Circular No. 34/2013/TT-BTC amending and supplementing a number of articles đã được thay thế bởi Circular 301/2016/TT-BTC on guidelines for the registration charge và được áp dụng kể từ ngày 01/01/2017.

Nội dung toàn văn Circular No. 34/2013/TT-BTC amending and supplementing a number of articles

|

THE MINISTRY

OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 34/2013/TT-BTC |

Hanoi, March 28, 2013 |

CIRCULAR

AMENDING AND SUPPLEMENTING A NUMBER OF ARTICLES OF THE CIRCULAR NO. 124/2011/TT-BTC OF AUGUST 31, 2011, OF THE MINISTRY OF FINANCE, GUIDING REGISTRATION FEE

Pursuant to the Ordinance on Charges and Fees;

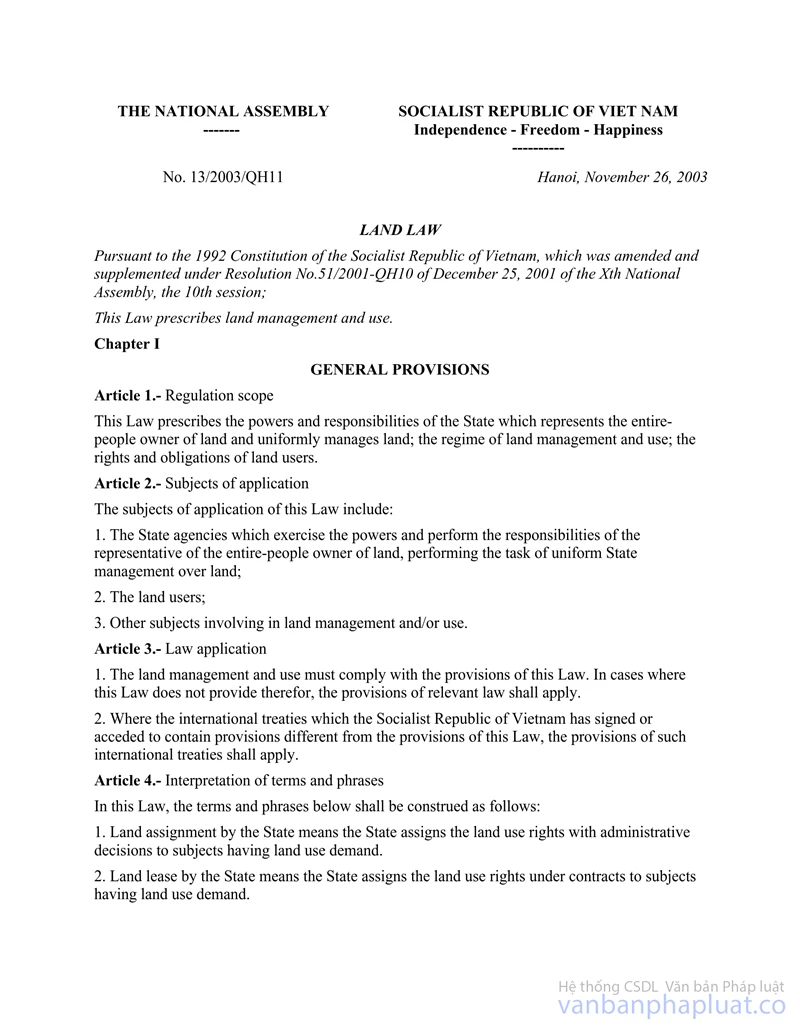

Pursuant to the 2003 Land Law and Government’s Decrees detailing the 2003 Land Law;

Pursuant to the Law on Tax Administration and Government’s Decrees detailing implementation of the Law on Tax Administration;

Pursuant to the Government’s Decree No. 45/2011/ND-CP of June 17, 2011, on registration fee;

Pursuant to the Government’s Decree No. 23/2013/ND-CP of March 25, 2013, on amending and supplementing some articles of the Government’s Decree No. 45/2011/ND-CP of June 17, 2011, on registration fee;

Pursuant to the Government’s Decree No. 118/2008/ND-CP of November 27, 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

At the proposal of Director General of the General Department of Taxation;

The Minister of Finance promulgates the Circular amending and supplementing a number of articles of the Circular No. 124/2011/TT-BTC of August 31, 2011, guiding registration fee as follows:

Article 1. To amend Article 3, Chapter 1 as follows:

1. To amend clause 10 of Article 3 as follows:

“Houses and land inherited or donated between spouses; between natural parent and natural child; adoptive parent and adopted child; parent-in-law and daughter-in-law- or son-in law; paternal grandparent and grandchild; maternal grandparent and grandchild or between siblings, for which land use right certificates or certificates of ownership of houses and other assets attached to land are granted by competent state agencies”

For these cases, when making registration fee registration, property recipients shall produce to tax agencies lawful papers proving their relationships with heirs, property givers or a written certification of the relationship above, made by the People's Committee of the commune, ward or township in which the property givers or recipients permanently reside.

