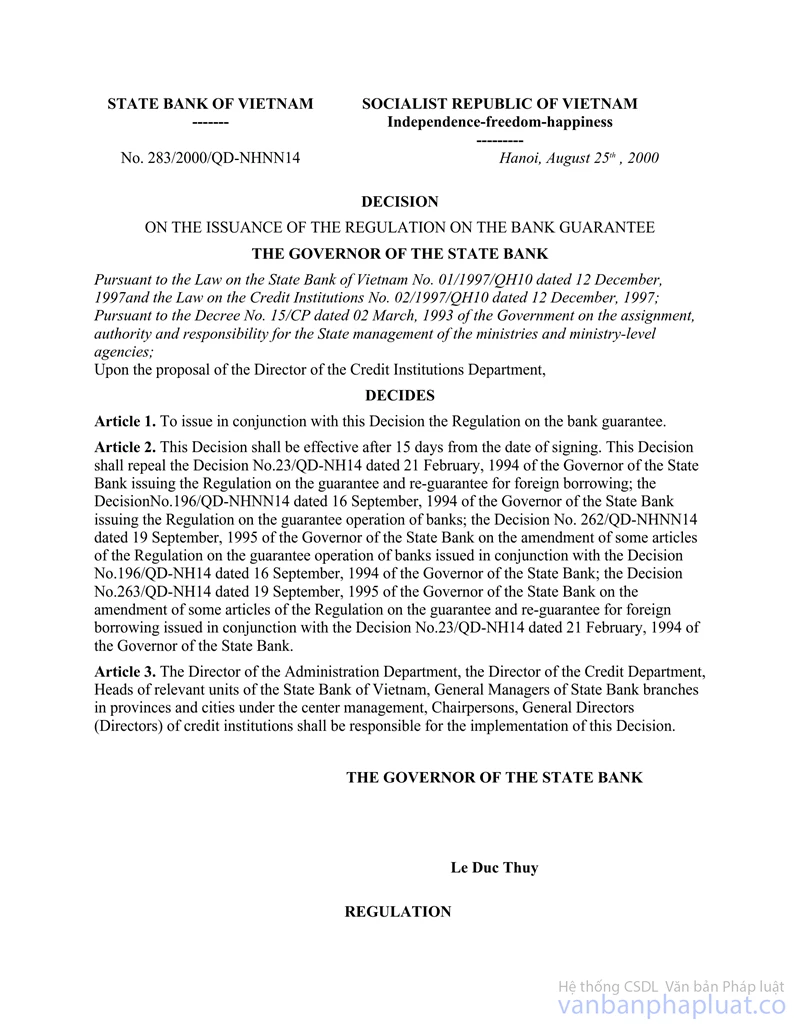

Decision No. 196/QD-NH14 1994 on the promulgation of regulation on guaranty operations of banks đã được thay thế bởi Decision No. 283/2000/QD-NHNN14 of August 25, 2000, on the issuance of the regulation on the bank guarantee và được áp dụng kể từ ngày 09/09/2000.

Nội dung toàn văn Decision No. 196/QD-NH14 1994 on the promulgation of regulation on guaranty operations of banks

