Nội dung toàn văn Circular No. 18/2009/TT-BTC of January 30, 2009, guiding implementation of fifty per cent reduction of value added tax rate in accordance with the list of goods on the preferential import tariff list.

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

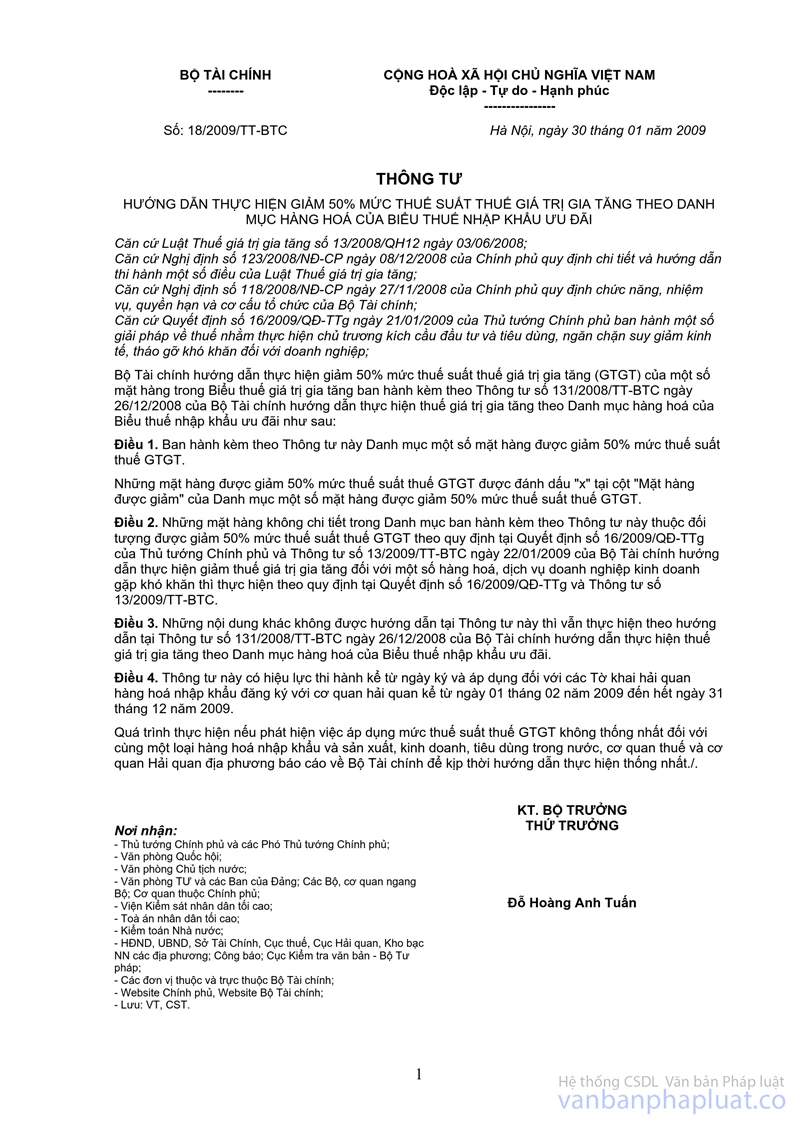

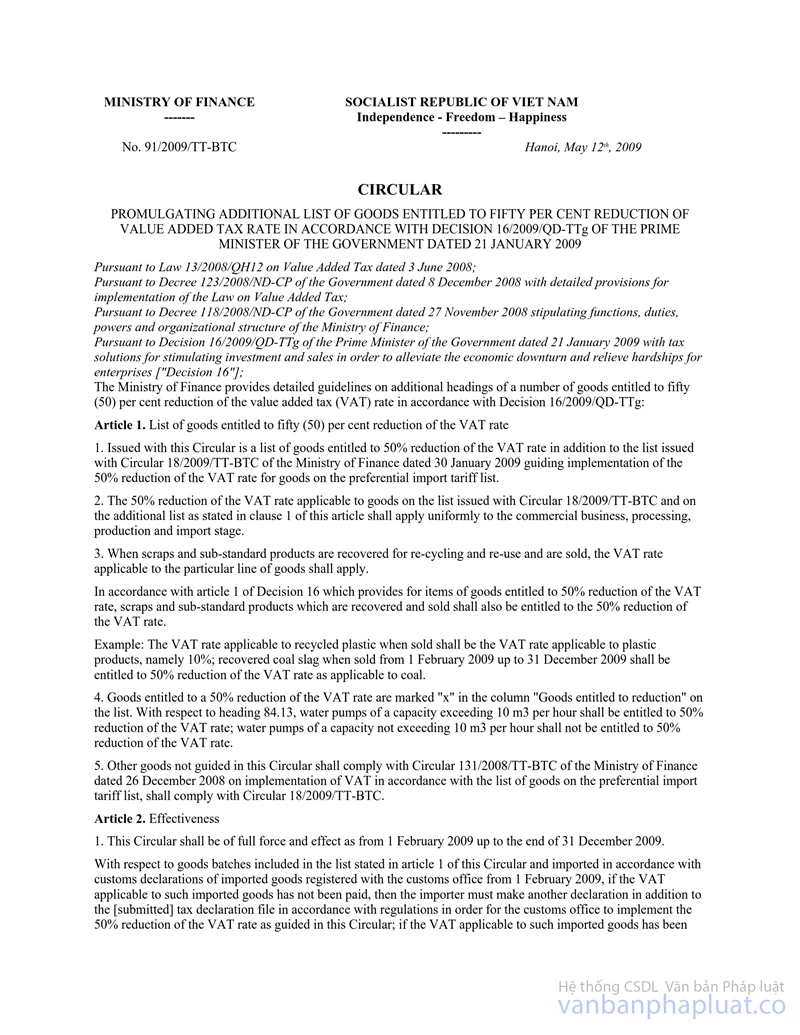

No. 18/2009/TT-BTC |

Hanoi, January 30, 2009 |

CIRCULAR

GUIDING IMPLEMENTATION OF FIFTY PER CENT REDUCTION OF VALUE ADDED TAX RATE IN ACCORDANCE WITH THE LIST OF GOODS ON THE PREFERENTIAL IMPORT TARIFF LIST

Pursuant to Law 13/2008/QH12 on Value Added Tax dated 3 June 2008;

Pursuant to Decree 123/2008/ND-CP of the Government dated 8 December 2008 on

implementation of the Law

on Value Added Tax;

Pursuant to Decree 118/2008/ND-CP of the

Government dated 27 November 2008 on functions, duties, powers and

organizational structure of the Ministry of Finance;

Pursuant to Decision 16/2009/QD-TTg of the Prime Minister of the Government

dated 21 January 2009 issuing tax solutions for implementing the policy on

stimulating investment and sales in order to alleviate the economic downturn

and relieve hardship for enterprises ["Decision 76"];

The Ministry of Finance hereby provides guidelines for implementation of the reduction of fifty (50) per cent VAT rates applicable to a number of goods on the value added tariff list issued with Circular 131/2008/TT-BTC of the Ministry of Finance dated 26 December 2008 guiding implementation of VAT in accordance with the list of goods on the preferential import tariff list, as follows:

Article 1

To issue with this Circular the list of a number of goods entitled to a 50% reduction of VAT rates.

Goods entitled to a 50% reduction of VAT rates are marked V in the column "Goods entitled to reduction" on the list of the goods entitled to a 50% reduction of VAT rates.

Article 2

The provisions of Decision 16 and Circular 13/2009/TT-BTC of the Ministry of Finance dated 22 January 2009 on reduction of VAT for a number of goods and services in which enterprises are meeting difficulties, shall apply to goods not detailed in the list issued with this Circular and which fall into the category of goods entitled to a 50% reduction of VAT pursuant to Decision 16 and Circular 13.

Article 3

Other goods not guided in this Circular shall comply with Circular 131/2008/TT-BTC of the Ministry of Finance dated 26 December 2008 on implementation of VAT in accordance with the list of goods on the preferential import tariff list

Article 4

This Circular shall be of full force and effect from the date of its signing and shall apply to import goods1 customs declarations registered with the customs office as from 1 February 2009 up to the end of 31 December 2009,

If during implementation any inconsistency is detected between application of VAT rates to the same kind of import goods and goods for domestic production, business and sales, then the tax office and the customs office shall report to the Ministry of Finance for timely guidelines and uniform implementation .

|

|

FOR THE

MINISTER OF FINANCE |

|

FILE ATTACHED

|