2. To amend clause 18 of Article 13 as follows:

“18. Properties of organizations or individuals for which registration fee has been paid and which are subject to re-registration of ownership or use rights as a result of division, splitting, equitization, consolidation, merger or renaming of organizations under decisions of competent state agencies

In case the renaming is made simultaneously with the change of property owners, the property owners shall have to pay registration fee”.

3. To amend clause 25 of Article 3 as follows:

“25. Workshops of production establishments; warehouses, dining halls and garages of production and business establishments”.

Article 2. To amend Article 4, Chapter II as follows:

“Article 4. Bases for registration fee calculation and registration fee rates

1. Bases for registration fee calculation include registration fee calculation price and registration fee rate (%).

2. Registration fee level:

To be determined according to the percentage rate on values of assets calculated registration fee which are specified for each asset type subject to registration fee at Article 7 of the Government’s Decree No. 45/2011/ND-CP of June 17, 2011 on registration fee and amended and supplemented at clause 4, Article 1 of the Government’s Decree No. 23/2013/ND-CP of March 25, 2013.

3. The payable registration fee amount is determined as follows:

|

Payable registration fee amount (VND) |

= |

Registration fee calculation price (VND) |

x |

Registration fee rate (%) |

The maximum registration fee level that must remitted into state budget, excluding passenger cars of under 10 seats (including the driver's), aircraft and yachts, is VND 500 million/property/time of registration.”

Article 3. To amend Article 5, Chapter II as follows:

“Article 5. Registration fee calculation prices

Registration fee calculation prices are prices issued by provincial-level People's. The provincial Departments of Finance shall coordinate with relevant departments and sectors in formulating and submitting to provincial-level People’s Committees for decisions on formulating the registration fee calculation price tables in accordance with regulation as follows:

1. Principles of issuance of registration fee calculation price table:

a) For land:

The land prices to calculate registration fee are the land prices promulgated by provincial-level People's Committees under the land law at time of declaration for registration fee submission.

b) For houses: Provincial-level Finance Departments shall assume the prime responsibility for and coordinate with provincial-level Construction Departments in formulating registration fee calculation prices on the basis of the actual "new" construction price of one (01) m2 of floor area of houses of each grade and class and submit to the provincial People’s Committee for promulgation and application in their localities.

c) For other properties:

The values of assets calculated registration fee are defined on the basis of suitability with the actual transfer prices of assets on domestic market.

The actual transfer prices of assets on market are defined under the database that local function agencies collected from: the sale prices declared by business and production establishments to tax agencies; price information from concerned state management agencies (the customs agencies, the provincial Departments of Industry and Trade, the Center of Price Verification of the Ministry of Finance, so on); the trading prices of the same assets in the same locality or in other localities; information collected from consumers; information on prices of assets on mass media such as newspapers, magazines, market newsletter and so on.

Principles for formulating the price table in several specific cases:

+ For sold/purchased assets: Registration lee calculation prices must not be lower than the prices stated in the sellers’ lawful sale invoices.

+ For produced/manufactured assets: Registration fee calculation prices must not be lower than the sale prices according to notice of producers. For assets are produced for consumption, the Registration fee calculation prices must not be lower than production costs of producers.

+ Registration fee calculation prices for directly-bought assets from the domestic establishments allowed to produce, assembly (generally called as production establishment) is the actual payment price (the sale price included VAT and excise tax – if any) inscribed in legal sale invoices.

Organizations, individual that buy goods from sale agents directly signing the agent contracts with production establishments and selling at the prices set by production establishments are considered as cases of direct purchase from production establishment.