|

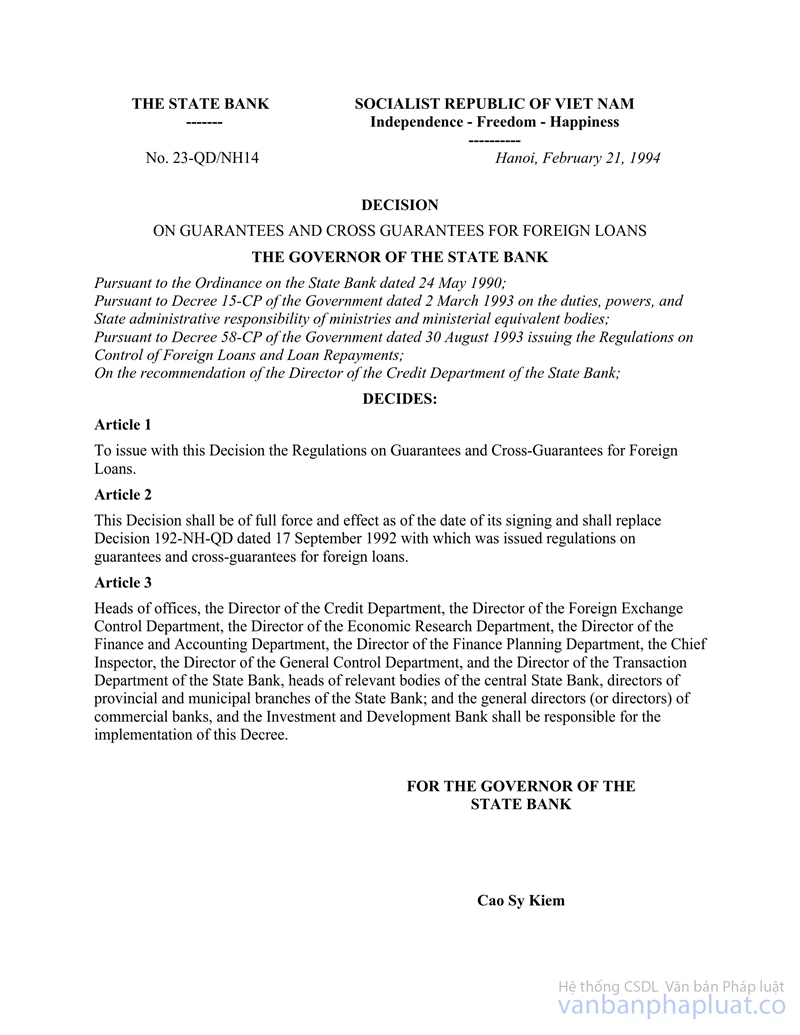

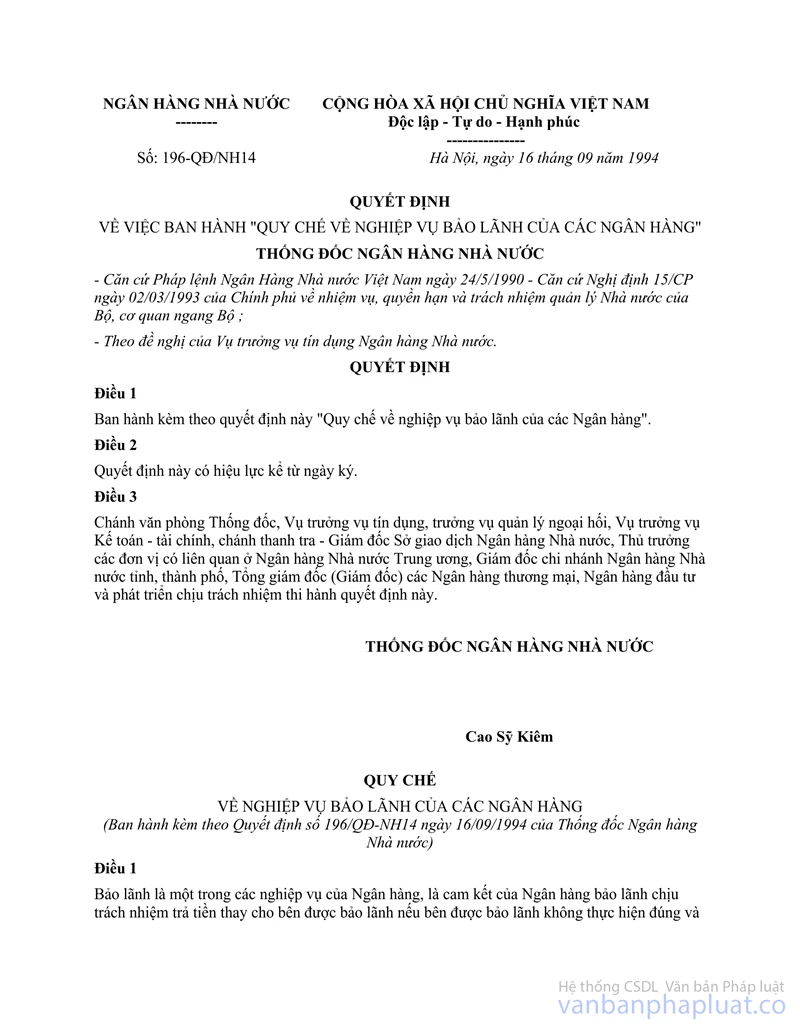

THE STATE BANK OF VIETNAM ------- |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 196/QD-NH14 |

Hanoi, September 16, 1994 |

DECISION

ON THE PROMULGATION OF REGULATION ON GUARANTY OPERATIONS OF BANKS.

