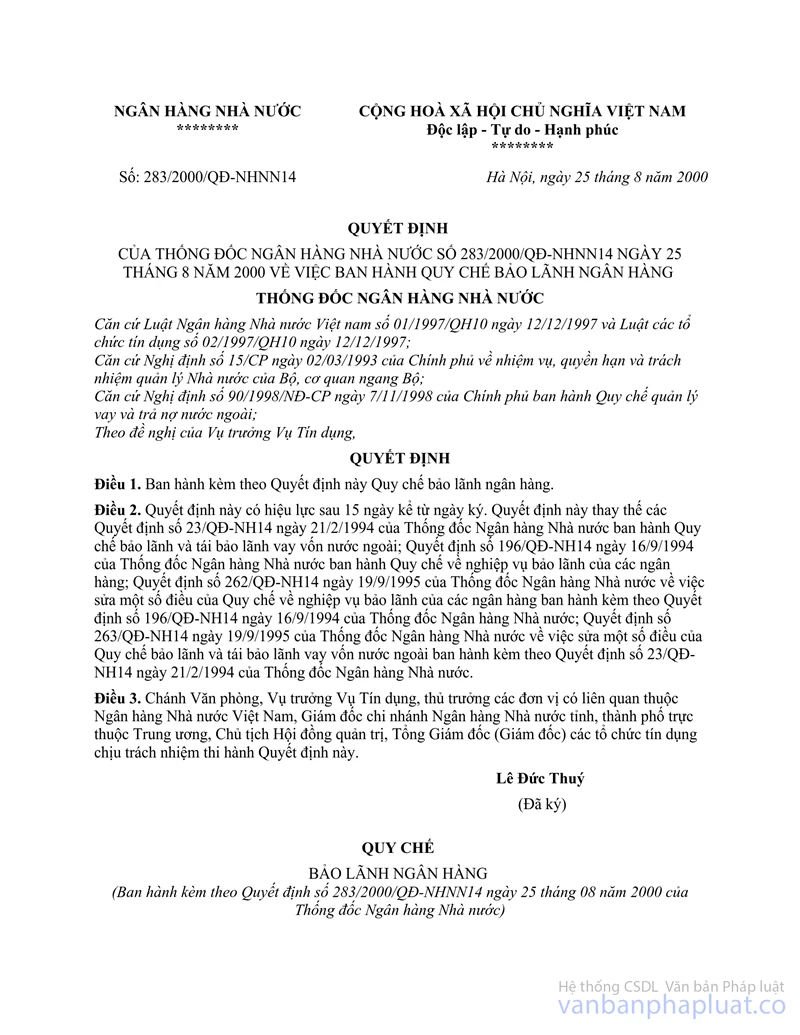

Decision No. 283/2000/QD-NHNN14 of August 25, 2000, on the issuance of the regulation on the bank guarantee đã được thay thế bởi Decision No. 26/2006/QD-NHNN of June 26, 2006, promulgating the regulation on bank guaranty và được áp dụng kể từ ngày 17/07/2006.

Nội dung toàn văn Decision No. 283/2000/QD-NHNN14 of August 25, 2000, on the issuance of the regulation on the bank guarantee

|

STATE

BANK OF VIETNAM |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 283/2000/QD-NHNN14 |

Hanoi, August 25th , 2000 |

DECISION

ON THE ISSUANCE OF THE REGULATION ON THE BANK GUARANTEE

THE GOVERNOR OF THE STATE BANK

Pursuant to the Law on the

State Bank of Vietnam No. 01/1997/QH10 dated 12 December, 1997and the Law on

the Credit Institutions No. 02/1997/QH10 dated 12 December, 1997;

Pursuant to the Decree No. 15/CP dated 02 March, 1993 of the Government on the

assignment, authority and responsibility for the State management of the

ministries and ministry-level agencies;

Upon the proposal of the Director of the Credit Institutions Department,

DECIDES

Article 1. To issue in conjunction with this Decision the Regulation on the bank guarantee.