+ For import assets not in the price tables prescribed by the provincial-level People’s Committees at the time of registration, the provincial Departments of Finance shall coordinate with concerned departments and sectors in need of reference of sale prices of assets of the same kind on domestic market and import prices according to the import tax calculation prices that have been defined by customs agencies and relevant costs to submit the provincial People’s Committee for timely promulgation.

The provincial People’s Committees shall direct function agencies to formulate the registration fee calculation price for each type of asset in order to have basis for defining and issuing the registration fee calculation price table, methods to define registration fee calculation prices for assets including housing and land, ships, boats, automobiles, motorcycles, hunting guns and sport guns apply in localities in each period.

In the course of registration fee collection management, when tax agencies detect or receive comments of organizations or individuals involving registration fee calculation prices of assets which have not yet been suitable with price determination specified in this Circular or prices of those assets have not been included in the local registration fee calculation price table, the provincial Departments of Taxation must have timely proposals (not later than 05 working days) and sent them to the provincial People’s Committees or agencies authorized in promulgation of the price tables for amending, supplementing the registration fee calculation price table.

Within 15 days after issuing the registration fee calculation price tables, the issuing agencies must send them to the Ministry of Finance (the General Department of Taxation) for monitoring implementation.

2. Bases for determining values of assets to calculate registration fee:

a) For land:

Bases for determining the land value to calculate registration fee include the whole land area subject to registration fee and land prices for registration fee calculation.

For the land purchased by method of auction in accordance with regulations of law on bidding, auction, the registration fee calculation price is the actual auction winning price inscribed in the sale invoice.

b) For houses:

Bases for determining housing value to calculate registration fee include the house area subject to registration fee and prices of 1 meter square house for calculation of registration fee.

Several special cases for determining registration fee calculation prices as follows:

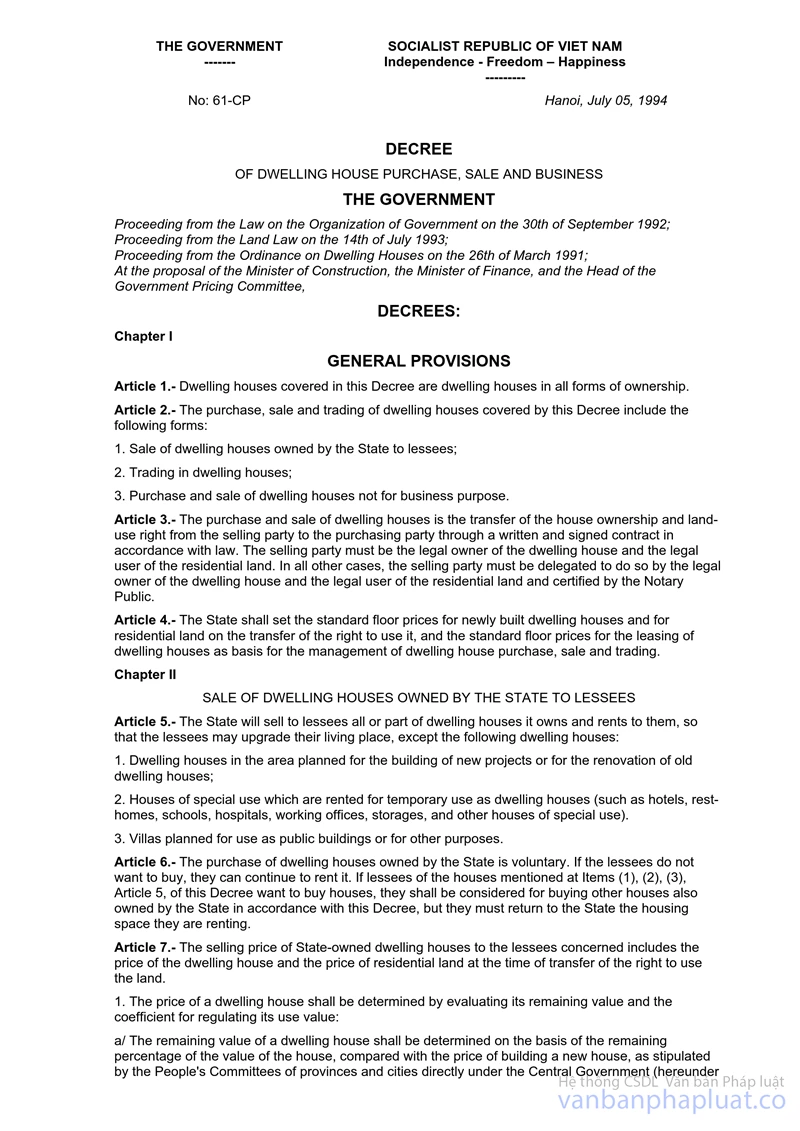

- The registration fee calculation price of state-owned house sold to lessee under the Government’s Decree No. 61/CP, of July 05, 1994 is the real sale price inscribed in the invoice of house sale according to decision of provincial People’s Committee.

