Circular No.193/2012/TT-BTC promulgating the preferential import and export tari đã được thay thế bởi Circular No. 164/2013/TT-BTC export tariff schedule and preferential import tariff schedule và được áp dụng kể từ ngày 01/01/2014.

Nội dung toàn văn Circular No.193/2012/TT-BTC promulgating the preferential import and export tari

|

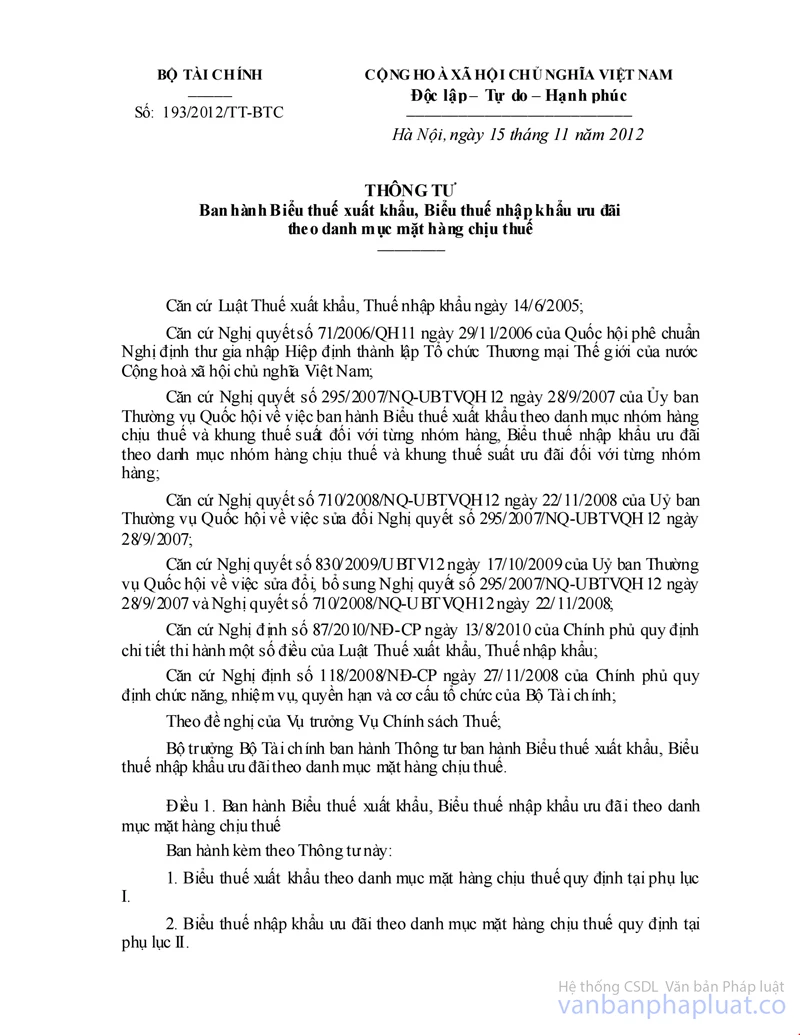

THE MINISTRY

OF FINANCE |

SOCIALIST

REPUBLIC OF VIETNAM |

|

No. 193/2012/TT-BTC |

Hanoi, November 15, 2012 |

CIRCULAR

PROMULGATING THE PREFERENTIAL IMPORT AND EXPORT TARIFF ACCORDING TO THE LIST OF TAXABLE PRODUCTS

Pursuant to the Law on Export and import tax dated June 14th 2005;

Pursuant to the National Assembly’s Resolution No. 71/2006/QH11 dated November 29th 2006, approving Protocols on the participation in the Agreement on establishing the World Trade Organization of the Socialist Republic of Vietnam;

Pursuant to the Resolution No. 295/2007/NQ-UBTVQH12 dated September 28th 2007 of the Standing Committee of the National Assembly, promulgating the Export tariff according to the list of taxable headings and the tax bracket on each heading, the preferential import tariff according to the list of taxable headings and preferential tax bracket on each heading

Pursuant to the Resolution No. 710/2008/NQ-UBTVQH12 dated November 22nd 2008 of the Standing Committee of the National Assembly, amending the the Resolution No. 295/2007/NQ-UBTVQH12 dated September 28th 2007;

Pursuant to the Resolution No. 830/2009/UBTV12 dated October 17th 2009 of the Standing Committee of the National Assembly, amending and supplementing the Resolution No. 295/2007/NQ-UBTVQH12 dated September 28th 2007 and the Resolution No. 710/2008/NQ-UBTVQH12 dated November 22nd 2008;

Pursuant to the Government's Decree No. 87/2010/NĐ-CP dated August 13th 2010, detailing the implementation of a number of articles of the Law on Export and import tax;

Pursuant to the Government's Decree No. 118/2008/NĐ-CP dated November 27th 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance ;

At the proposal of the Director of the Tax Policy Department;

The Minister of Finance issues a Circular promulgating the preferential import and export tariff according to the list of taxable products.