THE GOVERNOR OF THE STATE BANK OF VIETNAM

Pursuant to the Ordinance on

State Bank of Vietnam dated may 24, 1990;

Pursuant to the Decree No. 15/CP dated March 2nd, 1993 of the Government

stipulating the task, power and responsibility for the State management of the

Ministries and Ministerial-ranking offices;

On the proposal of the Director of the Credit Department of the State Bank of

Vietnam.

DECIDES

Article 1 :

To promulgate hereby in connection with this Decision "The regulations on Guaranty operations of Banks"

Article 2 :

This Decision shall come into effect from the signing date.

Article 3 :

The chief of Governor's Office, the Director of the Credit Department, the Director of the Foreign Exchange, Director of the Department for accounting - finance, the General Inspector, the Director of the State Bank's Department for External Relations, the Heads of the concerned sections in the Central State Bank, the Directors of the State Banks of provinces and cities, the General Directors (Directors) of the Commercial Banks, the Investment and Development Banks shall be responsible for the implementation of this Decision.

|

|

FOR

THE STATE BANK OF VIETNAM |

REGULATIONS

ON GUARANTY OPERATIONS OF BANKS

(Promulgated in Connection with Decision No. 196/QD-NH14 dated

September 16th, 1994 of the Governor of the State Bank of Vietnam)

Chapter I

GENERAL PROVISIONS

Article 1 :

Guaranty, as one of many operations of banks, is the commitment of a guaranty bank to take responsibility for paying the debt instead of the guaranteed party if the latter does not carry out correctly and fully its agreed obligations to the guaranty - requesting party. The obligations are specifically prescribed in the bank's letter of guaranty.

The guaranteed party is responsible for fulfilling its commitments to the guaranty - requesting party and to the guaranty bank.

Article 2 :

Guaranty banks are state-owned commercial banks, joint-stock commercial banks, joint-venture banks, foreign bank branches, investment and development banks. In special cases, when it is designated by the Government, the State Bank of Vietnam shall joint other banks in offering a guaranty.

Article 3 :

Guaranteed parties are enterprises (including credit organizations) which are established and operated in accordance with the existing laws of Vietnam.

Article 4 :

Banks carry out guaranty operations in the cases that enterprises request guaranty for contract bidding and implementation, for the repayment of advances, financial transactions, for the product quality as agreed upon in the contracts, for the repayment of borrowed capital, etc... (as in accompanying annex). Requests for guaranty regarding the borrowing of foreign capitals are met in accordance with the Regulations on guaranty and re-guaranty for loan of foreign capital promulgated in connection with Decision No. 23/QD-NH14 dated February 21, 1994 of the Governor of the State Bank of Vietnam.

Article 5 :

Many banks can at the same time offer guaranty for one guaranteed party (enterprise)

Guaranty banks have the right to decide whether or not to offer guaranty for a client on the basis of conditions set forth by the guaranty - requesting party.

Chapter II :

SPECIFIC PROVISIONS

Article 6 :

Conditions for guaranty

Enterprises which want to be guaranteed have to obtain the following conditions :

- Having legal status and operating in accordance with the existing laws of Vietnam;

- Having a contract relating to the guaranty;

- Operating profit - yielding businesses;

- Having proved reliable credit and payment relations;

- Having licenses for import export businesses if these businesses relate to the guaranty.

- Having no overdue debts in neither Vietnamese dong nor foreign currencies.

- Having enough properties to be used as legal collateral's for guaranty.

Article 7 :

Enterprises which request guaranty have to submit to the guaranty banks the following documents :

- Application for guaranty (attached form);

- Contract and documents relating to the guaranty;

- Licenses for exports and imports (in the cases that the guaranty relates to the businesses).

- A list of items of properties for collateral

Article 8 :

The duration of guaranty is determined on the basis of time needed for carrying out each obligation agreed upon by participating parties. In case one or more parties wish to change the previously agreed duration, this change must be accepted by the guaranty bank in a written document.

Article 9 :

The guaranty is carried out in form of letter of guaranty issued by guaranty bank. The duration for guaranty begins from the time proposed by the enterprise and it is prescribed in the letter of guaranty.

Article 10 :

Properties for collateral are real estates : land, houses ..., personal estates : gold, gems ... money bearing documents (bank bonds, credit cards ...) and have to gather enough of the following conditions :

- For the properties as real estates : It is compulsory to have the licenses of ownership (the original documents) which are ratified by state notary offices and easily transferable;

- For the bank bonds and credit cards ... They must be valid for transaction, issued by credible organizations, easily transferable and in the possession of the enterprise that requests the guaranty;

- For gold and gems : They must be appraised by the guaranty bank or a professional office designated by the guaranty bank : the guaranty - requesting enterprise has to wrap them up and put seals on them by itself at the witness of the guaranty bank before giving them to the bank.

For state - owned enterprises, the use of properties generating from state budget's' capital sources for collateral must be approved in the written form by the same ranking financial offices (the owners of the properties or their representatives).

Article 11 :

The guaranty bank determines guaranty fee and periodic payment that the enterprise has to pay for the bank. The fee may range to a maximum of 1% per year of the amount being guaranteed at that time.

Article 12 :

Money unit used in guaranty is the currency defined in the contract or agreement document between the guaranteed party and the body requesting a guaranty.

Article 13 :

Guaranty fund and guaranty amount : Banks base on the amounts of capital prescribed for doing business to project the amount of money in domestic and foreign currencies which can be mobilized for establishing their own guaranty funds. The total amount of money for guaranty defined on the basis of projected guaranty fund and the possibility of capital safety in guaranty of each bank, but the maximum amount can not exceed the amount of guaranty fund by 20 times (this means that the possibility for capital insecurity in guaranty can only reach a maximum of 5 percent).

The amount of money for establishing guaranty fund shall be accounted for by a separate sub-account at the guaranty bank on each guaranty operation with a minimum ratio of 5 per cent of the total guaranty turnover and can be used to pay the guaranty requesting bank when the guaranteed enterprise does not fulfill its obligation.

The total amount of money for guaranty for one enterprise can not exceed 10 percent and for ten enterprises can not exceed 30 percent of the total amount of money for guaranty of a guaranty bank.

Article 14 :

Within 20 days, since it receives the dossier for guaranty, the guaranty bank has to inform the enterprise of the result whether or not to accept guaranty.

Article 15 :

The authority to sign a guaranty operation : General director (director) of a guaranty bank has the authority to sign a document of guaranty and can delegate power in written form to the deputy or the directors of its branches to sign documents of guaranty of a certain scale and has to take responsibilities for the actions of the delegated people. Delegated people can not delegate power to another person.

Article 16 :

When its request for guaranty is accepted by a guaranty bank, the enterprise conducts the procedures of submitting the properties (documents) for collateral to the guaranty bank. After receiving properties or property document for collateral, the guaranty bank executes the procedures for guaranty.

Article 17 :

The guaranty banks which store the properties for collateral are responsible for keeping and preserving them. In case of loss or damage of the collateral properties, the guaranty banks have to bear the responsibilities for compensation of the material damage.

Article 18 :

During the guaranty, the enterprises are responsible for keeping and preserving the collateral properties which remain in storage or are utilized; in case of loss or damage, the enterprises shall bear total responsibilities for it.

In the case of the collateral property being a money bearing document which expires before the guaranty duration comes to an end, the enterprise has to replace it with another valid document of the same quality. In case of failure, the guaranteed enterprise has to pay a fine of 1% per month of the value of the expired document.

Article 19 :

During the period of guaranty, the enterprise is subject to inspection and supervision of all activities relating to guaranty operation. At the same time, it is obliged to provide, at the request of guaranty bank, the necessary information and documents for that inspection and supervision work.

Article 20 :

The guaranteed enterprise has to acute all the obligation it has committed to the guaranty requesting party. Once it has fulfilled its obligations, the guaranty bank has to return all collateral properties (or collateral documents) to the guaranteed enterprise.

In the case, the guaranty bank has to fulfill the obligation of a guarantor, the enterprise has to recognize in paper its debt to the guaranty bank which paid in its place before that and for which the enterprise has to pay an interest of 150% for the overdue debt owed by such an enterprise to guaranty bank. After that the guaranty bank shall hold auction for the collateral properties to get back the amount of money it has paid in the place of the enterprise in accordance with the laws.

Chapter III :

PROVISIONS FOR IMPLEMENTATION

Article 21 :

The General Director (Director) of State-owned commercial banks, investment and development banks, joint-stock commercial banks, joint-venture bank and branches of foreign banks in Vietnam are reliable to provide guidance for the implementation of this Regulation within their own banking systems.

Article 22 :

Any changes to this Regulation are subject to the governor of the State Bank of Vietnam for final decision.

ANNEX

OF THE REGULATIONS ON GUARANTY OPERATIONS OF BANKS

1. Guaranty for contract bidding

- The guaranty bank commits itself to the contract issuing body on the participation of a contractor. In case the contractor has to pay a fine for violating the contract application, but it does not pay any or all of its to the contract issuing body, the guaranty bank shall pay instead of the contractor.

- Forms of guaranty for contract bidding.

+ Guaranty for bidding contracts of construction.

+ Guaranty for bidding contracts of supplying machinery and equipment (contracts of supply).

- The amount of money and duration of guaranty are those defined by the contract issuing body in accordance with the regulations on contract bidding.

2. Guaranty for the contract implementation

- Guaranty bank commits itself to the contract implementation by the contractor. In the case that the contractor does not implement the contract and nor pay any or all of the fine to the contract issuing body, the guaranty bank shall pay instead of the contractor.

- Forms of guaranty for the implementation of contract

+ Guaranty for implementation of construction contract

+ Guaranty for implementation of contract for machinery and equipment supply (contract of supply).

- The amount of money and duration of guaranty are those defined by the contract issuing body and contractor in the contracts.

3. Guaranty for the advances.

- Guaranty bank commits to the contract issuing body on the use of the advances received by the contractor. In case the contractor violates the contract by not repaying any or all the advances to the contract issuing body, the guaranty bank is responsible for payment on behalf of the contractor.

- Forms of guaranty for the advances :

+ Guaranty for the advances used for the execution of the project.

+ Guaranty for the advances used for manufacturing machinery and equipment.

- The amount of money and duration of the guaranty are those defined by the contract issuing body and the contractor in the contract.

4 - Guaranty for payment.

- Guaranty bank commits itself to the contract issuing body on the payment in accordance with the contract. In the case that the contractor does not pay any or all of the amount of money as defined in the contract, the guaranty bank is responsible for the payment of the contractor.

- Forms of guaranty :

+ Guaranty for the payment of construction costs.

+ Guaranty for the payment of machinery and equipment installation.

- The amount of money and duration of the guaranty are those defined by the contract issuing body and the contractor in the contract.

5. Guaranty for the product quality as defined in the contract.

Guaranty bank commits to the contract issuing body on the case that the contractor violates the contract in regard to product quality and therefore has to compensate for the issuing body of the contract, but the contractor does not compensate any or all, the guaranty bank is responsible for payment on behalf of the contractor.

- Forms of guaranty :

+ Guaranty for the project quality

+ Guaranty for the quality of machinery and equipment.

- The amount of money and duration of guaranty are those defined by the contract issuing body and the contractor in the contract.

6. Guaranty for the repayment of borrowed capital.

- Guaranty bank commits itself to the lender that in the case that the borrower does not pay all nor on time the debt (both principal and interest), the guaranty bank shall be responsible for the payment on behalf of the borrower.

The amount of money and duration of guaranty are those defined in the contract for borrowing capital.