- The registration fee calculation price of resettlement house of which specific price has been approved by competent state agencies and the approved price has been balanced by clearing between the compensation price for the revoked place and house price in resettlement place, shall be the house price approved by competent state agencies.

- For the houses purchased by method of auction in accordance with regulations of law on bidding, auction, the registration fee calculation price are the actual auction winning price inscribed in the sale invoice.

c) For other assets such as aircraft, ships, boats, automobiles, trailers, motorcycles, hunting guns and sports guns:

Tax agencies shall base on the registration fee calculation price tables promulgated by provincial-level People’s Committees to calculate registration fee. In case where the price inscribed in invoice is higher than the price stipulated by provincial People’s Committee, the price in invoice shall be applied.

Asset value to calculate registration fee is the registration fee calculation price as prescribed in the registration fee calculation price table issued by provincial People’s Committee in principled specified in clause 1 of this Article.

In case of assets bought under the installment method, the registration fee shall be calculated under entire the set value of asset upon payment once (excluding interest rate of installment).

Article 4. To amend clause 4 and clause 5, Article 6, Chapter II as follows:

1. To supplement the following provision in the end of item a, clause 4:

“Centrally-run cities, provincial cities; towns where the People’s Committees of provinces and centrally-run cities place their headquarters defined by state administrative boundaries at the time of registration fee declaration, of which: a centrally-run city covers all districts affiliated that city, irrespective of inner city or suburb districts, rural or urban districts; the provincial cities and towns where the provincial People’s Committees place their headquarters covering all wards and communes of that city or town, irrespective of inner city, town or suburb communes”.

2. To replace clause 5 of Article 6 by new clause 5 as follows:

“5. For automobiles, trailers or semi trailers drawn by automobiles: 2%.

Particularly for passenger cars of under 10 seats (including the driver's), the first-time registration fee shall be paid at a rate of 10%. In case application of a higher rate which is suitable with actual conditions of each locality is neccessary, the People’s Council of a province or centrally-run city shall decide adjustment for increase but the maximum rate does not exceed 50% of the general provided rate.

Automobiles carrying passengers less than 10 seats (including driver) shall be paid the registration fee from the second time forward at the rate of 2% and applied uniformly in nationwide.

Tax agencies shall define the level of registration fee for automobiles on the basis:

- Number of seats in automobile that is defined under design of producer;

- Type of automobile that is defined as follows:

In case of imported automobiles, basing on the determination of Register Agencies in the section “Type of vehicle” of its Certificate of technical safety quality and environmental protection or Notice for exemption from inspection on technical safety quality and environmental protection for imported motor vehicles been issued by Vietnam Register agencies;

In case of automobiles that are produced and assembled in country, basing on the section “Type of vehicle” inscribed in their Certificates of technical safety quality and environmental protection or the slip of inspection of ex-workshop quality for motor vehicles;

In case where the section “Type of vehicle” of the papers mentioned above fail to determine as trucks, registration fee for passenger automobiles shall be applied.

If upon check, the police agencies issuing the vehicle register number plate detect that the Certificate of technical safety quality and environmental protection or the Notice on exemption from inspection on technical safety quality and environmental protection or the slip of inspection of ex-workshop quality used for motor vehicle inscribed improperly with type of trucks or passenger automobiles, leading to applying inconsistent the registration fee collection level, shall inform timely to the register agencies for re-determining type of vehicle before issuing number plate. In case where the register agency re-determine type of vehicle and accordingly must re-calculate the level of receivable registration fee, the police agency shall transfer dossier attached with the verifying documents to tax agencies for issuance of notice of receivable registration fee in accordance with regulation.”