Article 1. Promulgating the preferential import tariff and export tariff according to the list of taxable product:

1. The export tariff according to the list of taxable products in Annex I.

2. The preferential import tariff according to the list of taxable products in Annex II.

Article 2. The export tariff according to the list of taxable products

1. The export tariff according to the list of taxable products in Annex I includes the description (names of headings and products), the codes (a heading has 04 digits, a particular product has 08 digits), the export tax rates on the headings and products subject to export tax. When following the customs procedures, the customs declarant must specify the 8-digit product codes in the export tariff. If an exported product does not have a specific 8-digit code in the export tariff, the declarant must provide the 8-digit code of that product in the preferential import tariff in Section I Annex II enclosed with this Circular, and specify the export tax rate on the heading or sub-heading of products in the export tariff.

Example: Write the 8-digit code 4404.10.00 and the tax rate of 5% of heading 4404 when exporting coniferous wood.

2. If a product is not specified in the export tariff, the customs declarant must provide its corresponding 8-digit of that product in the preferential import tariff in Section I of Annex II enclosed with this Circular, and the export tax rate of 0%.

3. The export tax rate on exported goods produced or processed using imported materials:

a) The goods entirely produced or processed using imported materials are exempted from export tax. Paint, varnish, and screw attach to wood are considered accessories.

b) If the goods are produced or processed from imported materials and domestic materials, the export tax on the amount of exported goods proportional to the amount of imported materials used for producing and processing such exported goods is exempted. The amount exported goods produced or processed from domestic materials are subject to the export tax rate on such exported goods.

c) The dossier of application for the exemption of export tax on exported goods submitted to the Customs includes:

- The written application for the exemption of export tax on exported goods produced or processed from imported materials, specifying the amount and value of imported materials used for producing or processing exported goods; the amount of exported goods, the exempted export tax: submit 01 original;

- The declaration of imported materials that have undergone customs procedures: submit 01 photocopy and present 01 original for comparison;

- The declaration of exported goods: submit 01 original;

- The export and import contracts; or the export and import authorization contract (applicable to export and import authorization): submit 01 photocopy;

- The sale contract (if the enterprise that imports the materials for producing or processing exported goods does not directly export them nor authorize the export, but sells them to another exporter): submit 01 photocopy;

- The contract on the cooperation in producing or processing exported goods if the exported goods are produced or processed in cooperation: submit 01 photocopy;

- The registration sheet of the amount of imported materials for producing or processing exported goods, specifying the proportion imported materials and domestic materials (each declaration of imported materials shall apply for 01 registration): present 01 original and submit 01 photocopy.

- The list of declarations of imported materials for producing or processing exported goods, specifying the amount of imported materials: submit 01 photocopy;

- The list of documents in the dossier of application for the tax exemption: submit 01 original.

The declaration content in the dossier of application for the exemption of export tax on exported goods prescribed in this Point is guided in the Circular No. 194/ 2010/TT-BTC dated December 06th 2010 of the Ministry of Finance, guiding the customs procedures, customs supervision; export tax, import tax, and tax administration applicable to exported and imported goods.

4. For gold (in Heading 71.08), golden jewelry (in Heading 71.13), articles of goldsmith (in Heading 71.14) and other golden articles (in Heading 71.15) eligible for the tax rate of 0%: apart from the customs dossier of exported goods according to common regulations, it is required to have the certificate of gold content issued by an competent agency guided in the Circular No. 49/2010/TT-BTC dated April 12th 2010 of the Ministry of Finance, guiding the classification and tax rates on exported and imported goods (present 01 original for comparison and submit 01 photocopy to the Customs) If there are grounds to conclude that the gold is entirely produced from imported materials, and is exported in the form of export production, the certificate of gold content is exempted, but the license for importing gold as material issued by the State bank is compulsory as prescribed in the Circular No. 16/2012/TT-NHNN dated May 25th 2012: submit 01 copy bearing the stamp of the enterprise, and present the original for comparison.

Article 3. The preferential import tariff according to the list of taxable products

The preferential import tariff according to the list of taxable products in Annex II includes:

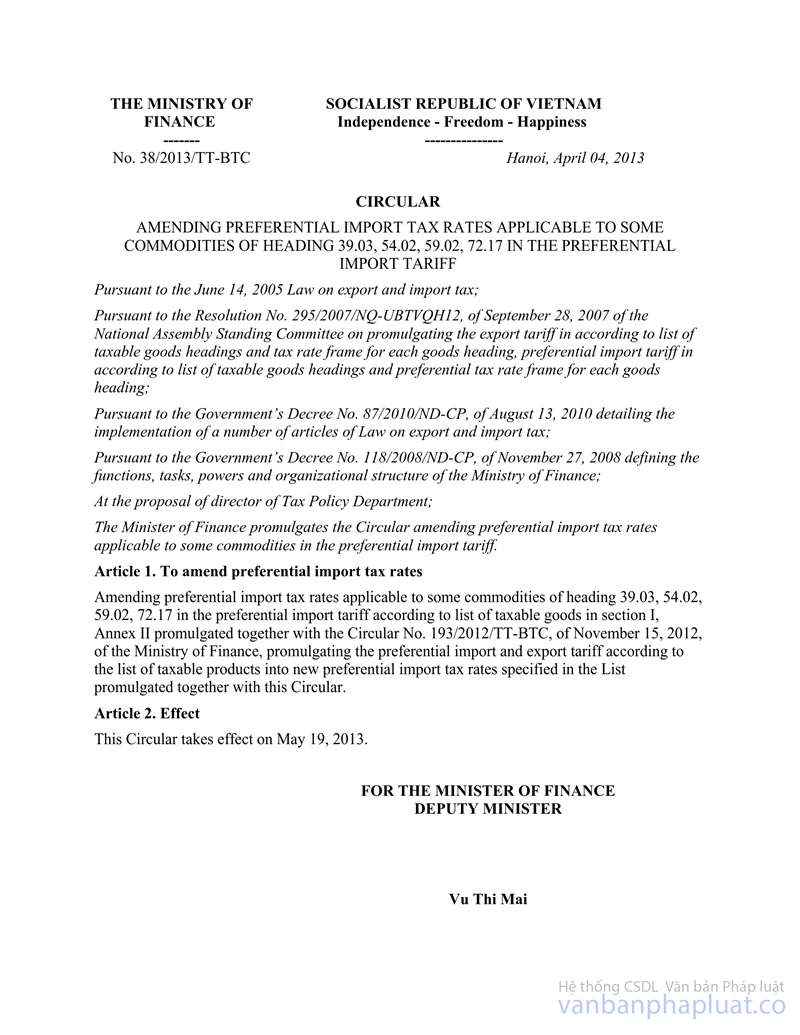

1. Section I: The preferential import tax rates applicable in 97 chapters according to the list of goods imported to Vietnam. The content includes the description (names of headings and products), the codes (a heading has 04 digits, a particular product has 08 digits), the preferential import tax rates on the headings and taxable products.

2. Section II: Chapter 98 - The codes and the other preferential import tax rates on some particular headings and products. Including:

a) The description and application of other preferential import tax rates. For the headings and products subject to the other preferential import tax rates for headings from 98.17 to 98.23 in Chapter 98: the tax payer must finalize the import and use of goods in Section II of Annex II enclosed with this Circular (except for the imported goods in Headings 9820, 9821 and 9823).

b) The list of headings, products, and the preferential import tax rates: the names of headings, products; the product codes in Chapter 98; the corresponding codes of those headings and products in Section I of Annex II (97 Chapters according to the Vietnam’s import tariff) and the special preferential import tax rates in Chapter 98.

c) If the goods eligible for the other preferential import tax rates prescribed in Chapter 98 are eligible for special preferential import tax rates as prescribed by current regulations, they may apply the special preferential import tax rates prescribed in the Circulars promulgating the special preferential import tariff or other preferential import tax rates prescribed in Chapter 98 of this Circular. When following the customs procedures, the customs declarant must specify their goods using the 8-digit codes in Section I of Annex II in Chapter 98, and write the codes according to Section II of Chapter 98 by the side.

Article 4. Preferential import tax on imported used cars

1. The motor vehicles for the transport of 15 persons or fewer (including the driver) in Heading 87.02 and 87.03 shall apply the import tax rates prescribed in the Prime Minister’s Decision No. 36/2011/QĐ-TTg dated June 29th 2011, imposing the import tax rates on used motor vehicles for the transport of 15 persons or fewer, and its guiding documents issued by the Ministry of Finance.

