% reduction of payable value-added tax for suppliers of shift meals to workers

1. To reduce 50% of payable value-added tax amounts arising from July 1 through December 31, 2011, for suppliers of shift meals to workers (excluding their supply of meals to transportation companies and airlines and their other business activities).

2. A supplier of shift meals to workers which trades in different goods and services shall make separate declarations of revenues, and input and output value-added tax amounts for the supply of shift meals to determine the payable value-added tax amount to be reduced for this business activity.

The payable value-added tax amount to be reduced shall be determined as follows:

|

Payable VAT amount for supply of shift meals to workers |

= |

Output VAT amount for supply of shift meals to workers |

- |

Input VAT amount credited for supply of shift meals to workers |

|

Reduced VAT amount for supply of shift meals to workers |

= |

Payable VAT amount for supply of shift meals to workers |

x |

50% |

Of which:

a/ The output value-added tax amount for the supply of shift meals to workers equals (=) the total value-added tax amount for sold shift meals indicated in the value-added tax invoice;

The value-added tax amount indicated in the value-added tax invoice equals (=) the taxed shift meal price multiplied by (x) the value-added tax rate (10%);

b/ Determination of creditable input value-added tax

- The input value-added tax for goods and services used for the supply of shift meals to workers shall be wholly credited;

- For fixed assets, goods and services used for both the supply of shift meals to workers and other taxable business activities, the creditable input value-added tax for the supply of shift meals shall be accounted separately. When impossible to do so, the input tax shall be credited according to the percentage (%) of revenues from the supply of shift meals to workers to the total revenues from sale of VAT-liable goods and services.

For a supplier of shift meals to workers trading in different goods and services which cannot separately account revenues from and input and output value-added tax for the supply of shift meals and other goods and service trading activities and therefore cannot accurately determine the payable value-added tax amount to be reduced, the reduced value-added tax amount shall be determined as follows:

|

Reduced VAT amount |

= |

Payable VAT amount according to declaration of the tax period |

x |

Revenues from shift meal supply |

x |

50% |

|

Total revenues from VAT-liable goods and services |

Of which:

|

Payable VAT amount |

= |

Total output VAT amount |

- |

Total creditable input VAT arising in the tax period (excluding the negative VAT amount carried forward from the previous period) |

If an enterprise has no payable value-added tax amount according to the above formula (meaning the enterprise has a negative value-added tax amount), value-added tax reduction does not apply.

3. A shift meal supplier eligible for the 50% reduction of value-added tax under Clause 1 of this Article must:

- Be an enterprise established and operating under Vietnamese law; implement the regime of accounting, invoices and vouchers under regulations and pay tax by declaration.

- Make a written commitment to keeping the shift meal price at the level applied in December, 2010, for enterprises commencing operation in 2010 or earlier; or keeping the shift meal price not higher than the level applied in December, 2010, by shift meal suppliers commencing operation in 2010 or earlier in the same locality, for enterprises operating in 2011 or later.

- Post up the shift meal price at its business office and send a notice of this price to its managing tax office.

4. Shift meal suppliers eligible for tax reduction that have not made declaration for a 50% reduction of the payable value-added tax amount arising from July 1 through December 31, 2011, shall make declaration for clearing the reduced value-added tax amount against the payable value- added tax amounts of subsequent months.

Shift meal suppliers eligible for tax reduction shall account the reduced payable value-added tax amount into other incomes when determining enterprise income tax-liable incomes.

5. A shift meal supplier that is detected through examination or inspection to fail to keep its price commitment may not enjoy reduction of payable value-added tax.

6. Declaration of reduced value-added tax

Value-added tax declaration procedures and dossiers comply with Circular No. 28/2011/TT-BTC of February 28, 2011, and Appendix 01-7/GTGT on table of preferential value-added tax under Resolution No. 08/2011/QH13 to this Circular, in which:

- Section 4 “Goods and services subject to 10% tax rate” of Appendix 01-1/GTGT to Circular No. 28/2011/TT-BTC: For goods or service sale invoices and vouchers for the supply of shift meals for workers, to clearly write “considered for incentives under Resolution 08” in Column 10 “Note”.

- Appendix 01-2/GTGT to Circular No. 28/2011/TT-BTC:

+ Section 1 “Goods and services exclusively used for VAT-liable production and business activities eligible for tax deduction”: for invoices and vouchers of goods and services bought in for the supply of shift meals to workers, to clearly write “considered for incentives under Resolution 08.”