Article 5. To amend Article 7, Chapter III as follows:

“Article 7. Owing of registration fee

1. Subjects allowed owing registration fee:

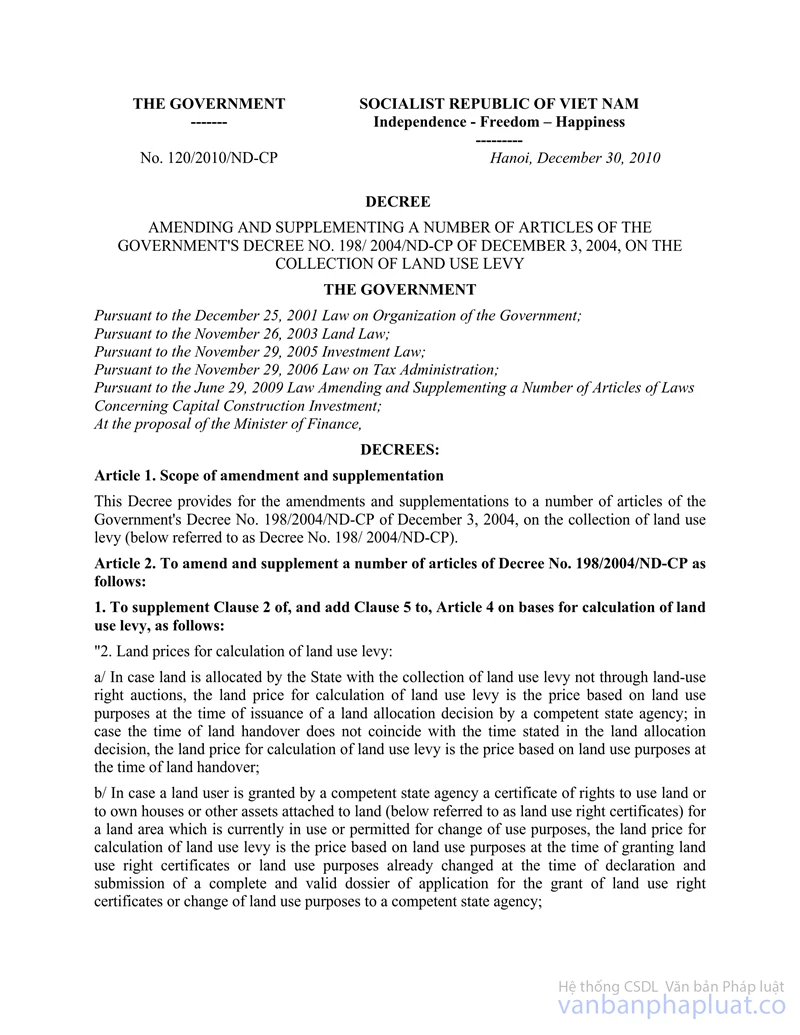

To own registration fee for Houses and residential land of households or individuals subject to owe land use levy under Clause 8 Article 2 of the Government's Decree No. 120/2010/ND-CP of December 30, 2010, amending and supplementing a number of articles of the Government's Decree No. 198/2004/ND-CP of December 3, 2004, on collection of land use levy.

2. Payment of owed registration fee:

When paying the owed registration fee, households and individuals must pay the registration fee which is calculated under the land and housing price prescribed by the provincial People's Committee at the time of determining the obligation of land use levy payment.

In case households or individuals entitled to owe registration fee upon transfer or swap such houses or land plots to others, they must pay full owed registration fee amount before carrying out such transfer or swap.

3. Procedures for owing registration fee:

a/ Households or individuals entitled to owe registration fee for houses or residential land specified in Clause 1 of this Article shall submit dossiers (comprising documents evidencing their eligibility to owe registration fee under Clause 1 of this Article) to competent state agencies according to law.

b/ Agencies competent to grant house ownership or residential land use right certificates shall inspect the dossiers and if ascertaining that the applicants are entitled to owe registration fee for houses or residential land under Clause 1 of this Article, write in the house ownership or residential land use rights certificates the phrase "Registration fee owed" before handing such certificates to the house owners or land users.

When receiving dossiers of application for carrying out procedures for the transfer or swap of house ownership or land use rights submitted by households or individuals that still owe registration fee, agencies competent to grant house ownership or residential land use right certificates shall transfer such dossiers together with a "sheet on cadastral information for performance of financial obligations" to tax agencies for the latter to calculate and notify the owed registration fee amount to the households or individuals for full payment before carrying out transfer or swap procedures.”