Article 2. This Decision shall be effective after 15 days from the date of signing. This Decision shall repeal the Decision No.23/QD-NH14 dated 21 February, 1994 of the Governor of the State Bank issuing the Regulation on the guarantee and re-guarantee for foreign borrowing; the DecisionNo.196/QD-NHNN14 dated 16 September, 1994 of the Governor of the State Bank issuing the Regulation on the guarantee operation of banks; the Decision No. 262/QD-NHNN14 dated 19 September, 1995 of the Governor of the State Bank on the amendment of some articles of the Regulation on the guarantee operation of banks issued in conjunction with the Decision No.196/QD-NH14 dated 16 September, 1994 of the Governor of the State Bank; the Decision No.263/QD-NH14 dated 19 September, 1995 of the Governor of the State Bank on the amendment of some articles of the Regulation on the guarantee and re-guarantee for foreign borrowing issued in conjunction with the Decision No.23/QD-NH14 dated 21 February, 1994 of the Governor of the State Bank.

Article 3. The Director of the Administration Department, the Director of the Credit Department, Heads of relevant units of the State Bank of Vietnam, General Managers of State Bank branches in provinces and cities under the center management, Chairpersons, General Directors (Directors) of credit institutions shall be responsible for the implementation of this Decision.

|

|

THE

GOVERNOR OF THE STATE BANK |

REGULATION

ON THE BANK GUARANTEE

(issued in conjunction with the Decision No. 283/2000/QD-NHNN14 dated 25

August,2000 of the Governor of the State Bank)

Chapter I

GENERAL PROVISIONS

Article 1. Governing scope

This Regulation shall provide for the implementation of the guarantee operation by credit institutions for their customers.

Article 2. Interpretation

In this Regulation, following terms shall be construed as follows:

1. "Bank guarantee" is a written commitment of a credit institution (the guaranteeing party) to the obligee (the guarantee accepting party) in respect of the performance of financial obligation in lieu of the customer (the guaranteed party) upon the failure by the customer to perform or duly perform the obligation committed to the guarantee accepting party. The customer must recognize the debt and repay the credit institution the payment made on his behalf.

2. "Guaranteeing party" is credit institutions provided for in Article 3 of this Regulation;

3. "Guaranteed party" is customers provided for in Article 4 of this Regulation;

4. "Guarantee accepting party" is organizations, individuals, inside and outside the country, who are entitled to benefit from the guarantee commitments of credit institutions.

5. "Guarantee commitment" is an unilateral written commitment of credit institutions or a written agreement between credit institutions, guaranteed customers and guarantee accepting party that credit institutions shall perform financial obligations in lieu of customers upon the failure of customers to perform duly obligation committed to the guarantee accepting party.

6. "Guarantee contract" is a written agreement between credit institutions and customers in respect of the rights and obligations of the parties in the guarantee and repayment;

7. "Borrowing guarantee" is a bank guarantee issued by credit institutions to the guarantee accepting party in respect of the commitment to repay in lieu of customers in the event the customers fail to repay or repay adequately, timely;

8. "Payment guarantee" is a bank guarantee issued by credit institutions to the guarantee accepting party in respect of the commitment to make payment in lieu of the customers in the event the customers fail to perform or duly perform their obligation when it becomes due;

9. "Bidding guarantee" is a bank guarantee issued by credit institutions to the Bid inviting party to ensure the obligation of the customer to participate to the bid. In the event the customer is fined for violation of bidding requirements but fails to pay the fine or is not able to pay the fine to the bid inviting party, credit institutions shall perform the guarantee obligation as committed;

10. "Performance guarantee" is a bank guarantee issued by credit institutions to the guarantee accepting party to guarantee the adequate, full performance of obligations of a customer to the guarantee accepting party in accordance of a signed contract. In the event the customer fails to perform adequately, fully obligations stated in the contract, credit institutions shall perform the guarantee obligations as committed.

11. "Product quality guarantee" is a bank guarantee issued by credit institutions to the guarantee accepting party to guarantee the adequate performance of agreements on the quality of products in accordance with the contract signed with the guarantee accepting party. In the event the customer is fined due to its failure to adequately perform the contract's agreements on the product quality but fails to pay or pay fully the fine to the guarantee accepting party, credit institutions shall perform the guarantee obligations as committed;

12 "Repayment guarantee" is a bank guarantee issued by credit institutions to the guarantee accepting party to guarantee the obligation to repay the advance payment made by a customer under a contract signed with the guarantee accepting party. In the event the customer violates commitments undertaken towards the guarantee accepting party and must return the advance payment but fails to repay or repay fully the advance payment to the guarantee accepting party, credit institutions shall pay the advance payment to the guarantee accepting party.

13. "Counter guarantee" is a bank guarantee issued by credit institutions (the counter-guarantee issuing party) to an another credit institution (the guaranteeing credit institution) requesting the guaranteeing credit institution to provide a guarantee to the guarantee accepting party for obligations of the counter-guarantee issuing partys customer. In the event the borrower fails to honor the commitments made to the guarantee accepting party and the guaranteeing party must perform the guarantee obligations, the counter-guarantee issuing party shall perform the counter-guarantee obligations for the guaranteeing party;

14. "Guarantee confirmation" is a bank guarantee issued by credit institutions (the guarantee confirming party) to the guarantee accepting party to guarantee the performance of the guarantee obligations by another credit institution (confirmed party). In the event the confirmed party fails to perform or perform fully its obligation it has committed to the guarantee accepting party, the confirming party shall perform the obligation in lieu of the confirmed party;

15. "Joint guarantee" is a guarantee jointly provided by several credit institutions for an obligation of a customer through a co-ordinating credit institution.

Article 3. Credit institutions providing guarantees

1. State-owned commercial banks, joint-stock commercial banks, investment banks, development banks, policy banks, joint-venture banks, foreign banks branches in Vietnam, cooperative banks, other form of banks and non-bank credit institutions which are established and operate in accordance with the Law on credit institutions (hereinafter referred to as credit institutions) shall be entitled to provide bank guarantees in compliance with applicable provisions of related laws and provisions of this Regulation.

2. Banks which are permitted by the Governor of the State Bank to provide international payment service shall be entitled to provide borrowing guarantees, payment guarantees and other forms of guarantee where guarantee accepting parties are foreign organizations, individuals.

3. Credit institutions shall provide guarantees for bill of exchanges, promissory notes in accordance with applicable laws on commercial paper and this Regulation.

Article 4. Customers guaranteed by credit institutions

1. Enterprises which are legally operating in Vietnam.

a. State-owned enterprises;

b. Joint-stock companies;

c. Limited companies;

d. Partnership companies;

e. Enterprises of political organizations, socio-political organizations;

g. Joint-venture enterprises;

h. Enterprises with 100% foreign invested capital;

i. Private enterprises, individual business household.

2. Credit institutions, which are established and operating in accordance with the Law on credit institutions.

3. Cooperatives and other organizations, which satisfy conditions, provided for in Article 94 of the Civil Code.

4. Foreign economic organizations to Business Cooperation Contracts and participating in the bidding for investment projects in Vietnam or where they borrow funds from abroad for the implementation of investment projects in Vietnam.

Article 5. Types of guarantee

1. Borrowing guarantee

a. Guarantee for domestic borrowing;

b. Guarantee for borrowing abroad.

2. Payment guarantee;

3. Bid guarantee;

4. Performance guarantee;

5. Product quality guarantee;

6. Repayment guarantee;

7. Other type of guarantee.

Article 6. Forms of guarantee issuance

1. Issuance of a guarantee letter, guarantee confirmation;

2. Guarantee by signature on the a bill of exchange, promissory note;

3. Other forms as provided for by applicable laws.

Chapter II

DETAILED PROVISIONS

Article 7. Scope of guarantee

1. Guarantee obligations shall include one, several or all of following obligations:

a. Obligation to repay the principal, interests and other fees relating to the loan;

b. Obligation to pay the expenses of the acquisition of material, goods, machinery, equipment and other expenditures for customers to carry out the projects or proposals of production, business, living standard improvement, development investment.

c. Obligation to pay tax, other financial obligations to the State;

d. Obligation of customers when they participate in the bidding, performance of contracts in accordance with applicable laws.

dd. Other lawful obligations agreed between parties in related contracts.

2. Total outstanding guarantee obligations assumed by a credit institution for a single customer shall not exceed 15% (fifteen percentage) of its own capital. Where the performance of the payment by a credit institution in lieu of customers results in the total outstanding credit and the credit arising from that payment exceeding 15% of the own capital of the credit institution, that credit institution must stop immediately new lending and guarantee to that customer and recover the debt in order to ensure that the total outstanding credit to a single customer is in compliance with applicable provision.

For customers who require a guarantee in excess of 15% of the own capital of a credit institution, the credit institution shall, together with other credit institutions, provide the guarantee in accordance with the provision of Article 14 of this Regulation.

3. Total outstanding guarantee obligations of a foreign bank branch to a single customer shall not exceed 15% the own capital of the foreign bank.

4. Credit institutions shall determine their total guarantee obligations in line with their financial capability and ensure their compliance with current provisions of the State Bank on the prudential ratios in the activities of credit institutions.

Article 8. Conditions for the provision of a guarantee

Credit institutions shall consider and decide on the provision of a guarantee upon the satisfaction by customers of following conditions:

1. Having full legal capacity for civil relations, civil act capacity in accordance with applicable laws;

2. Having the creditability in respect of credit, payment relations with credit institutions;

3. Availability of lawful security for the obligation to be guaranteed in accordance with the provision of Article 19 of this Regulation;

4. Availability of an feasible, effective investment project or a feasible, effective business plan in the event of a request for a borrowing guarantee.

5. Satisfaction of conditions provided for by applicable laws on bill of exchange, in the event of the guarantee of a bill of exchange, promissory note

6. Compliance with provisions of applicable laws on the management of foreign borrowing and repayment in the event of the guarantee for a foreign borrowing;

7. Customers being foreign economic organization permitted to perform investments, business activities or participate in the bidding in Vietnam in accordance with provisions of applicable laws of Vietnam.

Article 9. Application file for guarantee

The application file for a guarantee to be prepared by a customer shall include: an application letter for the guarantee (Form No. 01/BL attached) and other documents relating to the guarantee transaction stipulated by the credit institution.

Article 10. Guarantee contract

1. A guarantee contract shall be agreed upon by the guaranteeing credit institution, the guaranteed customer and other relating parties (if any) shall include following main contents:

a. Name, address of the credit institution and the customer;

b. The guaranteed amount, the term of the guarantee and the guarantee fee;

c. The purpose, scope and subjects of the guarantee;

d. Conditions for the performance of the guarantee obligations;

dd. Form of security for the guarantee obligations, the value of the security assets;

e. Rights and obligations of the parties;

g. Indemnity clause after the credit institution has completed the performance of the guarantee obligation.

h. Settlement of disputes;

i. Transfer of rights and obligations of the parties;

k. Other agreements.

2. The guarantee contract may be amended, supplemented or canceled upon agreement of the related parties.

Article 11. Guarantee commitment

1. A guarantee commitment shall include following main contents:

a. Name, address of the credit institution, guaranteed customer, the guarantee accepting party;

b. The guaranteed amount;

c. The scope, subjects and the effective term of the guarantee;

d. Form and conditions for the performance of the guarantee obligations;

In addition to above-mentioned issues, a guarantee commitment may have other contents such as rights and obligations of the parties; settlement of disputes; transfer of rights and obligations of the parties and others.

2. Where the content of a guarantee provides for the use of documents relating to the guarantee transaction (for example the contract between the customer and the guarantee accepting party, the confirmation by the third party of the customers violation or other documents) as conditions for the performance of the guarantee obligation, the guarantee obligation shall be performed in accordance with above-mentioned conditions.

3. In the event of the guarantee by signature on a bill of exchange, promissory note, the guarantee commitment shall be performed in accordance with applicable provisions of the Ordinance on commercial paper and related guiding documents.

4. A guarantee commitment may be amended, supplemented or canceled upon agreement by the related parties.

Article 12. Use of language

1. Written documents relating to the guarantee transaction shall be made in Vietnamese language;

2. In the event of the participation by a foreign party to the guarantee transaction, documents relating to the guarantee transaction shall be made in two languages: the Vietnamese language and one commonly used foreign language, which is agreed upon by the parties.

Article 13. Application of international treaties and customs to the guarantee transaction upon the participation by a foreign party

1. In the event international treaties on guarantee where the Socialist Republic of Vietnam is a signatory or acceded to contain provisions other than provisions of this Regulation, respective provisions of those treaties shall apply.

2. The parties may agree on the application of international rules, customs on guarantee, if those rules, customs do not conflict with the applicable laws of Vietnam.

