Nội dung toàn văn Circular 91/2016/TT-BTC guidelines estimation state budget 2017

|

MINISTRY OF

FINANCE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 91/2016/TT-BTC |

Hanoi, June 24, 2016 |

CIRCULAR

ON GUIDELINES FOR THE ESTIMATION OF THE STATE BUDGET IN 2017

Pursuant to the State Budget Law No. 83/2015/QH13 dated June 25, 2015;

Pursuant to the Government’s Decree No. 215/2013/ND-CP dated December 23, 2013 on the functions, missions, authority and organizational structure of the Ministry of Finance;

At the request of the Head of the Department of State Budget;

Minister of Finance promulgates the Circular on guidelines for the estimation of the state budget in 2017.

Chapter I

THE EVALUATION OF THE IMPLEMENTATION OF MISSIONS FOR THE STATE BUDGET IN 2016

Article 1. Grounds for the evaluation of the implementation of missions for the state budget in 2016

Ministries, central and local authorities shall base on the following grounds to evaluate the state budget revenue and expenditure in 2016:

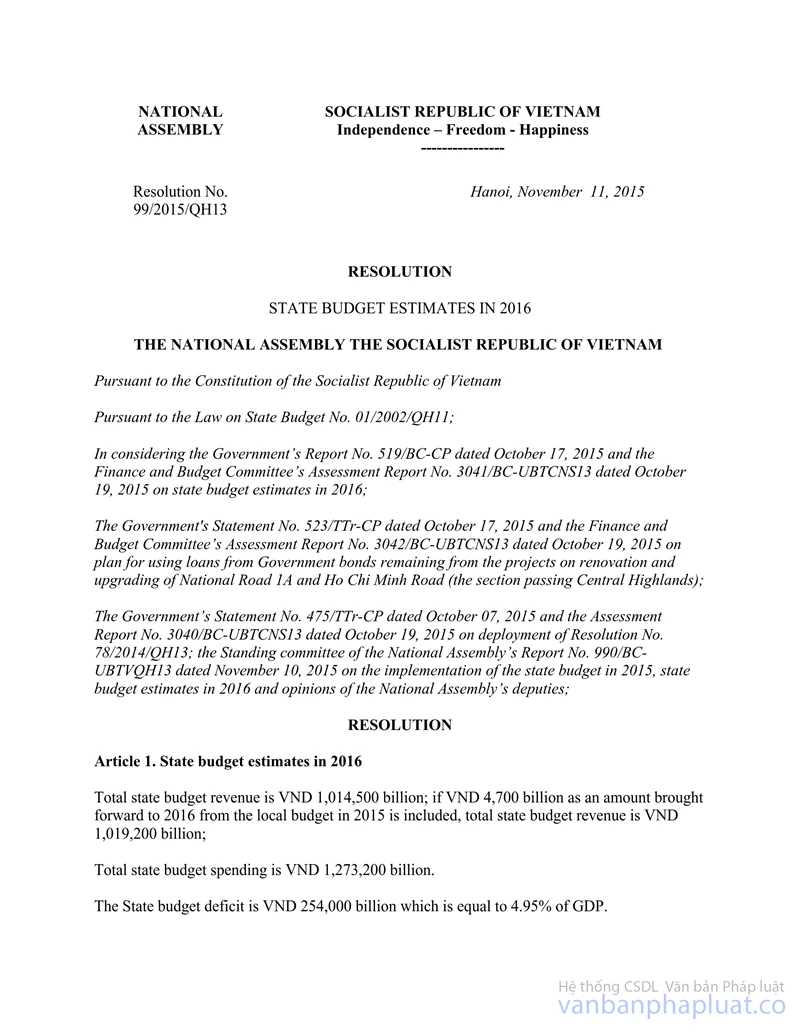

1. The missions for the 2016’s state budget as passed by the 13th National Assembly via the Resolution No. 99/2015/QH13 dated November 11, 2015 on the estimation of the 2016's state budget and via the Resolution No. 101/2015/QH13 dated November 14, 2015 on the allocation of the central budget in 2016; and defined by the Prime Minister via the Decision No. 2100/QD-TTg and Decision No. 2101/QD-TTg dated November 28, 2015 on assignments for the estimation of the 2016’s state budget, the Decision No. 2526/QD-TTg dated December 31, 2015 on assignments for the planning of development investment finances from the 2016’s state budget and other decisions on budget replenishment during the operation of the 2016’s state budget.

2. Written instructions by the Government and Prime Minister, including: Resolution No. 01/NQ-CP dated January 07, 2016 on missions and primary solutions for directing and managing the implementation of the economic - social development plan and the estimation of the state budget in 2016 (Resolution No. 01/NQ-CP); resolutions passed in the Government's monthly scheduled meetings; the Directive No. 22/CT-TTg dated June 03, 2016 on expediting the direction and management of the implementation of missions of finance and state budget in 2016 (Directive No, 22/CT-TTg).

3. Circular No. 206/2015/TT-BTC dated December 24, 2015 by the Ministry of Finance on organizing the estimation of the 2016’s state budget.

4. The advancement of the missions of finance and state budget in the first 6 months; solutions as approved by competent authorities for accomplishing the 2016’s state budget estimate beyond expectation.

5. Conclusions and propositions by specialized agencies for administrative formality reform, inspection, audit, settlement of complaints and denunciations, thrift and corruption eradication with regard to the collection of revenues and disbursement of finances from the state budget; tightening of financial discipline and regulations, prevention of losses of budget revenues, prevention of transfer pricing, reclaiming of tax debts, reduction of outstanding tax debts; outcome of social security policies, benefits for meritorious individuals, financially challenged households, ethnic minority communities, residents in remote areas; sustainment of expenditure for national defense and security, political stability and social order.

Article 2. Evaluation of the collection of state budget revenues

Forecast the circumstances of production and business and fluctuations in market prices in the last 6 months, review and assess influential factors and propose operational solutions to accomplish the collection of the 2016’s state budget revenues beyond expectations according to the approval of the National Assembly and People’s councils at various levels, on the basis of the state budget revenues collected in the first 6 months, with primary attention to:

1. The evaluation and analsysi of each factor that affects the 2016’s state budget revenues, including:

a) Advantages and obstacles to the activities of production, trading, import and export of enterprises and business organizations in various economic sectors under the influence of domestic and foreign elements; production output and consumption, selling prices and gains of dominant goods and services;

b) Pace of growth of total retail sale of goods and of earnings from consumer services;

c) Pace of surge in values of industrial production;

d) Increase and decrease in investments among types of business ownership;

dd) Enterprises’ access to loan capital and capacities for new investment projects, expansion projects and in-depth investments; circumstances of the real estate market.

Dissect the impacts of fluctuations in the pricing of crude oil and farm produce, the effects of drought, saltwater intrusion and marine environment issues in certain provinces along the North Central coast, the fulfillment of international economic integration commitments, the implementation of the Government’s Decree No. 19-2016/NQ-CP dated April 28, 2016 on primary missions and solutions for augmenting the business environment and national competitiveness in 2016 and 2017, with a vision towards 2020, the implementation of policies on currency, credit, commerce, investment, pricing and administrative formality reform, the implementation of the Decree No. 36a/NQ-CP dated October 14, 2015 on e-government, other factors' influence on the economy, and the state budget revenues collected in the first 6 months, in order to establish grounds for evaluating the state budget revenues collected in the last 6 months of 2016.