Article 6. Effect

1. This Circular takes effect on April 01, 2013. Other regulations contrary to this Circular shall be annulled.

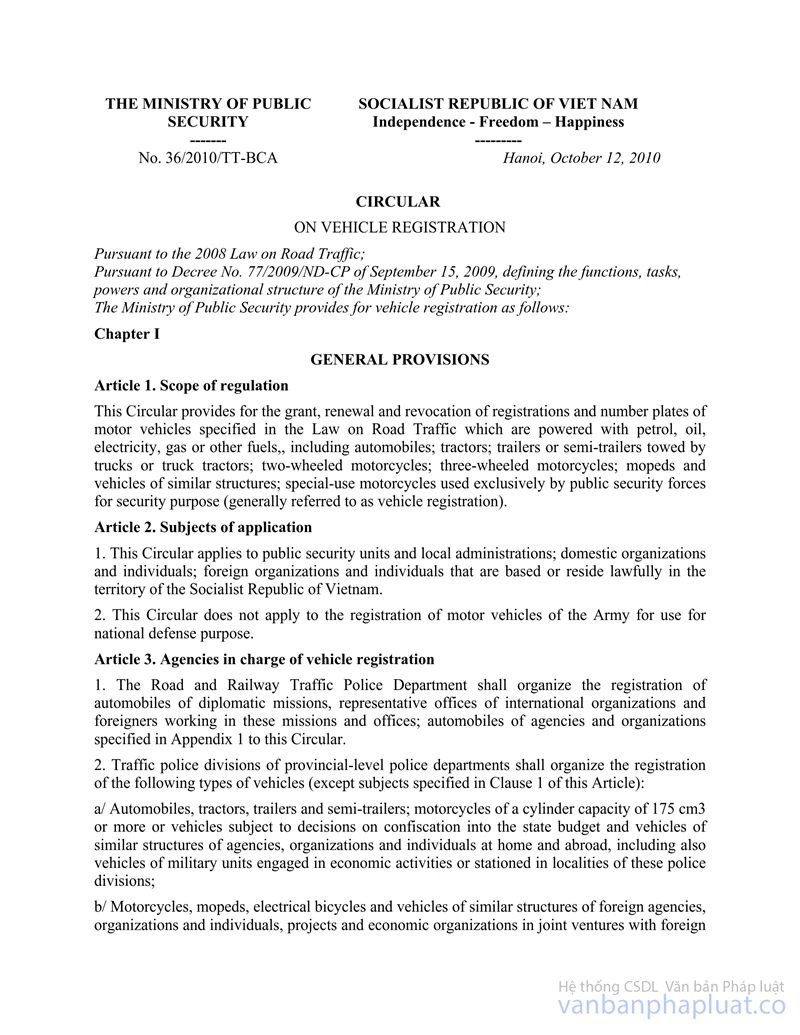

2. For case where vehicles that have been registered and transferred through many people and settled to register in accordance with the Circular No. 12/2013/TT-BCA of March 01, 2013 of the Ministry of Public Security amending, supplementing clause 3, Article 20 of the Circular No. 36/2010/TT-BCA of October 12, 2010 on vehicle registration, dossier of registration fee declaration is the legal dossier to register vehicle ownership and use right, including papers in accordance with regulations of the Ministry of Public Security and other papers in accordance with law on tax administration (except for vouchers of registration fee payment).

3. Organizations and individuals having assets subject to registration fee, relevant agencies shall implement the Government’s Decree No. 23/2013/ND-CP the Government’s Decree No. 45/2011/ND-CP and guides in the Circular No. 124/2011/TT-BTC and this Circular.

For automobiles carrying passengers less than 10 seats (including driver) that are registered for the first time in provinces, cities applying the rates higher than 10% but not exceeding 15%, the rates of registration fee in accordance with current regulation shall be applied and if the rates are higher than 15%, the rates of registration fee shall be 15% untill such People’s Councils of provinces or central-run cities promulgate new rates of registration fee as prescribed in the Decree No. 23/2013/ND-CP.

For automobiles carrying passengers less than 10 seats (including driver) that are registered from the second time forward, they shall pay the registration fee at the rate of 2% and applied uniformly in nationwide.

4. In the course of implementation, any problems arising should be promptly reported to the Ministry of Finance for study and additional guidance.

|

|

FOR THE

MINISTER OF FINANCE |

------------------------------------------------------------------------------------------------------

This translation is translated by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments