Nội dung toàn văn Official Dispatch No. 12399/BTC-TCT, on guidance on tax declaration and payment

|

THE

MINISTRY OF FINANCE |

SOCIALIST

REPUBLIC OF VIET NAM |

|

No. 12399/BTC-TCT |

Hanoi, September 03, 2009 |

To: Provincial – level Tax Departments

Pursuant to Tax

Administration Law No. 78/2006/QH11 of November 29, 2006, and its guiding

documents;

Pursuant to the Government's Decree No. 142/2007/ND-CP of September 5, 2007,

promulgating the financial management regulation of the parent company -

Vietnam Oil and Gas Group;

Pursuant to the Ministry of Finance's Circular No. 56/2008/TT-BTC of June 23,

2008, guiding the declaration, payment and finalization of state revenues

specified in Article 18 of the financial management regulation of the parent

company - Vietnam Oil and Gas Group, promulgated together with the Government's

Decree No. 142/2007/ND-CP of September 5, 2007;

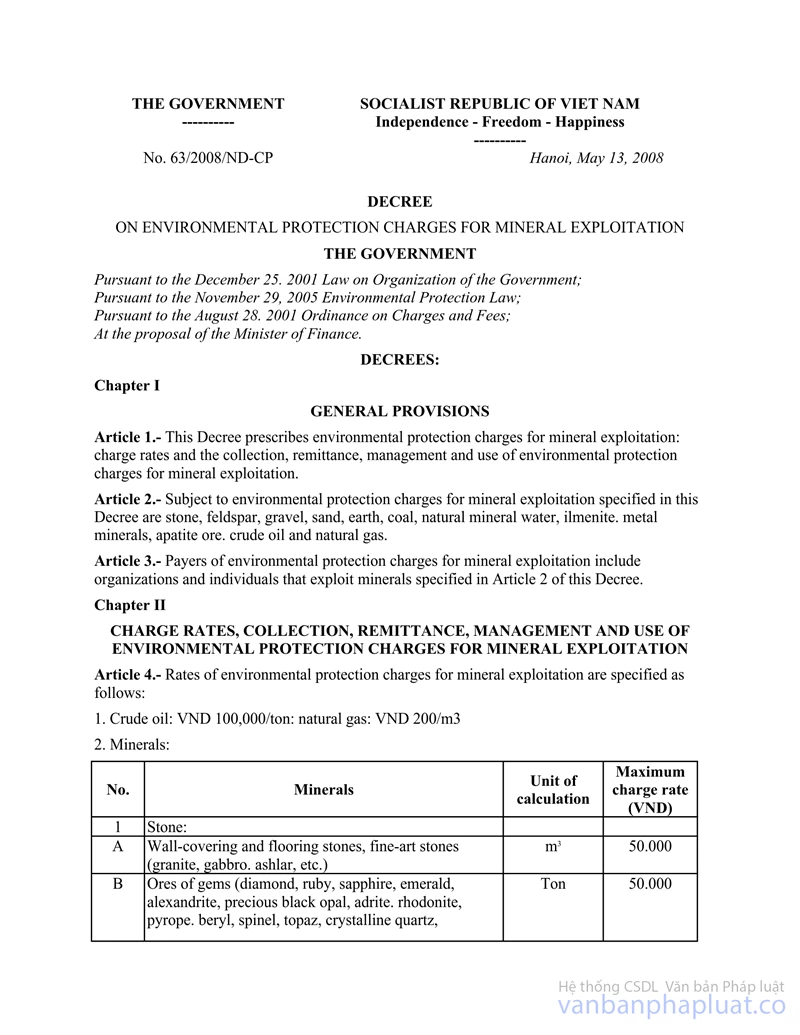

Pursuant to the Government's Decree No. 63/2008/ND-CP of May 13, 2008, on

environmental protection charges for mining;

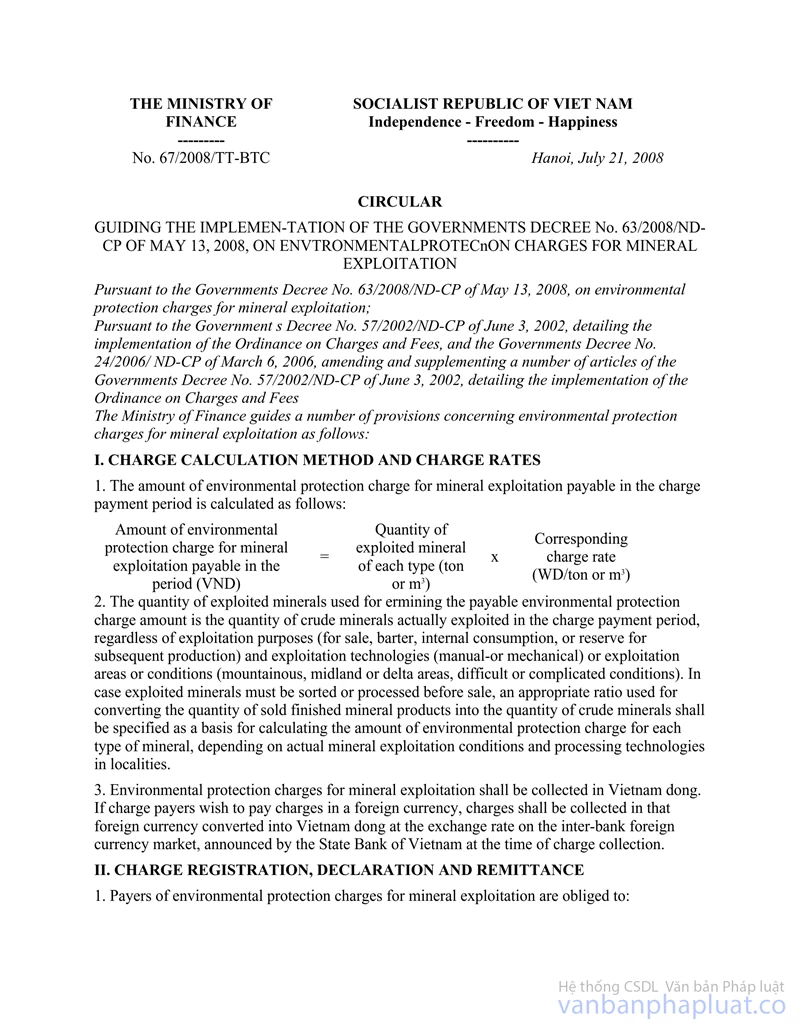

Pursuant to the Ministry of Finance's Circular No. 67/2008/TT-BTC of July 21,

2008, guiding the Government's Decree No. 63/2008/ND-CP of May 13, 2008, on

environmental protection charges for mining;

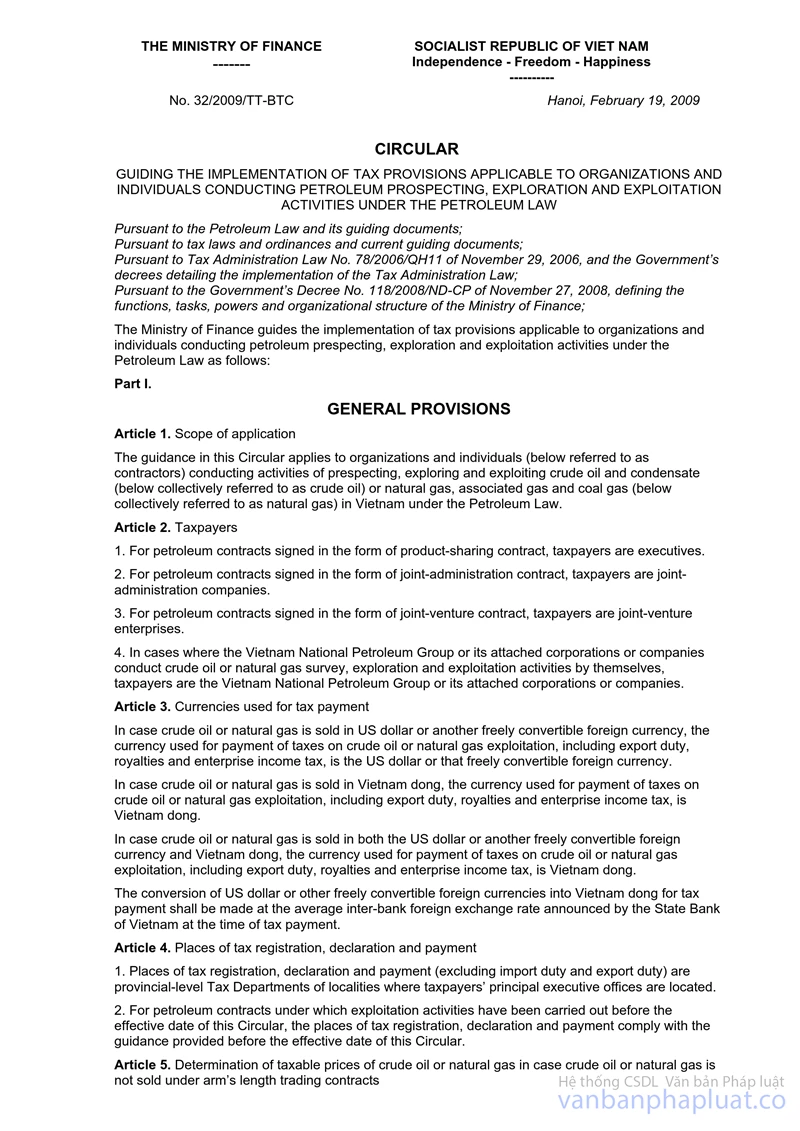

Pursuant to the Ministry of Finance's Circular No. 32/2009/TT-BTC of February

19, 2009, guiding tax regulations applicable to organizations and individuals

engaged in oil and gas exploration and exploitation under the Petroleum Law;

Pursuant to the Minister of Finance’s Decision No. 33/2008/QD-BTC of June 2,

2008, promulgating the state budget revenue index;

Pursuant to the Ministry of Finance's Circular No. 136/2009/TT-BTC of July 2,

2009, supplementing and amending the state budget revenue index;

The Ministry of Finance guides the declaration and remittance into the state

budget of revenues from crude oil, condensate and natural and associated gas as

follows:

1. Places of registration and declaration of taxes, charges and fees on crude oil, condensate and natural and associated gas:

- Places of registration and declaration of royalty tax, business income tax and export and import duties on crude oil, condensate and natural and associated gas comply with the Ministry of Finance's Circular No. 32/2009/TT-BTC of February 19, 2009.

- Places of registration and declaration of the Vietnamese Government’s shared post-tax profits and profit oil and gas comply with the Ministry of Finance's Circular No. 56/2008/TT-BTC of June 23, 2008. Royalty tax on the Black Lion field shall be declared at Ho Chi Minh City Tax Department.

- Places of registration, declaration and payment of environmental protection charges for crude oil, condensate and natural and associated gas comply with the Ministry of Finance's Circular No. 67/2008/TT-BTC of July 21, 2008.

2. Accounts for deposit of revenues from crude oil, condensate and natural and associated gas:

All revenues from crude oil, condensate and natural and associated gas at the exploitation stage shall be deposited into state budget revenue accounts at state treasuries of localities where enterprises register and declare tax, and wholly transferred to the central budget under regulations.

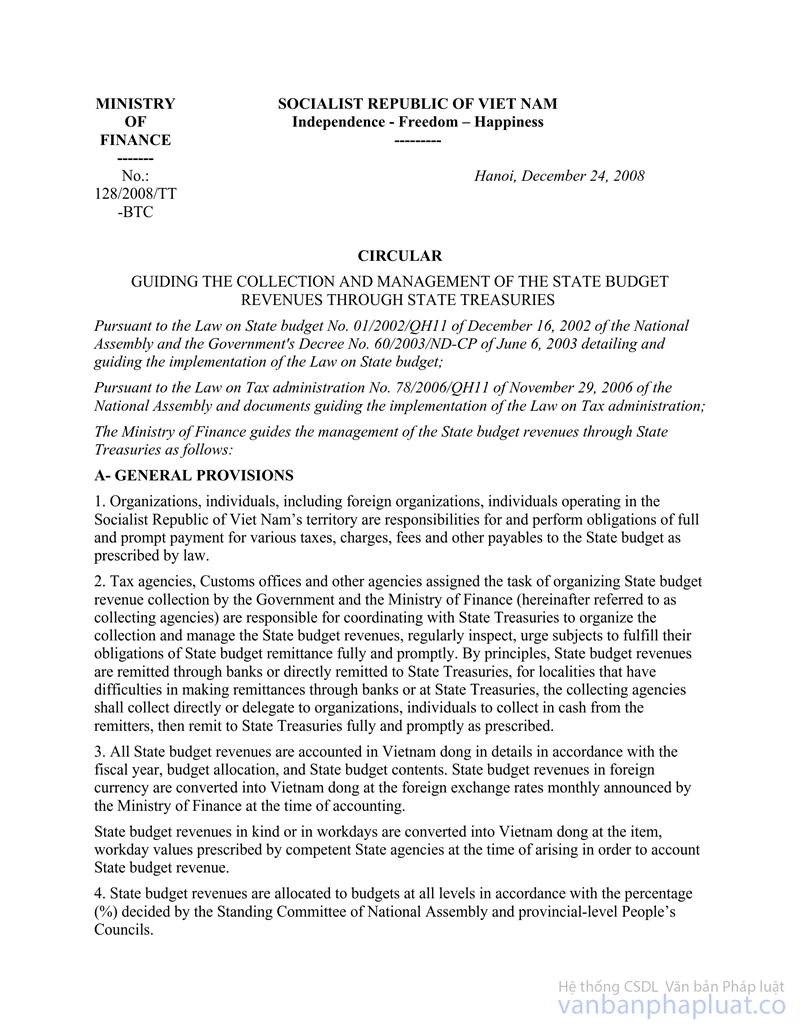

The accounting and management of foreign currencies comply with the Ministry of Finance's Circular No. 128/2008/TT-BTC of December 24, 2008, guiding the collection and management of state budget revenues through the State Treasury and the Minister of Finance’s Decision No. 120/2008/QD-BTC of December 22, 2008, promulgating the Regulation on the state budget accounting system and state treasury operations.

3. Accounting of revenues from oil and gas:

Under the Minister of Finance’s Decision No.33/2008/QD-BTC of June 2, 2008, promulgating the state budget revenue index, and the Ministry of Finance's Circulars No. 128/2008/TT-BTC of December 24, 2008, guiding the collection and management of state budget revenues through the State Treasury and No. 136/2009/TT-BTC of July 2, 2009, supplementing and amending the state budget index, the Ministry of Finance guides the accounting of revenues from oil and gas as follows:

3.1. Chapter, items:

- Chapters: Under the chapters applicable to explorers, traders or processors or units enjoying benefits from oil and gas exploration and exploitation.

- Items:

|

Item |

Name |

Content |

|

042 |

Crude oil and natural gas exploitation |

Exploitation of oil wells by different methods, exploitation and production of natural fuel gas, including liquefied gas; also covering such treatments as salt decanting, desalting, dehydrating, purifying and some other processes without changing the basic characteristics of products |

|

048 |

Support services for exploitation of crude oil and natural fuel gas |

Covering prospecting drilling, oil rig construction, well bank plastering, oil well pumping, etc. |

|

069 |

Other support services for mining and ore exploitation |

Including surveying and exploration in service of mining and ore exploitation. |

3.2. Sub-items:

3.2.1. Oil revenues under agreements and contracts shall be accounted in item 3750 “oil revenues under agreements and contracts”:

|

Sub-item |

Name |

|

3751 |

Royalty tax |

|

3752 |

Business income tax |

|

3753 |

Vietnamese Government’s shared post-tax profit |

|

3754 |

Vietnamese Government’s shared profit oil |

|

3799 |

Others |

3.2.2. Condensate revenues under agreements and contracts shall be accounted in item 3950 “condensate revenues under agreement and contracts”:

|

Sub-item |

Name |

|

3951 |

Royalty tax |

|

3952 |

Business income tax |

|

3953 |

Vietnamese Government’s shared profit |

|

3999 |

Others |

Condensate revenues between January 1, 2009, and before the effective date of Circular No. 136/2009/TT-BTC which have been accounted in the item “natural gas,” will not be adjusted again.

As the 2009 state budget estimates have accounted condensate revenues as domestic revenues, condensate revenues in 2009 accounted in item 3950 will be included in the 2009 domestic revenue target for evaluation of the fulfillment of 2009 budget estimate targets. From 2010 onward, all condensate revenues will be included in the crude oil revenue target.

3.2.3. The Government’s shared revenues from natural and associated gas under agreements and contracts shall be accounted in item 3800 “the Government’s shared revenues from natural gas under agreements and contracts on oil and gas exploration and exploitation”:

|

Sub-item |

Name |

|

3801 |

Royalty tax |

|

3802 |

Business income tax |

|

3803 |

Vietnamese Government’s shared profit gas |

|

3849 |

Others |

3.2.4. Revenues from royalty tax on crude oil and natural and associated gas not under product sharing agreements and contracts (for instance, damp gas from the White Tiger field) shall be accounted in item 1550 “royalty tax” - sub-item 1551 “oil, gas (excluding royalty tax collected under agreements and contracts on oil and gas exploration and exploitation).”

3.2.5. Vouchers on remittance into the state budget: To specify revenues from each item, namely crude oil, condensate, natural gas and associated gas, in the part “payment details.”

Provincial-level Tax Departments are requested to guide units in complying with the guidance under this Official Letter. In the course of implementation, provincial-level Tax Departments and units should promptly report on any arising problems to the Ministry of Finance (the General Department of Taxation) for consideration and settlement.

|

|

FOR

THE MINISTER OF FINANCE |