2. Assess the implementation and accomplishment of measures for the management of state budget revenues according to the Decree No. 01/NQ-CP and Directive No. 22/CT-TTg; the implementation of tax policies, including the alleviation of corporate income tax rate, as amended and effected in 2016; the implementation of the Law No. 106/2016/QH13 on amendments to certain articles of the Law on value added tax (VAT), Law on special consumption tax (SCT) and Tax Administration Law; the implementation of the Decree No. 1084/2015/UBTVQH13 on amendments to the schedule of natural resource tax rates; the implementation of the Circular No. 195/2015/TT-BTC dated November 24, 2015 by the Ministry of Finance on revision to the SCT-included pricing of imports and domestically produced goods incurring the SCT; the implementation of the Circular No. 61/2016/TT-BTC dated April 11, 2016 by the Ministry of Finance on guidelines for the collection, payment and management of profits and dividends from state-owned investments in enterprises; the implementation of the Circular No. 36/2016/TT-BTC dated February 26, 2016 by the Ministry of Finance on taxes levied on organizations and individuals engaging in the exploration and drilling of oil and gas, and the implementation of other documents, policies and regulations on taxes and fees in connection with the collection of revenues in 2016.

3. Evaluate the settlement and reclaiming of outstanding tax debts

The result of the expedited and coerced reclaiming of outstanding tax debts in 2016; the implementation of propositions by the State Audit Office and Government Inspectorate, decisions by tax authorities for reclaiming of tax arrears in connection with the implementation of plans and missions for inspecting the compliance with tax laws.

Ascertain tax debts that remain outstanding until December 31, 2015, anticipate tax debts ensuing, written off and reclaimed in 2016 and total debts recorded until December 31, 2016. Moreover, outstanding tax debts shall be summarized and classified fully and precisely as per regulations.

4. Evaluate companies’ tax declaration, VAT refund thereof and amounts to be refunded to companies in 2016, as well as strengthen the activities of supervision and inspection following VAT refunds and the settlement of VATs refunded against regulations. Particularly, the effects of details on VAT reduction and refund in the Law No. 106/2016/QH13 on amendments to certain articles of the laws on VAT, SCT and tax administration on the amount of VAT refunded in 2016 and state budget revenues shall be assessed. Make recommendations to revise the regulations on the stringent management of VAT refunds in conformity to the laws.

5. Verify the result of the coordination of ministries, central bodies and local authorities in the administration and eradication of difficulties and obstacles against the collection of state budget revenues, auction sale of state-owned assets, auction sale of land use rights. Moreover, relevant agencies shall inspect tax debts and expedite the claiming of such debts, forestall losses and transfer pricing, detect and solve hindrances.

6. Verify the result of the collection of fees, administrative fines and other forfeits in the first 6 months and in the entire year of 2016.

Article 3. Evaluation of the disbursement of finances for investment and development

Ministries, central bodies and local authorities shall aim attention at assessing the following matters:

1. The allocation and estimation of finances for investment and development in 2016

a) The formulation and verification of proposals and decisions on investments into public-funded projects and revising such projects (if possible) in conformity to the Law on public investment and written instructions by the Government and Prime Minister.

b) The apportionment and assignment of finances estimated for investment and development in 2016; i.e. the allocation and assignment of finances for investment and development of projects and buildings in 2016 according to the Law on public investment; the duration for allocating finances and assigning plans to project investors; the result of the arrangement of estimates for recovering advances from the state budget and settling payments for infrastructure development under the state budget.

c) The disbursement of finances for investment and development in 2016; the implementation of investment and development plans in 2016, i.e. the workload performed and funds disbursed until the end of the 2nd quarter of 2016 (including the workloads finished and advances), the anticipation of remaining workloads and spending required until December 31, 2016 (provide detailed schedules for each project, data on total investments approved, funds disbursed until the end of 2015, finances planned for 2016 and explanations).

The progress of vital programs and projects, national target programs, projects that utilize ODA and concessional loans (e.g. disbursement and capacity of counterpart financing). Determine the possibility of disbursement of funds in excess of those estimated and assigned (if applicable) for projects and programs utilizing ODA and concessional loans as apportioned from the state budget and report such possibility to the Ministry of Planning and Investment and the Ministry of Finance, which in turn summarize and present data to the Prime Minister who makes a report thereof to the Standing Committee of the National Assembly for approval.

d) Summarize and evaluate the undisbursed investments from the state budget into infrastructure development according to the Prime Minister’s written instructions (e.g. Directive No. 27/CT-TTg dated October 10, 2012, Directive No. 14/CT-TTg dated June 28, 2013 and Directive No. 07/CT-TTg dated April 30, 2015): amounts undisbursed until December 31, 2015, settled in 2016 and undisbursed until December 31, 2016 (enumerate and specify undisbursed amounts for each project).

dd) Advances that the state budget has furnished, without sources available for recouping such advances, to investment projects until June 30, 2016.

e) The mobilization and recouping of funds, repayment of debts (including advances from unused funds of the State Treasury) for infrastructure investment projects and programs.

g) The finalization of accounting records of investment projects completed, which specifies the information on: the quantity of finished projects, whose accounting data has not been finalized, in late June 2016 and at the end of 2016; reasons and solutions.

h) Evaluate obstacles against the management of investments according to the Law on public investment, the Law on construction and relevant legislative documents; and propose solutions.

2. Assess the achievements in spending on development assistance.

a) The deployment of the Government’s preferential investment credits (e.g. total level of credit growth, sources of funding for implementing credit growth plans, subsidies from the state budget on interest rate differences, etc.); beneficiaries and scope of incentives; entities implementing credit policies; loan interest (e.g. justification of such rates, interest rate, preferential interest rate policies in case of fluctuations in market interest rates); reform of administrative formalities for processing loan applications.

b) The granting of credits to households that live in or near poverty or have recently escaped poverty, to ethnic minority households that are financially distressed, to students, to job seekers and to overseas workers; the granting of loans to programs for clean water and rural sanitation, etc. Each program that receives such loan(s) must be clearly identified with regard to the scope and conditions of the loan, borrowers, performance, outstanding debt, interest rate and amounts spent on covering differences in interest rate, etc.

c) The implementation of the 2016’s national reserve plan, with regard to: purchase, sale, import, export, replacement and distribution of the inventory in national reserve (e.g. details on the type, quantity and value of items). Specify the quantity and type of purchases, for supplementing or compensating the national reserve, being auctioned, contracted and warehoused according to the plan until the time of reporting.

Article 4. Evaluation of the disbursement of regular spending

1. The allocation, assignment and actualization of estimates of the state budget in the first 6 months and in the entire year of 2016 by sector; the accomplishment of major objectives, missions, programs and projects; difficulties, obstacles and solutions.

2. The cessation and recouping of regular spending, which have been assigned in estimates of ministries, central bodies and local authorities at the start of the year but have not been allocated, and of those that have been allocated but have not been utilized, have not been endorsed with regard to the estimates or have not initiated any auctions for additional provisions according to the Government’s Resolution No. 01/NQ-CP and the Prime Minister's Directive No. 22/CT-TTg until June 30, 2016.

3. The result of the implementation of missions, regulations, policies and regimes on spending, difficulties and obstacles thereof, and solutions in 2016, as follows:

a) For regimes and policies: Assess, in general, all policies and regimes; scrutinize and propose revisions to policies and regimes unfit for practical circumstances.

b) The progress and result of the self-management of and self-accountability for permanent tenure and administrative expenditure according to the Government’s Decree No. 130/2005/ND-CP dated October 17, 2005 and its amendments as defined in the Decree No. 117/2013/ND-CP dated October 07, 2013.

c) The implementation, in the first 6 months and the entire year of 2016, of the missions defined in the Prime Minister's Decision No. 695/QD-TTg dated May 21, 2015 on the scheme for implementing the Government’s Decree No. 16/2015/ND-CP dated February 14, 2015 on the mechanism of self management of public service agencies (Decree No. 16/2015/ND-CP); the progress of self-management of public service agencies by sector (e.g. education, health care, science and technology, etc.): Self-managed agencies by type; schemes for the adjustment of public services' fees; effects on the state budget (e.g. public service agencies' proceeds and their additional aids from the state budget - if available).

d) The evaluation of the state budget expenditure for sectors shall focus on:

Education, training and vocational instruction: Evaluate the application of preferential policies for education, training and vocational instruction and the adjustment of tuitions in 2016 according to the Government’s Decree No. 86/2015/ND-CP Ministries and central bodies shall provide instructions to public tertiary education institutions, which were approved by the Prime Minister to conduct the pilot project on new operational mechanism via the Government’s Decree No, 77/NQ-CP dated October 24, 2014 on the assessment of the progress and result of the project towards the end of 2016. Responsibilities of tertiary education institutions for fulfilling commitments, responsibilities of ministries, agencies and provincial people’s committees for inspecting, supervising, guiding and supporting tertiary education institutions' piloting the project.

Health care: Evaluate the application of preferential policies for the sector of health care; the pricing of insured health care and effects thereof according to the Joint Circular No. 37/2015/TTLT-BYT-BTC by the Ministry of Health and Ministry of Finance; the classification of public service agencies’ self-management.

Evaluate the implementation of the project for easing hospitals’ overload via the Prime Minister’s Decision No. 92/QD-TTg dated January 09, 2013. Evaluate the arrangement of resources for hygiene assurance as per regulations.

- National reserve:

Evaluate the estimation of spending on purchase, discharge, storage, insurance, etc. of articles in national reserve in the first 6 months and the entire year of 2016; the implementation of the plans for purchasing rice apportioned to full-day students and afforestation according to the Prime Minister’s decisions.

4. Evaluate the application of regulations and policies for mobilizing private sector’s engagement (e.g. sum and structure of private entities’ resources for the development of industries; quantity of infrastructures that receive investments from private entities; achievements; obstacles, reasons and solutions).

Article 5. Evaluation of the implementation of national target programs and target programs

1. Ministries shall report the progress of national target programs (NTPs) and target programs (TPs) in 2016 to 2020, which they advocate, to the Prime Minister for approval.

2. Local authorities shall evaluate the allocation, assignment and estimation of spending on NTPs and TPs; advantages, difficulties and obstacles (if any) thereof.

3. Evaluate the disbursement of foreign finances into TPs that are additionally funded by foreign entities, financial mechanisms and recommendations (if any).

4. The ability to balance the local state budget and mobilize private resources for local NTPs and TPs. Investigate reasons and liabilities of relevant agencies if resources mobilized are lower than expected.

Article 6. Evaluation of the assurance of finances for the adjustment of statutory pay rate in 2016

Make reports on permanent tenure, payroll fund, allowances and benefits; determine the need and source of finances for salary reform according to the Government’s Decree No. 47/2016/ND-CP dated May 26, 2016 on statutory pay rate for public officials, public employees and armed forces’ personnel.

Provinces and centrally affiliated cities shall supplement their reports on payroll fund, allowances and benefits granted in 2014 (according to the figures finalized), granted in 2015 and expected in 2016. Furthermore, reports on the demand for additional expenditure to increase the 2015’s statutory pay rate to VND 1,150,000 per month and on the demand expected for 2016 shall be required according to the form no 16, 17, 18 and 19 of this Circular.

Article 7. Evaluation of the implementation of the 2016’s state budget missions in provinces and centrally affiliated cities

Apart from general requirements stated above, provinces and centrally affiliated cities shall mainly assess the following contents:

1. The mobilization of local financial resources for the implementation of local socio-economic development missions.

2. The ability to balance the local budget according to the estimate, past and future measures for balancing the local budget under the circumstance that the local budget revenues hardly match the estimate defined in the Directive No. 22/CT-TTg as follows: increase in revenue collected, reduction of spending, utilization of local financial resources (50% of the local budget provisions, finances for salary reform, the 2015's budget in surplus, financial reserve fund, etc.). Quantify each resource and amount in use and in surplus (if any).

3. The implementation of social security policies:

3.1. Regular policies included in the 2016’s estimate:

The social protection policy defined in the Government’s Decree No. 136/2013/ND-CP dated October 21, 2013, the Law on the Elderly and the Law on persons with disabilities; the policy on lunch subsidy for children of 3 to 5 years of age according to the Prime Minister's Decision No. 239/QD-TTg dated February 09, 2010 and Decision No. 60/2011/QD-TTg dated October 26, 2011; the policy on supports for ethnic minority students in boarding schools according to the Prime Minister's Decision No. 82/2006/QD-TTg dated April 14, 2016; the policy on supports for day students according to the Prime Minister Decision No. 85/2010/QD-TTg dated December 21, 2010; the policy on supports for high school students in severely disadvantaged areas according to the Prime Minister’s Decision No. 12/2013/QD-TTg dated January 24, 2013; the policy on reduction and exemption of tuition and educational expenses for students who live in or near poverty according to the Government's Decree No. 86/2015/ND-CP dated October 02, 2015; the policy on education aids for ethnic minority students according to the Prime Minister's Decision No. 66/2013/QD-TTg dated November 11, 2013; the policy on supports for disabled students who live in or near poverty according to the Joint Circular No. 42/2013/TTLT-BGDDT-BLDTBXH-BTC dated December 31, 2013 by the Ministry of Education and Training, Ministry of Labor - Invalids and Social affairs and Ministry of Finance; the policy on health insurance subscription support for poor people, ethnic minority compatriots, children under 6, individuals living in near poverty, students, members of households that earn average living from agriculture, forestry, aquaculture and salt farming; the policy on electricity bill support for financially disturbed households according to the Prime Minister’s Decision No. 28/2014/QD-TTg dated April 07, 2014; the policy on supports for the protection and development of rice paddies according to the Government’s Decree No. 35/2015/ND-CP dated April 13, 2015 on the management and utilization of rice paddies; the policy on exemption of irrigation fee according to the Government’s Decree No. 67/2012/ND-CP dated September 10, 2012; etc. (A report on each policy must specify beneficiaries and expenditure in need according to the form no 13 of this Circular).

3.2. Other local policies:

The policy on benefits for individuals having engaged in national defense wars or in international missions; the policy on residence supports for contributors to the revolution; the policy on supports for households living in or near poverty, people of ethnic minority communities or in severely disadvantaged areas (e.g. the fast and sustainable poverty eradication program for meager districts according to the Government's Resolution No. 30a/2008/NQ-CP dated December 27, 2008; supports regarding productive and residential land, housing and domestic water for poverty-stricken ethnic minority households, etc.); rice aid for students in severely disadvantaged areas according to the Prime Minister's Decision No. 36/2013/QD-TTg dated June 18, 2013; the policy on supports for young intellectuals volunteering to develop rural and mountainous areas in 2013 to 2020 according to the Prime Minister’s Decision No. 1758/QD-TTg dated September 30, 2013; the policy on unemployment insurance; the policy on supports for epidemic prevention, impediment to and recovery from natural disasters, flood and storm, famine rescue; the policy on supports for fishermen troubled pursuing or taking off-shore fishing trips; the policy on preferential rate of loan interest and on subsidy on interest rate differences, which reduce losses upon the harvesting of farm produce or aquatic products; the policy on the development of aquaculture according to the Government’s Decree No. 67/2014/ND-CP dated July 07, 2014, etc.

4. Detailed report on the allocation of the budget (including targeted finances from the central budget to the local budget - if any) and the spending of the local budget provisions on security, national defense, deterrence of and recovery from natural disasters and epidemic on human, cattle, poultry and plants; and the utilization of the local budget provisions until June 30, 2016.

5. The allocation and assignment of spending from land use revenues on local infrastructure projects, cadastral measurement and documentation, certification of land use right, and the establishment of the land development fund from land use revenues and land rent according to the Government’s Decree No. 43/2014/ND-CP dated May 15, 2014.

6. The mobilization of finances into the local budget for investing in infrastructure (including the mobilization and arrangement of finances for repaying principal loan and interest until June 30, 2016), as follows: outstanding debts at the start of the year, estimated amounts mobilized in the year, payables due, loan-derived outstanding debts estimated until December 31, 2016. The loan-derived outstanding debts in the local budget, as defined in Section 3, Article 8 of the Law on state budget, shall include borrowings of the Government's development investment credits for the reinforcement of canals, development of rural routes, and facilities for aquaculture and rural trades (the detailed report on the local budget’s outstanding debts, borrowings and debt repayment shall be subject to the form no 9 of this Circular).

7. The revenue from and spending on the lottery business; the investment of lottery revenues into essential local public buildings, particularly in education, health care and rural agriculture as per regulations.

8. The implementation of the national target program for new rural development: The quantity of communes that accomplish the program and expenses specified by source (e.g. central budget, local budget, government bond, etc.).

9. The implementation of the national target program for poverty reduction: Expenses specified by source (e.g. central budget, local budget, government bond, etc.).

Chapter II

ESTIMATION OF THE STATE BUDGET IN 2017

Article 8. Objectives and requirements

1. Since 2017 the second year of the 5-year socio-economic development plan for 2016 to 2020, the first year to which the 2015's Law on state budget applies and the first year of the state budget stabilization period of 2017 to 2020, the said year is of extreme importance for the implementation of objectives and missions in socio-economic development for the entire period of 2016 to 2020 and targeted financial strategies towards 2020.

2. The estimation of the state budget shall abide by the 2015’s Law on state budget and guiding documents in accordance with the objectives and missions defined in the 5-year socio-economic development plan for 2016 to 2020, which was passed by the National Assembly, and the objectives and missions of socio-economic development in 2017.

3. The estimation of the 2017's state budget revenues and expenditure shall adhere to the laws on the collection, dispensing and management of the budget revenues and in conformity to the principles, norms and rate of estimated regular allocations of the 2017’s state budget and to the principles, norms and rate of investments from the state budget in 2016 to 2020 at the discretion of competent authorities. Be immersed in the policy of thorough thrift and waste prevention upon the process of estimation.

4. Ministries, central bodies and local authorities shall base on their assessments of the implementation of the 2016’s socio-economic development missions, in line with the objectives and missions of socio-economic development in 2017 and from 2016 to 2020 in connection with industries, sectors and localities and the medium-term public investment plan for 2016 to 2020, to determine the core and vital missions in 2017. They shall actively prioritize the 2017’s expenditure by necessity and feasibility in order to accomplish missions, programs and projects, which competent authorities have approved, on the basis of allocations of the state budget and other legitimate finances mobilized.

5. Ministries and central bodies that manage industries and sectors shall continue scrutinizing, abrogating and integrating overlapping, duplicate and inefficient regulations and policies (particularly in connection with social security) intra vires or through competent authorities. They shall only present new policies to competent authorities for promulgation upon balancing resources. Moreover, they shall actively anticipate every expenditure in need for the implementation of new policies, regulations and missions that competent authorities have decided.

6. The estimation of the state budget shall conform to the time limit defined in the 2015's Law on state budget. Legal grounds, calculations and explanations shall be specified.

Article 9. Estimation of the state budget revenues

The estimation of the 2017’s state budget revenues shall adhere to current policies and regulations and record all revenues from taxes, fees and other gains of the state budget according to the 2015's Law on state budget on the basis of the strict evaluation of capacities to collect state budget revenues in 2016 and the anticipation of investments, growth of production and trading, commercial activities, import and export in 2017 with due account for domestic and foreign factors. Moreover, such estimation shall formulate increases and decreases that originate from the application of amended legislative documents on taxation and the reduction of taxes as per international commitments. Furthermore, such estimation shall record increases that result from the intensification of inspections of entities' declaration and payment of taxes, revenues detected through inspections and audits, increases owing to drastic instructions on loss prevention, reclaiming of outstanding tax debts from previous years, and receivables from investment projects whose incentives expire.

The revenues thereof into the 2017's state budget shall be approximately 20 to 21% of the GDP. The average increase in domestic revenues (excluding those from crude oil, land use subscription and lottery business) is estimated to be at least 13 to 15% of that anticipated in 2016 (to the exclusion of fluctuations caused by changes in policies). The average increase in revenues from import and export is estimated to be at least 5 to 7% of that anticipated in 2016. The actual increase in each locality shall be subject to local conditions, characteristics and economic growth pace. The guidance and designation of agencies managing taxpayers shall be governed by separate instructions from the Ministry of Finance.

1. The estimation of domestic revenues

a) When local authorities estimate state budget revenues in their localities in 2017, they must, apart from fulfilling the said objectives and requirements, amass the information on all local sources of revenues (including the revenues collected in communes, wards and towns), particularly taxes paid by foreign and domestic contractors that carry out investment projects.

b) The estimation of the 2017's state budget shall precisely and fully calculate each revenue or tax by sector and by locality in conformity to current regulations on taxes, fees and other earnings not related to the state budget, to new regulations coming into force since 2016 and affecting the 2017's state budget revenues and to amended regulations to be effected in 2017; including: The 2015’s Law on state budget, Law on fees and guiding documents that come into effect in the budgetary year of 2017; the Law on amendments to certain articles of the Law on value added tax, Law on special consumption tax and Law on tax administration; the Resolution No. 1084/2015/UBTVQH by the Standing Committee of the National Assembly on promulgating the schedule of natural resource tax rates; the business license fee (replacing the license tax); the corporate income tax for enterprises using a centralized accounting system and operating in commerce or service, and the environment protection tax on petroleum products domestically manufactured; lottery revenues collected according to legislative documents on the taxation and financial administration of lottery enterprises as defined in the Circular No. 01/2014/TT-BTC dated January 02, 2014 by the Ministry of Finance.

c) Summarize the collection of all fees from the licensing by central bodies and provincial people’s committees of mineral mining; administrative fines, other fines and money confiscated as per the laws and handled by central government agencies and local agencies; earnings from the sale of state-owned properties, including those from the transfer or conversion of lands under the management of government agencies, political organizations, socio-political organizations, public service agencies, single-member limited liability enterprises that are state-owned, or enterprises in which a central or local body holds share prior to the privatization or restructuring of such enterprises, and other central or local organizations.

d) Ministries, industry-based agencies and local authorities must consider sources of revenues in connection with the intensification of solutions on expediting and coercing the reclaiming of taxes, inspections, encountering of transfer pricing, smuggling and trade fraud, inspection and supervision of VAT refunds, stricter supervision, control and prevention of losses on enterprises and businesspeople in the sector of commerce and services as per the instructions by the Government, Prime Minister and Ministry of Finance; revenues collected owing to the expediting of the implementation of propositions of auditing agencies, government inspectorate and function-assigned agencies. Also include are tax arrears reclaimed and to be reclaimed for the state budget.

2. The estimation of revenues from import and export

Revenues from import and export shall be estimated:

a) On the basis of the anticipated pace of the growth of turnover of taxed goods and services imported and exported in the context of integration, greater trade promotion, consolidation and expansion of export markets; the transformation of the structure of goods, particularly traditional ones that produce primary revenues and those that newly ensue.

b) According to these primary factors: domestic and international market prices of goods that produce major revenues; exchange rates between Vietnam Dong and the currencies of strategic trade partners; decrease in revenues due to the imposition of special preferential tax rates or tax rebates amid the reduction of taxes as per free trade agreements signed and to be signed; commercial advantages and technical barriers; scale and progress of focal investment projects for which materials and equipment are imported; and changes in domestic and foreign policies.

3. Fees paid to the budget and retained for later spending as regulations.

a) Pursuant to the Law on fees and the 2015’s Law on state budget, certain fees re-defined as service price, from the budgetary year of 2017, shall not be included in the list of amounts estimated for the state budget; fees are fully contributed to the state budget while charges may be retained partly or fully by public service agencies, which collect such charges, and be deducted for government agencies whose activities are funded by such charges.

Ministries, central bodies and local authorities shall review and report fees and charges, which are against regulations or re-defined as service price, to competent authorities for abrogation or exclusion, respectively, in accordance with the list defined in the Law on fees. Each fee or charge shall be reported in details (i.e. the amounts collected, retained for spending as per regulations, and contributed to the state budget) to support the estimation of the fees and charges collected and of the spending of fees retained.

Tuitions (not included in the list of fees and charges as per the Law on fees) shall not be included in the estimation of the state budget revenues and expenditure in ministries and central bodies from the year of 2017. However, ministries and central bodies shall spend such proceeds and other receipts retained for regulated spending on the reform of salary as per regulations.

b) Receipts for function-based services, which are not included in this list of fees and charges, and receipts re-defined as service pricing shall not be a contribution to the state budget and not be included in the estimate of fees and charges collected for the state budget; however, such receipts must be separately estimated and planned with regard to the spending of such receipts. The plan thereof shall be sent to supervisory authorities as regulated.

Article 10. Estimation of the state budget expenditure

When estimating the expenditure from the 2017’s state budget, ministries, central bodies and local authorities shall focus on:

1. The estimation of the expenditure for development investment

a) From the year of 2017, the estimation of the expenditure for development investment from the state budget shall include investments financed by government bonds and earnings from the lottery business. The government shall present the plan for issuance of government bonds in 2017 to 2020 to the National Assembly for the latter's approval at the 2nd meeting of the 14th National Assembly.

b) The estimation of the expenditure for development investment from the state budget shall accord with the 2017’s plan for socio-economic development, the 5-year plan for socio-economic development from 2016 to 2020, the 5-year plan for medium-term public investments from 2016 to 2020 and the 10-year strategy of socio-economic development from 2011 to 2020. Such estimation shall adhere to the Law on public investment and shall only allocate finances to projects and programs expectedly included in the 5-year plan for medium-term public investments from 2016 to 2020 in conformity to principles, norms and rate of allocations for development investment from the state budget from 2016 to 2020 as defined in the Resolution No. 1023/NQ-UBTVQH13 dated August 28, 2015 by the Standing Committee of the National Assembly and the Prime Minister’s Decision No. 40/2015/QD-TTg dated September 14, 2015.

c) When estimating the expenditure for development investment from the state budget, ministries, agencies and local authorities shall specify details by sector as per the 2015's Law on state budget and prioritize projects in the following order: (i) allocation of finances for the completion and advancement of national target programs, projects of national importance, target programs and projects greatly significant to the nation-wide development of economy and society; (ii) counterpart financing of projects that employ ODA and concessional loans from foreign sponsors; government's investments in projects under public private partnership; settlement of outstanding payables for infrastructure construction and recovery of advances; (iii) remaining amounts allocated to new projects that satisfy all investment formalities as regulated.

d) If ministries, central bodies and local agencies are permitted by competent authorities to source investments from the proceeds of the sale of assets and collection of fee(s) for the use of land parcels on which there is (are) building(s), the former shall estimate the expenditure for development investment from such sources of finances and combine data in the estimate of their expenditure for development investment according to the Prime Minister’s decisions: No. 11/2016/QD-TTg dated March 07, 2016, No. 69/2014/QD-TTg dated December 10, 2014, No. 71/2014/QD-TTg dated February 15, 2014, No. 140/2008/QD-TTg dated October 21, 2008 and No. 09/2007/QD-TTg dated January 19, 2007.

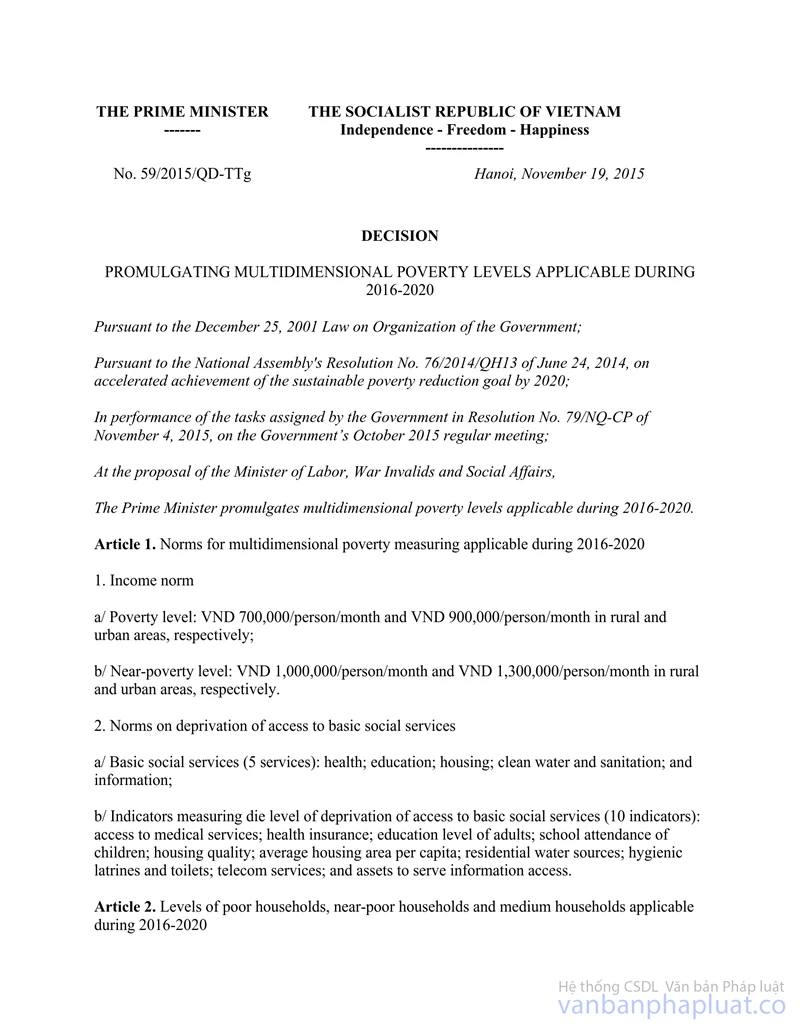

dd) Estimate the subsidy on differences in interest rates of the Government's loans for investment or social support by anticipate the 2017’s changes in beneficiaries, policies and missions according to the 2016’s situations (the anticipation of effects upon the application of the new poverty line according to the Prime Minister’s Decision No. 59/2015/QD-TTg dated November 19, 2015 on multi-sided poverty guidelines for the period of 2016 to 2020).

2. The estimation of the spending on the national reserve

From 2017, the spending on the national reserve shall be regarded as the state budget expenditure and excluded from the expenditure for development investment. Pursuant to the strategy for the development of the national reserve toward 2020, to the national reserve targets defined in the Law on national reserve and to the national reserve inventory anticipated until December 31, 2016, ministries and central bodies managing the national reserve shall plan the increase in purchases (enumerate each item in the national reserve), decrease in stock output and renewal of items in the national reserve. Moreover, they shall estimate the state budget expenditure for the 2017’s purchases for the national reserve on the principle of thorough thrift, focus on tactical necessities that are frequently consumed and useful in time of emergency, priority over nationally reserved items for prevention of and recovery from natural disasters, epidemic, fire, starvation, national defense and security.

3. The estimation of the regular expenditure

a) Ministries, central bodies and local authorities shall consider the 2017's political missions, socio-economic development plan(s) and estimate of budgetary revenues and expenditure to estimate the regular expenditure by sector in line with policies, regulations, principles, norms and rate of allocations for regular expenditure from the state budget in 2017.

Ministries, central and local bodies and agencies that utilize the state budget shall estimate the regular expenditure according to the nature of funds on the basis of thorough thrift. The estimation of the expenditure for the purchase, maintenance and repair of assets shall be subject to regulated standards, norms and regimes of the management and utilization of state-owned assets. The estimation of the expenditure for purchases of machinery and equipment as per the Prime Minister’s Decision No. 58/2015/QD-TTg dated November 17, 2015 and the estimation of the expenditure for purchases of vehicles shall only proceed if existing vehicles, after scrutinized, re-arranged and handled, do not suffice in standard and norm as defined in the Prime Minister’s Decision No. 32/2015/QD-TTg dated August 04, 2015. Downsize festivities, meetings, seminars, closing ceremonies, signing ceremonies, commencement ceremonies, title awarding and guest reception events as much as possible; and minimize allocations for overseas research trips, exploration trips and other unnecessary or non-exigent missions.

b) Estimate the administrative expenditure in connection with the schedule for downsizing of tenure and restructuring of the administrative system from 2016 to 2020 according to the Politburo’s Resolution No. 39-NQ/TW on tenure downsizing and public personnel restructuring; boost revenues, exercise thrift and downsize tenure faster than scheduled in order to elevate public personnel's income.

c) Ministries, central bodies and local authorities shall strictly embrace the schedule for pricing of public services funded by the state budget according to the Government’s Decree No. 16/2015/ND-CP expedite public service agencies' self-management, calculate the possibility of increase in public service agencies' revenues by sector as to lessen financial aids from the state budget. Determine the capacity of reserving fund(s), thereof, for higher direct aids to contributors to the revolution, poverty-stricken people and beneficiaries of regulated benefits as to allow them to access and use basic and necessary public services, and for higher spending on missions to which no source of revenues is available with the aim of restructuring the budgetary expenditure by sector and restructuring the state budget expenditure gradually.

d) Formulate and include in the estimate the regular sector-based expenditure of ministries, central and local bodies, the spending on operations of functional units that enforce administrative fines, and previous spending sourced from fees and charges that collecting units collect and retain but, according to the 2015's Law on state budget, shall be contributed to the state budget.

dd) Further notice for the estimation of the 2017’s state budget:

- Special spending and subsidy: From 2017, special spending and subsidies shall be categorized into relevant budgetary allocations and shall not be separately disbursed. Ministries, central and local bodies, whose missions receive such funding, shall formulate and present a detailed estimate with specific explanations to the Ministry of Finance, which shall summarize and report data to competent authorities for approval.

- Spending on science research: Estimate and explain the spending on the following science and technology missions approved by competent authorities:

+ Regular function-based missions (including the regular operational expenses of science and technology organizations) shall be estimated according to the Joint Circular No. 121/2014/TTLT-BTC-BKHCN dated August 25, 2014 by the Ministry of Finance and Ministry of Science and Technology on guidelines for the estimation, management, utilization and finalization of expenditure for regular function-based missions of public organizations in science and technology.

+ The spending on the science and technology missions at national, ministerial and grass-rote level and the competent authorities’ management of science and technology missions shall be estimated according to the Joint Circular No. 55/2015/TTLT-BTC-BKHCN dated April 22, 2015 by the Ministry of Finance and Ministry of Science and Technology on guidelines for the limitation, estimation and finalization of expenditure for state-funded science and technology missions.

+ Other non-regular missions of science and technology organizations shall be estimated as per the 2015’s Law on state budget and guiding documents.

- Spending on education and training: Explain the grounds for estimating the expenditure for exempting and reducing tuitions, providing educational aids, granting seniority pay and incentives to teachers and education management personnel in severely disadvantaged areas, etc.

- Spending on health care: Explain the grounds for calculating the expenditure required to implement the hospital overload reduction scheme in 2017 by project, mission and source of fund; assure that the state budget expenditure cover salary and particular allowances that have not been included in medical service prices and epidemic control allowances as per regulations; estimate the expenditure for examining, verifying and disposing unsafe food, inspecting, preventing and combating contraband, commercial fraud and counterfeits with regard to food safety and hygiene, etc.

- Spending on economic tasks: Formulate figures according to the workload assigned by competent authorities, regulations and rate of budgetary allocations; focus the spending on essential missions such as the maintenance of vital economic infrastructure (e.g. traffic, irrigation, etc.) in order to increase the lifetime of works and efficiency of investments; the activities of land planning; the advancement of agriculture, forestry, fishery, industry; the marking of border lines; the supporting of aquaculture; etc.

- Spending on administration, backed by clear explanation of:

+ The quantity of tenured positions in 2017 (the number defined by competent authorities in 2016 - tenured positions removed and added in 2016), including the actual number of tenured positions upon estimation and the amount of tenured positions approved but vacant (if any).

+ Formulate the fund(s) of salary and allowances on the basis of the statutory pay rate of VND 1,210,000 per month (in 12 months) as guaranteed by the state budget, as follows: (i) The fund(s) of salary and allowances for tenured positions approved and actually filled until the time of estimation, as formulated according to the salary grade, rank and position; the salary-related allowances and regulated contributions (i.e. social insurance, unemployment insurance, health insurance and labor union membership fee); (ii) the fund(s) of salary and allowances for tenured positions approved but vacant, as anticipated according to the statutory pay rate of VND 1,210,000 per month, salary rate of 2.34 per tenured position and regulated contributions.

+ Explain the grounds for estimating peculiar expenses (i.e. legal grounds, content and amount of spending, etc.) in 2017 on the basis of thrift and efficiency.

4. Ministries in charge of sectors and industries, apart from estimating the state budget revenues and expenditure in 2017 (in which they are directly involved), shall calculate the expenditure for implementing policies and mechanisms promulgated by competent authorities in 2017. Detailed explanation of such calculations must be enclosed.

5. Financing of salary reform

In 2017, the mechanism for financing of salary reform shall progress to augment the statutory pay rate more than VND 1,210,000 per month (if applicable) as per regulations.

6. The estimation of the expenditure for national target programs and target programs.

Ministries presiding at national target programs and target programs shall base on the Prime Minister’s approvals of such programs to estimate the expenditure thereof, as follows:

- The expenditure for development investment in line with the plan for medium-term public investments in 2016 to 2020 and in conformity with the norms and rate of the state budget expenditure for development investment in 2016 to 2020 are stated in the Prime Minister's Decision No. 40/2015/QD-TTg dated September 14, 2015.

- The regular expenditure for national target programs and target programs connects with the formulation of the 2017's objectives and missions.

7. For projects and programs funded by the official development assistance (ODA) and concessional loans

Estimate the 2017’s budget as per the Law on state budget, Law on public debt management, Law on public investment and guiding documents, and specify sponsors' ODAs, concessional loans, grant aids, counterpart finances by project or program according to the nature of funds in use (for development investment and function-based operation) by project and sector.

Estimate the budgetary expenditure sourced from ODAs and concessional loans in line with the schedule of disbursement as committed to the sponsors, counterpart financing capacity and feasibility. Minimize the enlargement of funds beyond the estimate assigned to the organizations that carry out projects. Carry out only new projects and programs that are truly feasible and conformable to the disbursement of ODAs in conformity to signed treaties and the Prime Minister's approval.

The agencies governing joint programs and projects of ministries, central and local bodies shall prepare and send the detailed estimate with specific grounds of allocations for each ministry, each central body and each local authority to the Ministry of Finance and Ministry of Planning and Investment, which shall summarize and present data to competent authorities for approval.

8. Provisions for the state budget

The state budget and local budgets at various levels shall arrange budgetary provisions according to the 2015's Law on state budget as to make an active response to natural disasters, flood, epidemic, vital and urgent missions beyond estimation.

9. The estimation the expenditure sourced from revenues retained as per regulations

Ministries, central and local bodies shall estimate the expenditure sourced from regulated revenues retained (i.e. fees collected and cash mobilized) as per Section 1 and 3 of this Article. Such expenditure shall be incorporated into the estimates of budgetary expenditure of ministries, central and local bodies.

10. Ministries, central and local bodies shall base on the examination of the 2017's budgetary revenues and expenditure to estimate the spending by sector minutely according to the 2015’s Law on state budget for each mission and each subordinate unit receiving funds. Ministries, central bodies and provincial authorities, after discussing matters with the Ministry of Finance and Ministry of Planning and Investment, shall promptly plan the relevant budgetary allocations estimated for 2017 as to apply for competent authorities' approval of the allocations and to assign the budgetary estimates to funded units, upon their receipt of the Prime Minister's budget estimates, before December 31, 2016 as per the 2015's Law on state budget.

11. Ministries, central bodies and local agencies shall make report(s) on the 2016's financial revenues and spending and on the 2017’s anticipated revenues and spending in connection with off-budget financial funds under their management as per Section 11, Article 8 of the 2015’s Law on state budget. Such report(s) shall be submitted with the estimate of the 2017’s state budget.

Article 11. Estimation of local budget

The year of 2017 shall be the first year of the local budget stabilization period of 2017 to 2020 as defined in the 2015‘s Law on state budget. The estimation of the revenues and expenditure in 2017 and from 2017 to 2020 shall adhere to the national and local objectives and missions of socio-economic development in 2017 and from 2016 to 2020. Sources of revenues and funded missions shall be arranged on according to the 2015‘s Law on state budget and guiding documents, principles, norms and rate of allocations (for development investment and regular activities) with the aim of maintaining resources for implementing policies and regulations that the central government has promulgated in conformity to the Law on state budget.

In addition to general guidelines for the estimation of the state budget, the estimation of the local budget shall aim attention at:

1. The estimation of local budget revenues

Local authorities shall estimate all revenues sourced from taxes, fees, charges and other proceeds collected locally as per Article 7 of the 2015’s Law on state budget and relevant laws.

Consider the objects and plans of socio-economic development for 5-year period of 2016 to 2020 and the feasibility of socio-economic norms and the 2016’s budget to calculate fully and precisely each regulated revenue by sector on the basis of the anticipated pace of economic growth and scope of state budget revenues as per the 2015's Law on state budget, of the 2017's revenues anticipated by industry and by sector, of economic units of each locality and local revenues having recently ensued. Analyze and evaluate particular factors that influence proceeds estimated for the 2017’s state budget by locality, by sector, by revenue and by tax.

2. The estimation of the local budget expenditure

Determine the proportion (%) of revenues of the central budget to the local budget and the supplementary amounts (if any) from the central budget to the local budget on the basis of the estimate of local revenues for the state budget, the local budget revenues fully retained as per the 2015’s Law on state budget, the balanced expenditure from the local budget according to the norms and rate of budgetary allocations (for development investment and regular activities) in conformity to the Resolution of the Standing Committee of the National Assembly and the Prime Minister’s decisions. Departments of Finance shall lead and coordinate with relevant agencies, thereof, consider the local missions of socio-economic development from 2016 to 2020, the 2017's objectives of socio-economic development, the current regulations and policies on spending and local circumstances, to provide counsels to the provincial People's Committees, which shall present data to the equivalent People's Councils for decisions on: The gradation of revenue sources and funded missions in the budget stabilization period of 2017 to 2020, the rating of allocations from the local budget in 2017 for each inferior local authority, as to determine the supplementary amounts from the budget to the lower ones and the apportionment (%) of revenues for the budgets of various local authorities during the stabilization period of 2017 to 2020 in line with local circumstances. The rate of allocations from the local budget to vital funded missions (e.g. education, vocational training, science and technology) shall be maintained at least on a par with the demands stated in the resolutions of the Vietnam Communist Party, decisions of the National Assembly and the assignment by the Prime Minister (the estimated expenditure for science and technology research is only arranged on at provincial level but not at district or communal level as per the 2015's Law on state budget). Moreover, these primary contents shall be actualized:

a) For the estimation of the local budget expenditure for development investment: Base on the Law on public investment , the requirements for the planning of medium-term public investments from 2016 to 2020, and the estimate of the local budget expenditure for development investment as per the Prime Minister’s Decision No. 40/2015/QD-TTg dated September 14, 2015 on the principles, norms and rate of allocations for development investment from the state budget from 2016 to 2020, in order to prioritize finances for the construction of infrastructure, investment into vital local projects and buildings to be soon operated in 2017; scrutinize and supervise minutely the allocations estimated for economic infrastructure projects, e.g. economic zones and industrial parks, particularly those essential to the development of local and regional economy and society, focus on the eradication and reduction of poverty, create jobs, cope with social unrest; etc. Counsels and supervisory opinions from central bodies, critics from professional and social organizations and relevant local agencies must be actively sought after prior to such actions as to maintain the general economic efficiency of the locality and the entire region.

b) Estimate the targeted supplementary capital outlay disbursed from the central budget to the local budget according to the balancing of the local budget, the estimation of targeted supplementary amounts disbursed from the central budget to the local budget in 2016, the current policies and regulations, the vital programs and missions that progress under targeted supplementary finances given by the central authorities to localities, the National Assembly's resolution(s) on national target programs and target programs, the norms and rate of allocations for development investment and the public investment plan for 2016 to 2020.

c) Arrange the counterpart finances adequately for local ODA projects intra vires; formulate and arrange resources in active manner to settle financial liabilities for infrastructure construction and mature debts derived from funds mobilized.

d) Arrange the finances estimated for development investment, which are sourced from land use levy, into economic and social infrastructure, relocation, resettlement and preparation of construction grounds; allocation finances to establish the land development fund in active manner according to the Government's Decree No. 43/2014/ND-CP dated May 15, 2014. At least 10% of the levy of land use and land rent shall be spent on land measurement and registration, cadastral documentation and certification of land use right according to the Prime Minister's Directive No. 1474/CT-TTg dated August 24, 2011 and Directive No. 05/CT-TTg dated April 04, 2013.

dd) With regard to revenues from the lottery business: From 2017, these revenues shall be included in the estimate of revenues for balancing the local budget and for development investment, as follows: Provinces in the North, the Central and central highlands shall invest at least 60% of the estimated revenues from the lottery business, at the discretion of the provincial People’s Council, in education, vocational training and health care. At least 50% of such revenues shall be invested by the Provinces in the Southeast and Mekong Delta. At least 10% of such revenues shall be locally invested into the national target program of new rural development. After finances for the completion of the said investment projects have been arranged as per competent authorities' approval, the remaining revenues (if available) shall be reserved for construction works that respond to climate change and other vital buildings eligible for investments from the local budget. The extra revenues from the lottery business (if available) beyond the estimate assigned by the provincial People's Council shall be locally invested, at local authorities’ discretion, into vital projects for education, vocational training, health care, agriculture, rural development and response to climate change.

e) Local authorities shall actively formulate the missions on infrastructure development investment, arrange the local budget and financial resources as regulated for such missions, and reduce dependence on supplementary funds from the central budget in accordance with the Politburo’s resolutions, Prime Minister’s decisions, objectives, missions and demand of regulated investments, result of investments finished in 2015 and possibly made in 2016.

g) Estimate the 2017’s budgetary expenditure and actively formulate resources as per regulations for salary reform.

h) Estimate the expenditure for repayment of principal loan and interest:

Pursuant to Section 3, Article 8 of the 2002’s Law on state budget, provinces can mobilize domestic finances into the provincial budget for later investments and arrange funds from their balanced capital for annual development investment to repay the interest and principal loans mobilized. Pursuant to the 2015’s Law on state budget, from the year of 2017:

- Arrange the separate expenditure for payment of interest, fees and other expenses from the balanced local budget.

- Arrange resources defined in Point a, Section 3.4, Clause 3 of this Article to repay principal loans. If loan debts estimated until December 31, 2016 exceed the loan debt limit defined in the 2015's Law on state budget, the budget estimates for 2017 and subsequent years must reserve the local budget revenues apportioned by level and reduce the medium-term public investments planned for 2016 to 2020 for repayment of principal loans and for maintaining of the loan debt balance below the local loan debt limit defined in the 2015’s Law on state budget.

3. Local budget deficit: Local authorities shall propose the level of provincial budget deficit for 2017 on the basis of the loan debt limit defined in the 2015’s Law on state budget, loan debts actually incurred until the end of 2016 and demand for additional finances for development investment and repayment of debts.

Ministry of Finance shall consider the limit of public debts and capacity of mobilizing domestic finances for repayment of debts to propose the general level of state budget deficit, including the deficit levels of the central budget, total and separate local budgets (if applicable), and present such proposition to competent authorities for approval in conformity to the 2015's Law on state budget.

Local authorities, in addition to their proposal of the local budget deficit as per Section 5, Article 7 of the 2015’s Law on state budget, shall determine the total level of borrowing for the local budget, including borrowings for offsetting the local budget deficit and for repayment of principal loans; as follows:

3.1. Local budget deficit is cut by:

a) Domestic loan sourced from the issuance from municipal bonds and other domestic loans gained as per the laws;

b) Loans that the Government relends to local budgets.

3.2. Borrowings for offsetting the budget deficit as stated in Section 3.1 above do not include those for repayment of principal loans.

3.3. Local budget deficit is permissible on the following conditions:

a) Only for medium-term public investments into the projects approved by the provincial People’s Council as per Point a, Section 5, Article 7 of the Law on state budget;

b) A province's budget deficit per year shall not exceed the level of annual budget deficit that the National Assembly sets for the province as per Point c, Section 5, Article 7 of the Law on state budget;

c) Loan debts payable in the fiscal year prior to the year of estimation do not become overdue in 90 days from the end of such fiscal year. Ministry of Finance shall present special circumstances to the National Assembly for the latter’s decisions;

d) Borrowings for offsetting the local budget deficit shall be primarily sourced from medium-term and long-term loans. On annual basis, the Ministry of Finance shall consider the capital market’s occurrences and present data to the Government and the National Assembly for their regulation of the minimum proportion of medium-term and long-term loans for offsetting the local budget deficit;

dd) In comparison with the loan debt limit, the loan debt balance of the local budget shall consist of debts sourced from: loans from the State Treasury, loans from the Vietnam Development Bank, municipal bonds, foreign loans that the Government relends and other domestic loans as per the laws. The debt balance of the local budget, including borrowings for offsetting deficit as estimated, shall not exceed the limit of loan debt defined in Section 6, Article 7 of the 2015's Law on state budget.

e) The local budget revenues granted by echelon shall be higher or lower than or equal to regular expenditure defined in Section 6, Article 7 of the 2015's Law on state budget on the basis of the estimate of local budget revenues and expenditure that the National Assembly has decided for the year of budget estimation.

3.4. Repayment of principal loans

a) Resources for repayment of principal loans:

- Borrowings for repayment of principal loans, as defined by the National Assembly and provincial People’s Council on annual basis;

- Provinces' local budget revenues in surplus (i.e. the total provincial budget revenues estimated is larger than the total provincial budget expenditure estimated for a province in a fiscal year);

- Surplus from the central budget and provincial budget as per Section 1, Article 72 of the Law on state budget;

- Revenues increased and spending spared in comparison with the estimate upon the adherence to the state budget as per Point a, Section 2, Article 59 of the Law on state budget;

b) Principal loans due must be prepaid fully and punctually according to commitments and signed contracts.

c) Repayment of principal loans shall be subjected to the management and accounting of the State Treasury.

Chapter III

IMPLEMENTATION

Article 12. Responsibilities for ministries and agencies that manage national target programs and target programs

1. Coordinate with relevant ministries, central bodies and local authorities in anticipating the missions and expenditure for national target programs and target programs in 2017 and deliver such information to the Ministry of Finance and Ministry of Planning and Investment by July 20, 2016.

2. Plan allocations estimated for 2017 for each ministry, central body and province and send such plans to the Ministry of Finance and Ministry of Planning and Investment for their summarization by the time limit defined in the written notice by the Ministry of Finance and Ministry of Planning and Investment of the 2017’s expenditure for national target programs and target programs.

Article 13. Responsibilities of ministries, central bodies and local authorities

1. Ministries, central bodies and provincial People’s Committees shall consider figures verified and announced to provide guidelines and such figures on budgetary revenues and expenditure to inferior recipients of funds and subordinate budgets as per regulations.

2. Ministry of Planning and Investment shall lead and cooperate with the Ministry of Finance in planning allocations for development investment (including the expenditure for development investment through national target programs and target programs) and deliver such plan to the Ministry of Finance by August 31, 2016.

3. Ministries and agencies managing the national reserve shall plan the national reserve, estimate the budgetary spending on the national reserve and send such information to the Ministry of Finance by July 20, 2016.

4. The estimation, summarization and reporting of the 2017’s budget shall abide by the 2015’s Law on state budget, Law on public investment, guiding documents and this Circular’s guidelines. Since guiding documents for the 2015’s Law on state budget are not yet promulgated, ministries and central bodies shall use the report forms in the Circular No. 59/2003/TT-BTC dated June 23, 2003 by the Ministry of Finance and other forms defined in this Circular. Local authorities shall use report forms defined in this Circular. Reports must be sent to the Ministry of Finance and Ministry of Planning and Investment by July 20, 2016.

Article 14. Discussion of estimates and forms for estimation and reporting of the 2017's state budget

1. For the year of 2017, as the first year of the budget stabilization period of 2017 to 2020, finance agencies shall lead and coordinate with other agencies in planning and investment, taxation and relevant sectors in organizing discussions with inferior People’s Committees to estimate the budgetary revenues and expenditure, proportion (%) of revenues and supplementary aids of superior budgets to inferior budgets.

2. Ministries and central bodies shall:

Summarize and report the budget estimates to the Ministry of Finance via the forms defined in the Circular No. 59/2003/TT-BTC additional forms (Form No. 2, 20, 21, 22, 23, 24, 25a, 25b, 26a and 26b) as defined in this Circular and the forms defined in the Joint Circular No. 71/2014/TTLT-BTC-BNV dated May 30, 2014 by the Ministry of Finance and Ministry of Home affairs on guidelines for the implementation of the Government’s Decree No. 130/2005/ND-CP dated October 17, 2005 on government authorities’ self-management and self-accountability in spending on administration, the Government's Decree No. 117/2013/ND-CP dated May 30, 2013 on amendments to certain articles of the Decree No. 130/2005/ND-CP The budget estimate shall be specific to each essential mission of ministries and agencies; therefore, the budget estimate of each ministry or central body shall be reported to the National Assembly.

3. Local authorities shall: Summarize and estimate the local budget and make reports to the Ministry of Finance via the forms (Form No. 1, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 18 and 19) as defined in this Circular.

Article 15. Implementation

1. This Circular comes into effect as of August 10, 2016. The content, procedure and time for the estimation of the 2017's state budget shall abide by the 2015's Law on state budget and this Circular’s guidelines.

2. During the estimation of the 2017’s state budget, the Ministry of Finance shall announce further guidelines if new policies and regulations are promulgated. Ministries, central and local authorities, state-owned business groups and corporations shall report difficulties regarding the estimation of the 2017's state budget to the Ministry of Finance for timely solutions./.

|

|

p.p. MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft and

for reference purposes only. Its copyright is owned by LawSoft

and protected under Clause 2, Article 14 of the Law on Intellectual Property.Your comments are always welcomed