Article 14. Joint guarantee by several credit institutions for an obligation of customer

1. Co-guarantee

a. The co-ordinating credit institution shall issue the guarantee to the guarantee accepting party on the basis of an guarantee contract signed by credit institutions participating in the co-guarantee;

b. In the event of the failure of the customer to perform or duly perform the obligation committed to the guarantee accepting party, the co-ordinating credit institution shall be responsible to perform the guarantee obligation. The credit institutions participating to the co-guarantee shall be responsible for the repayment of the amount which is paid by the co-ordinating credit institution in lieu of their respective commitment in the guarantee contract of joint liability signed by credit institutions participating to the co-guarantee.

c. In the event the co-ordinating credit institution fails to perform or fully perform the guarantee obligation to the guarantee accepting party, the guarantee accepting party shall have the right to request any credit institution of those co-guaranteeing credit institutions to perform the guarantee obligation.

2. In the event the obligation of the customer can be divided into several separate, independent obligation components, each credit institution may issue guarantee for those individual obligation components and are not jointly liable. Each credit institution shall be liable for its committed obligation.

Article 15. Credit institutions guarantee for an obligation to be performed by several customers who are jointly liable

Credit institutions shall be entitled to provide a guarantee for an obligation which is to be performed by several customers who are jointly liable under an joint liability contract between them, on the basis of the consideration of the creditability and financial capability of each party to that obligation.

Article 16. Rights and obligations of guaranteeing credit institutions

1. Guaranteeing credit institutions shall have the rights:

a. to request an other credit institution to confirm its guarantee for the customer;

b. to accept or refuse to accept the request for guarantee by customers and counter-guarantee issuing credit institutions within a maximum period of 45 days from the date of the receipt of the complete application file for the guarantee;

c. to request the provision by customers of documents in respect of financial capability as well as the guarantee transaction; reports on the production, business performance; reports on the performance of the contract and obligations relating to the guarantee transaction;

d. to request the pledge of security by customers for the obligation to be guaranteed;

dd. to collect a guarantee fee as agreed upon;

e. to request the customer to repay the guaranteed amount which is paid by the credit institution on its behalf;

g. to debit the customer or the counter-guarantee issuing party the amount paid on its behalf in order to perform the guarantee obligation, if the customer or the counter-guarantee issuing party does not recognize the debt after 15 days since the date of payment by the credit institution;

h. to dispose of the security assets of the customer in accordance with the Decree No. 178/1999/ND-CP dated 29 December, 1999 of the Government and written guidance on the implementation of this Decree;

i. to initiate court suits in accordance with provisions of applicable laws where customers, counter-guaranteeing party violate the guarantee contract;

k. to transfer their rights and obligations to other credit institutions as provided for in Article 3 of this Regulation upon a written acceptance by the guarantee accepting party.

2. Guaranteeing credit institutions shall have the obligation:

a. to perform the guarantee obligation in accordance with the guarantee commitment;

b. to encourage the full and timely performance by the customer of obligation to the guarantee accepting party.

c. to return completely the security assets, if any, and related documents to customers upon their full performance of obligations to guarantee accepting party.

Article 17. Rights and obligations of credit institutions which issue a counter-guarantee

1. Counter-guarantee issuing credit institutions shall have the rights:

a. to request the guaranteeing credit institution to issue a guarantee for their customers;

b. to accept or refuse to accept the request for the issuance of a counter- guarantee by customers;

c. to request the provision by customers of documents in respect of financial capability as well as the guarantee transaction; reports on the production, business performance; reports on the performance of the contract implementation and obligations relating to the guarantee transaction;

d. to request the pledge of security by customers for the obligation to be guaranteed;

dd. to collect a guarantee fee as agreed upon;

e. to request the customer to repay the guaranteed amount which is paid by the credit institution on its behalf;

g. to debit the customer the amount paid on its behalf in order to perform the guarantee obligation, if the customer does not recognize the debt after 15 days since the date of payment by the credit institution;

h. to dispose of the security assets of the customer in accordance with the Decree No. 178/1999/ND-CP dated 29 December, 1999 of the Government and written guidance on the implementation of this Decree;

i. to initiate court suits in accordance with provisions of applicable laws where customers, guaranteeing credit institutions violate the guarantee contract;

k. to transfer their rights and obligations to other credit institutions as provided for in Article 3 of this Regulation upon a written acceptance by the guarantee accepting party.

2. Counter-guaranteeing credit institutions shall have the obligation:

a. to perform the guarantee obligation in accordance with the guarantee commitment;

b. to encourage the full and timely performance by the customer of obligation to the guarantee accepting party and guaranteeing credit institution;

c. to return completely the security assets, if any, and related documents to customers upon their full performance of obligations to guarantee accepting party.

Article 18. Rights and obligations of confirming credit institutions

1. Confirming credit institutions shall have the rights:

a. to accept or refuse to accept the request for the confirmation of a guarantee by customers or guaranteeing credit institutions;

b. to request the provision by customers of documents in respect of financial capability as well as documents relating to the guarantee transaction; reports on the production, business performance; reports on the performance of the contract and obligations relating to the guarantee transaction;

c. to request the pledge of security by customers or guaranteeing credit institutions for the obligation to be guaranteed;

d. to collect a guarantee fee as agreed upon;

dd. to request the customers or guaranteeing credit institutions to repay the guaranteed amount which is paid by the credit institution on their behalf;

e. to debit the customer or the guaranteeing party the amount paid on its behalf in order to perform the guarantee obligation, if the customer or the guaranteeing party does not recognize the debt after 15 days since the date of payment by the credit institution;

g. to dispose of the security assets of the customer or the guaranteeing credit institution in accordance with the Decree No. 178/1999/ND-CP dated 29 December, 1999 of the Government and written guidance on the implementation of this Decree;

h. to initiate court suits in accordance with provisions of applicable laws where customers, guaranteeing credit institutions violate the guarantee contract;

i. to transfer their rights and obligations to other credit institutions as provided for in Article 3 of this Regulation upon a written acceptance by the guarantee accepting party.

2. Confirming credit institutions shall have the obligation:

a. to perform the guarantee obligation in accordance with the guarantee commitment;

b. to encourage the full and timely performance by the customers and guaranteeing credit institutions of obligation to the guarantee accepting party.

c. to return completely the security assets, if any, and related documents to customers or guaranteeing credit institutions upon their full performance of obligations to guarantee accepting party.

Article 19. Rights and obligations of the customer

1. The customer shall have the right:

a. to demand the credit institution to comply with the commitment made to the guarantee accepting party;

b. to demand the credit institution to comply with agreements in the guarantee contract;

c. to initiate a court suit in accordance with provisions of applicable laws if the credit institution violates the guarantee contract;

d. Guaranteed customers may transfer their rights and obligations to other parties which satisfy conditions provided for in Article 8 of this regulation if the transfer is accepted in writing by the guaranteeing party, the guarantee accepting party.

2. The customer shall have the obligation:

a. to provide fully, accurately and truthfully documents, reports relating to the guaranteed transaction upon request by the guaranteeing credit institution or the counter-guarantee issuing credit institutions;

b. to pay the guarantee fee and other related fees in accordance with agreements in the guarantee contract to the confirming credit institution, counter-guarantee issuing credit institution;

c. to recognize the debt and repay to the guaranteeing credit institution or the counter-guarantee issuing credit institution, the confirming credit institution the amount of money which is paid on its behalf to perform the guarantee obligation, including the principal, interest and other expenses directly arising out of the performance of the guarantee obligation;

d. to perform accurately and fully obligations committed to the guarantee accepting party and the guaranteeing credit institution or the counter-guarantee issuing credit institution;

e. to be subject to the control by the guaranteeing credit institution or the counter-guarantee issuing credit institution in respect of activities relating to the guaranteed transaction.

Article 20. Authority to sign the guarantee

1. The legal representative of a credit institution shall be competent to sign written guarantee documents of the credit institution;

2. The legal representative of a credit institution may authorize General Director or Director (in the event the Chairman of the Board of Directors is the legal representative), the Deputy General Director or the Deputy Director, General Manager of a Branch of the credit institution to sign the guarantee documents; or provide for the authorization to sign the guarantee of the credit institution in accordance with applicable laws.

Article 21. Security for a guarantee

1. Credit institutions and their customers shall agree on whether or not to apply security measures for the guarantee taking into consideration of characteristics of the production, business performance, financial capability and the creditability of customers. Forms of security for a guarantee shall include: deposit, mortgage, pledge of asset, guarantee of a third party and other forms of security in accordance with applicable laws;

2. The use of assets to be created from the loan funds to secure the performance of the guarantee obligation (for borrowing guarantee) or the exemption of the application of asset security for the performance of guarantee obligation shall be carried out in compliance with the Decree No. 178/1999/ND-CP dated 29 December, 1999 of the Government on the loan security for credit institutions and written documents guiding the implementation of this Decree..

Article 22. Guarantee fee

1. Customers shall pay a guarantee fee to credit institutions. The level of fee shall be agreed by the parties, but not in excess of 2%/annum calculated on the outstanding guarantee obligation. In the event the guarantee fee calculated at this percentage is lower than VND 300,000, credit institutions shall be entitled to charge the minimum guarantee fee of VND 300,000. In addition, customers must pay to credit institution other reasonable fees arising from the guaranteed transactions if and when agreed upon by the parties.

2. The fee level provided for in paragraph 1 this Article shall be the maximum fee level that customers have to pay to credit institutions in the event of a counter-guarantee and guarantee confirmation. The specific level of each credit institution shall be agreed upon by guaranteeing credit institutions.

3. In the event of a co-guarantee, customers shall pay the guarantee fee to the co-ordinating credit institution, which is paid then by the co-ordinating credit institution to other credit institutions in proportion with their participation to the guarantee in accordance with paragraph 1 Article 15.

4. In the event a credit institution provides a guarantee for an obligation performed by several organisations, the individual participating parties shall pay the guarantee fee to the credit institution in proportion to their share in the joint obligation respectively;

5. The calculation period for the guarantee fee and the mode of its collection shall be agreed upon by the parties in the guarantee contract;

6. Late payment by customers of the guarantee fee to the credit institutions shall be subject to an overdue interest rate which is not in excess of 150% of the interest rate of the guaranteed loan in the event of a borrowing guarantee, or the short-term borrowing interest rate applicable by the respective credit institution to other late payment of guarantee fee in the event of other forms of guarantee, calculated from the payment date and for the period of the late payment of that fee.

Article 23. Sequence and procedure of the provision of a guarantee

Credit institutions shall provide in detail the sequence, procedures, conditions and competence to issue a guarantee in line with the characteristics of each credit institution and each type of guarantee.

Article 24. Term of a guarantee

1. The term of a guarantee shall be determined on the basis of the term of the performance by customers of the guaranteed obligation to the guarantee accepting party, unless otherwise agreed or committed;

2. The extension of a guarantee must be accepted by the guarantee accepting party in writing.

Article 25. Sequence of the performance of a guarantee obligation

1. Credit institutions shall perform the guarantee obligation to the guarantee accepting party upon the satisfaction of following conditions:

a. The guarantee obligation has become due;

b. The guarantee accepting party has requested in writing the performance of the guarantee obligation by credit institutions;

c. Availability of documents evidencing the failure by customers to perform or fully perform the committed obligation to the guarantee accepting party, in the event the guarantee commitment provides these availability of those documents as a pre-condition for the performance of the guarantee obligation.

Credit institutions shall perform the guarantee obligation, if documents are in compliance with the guarantee commitment.

2. Credit institutions shall, after the performance of the guarantee obligation, request the redemption by the customers in following steps:

a. In the event of a conventional guarantee

- Guaranteeing credit institutions give notice to customers, together with related documents, to request the customers to repay the amount paid by credit institutions on their behalf;

- Upon the receipt of the notice from credit institutions, customers are obliged to repay the debt or give a written recognition to credit institutions of the amount paid by credit institutions on their behalf. After 15 days from the date of receipt of the notice, if the customers do not repay or do not give the written recognition, credit institutions shall debit the customers (the entry date is the day where credit institutions perform the guarantee obligation). Customers shall be subject to an overdue interest rate agreed upon by the parties, but not in excess of 150% of the interest rate in the contract between the customers and the guarantee accepting party (in the event of a borrowing guarantee) or a short-term lending interest rate applicable by respective credit institutions, calculated from the date where credit institutions perform the guarantee obligation.

- In the event customers do not yet perform duly their obligation to the guarantee accepting party due to objective reasons such as natural calamities, fire, temporarily financial difficulties or due to the mismatch between the repayment period and the business circle. Credit institutions may, on the basis of recommendation made by customers in their written recognition of debt, consider to re-determine the periods of payment and apply the conventional lending interest rate to the amount paid by credit institutions in lieu of customers.

- Guaranteeing credit institutions shall reserve the right to apply measures such as assets sale, deduction of customers accounts( if agreed upon), initiation of court suit and other measures of asset disposal in accordance with provisions of the Decree No, 178/1999/ND-CP dated 29 December, 1999 of the Government and documents guiding the implementation of this Decree in order to recover the amount paid in lieu of customers.

b. In the event of a counter guarantee

After the performance of the counter-guarantee obligation, the counter-guarantee issuing party shall have the right to request the repayment by customers of the amount the counter-guarantee issuing party has paid to the guaranteeing credit institution. The sequence of the repayment of the debt or the recognition of the debt between the counter-guarantee issuing party and customers shall be carried out in a similar manner as provided for in paragraph 1.a of this Article.

c. In the event of the confirmation of a guarantee

After the performance of the guarantee obligation in lieu of the confirmed party, the guarantee confirming party shall have the right to request the repayment by the confirmed party of the amount it has paid to the guarantee accepting party. The sequence of the repayment of the debt or the recognition of the debt between the confirmed party and the confirming party shall be carried out in a similar manner as provided for in paragraph 1.a of this Article.

d. In the event credit institutions provide guarantee for an obligation to be performed by several customers, participating parties shall be responsible for the repayment or the recognition of the debt in proportion to their individual obligation components in the joint obligation. If one of the participating parties fails to perform its obligation component, the credit institutions shall have the right to request any party of the participating parties to perform that obligation component. The sequence of the repayment of the debt or the recognition of the debt by participating parties toward credit institutions shall be carried out in accordance with paragraph 2.a of this Article.

3. In the event of guarantee for a bill of exchange, promissory note, the performance of the guarantee obligation and the request for the redemption shall be carried out in accordance with provisions of applicable laws on bill of exchange.

Article 26. Exemption of the performance of the guarantee obligation

1. In the event the guarantee accepting party exempts the credit institution from the performance of the guarantee obligation, customers still must perform the obligation to the guarantee accepting party, unless otherwise agreed upon or applicable laws provides that the credit institution must perform the guarantee obligation;

2. In the event only one of several co-guaranteeing credit institutions is exempted from the performance of its obligation, other credit institution still must perform their respective obligations and are not required to be responsible for the repayment of the obligation component of the exempted credit institution.

Article 27. The guarantee obligation shall terminate in following cases:

1. The guarantee obligation has been fulfilled by credit institutions;

2. The guarantee obligation terminates in accordance with applicable laws;

3. The guaranteed party has fully performed its obligations to the guarantee accepting party;

4. The guarantee accepting party agrees to cancel the guarantee in accordance with applicable laws;

5. The guarantee is replaced by another security measures in accordance with agreements of the parties;

6. The term of the guarantee has expired in the event the guarantee has stipulated for the effective term of the guarantee;

7. In the event of the termination of activities of a credit institution, the guarantee obligation shall be performed in accordance with provisions of related laws.

Chapter III

REGIME ON THE CONTROL AND INFORMATION, REPORTING

Article 28. Regime on the control, supervision of the guarantee

1. Customers shall be subject to the control, supervision by the guaranteeing credit institution during the effective term of the guarantee;

2. Credit institutions shall be subject to the inspection, control by the State Bank in accordance with current provisions.

Article 29. Accounting regime and information, reporting

1. The accounting and monitor of guarantees provided by credit institutions shall be carried out in accordance with current provisions;

2. Customers shall be responsible to submit periodical or irregular reports to credit institutions on the performance of activities relating to guaranteed transactions;

3. Credit institutions shall consolidate the guarantee activities of their institutions to report to the State Bank in accordance with the current information and reporting regime.

Chapter IV

IMPLEMENTING PROVISIONS

Article 30. Credit institutions and customers shall be responsible for the implementation of this Regulation. Based on this regulation and provisions of related legal documents, credit institutions shall issue written operational guidelines in line with their conditions, characteristics and Charter.

Article 31. The supplement, amendment of this Regulation shall be decided upon by the Governor of the State Bank.

|

|

THE

GOVERNOR OF THE STATE BANK |