+ Column 11 “Note…” of Section 3 “Goods and services used for both taxable and non-taxable production and business activities eligible for tax deduction”: for fixed assets used for both VAT-liable and -free production and business activities, to clearly write “fixed assets considered for incentives under Resolution 08”; for goods and services (excluding fixed assets) used for both supply of shift meals to workers and production and trading of VAT-free goods and services, to clearly write “goods and services considered for incentives under Resolution 08”.

- Item 16 “Preferential VAT for supply of shift meals to workers” of Appendix 01-7/GTGT is incorporated into Item 38 “Reduction of VAT of previous periods” of VAT declaration form No. 01/GTGT attached to Circular No. 28/2011/TT-BTC.

Chapter III

PERSONAL INCOME TAX

Article 8. Scope of application

Taxed incomes from salaries, wages; business activities; dividends from securities investment or capital contributions to buy corporate shares; and transfer of securities by individuals are eligible for tax exemption or reduction and shall be declared and withheld under this Chapter.

Article 9. Tax exemption and tax exemption duration for incomes from salaries, wages and business activities

1. To exempt personal income tax from August 1 through December 31, 2011, for business individuals and households having taxed incomes from salaries, wages or business activities which reach the tax threshold at grade 1 in the Partially Progressive Tariff provided in Article 22 of November 21, 2007 Law No. 04/2007/QH12 on Personal Income Tax.

2. Business individuals and households having taxed incomes from salaries, wages or business activities which reach the tax threshold at grade 2 or higher in the Partially Progressive Tariff provided in Article 22 of November 21, 2007 Law No. 04/2007/QH12 on Personal Income Tax may not enjoy tax reduction at grade 1 in the Partially Progressive Tariff.

Article 10. Reduction and exemption level and duration for presumptive personal income tax for incomes from lodging business; child care and supply of shift meals to workers

1. To reduce 50% of the presumptive personal income tax from July 1 through December 31, 2011, for individuals and households leasing houses or rooms to workers, laborers, students and pupils; taking care of children; and supplying meals to workers, that have taxed incomes at grade 2 or higher in the Partially Progressive Tariff, provided that they keep stable rent rates; child care charge rates; and meal prices posted up and actually charged in December, 2010.

2. To reduce 50% of the presumptive personal income tax in July, 2011, and exempt personal income tax from August 1 through December 31, 2011, for individuals and households leasing houses or rooms to workers, laborers, students and pupils; taking care of children; and supplying meals to workers, that have taxed incomes at grade 1 in the Partially Progressive Tariff, provided that they keep stable rent rates; child care charge rates; and meal prices posted up and actually charged in December, 2010.

Article 11. Personal income tax exemption duration for incomes from dividends

1. To exempt personal income tax for incomes from dividends actually received by individuals from August 1, 2011, through December 31, 2012, for investing in the securities market or contributing capital to buy corporate shares.

Individuals transferring stocks (paid in replacement of dividends) from August 1, 2011, through December 31, 2012, are exempted from personal income tax for incomes from dividends.

2. Dividends received by individuals from joint-stock banks, financial investment funds and credit institutions may not enjoy tax exemption under Clause 1 of this Article.

Article 12. 50% reduction of personal income tax for incomes from individuals’ transfer of securities from August 1, 2011, through December 31, 2012.

Article 13. Declaration and withholding of incomes from salaries and wages

1. For income payers:

From August 1 through December 31, 2011, payers of incomes as monthly salaries and wages shall declare taxes, but temporarily shall not calculate and withhold personal income tax for individuals having taxed incomes from salaries and wages at grade 1 (taxed income equal to VND 5 million/month or lower) in the Partially Progressive Tariff provided in Article 22 of the Law on Personal Income Tax. For individuals having taxed incomes at grade 2 or higher (taxed income higher than VND 5 million/month), income payers shall declare, withhold and pay personal income tax from grade 1 in the Partially Progressive Tariff provided in Article 22 of the Law on Personal Income Tax.

Income payers shall write the tax amount withheld at the exempted or reduced level in Items [33], [34] and [35] of declaration form No. 02/KK-

TNCN attached to the Finance Ministry’s Circular No. 28/2011/TT-BTC of February 28, 2011.

Example 1: A has an income of VND 9.2 million from salaries and wages in August 2011. He only enjoys a reduction of VND 4 million for himself, pays insurance premiums of VND 200,000, makes no humanitarian donations and has no dependant.

A’s taxed income is:

VND 9.2 million - VND 4 million - VND 200,000 = VND 5 million.

A has a taxed income at grade 1 in the Partially Progressive Tariff so he temporarily does not have to pay personal income tax for August 2011.

Example 2: B has an income of VND 21.2 million from salaries and wages in August 2011. He only enjoys a reduction of VND 4 million for himself, pays insurance premiums of VND 318,000, makes no humanitarian donations and has no dependant.

B’s taxed income is:

VND 21.2 million - VND 4 million - VND 318,000 = VND 16.882 million.

B has a taxed income at grade 2 and higher (to grade 3) in the Partially Progressive Tariff so he has to pay personal income tax under Article 22 of the Law on Personal Income Tax:

B’s payable personal income tax amount is calculated as follows:

+ Grade 1: VND 5 million x 5% = VND 250,000.

+ Grade 2: (VND 10 million - VND 5 million) x 10% = VND 500,000.

+ Grade 3: (VND 16.882 million - VND 10 million) x 15% = VND 1,032,300.

B’s total payable personal income tax amount is VND 1,782,300 (= 250,000 + 500,000 + 1,032,300).

2. For individuals making direct declaration

From August 1 through December 31, 2011, individuals having taxed incomes at grade 1 (taxed income lower than or equal to VND 5 million/month) in the Partially Progressive Tariff under Article 22 of the Law on Personal Income Tax temporarily are not required to declare and pay personal income tax for their salaries and wages.

Individuals having taxed incomes at grade 2 or higher (taxed income higher than VND 5 million/month) shall declare and pay personal income tax from grade 1 in the Partially Progressive Tariff under Article 22 of the Law on Personal Income Tax.

Article 14. Tax declaration for business individuals and households

1. Business individuals and households paying tax by declaration shall declare tax as follows:

a/ Business individuals and households having a taxed income at grade 1 in the Partially Progressive Tariff (taxed income of VND 5 million/month or lower) shall still declare tax on a quarterly basis and are temporarily exempted for two-thirds of the payable tax amount of the declaration of the 3rd quarter of 2011 and the whole payable tax amount of the declaration of the 4th quarter of 2011.

Business individuals and households shall declare the remaining tax amount after subtracting the exempted tax amount in Item [33] (temporarily paid personal income tax amount) of declaration form No. 08/KK-TNCN attached to the Finance Ministry’s Circular No. 28/2011/TT-BTC of February 28, 2011.

Example 3: A’s taxable income of the 3rd quarter is VND 22.8 million. A has a dependant

Family circumstance-based reduction for the taxpayer and 1 dependant in the 3rd quarter is:

(VND 4 million x 3 months) + (VND 1.6 million x 3 months) = VND 16.8 million

Taxed income in the 3rd quarter = VND 22.8 million - VND 16.8 million = VND 6 million

Average monthly temporarily calculated taxed income = VND 6 million: 3 months = VND 2 million (lower than VND 5 million)

A has a taxed income at grade 1 in the Partially Progressive Tariff so he is temporarily exempted for two-thirds of the temporarily paid tax amount in the 3rd quarter.

Temporarily paid tax amount in the 3rd quarter before tax exemption and reduction = (VND 2 million x 5% x 3 months) = VND 0.3 million.

Temporarily exempted tax amount of the declaration of the 3rd quarter = VND 0.3 million x 2/3 = VND 0.2 million.

Temporarily paid tax amount in the 3rd quarter after tax exemption and reduction = VND 0.3 million - 0.2 million = VND 0.1 million.

Suppose in the 4th quarter of 2011, A has revenues and expenses like the 3rd quarter, he is exempted from the whole payable tax amount in the 4th quarter.

b/ For groups of business individuals

Groups of business individuals shall declare remaining tax amounts after receiving tax exemption under Point a of this Clause in Item [35] (temporarily paid personal income tax amount) of declaration form No.08A/KK-TNCN attached to the Finance Ministry’s Circular No.28/2011/TT-BTC of February 28, 2011.

2. Tax declaration by business individuals and households eligible for tax reduction or exemption that pay tax by the presumptive method

a/ Business individuals and households paying tax by the presumptive method and having an yearly taxed income at grade 1 in the Partially Progressive Tariff (taxed income of VND 60 million/year or lower) may enjoy an exemption of two-thirds of the payable tax amount of the 3rd quarter and the whole payable tax amount of the 4th quarter of 2011 according to the tax office’s notice at the beginning of the year;

b/ Individuals and households leasing houses or rooms; taking care of children; and supplying meals to workers under Clause 1, Article 10 of this Circular that have an yearly taxed income at grade 2 or higher in the Partially Progressive Tariff may enjoy a 50% reduction of the presumptive tax amounts of the 3rd and 4th quarters of 2011 according to the tax office’s notice at the year’s beginning;

c/ Individuals and households leasing houses or rooms; taking care of children; and supplying meals for workers under Clause 2, Article 10 of this Circular that have an yearly taxed income at grade 1 in the Partially Progressive Tariff may enjoy a 50% reduction of the personal income tax amount of 1 month and exemption from the personal income tax of 2 months of the 3rd quarter; and exemption from the personal income tax amount of the 4th quarter of 2011 according to the tax office’s notice at the year’s beginning.

Business individuals and households eligible for tax exemption or reduction under this Clause shall post up charge rates applied on the last days of 2010 at their business offices and concurrently notify these rates in writing to their managing tax offices and commune-level administrations. Individuals and households that are detected through inspection or examination to fail to post up charge rates and charge their services not at the posted up rates may not enjoy tax reduction and concurrently shall be administratively sanctioned for violation of tax regulations.

Business individuals, households and individual groups paying tax by the presumptive method are not required to make written declarations again. Pursuant to Points a, b and c of this Clause, tax offices shall notify payable tax amounts to business individuals, households and individual groups after subtracting the exempted or reduced tax amounts.

Article 15. Tax declaration and withholding for incomes from transfer of securities and dividends

1. For transfer of securities:

From August 1, 2011, through December 31, 2012, institutions (securities companies, commercial banks, etc.) shall temporarily withhold personal income tax on individuals’ transfer of securities at the rate of 0.05% (reduction of 50% of the tax rate of 0.1%) of the total sales of securities for each transfer.

Institutions shall withhold personal income tax amounts, write the total personal income tax amounts withheld at the reduced level in Item [24] of declaration form No. 03/KK-TNCN attached to the Finance Ministry’s Circular No. 28/2011/TT-BTC of February 28, 2011.

Example 4: On September 1, 2011, A transferred 10,000 stocks coded Z at VND 31,000/stock. He opened a securities transaction account at Securities Company X which shall withhold A’s personal income tax as follows:

Payable tax amount = 10,000 x VND 31,000 x 0.05% = VND 155,000

2. For incomes from dividends:

From August 1, 2011, through December 31, 2012, payers of dividends to individual securities investors; contributors of capital to buy corporate shares (except dividends of joint-stock banks, financial investment funds and credit institutions) shall not withhold personal income tax for individuals’ incomes from dividends.

Income payers shall write the tax amount as zero (= 0) in Item [22] of declaration form No. 03/KK-TNCN attached to the Finance Ministry’s Circular No. 28/2011/TT-BTC of February 28, 2011.

Example 5: In 2010, A bought 2% of the share of Joint-Stock Company X. On August 1, 2011, he actually received dividends worth VND 100 million and these dividends are exempted from personal income tax.

Article 16. Declaration of personal income tax finalization

1. Declaration of personal income tax finalization for taxed incomes from salaries, wages or business activities of individuals at grade 1 in the Partially Progressive Tariff.

a/ The exempted tax amount for the whole year for incomes from salaries and wages or business activities of an individual having a taxed income at grade 1 in the Partially Progressive Tariff shall be determined as follows:

|

Exempted tax mount |

= |

Taxed income in 2011 at grade 1 |

x |

Tax rate according to the Partially Progressive Tariff |

x |

5 months |

|

12 months |

||||||

b/ Business individuals and households shall declare personal income tax amounts after deducting exempted tax amounts in Item [32] (tax amounts arising in the period) of personal income tax finalization form No. 09/KK- TNCN attached to the Finance Ministry’s Circular No. 28/2011/TT-BTC of February 28, 2011.

2. Declaration of tax finalization for individual transferors of securities registering to pay tax at the rate of 20%

a/ The reduced tax amount of the whole year for an individual transferor of securities registering to pay tax at the rate of 20% shall be determined as follows:

|

Reduced tax amount |

= |

Taxed income |

x |

20% |

x |

50% |

x |

5 months |

|

12 months |

||||||||

b/ Individuals shall declare personal income tax amounts after deducting the reduced tax amounts in Item [26] (payable tax mounts in the period) of personal income tax finalization form No. 13/KK-TNCN attached to the Finance Ministry’s Circular No. 28/2011/TT-BTC of February 28, 2011.

3. When making personal income tax finalization, an organization or individual eligible for tax exemption or reduction shall declare and submit to the tax office an appendix made according to form No. 25/MGT-TNCN attached to this Circular (not printed herein), which clearly indicates the total payable tax amount and total exempted or reduced tax amount, together with the tax finalization dossier.

Chapter IV

ORGANIZATION OF IMPLEMENTATION

Article 17. Effect

This Circular takes effect on December 26, 2011, and shall be implemented under the National Assembly’s Resolution No. 08/2011/QH13.

Article 18. Implementation responsibilities

1. Tax offices at all levels shall disseminate and guide organizations, individuals and taxpayers in implementing this Circular.

2. Organizations, individuals and taxpayers governed by this Circular shall comply with this Circular.

Any problems arising in the course of implementation should be promptly reported to the Ministry of Finance for study and settlement.-

|

|

FOR

THE MINISTER OF FINANCE |

Form No.: 01-7/GTGT

(Issued together with the Circular No.154/2011/TT-BTC dated 11/11/2011 of the Ministry of Finance)

APPENDIX

TABLE FOR DETERMINING THE AMOUNT OF PREFERENTIAL VALUE ADDED TAX UNDER THE RESOLUTION No.08/2011/QH13

(Together with to the VAT declaration-form No.01/GTGT day .... month .... year ....)

[01] Taxation perriod: month ……… year …………

[02] Tax payer’s name: ...................................................................................

|

[03] Tax code: |

|

|

|

|

|

|

|

|

|

|

|

|

|

[04] Tax agent’s name (if any): ...........................................................................

|

[05] Tax code: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Currency Unit: VND

|

No |

Indicators |

Code |

Amount |

|

1 |

Output VAT of industrial shift-meal providing services for workers |

[6] |

|

|

2 |

Input VAT of industrial shift-meal providing services for workers ([7] = [8] + [12] + [14]) |

[7] |

|

|

2.1 |

Input VAT of goods, services used separately for industrial shift-meal providing services for workers |

[8] |

|

|

2.2 |

Percentage (%) between revenues subject to VAT and total sales of goods and services sold [9] |

[9] |

|

|

2.3 |

VAT of goods, services of general use to be deducted |

[10] |

|

|

2.4 |

Percentage (%) of sales of industrial shift-meal providing services for workers and total revenues subject to VAT. |

[11] |

|

|

2.5 |

Input VAT of goods, services of general use to be deducted allocated for industrial shift-meal providing services for workers ([12] = [10] x [11]) |

[12] |

|

|

2.6 |

Percentage (%) of sales of industrial shift-meal providing services for workers and total revenues of sold goods and services subject to VAT. |

[13] |

|

|

2.7 |

Input VAT of fixed assets of general use allocated for the industrial shift-meal providing services for workers |

[14] |

|

|

3 |

VAT of industrial shift-meal providing services for workers incurred in the period ([15] = [6] - [7] |

[15] |

|

|

4 |

Preferential VAT of industrial shift-meal providing services for workers ([16] = [15] x 50%) |

[16] |

|

I certify that the data provided above is correct and take responsibility before law for the declared data.

|

|

Day

…..month …..year …… |

Note of Appendix No.: 01-7/GTGT

[6] Means the sum of data in column 9 of the lines having content of column 10 "preferential review according to NQ 08" of the indicator 4 "Goods and services subject to tax rate of 10%" in Appendix 01-1/VAT issued together with the Circular No.28/2011/TT-BTC.

[8] Means the sum of data in column 10 of the lines having content of column 11 "preferential review according to NQ 08" of the indicator 1 "Goods and services used separately for business and production subject to VAT which are eligible for deduction" in Appendix 01-2/GTGT issued together with the Circular No.28/2011/TT-BTC.

[9] By percentage (%) between indicator (**) compared with the indicator (*) in Appendix 01-1/GTGT issued together with the Circular No.28/2011/TT-BTC.

[10] By the sum of data in column 10 of the lines without content of column 11 "fixed assets preferentially reviewed according to NQ08 "under indicator 3 "Goods and services used generally for business and production subject to VAT and non-VAT which are eligible for deduction" in Appendix 01-2/GTGT issued together with the Circular No.28/2011/TT-BTC multiplying with indicator [9].

[11] By percentage (%) between the sum of data in column 9 of the lines having content of column 10 "preferential review according to NQ 08" of indicator 4 “goods and services subject to tax rate of 10%" compared with indicator (**) in Appendix 01-1/GTGT issued together with the Circular No.28/2011/TT-BTC.

[13] By percentage (%) between the sum of data in column 9 of the lines having content of column 10 "preferential review according to NQ 08" of indicator 4 "goods and services subject to tax rate of 10%" compared with indicator (*) in Appendix 01-1/GTGT inssued together with Circular No.28/2011/TT-BTC.

[14] By the sum of data in column 10 of the lines having content of column 11 "fixed assets preferentially reviewed according to NQ08" under indicator 3 "Goods and services used generally for business and production subject to VAT and non-VAT which are eligible for deduction" in Appendix 01-2/GTGT issued together with the Circular No.28/2011/TT-BTC multiplying with the indicator [11].

Form No.: 25/MGT-TNCN

(Issued together with the Circular No. 154/2011/TT-BTC dated 11/11/2011 of the Ministry of Finance)

SOCIALIST

REPUBLIC OF VIETNAM

Independence – Freedom - Happiness

---------------

APPENDIX

PERSONAL INCOME TAX REDUCTION, EXEMPTION BY

THE RESOLUTION No.08/2011/QH13

[01] Name of Tax payer: ....................................................................................

|

[02] Tax code: |

|

|

|

|

|

|

|

|

|

|

|

|

|

[03] Tax agent’s name (if any): ...............................................................................

|

[04] Tax code: |

|

|

|

|

|

|

|

|

|

|

|

|

|

I. Individuals having income from salary or wages; income from business

(Attached to the declaration of personal income settlement in the form No.09/KK-TNCN issued together with the Circular No.28/2011/TT-BTC dated 28/02/2011 of the Ministry of Finance)

[05]: The tax amount payable before exemption, deduction: ..................................... ....................

[06]: The tax amount deducted for the entire year for income from salary or wages; from business of individual having taxable income at step-ladder 1 of partially progressive Tariff: ........ .................................................. ...........

[07]: Contracted personal income tax deducted 50% (if any): ....................

[08]: The tax payable after exemption, deduction: .................................... ..................

II. Individuals transferring securities registered tax rate of 20% (attached the declaration of personal income settlement in the Form No.13/KK-TNCN issued together with the Circular No.28/2011/TT-BTC dated 28/02/2011 of the Ministry of Finance)

[09]: The tax amount payable at the rate of 20% before exemption, deduction: ............................

[10]: Reduced tax: ......................................... ...........................................

[11]: The tax amount payable at the rate of 20% after exemption, deduction: ........................

III. Organizations paying salaries and wages settled on behalf of individuals

(Attached to the declaration of personal income settlement in the form No.05A/KK-TNCN issued together with the Circular No.28/2011/TT-BTC dated 28/02/2011 of the Ministry of Finance)

[12]: The total tax amount payable of ..... (write down the total number of individuals whom the paying organizations are on behalf of) before exemption, deduction:

[13]: The total amount of reduced tax of .... (write down the total number of individuals whom the paying organizations are on behalf of - having taxable income of the whole year at step-ladder 1) individuals having taxable income from salaries, wages at step-ladder 1 of partially progressive Tariff:

[14]: The total tax amount payable after exemption, deduction: ................................... ...........

IV. Organizations being responsible for withholding personal income tax from securities transfers, capital investment (attached to declaration of personal income settlements in the form No. 06/KK-TNCN issued together with the Circular No. 28/2011/TT-dated 28/02/2011 of the Ministry of Finance)

a. Income from capital investment:

[15]: The total tax amount required to be withheld before exemption, deduction: ................................... .......

[16]: The total tax exempted: ........................................ ....................................

[17]: The total amount of tax withheld after exemption, deduction: ................................... .............

b. Income from securities transfers:

[18]: The total tax amount required to be withheld before exemption, deduction: ................................... .......

[19]: The total tax reduced: ........................................ ....................................

[20]: The total amount of tax withheld after exemption, deduction: ................................... .............

I certify that the data provided above is correct and take responsibility before law for the declared data.

|

|

Day

…..month …..year …… |