2. The preferential import tax rate on motor vehicles for the transport of at least 16 persons (including the driver’s seat) in heading 87.02, and motor vehicles for the transport of goods of which the loaded gross weight does not exceed 5 tonnes in Heading 87.04 (except for refrigerated trucks, garbage collection vehicles having a garbage compressing device, tanker vehicles, armoured cargo vehicles for transporting valuables, bulk-cement trucks, and hooklift trucks) is 150%.

3. The preferential import tax rates on other motor vehicles in the Headings 87.02, 87.03, and 87.04 are 1.5 times of the preferential import tax rates on the new motor vehicles of the same kinds in Headings 87.02, 87.03, and 87.04 in Section I, Annex II – Preferential import tariff according to the list of taxable products enclosed with this Circular.

Article 5. Implementation organization

1. This Circular takes effect on January 01st 2013.

2. This Circular supersedes:

a) The Circular No. 157/2011/TT-BTC dated November 14th 2011 of the Ministry of Finance, specifying the tax rates in the preferential import tariff and the export tariff according to the list of taxable products;

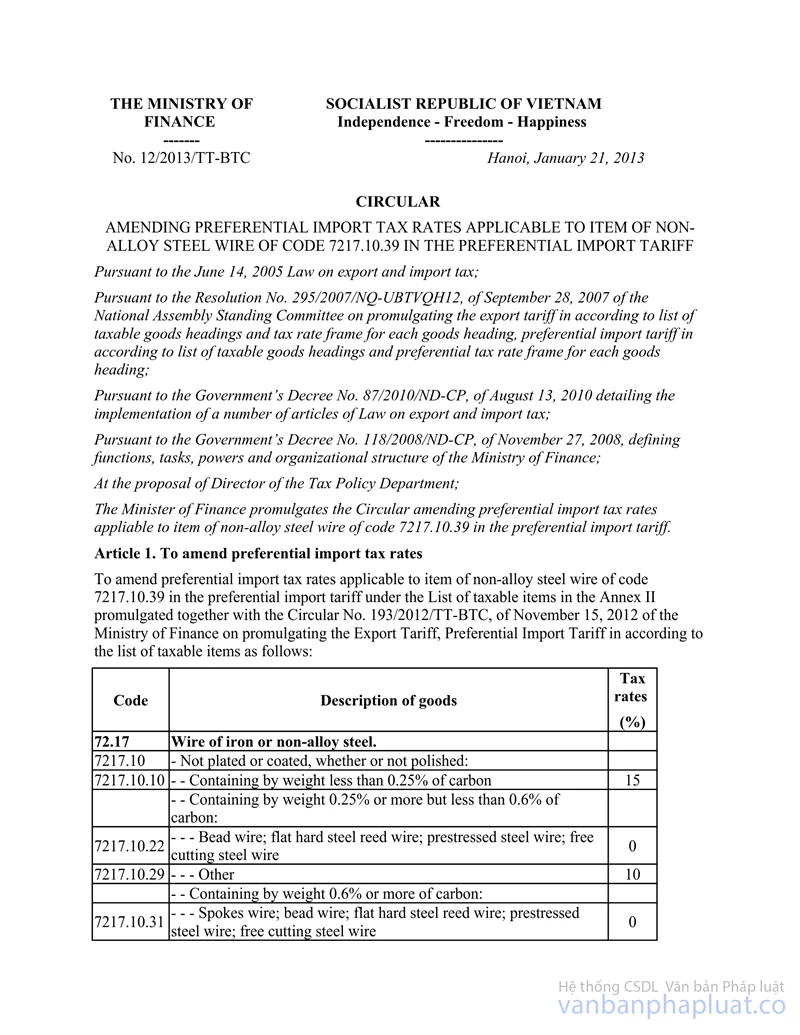

b) The Circular No. 67/2012/TT-BTC dated April 27th 2012 of the Ministry of Finance, adjusting the preferential import tax rates on bars and rods of stainless steel in sub-heading 7222.30.10 in the preferential import tariff;

c) The Circular No. 89/2012/TT-BTC dated May 30th 2012 of the Ministry of Finance, adjusting the preferential import tax rates on coke and semi-coke of coal in heading 2704 in the preferential import tariff;

d) The Circular No. 100/2012/TT-BTC dated June 20th 2012 of the Ministry of Finance, guiding the preferential import tax rates on some liquefied petroleum gases in heading 2711 in the preferential import tariff;

dd) The Circular No. 114/2012/TT-BTC dated July 18th 2012 of the Ministry of Finance, adjusting the preferential import tax rates on coconuts in heading 0801 in the preferential import tariff;

e) The Circular No. 119/2012/TT-BTC dated July 20th 2012 of the Ministry of Finance, amending and supplementing the Circular No. 157/2011/TT-BTC dated November 14th 2011 of the Ministry of Finance, promulgating the preferential import tariff and the export tariff according to the list of taxable products;

g) The Circular No. 148/2012/TT-BTC dated September 11th 2012 of the Ministry of Finance, guiding the preferential import tax rates on some products in heading 2710 in the preferential import tariff;

h) The Circular No. 154/2012/TT-BTC dated September 18th 2012 of the Ministry of Finance, adjusting the preferential import tax rates on the products in heading 2815.11.00 and 2842.10.00 in the preferential import tariff;

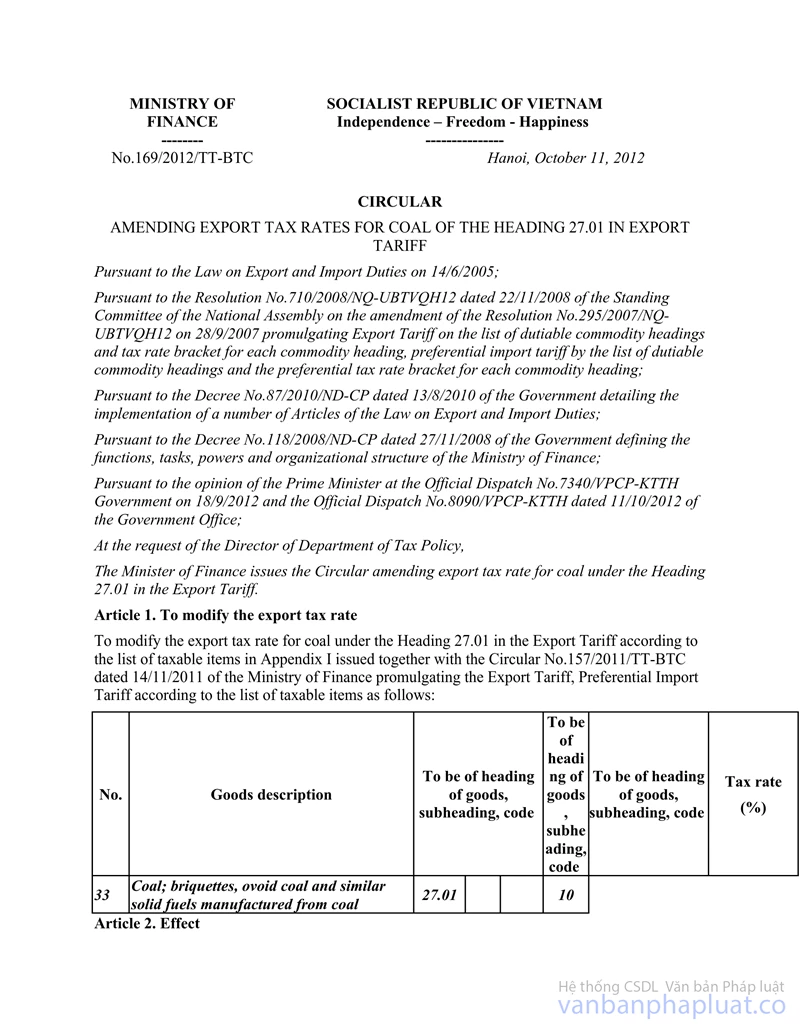

i) The Circular No. 169/2012/TT-BTC dated September 11th 2012 of the Ministry of Finance, adjusting the export tax rates on coal in heading 27.01 in the export tariff;

l) The Circular No. 170/2012/TT-BTC dated October 19th 2012 of the Ministry of Finance, adjusting the preferential import tax rates on the products in heading 3909.10.10 and 3909.20.10 in the preferential import tariff.

m) The Circular No. 208/ 2012/TT-BTC dated November 30th 2012 of the Ministry of Finance, adjusting the preferential import tax rates on aviation spirit in heading 2710 in the preferential import tariff.

n) Other regulations of the Ministry of Finance on preferential import tax and export tax that contradict this Circular.

3. If a relevant document cited in this Circular is amended, supplemented, or replaced during the implementation, the new document shall apply from the date on which it takes effect./.

|

|

FOR THE

MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments