Circular No. 164/2013/TT-BTC export tariff schedule and preferential import tariff schedule đã được thay thế bởi Circular No. 182/2015/TT-BTC preferential import and export tariff và được áp dụng kể từ ngày 01/01/2016.

Nội dung toàn văn Circular No. 164/2013/TT-BTC export tariff schedule and preferential import tariff schedule

|

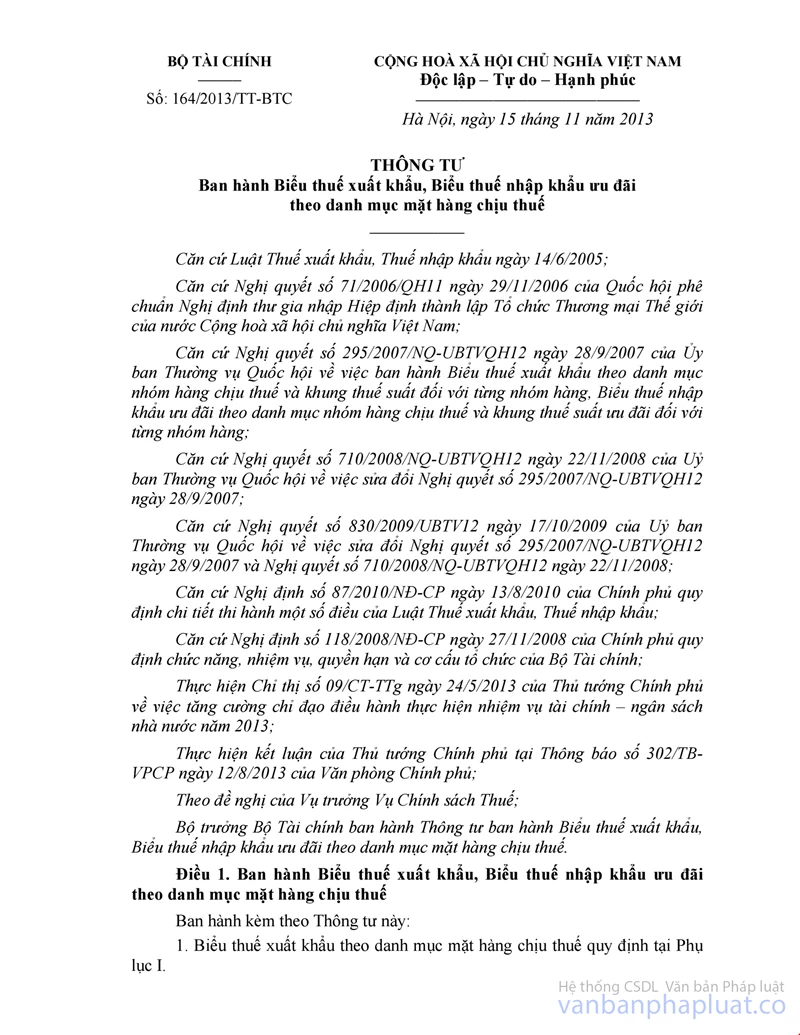

MINISTRY OF FINANCE |

SOCIALIST REPUBLIC

OF VIETNAM |

|

No. 164/2013/TT-BTC |

Hanoi, November 15, 2013 |

CIRCULAR

ON PROMULGATION OF EXPORT TARIFF SCHEDULE AND PREFERENTIAL IMPORT TARIFF SCHEDULE

Pursuant to the Law on Export and import tax dated June 14, 2005;

Pursuant to the National Assembly’s Resolution No. 71/2006/QH11 dated November 29, 2006 on approval for the Protocol on accession of Socialist Republic of Vietnam to the Agreement establishing the World Trade Organization;

Pursuant to the Resolution No. 295/2007/NQ-UBTVQH12 dated September 28th 2007 of the Standing committee of the National Assembly, promulgating the Export tariff according to the list of taxable headings and the tax bracket on each heading, the preferential import tariff according to the list of taxable headings and preferential tax bracket on each heading;

Pursuant to the Resolution No. 710/2008/NQ-UBTVQH12 dated November 22, 2008 of Standing Committee of the National Assembly on amendments to the Resolution No. 295/2007/NQ-UBTVQH12 dated September 28, 2007;

Pursuant to the Resolution No. 830/2009/UBTV12 dated October 17, 2009 of Standing Committee of the National Assembly on amendments to the Resolution No. 295/2007/NQ-UBTVQH12 dated September 28, 2007 and the Resolution No. 710/2008/NQ-UBTVQH12 dated November 22, 2008;

Pursuant to the Government's Decree No. 87/2010/NĐ-CP dated August 13th 2010, detailing the implementation of a number of articles of the Law on Export and import tax;

Pursuant to the Government's Decree No. 118/2008/NĐ-CP dated November 27, 2008, defining the functions, tasks, powers and organizational structure of the Ministry of Finance;

Pursuant to the Prime Minister’s Directive No. 09/CT-TTg dated May 24, 2013 on enhancement of management to fulfill finance - government budget objectives in 2013;

Pursuant to the Prime Minister’s conclusion in the Announcement No. 302/TB-VPCP dated August 12, 2013 of Office of the Government;

At the request of the Director of the Tax Policy Department;

The Minister of Finance promulgates a Circular on promulgation of export tariff schedule and preferential import tariff schedule.

Article 1. Promulgation of export tariff schedule and preferential import tariff schedule

The following tariff schedules are promulgated together with this Circular:

1. Export tariff schedule in Appendix I.

2. Preferential import tariff schedule in Appendix II.

Article 2. Promulgation of preferential import and export tariff schedule

1. Export tariff schedule in Appendix I contain goods description and a code (08 digits), the rate of tax on each article subject to export tax.

2. Where an article is not mentioned in the export tariff schedule, the declarant must provide its pLU code that corresponds to the 8-digit code of such article in the preferential import tariff schedule in Section I of Appendix II promulgated together with this Circular, and write the tax rate of 0%.

3. Export tax on the articles made of imported raw materials:

a) If it is confirmed that goods are entirely made of imported raw material, export duty is exempt. Paint, varnish, and screws on wooden goods are considered ancillary materials.

b) If goods are made of both imported raw materials and domestic raw matierals, export duty on the amount of export goods proportional to the amount of raw materials imported for manufacturing, processing such exported goods shall be exempt. The amount of exported goods made of domestic raw materials shall incur export duty at the rate of export duty on such articles.

c) The application for cancellation of export tax is specified in Clause 2 Article 126 of the Circular No. 128/2013/TT-BTC dated September 10, 2013 of the Ministry of Finance on customs procedure, customs supervision and inspection, export duty, import duty, and tax administration for exported and imported goods.

4. Wood charcoal that belongs to subheading 4402.90.90 must meet the requirements below to apply 5% tax in the export tariff schedule:

|

Criteria |

Requirement |

|

Hardness |

Hard and tough |

|

Ash content |

≤ 3% |

|

Fixed content of carbon element (C) without smell and smoke when set on fire |

≥ 70% |

|

Calorific value |

≥ 7000 Kcal/kg |

|

Sulfur content |

≤ 0.2% |

|

Combustion rate |

≥ 4% |

Article 3. The preferential import tariff schedule in Appendix II consists of:

1. Section I: Preferential import tax rates applied to 97 Chapters of Vietnam’s List of imported goods. The schedule consists of multiple Sections, Chapters, notes; the description of goods (names of headings and articles), their codes (08 digits), and preferential import tax rates are specified in the tariff schedule.

2. Section II: Chapter 98 - Codes and preferential import tax rates on certain special headings and articles.

2.1. Notes and conditions for applying preferential import tax in Chapter 98.

a) Notes of chapter: the articles mentioned in Clause 1 Part 1 Section II of Appendix II to this Circular are eligible for the preferential import tax in Chapter 98.

b) The classification method, the conditions for applying the preferential import tax in Chapter 98, the payment for and use of the goods in Chapter 98 shall comply with Clause 3 Part I Section II of Appendix II to this Circular.

2.2. The list of headings, articles, and preferential import tax include: the codes of the headings and subheadings in Chapter 98; description of goods (names of headings or articles); corresponding codes of the headings and subheadings in Section 1 of Appendix II (97 Chapters in Vietnam’s import tariff schedule) and preferential import tax on goods in Chapter 98 shall comply with specific regulations in Part II Section II of Appendix II to this Circular.

2.3. The headings and articles eligible for preferential import tax in Chapter 98 may apply the preferential import tax rates prescribed in the Circulars on promulgation of special preferential import tariff schedules or separate preferential import tax in Chapter 98 of this Circular.

2.4. During the customs procedure, the declarant shall enumerate goods in accordance with the column “Corresponding code in Section I Appendix II” mentioned in Chapter 98, and write the code in Chapter next to it.

Example: When importing sack kraft paper used for making cement bags, the declarant shall write the code 4804.29.00 (9807.00.00), and preferential import tax rate of 3%.

Article 4. Timetable for application of preferential import tax on some articles in heading 27.07, 29.02 and 39.02

Preferential import tax shall apply to some articles in headings 27.07, 29.02 and 39.02 as follows:

1. From January 01, 2013 to December 31, 2014: preferential import tax rates in Section I in Appendix II to this Circular shall apply.

2. From January 01, 2015 onwards: preferential import tax rates shall apply as follows:

|

HS code |

Description |

Tax rate (%) |

|

|

From January 01, 2015 to December 31, 2015 |

From January 01, 2016 onwards |

||

|

|

|

|

|

|

27.07 |

Oils and other products of the distillation of high temperature coal tar; similar products in which the weight of the aromatic constituents exceeds that of the non-aromatic constituents. |

|

|

|

2707.10.00 |

- Benzene |

2 |

3 |

|

2707.30.00 |

- Xylenes |

2 |

3 |

|

|

|

|

|

|

39.02 |

Polymers of propylene or of other olefins, in primary forms |

|

|

|

3902.10 |

- Polypropylene: |

|

|

|

3902.10.30 |

- - In dispersion |

2 |

3 |

|

3902.10.90 |

- - Other |

2 |

3 |

Article 5. Preferential import tax on used cars

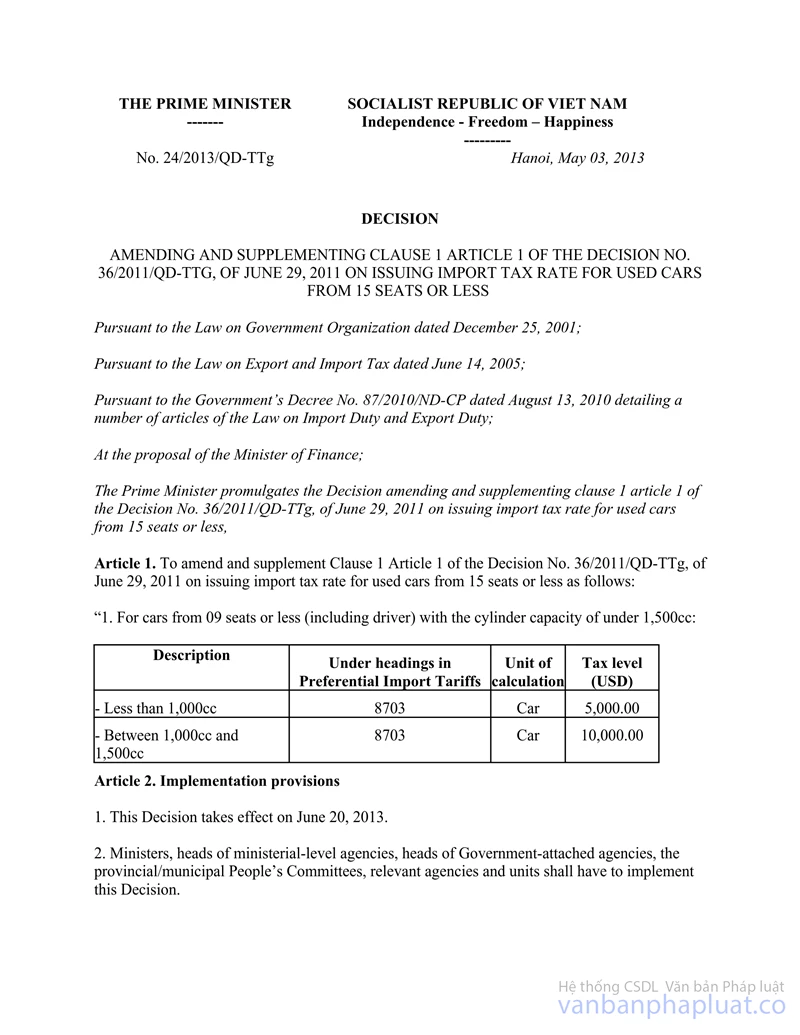

1. Import tax on motor vehicles for the transport of 15 persons or fewer (including the driver) in headings 87.02 and 87.03 is prescribed in the Prime Minister’s Decision No. 36/2011/QĐ-TTg dated June 29, 2011 on imposition of import tax on used motor vehicles for the transport of 15 persons or fewer, the Decision No. 24/2013/QĐ-TTg dated May 03, 2013 on amendments to Clause 1 Article 1 of the Decision No. 36/2011/QĐ-TTg dated June 29, 2011, and the documents on import tax adjustment of the Ministry of Finance.

2. Preferential import tax on motor vehicles for the transport of 16 persons or more (including the driver) in Heading 87.02 and motor vehicles for the goods transport, the gross vehicle weight of which does not exceed 5 tonnes, in Heading 87.04 (except for refrigerated trucks, refuse collection vehicles having a refuse compressing device, tanker vehicles, armored cargo vehicles for transporting valuables, bulk-cement trucks, and hooklift trucks) is 150%.

3. Preferential import tax on other kinds of motor vehicles in Headings 87.02, 87.03, and 87.04 is 1.5 times the preferential import tax on new motor vehicles of the same kinds in Headings 87.02, 87.03, and 87.04 in Section I Appendix II - Preferential import tariff schedule, which is promulgated together with this Circular.

Article 6. Implementation

1. This Circular takes effect on January 01, 2014.

2. The following documents are abrogated:

a) The Circular No. 193/2012/TT-BTC dated November 15, 2012 on promulgation of the export tariff schedule and preferential import tariff schedule.

b) The Circular No. 208/2012/TT-BTC dated November 30, 2012 of the Ministry of Finance on amendments to preferential import tax on aviation spirit and aviation fuel in heading 27.10 in the preferential import tariff schedule.

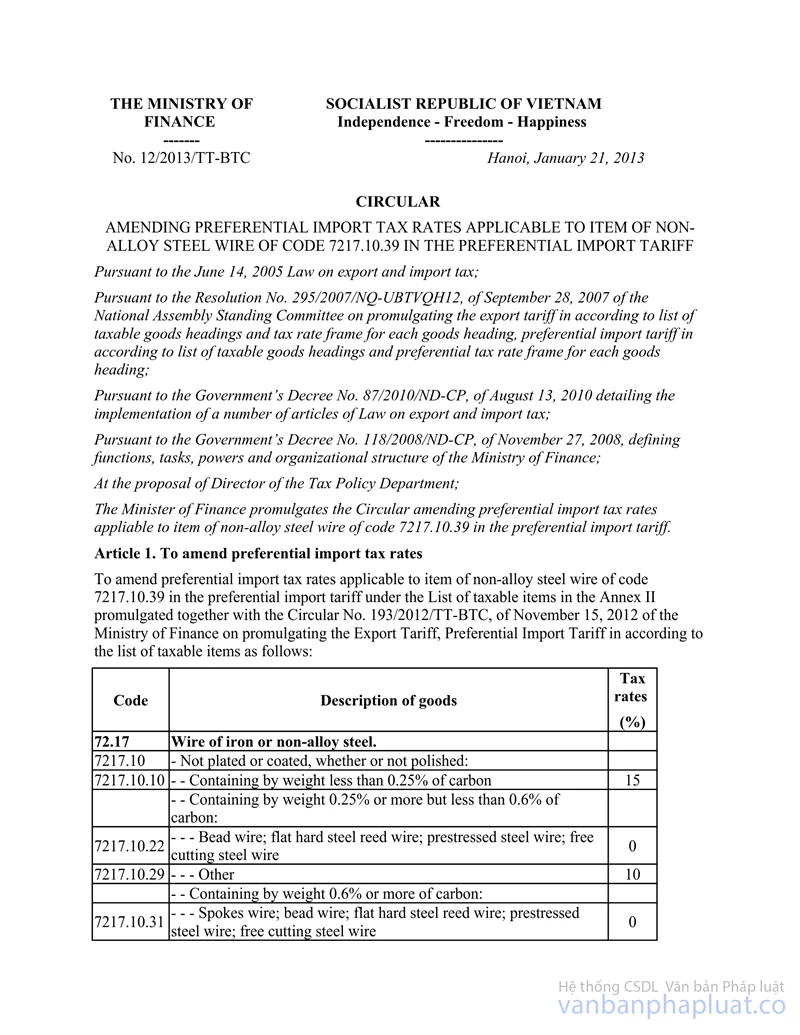

c) The Circular No. 12/2013/TT-BTC dated January 21, 2013 of the Ministry of Finance on amendments to preferential import tax on non-alloy steel in heading 7217.10.39 in the preferential import tariff schedule.

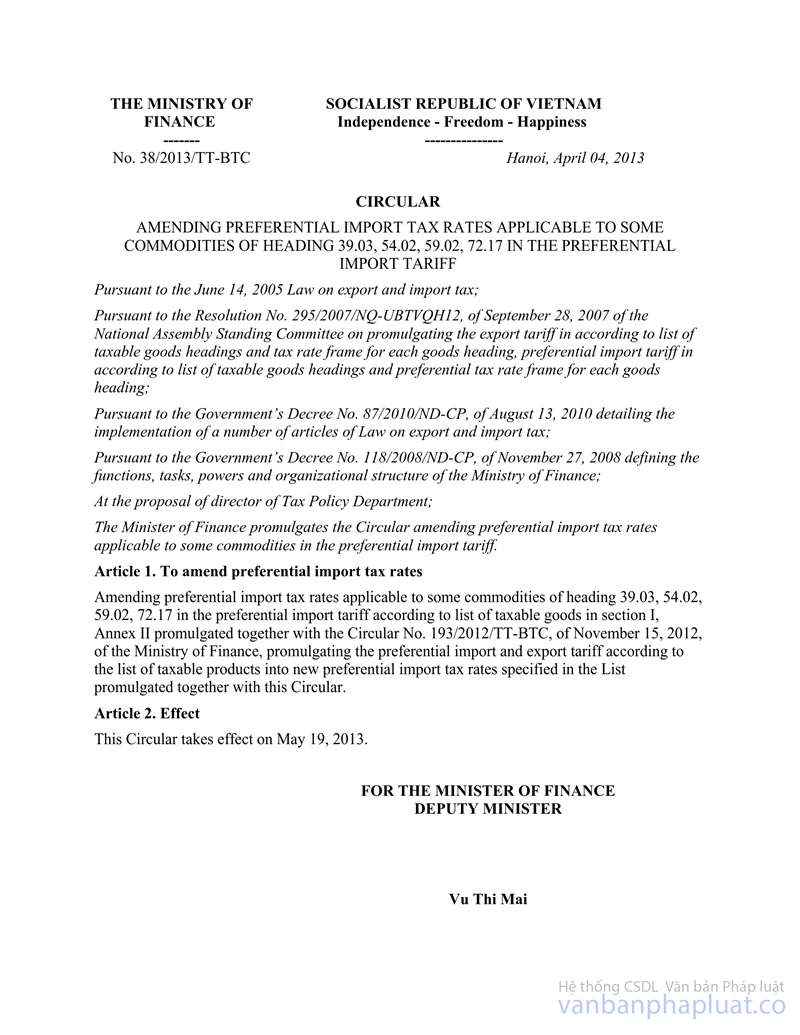

d) The Circular No. 38/2013/TT-BTC dated April 04, 2013 of the Ministry of Finance on amendments to preferential import tax on the articles in headings 39.03, 54.02, 59.02, and 72.17 in the preferential import tariff schedule.

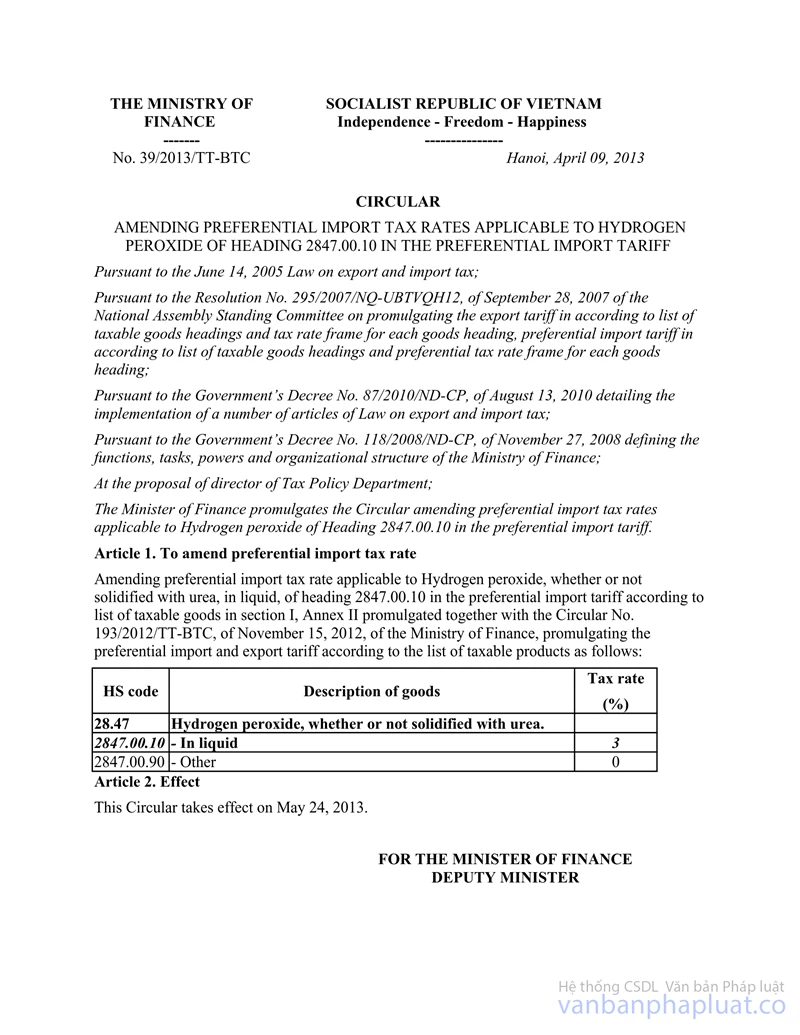

e) The Circular No. 39/2013/TT-BTC dated April 09, 2013 of the Ministry of Finance on amendments to preferential import tax on Hydrogen peroxide in heading 2847.00.10 in the preferential import tariff schedule.

g) The Circular No. 44/2013/TT-BTC dated April 25, 2013 of the Ministry of Finance on amendments to preferential import tax on minerals in the preferential import tariff schedule.

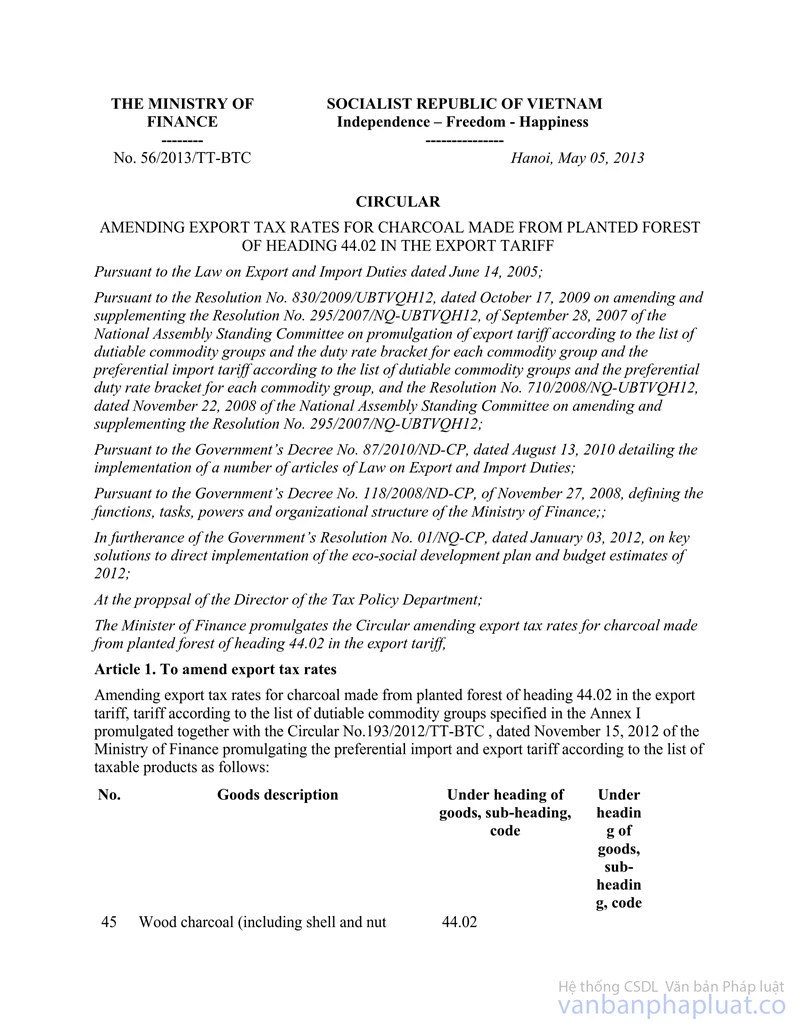

h) The Circular No. 56/2013/TT-BTC dated May 06, 2013 of the Ministry of Finance on amendments to preferential import tax on agglomerated wood in heading 44.02 in the preferential import tariff schedule.

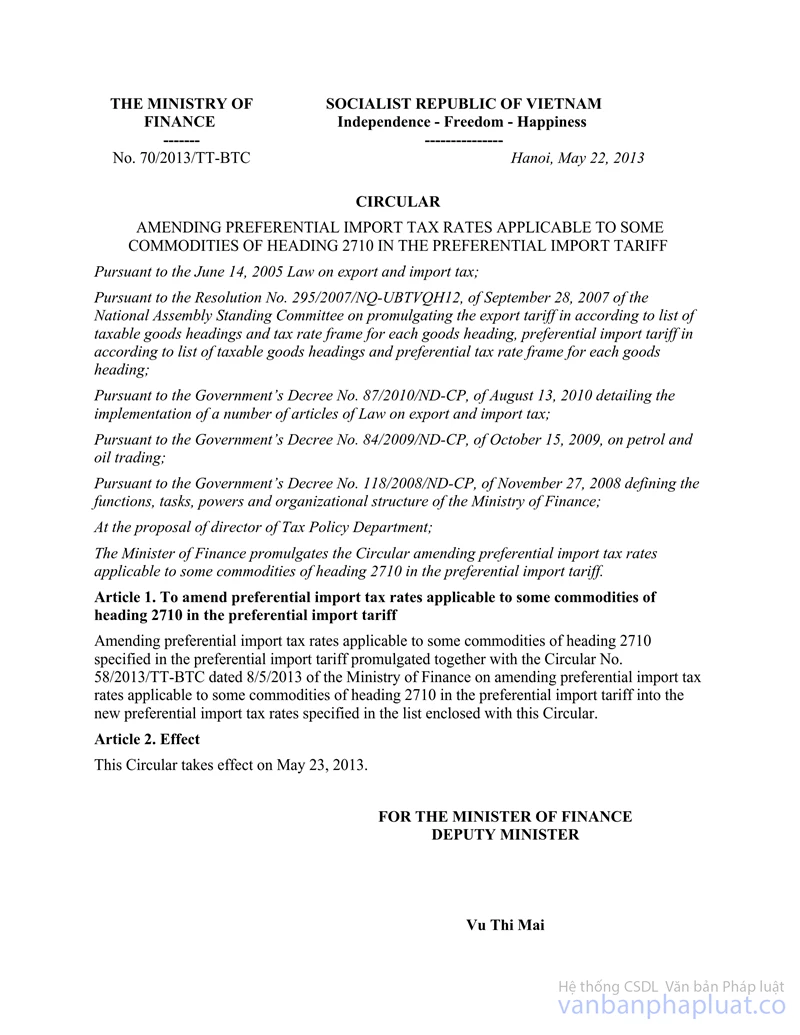

i) The Circular No. 70/2013/TT-BTC dated May 22, 2013 of the Ministry of Finance on amendments to preferential import tax on the articles in heading 27.10 in the preferential import tariff schedule.

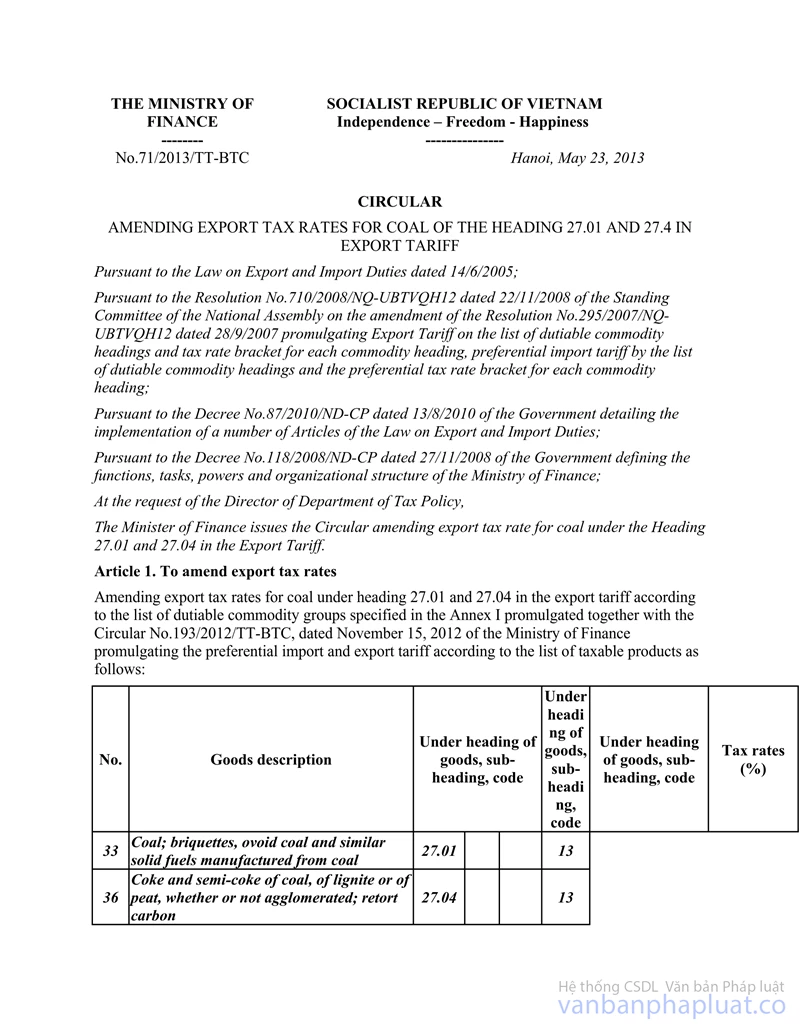

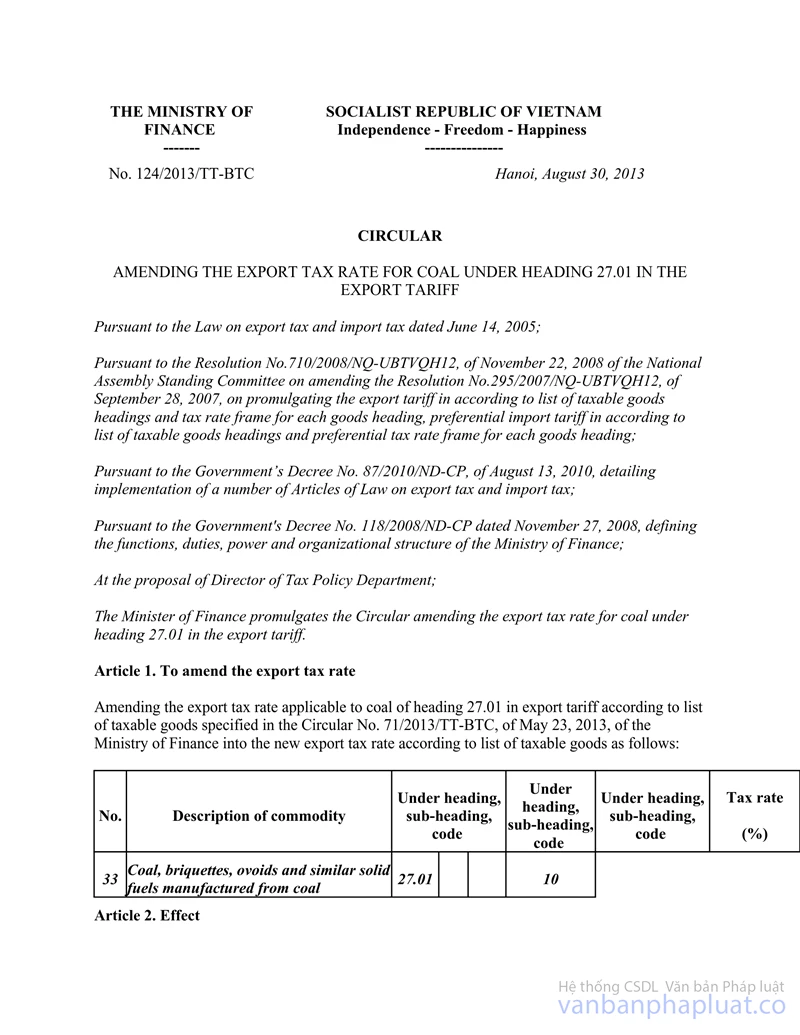

k) The Circular No. 71/2013/TT-BTC dated May 23, 2013 of the Ministry of Finance on amendments to preferential import tax on coal in heading 27.10 in the preferential import tariff schedule.

l) The Circular No. 79/2013/TT-BTC dated June 07, 2013 of the Ministry of Finance on amendments to preferential import tax on some articles in heading 17.02 in the preferential import tariff schedule.

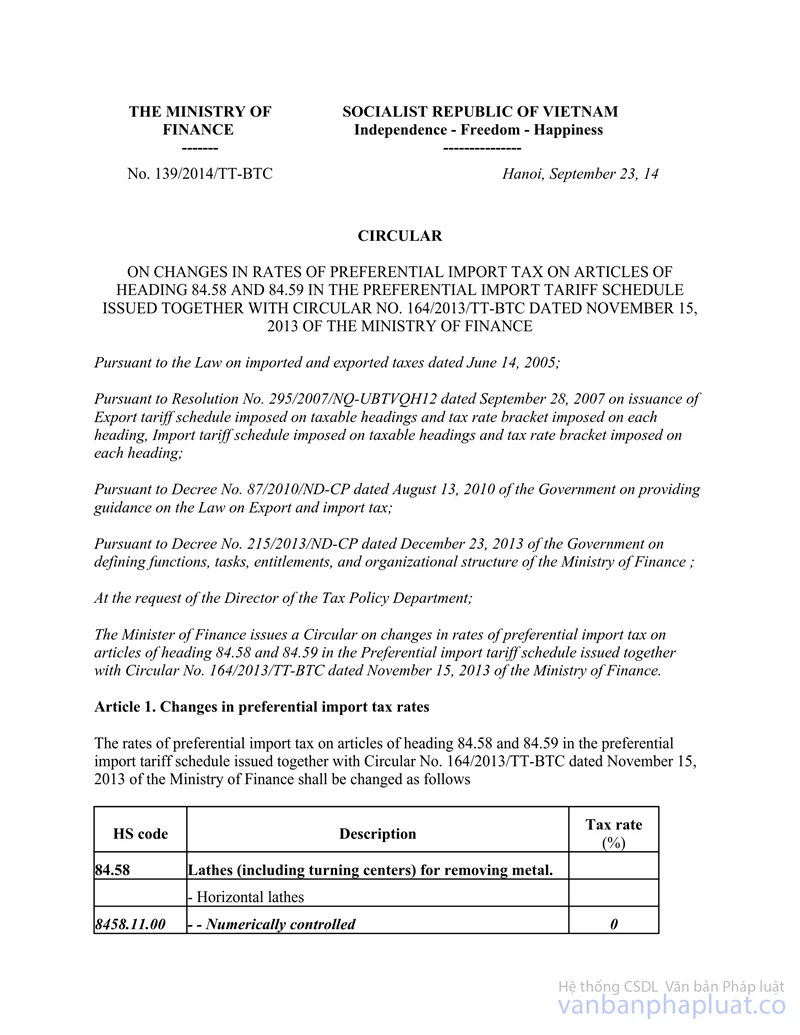

m) The Circular No. 107/2013/TT-BTC dated August 12, 2013 of the Ministry of Finance on amendments to preferential import tax on some articles in headings 27.07, 29.02 and 39.02 in the preferential import tariff schedule.

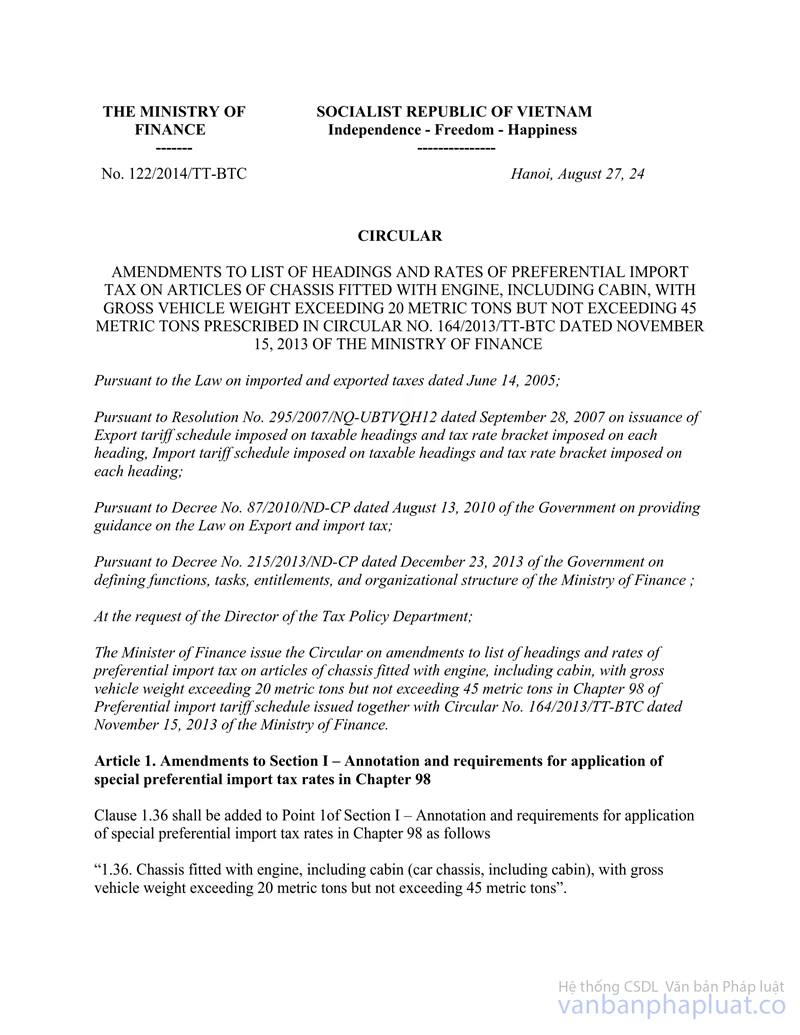

n) The Circular No. 120/2013/TT-BTC dated August 27, 2013 of the Ministry of Finance on amendments to the description of the articles in heading 98.25 in Chapter 98 of the preferential import tariff schedule that is promulgated together with the Circular No. 193/2012/TT-BTC dated November 15, 2012 of the Ministry of Finance.

o) The Circular No. 124/2013/TT-BTC dated August 30, 2013 of the Ministry of Finance on amendments to preferential import tax on some articles in heading 27.10 in the export tariff schedule.

p) The Circular No. 125/2013/TT-BTC dated August 30, 2013 of the Ministry of Finance on amendments to preferential import tax on some articles in headings 2836.30.00, 2916.31.00, 3302.10.90, and 3824.90.70 in the preferential import tariff schedule.

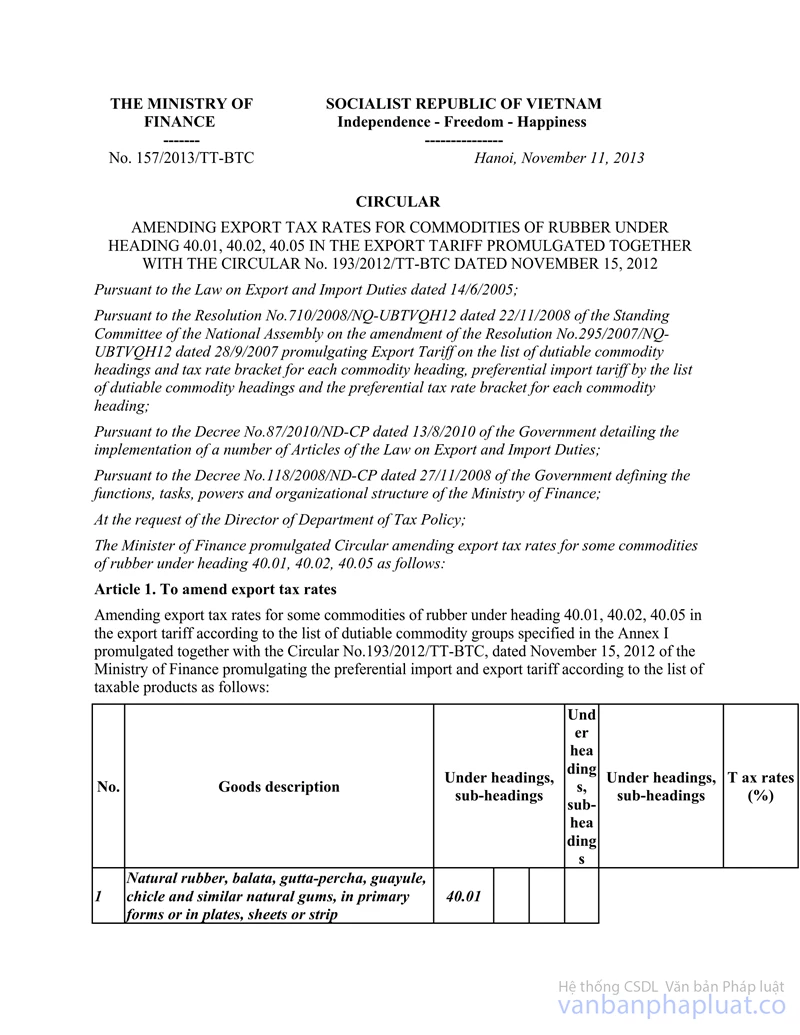

q) The Circular No. 157/2013/TT-BTC dated November 11, 2013 of the Ministry of Finance on amendments to preferential import tax on rubber in headings 40.01, 40.02, and 40.05 in the export tariff schedule that is promulgated together with the Circular No. 193/2012/TT-BTC dated November 15, 2012.

r) Other regulations of the Ministry of Finance on export tax and preferential import tax that contravene this Circular.

3. Where the documents cited in this Circular are amended or superseded, the newer ones shall apply./.

|

|

PP THE MINISTER |

------------------------------------------------------------------------------------------------------

This translation is made by LawSoft,

for reference only. LawSoft

is protected by copyright under clause 2, article 14 of the Law on Intellectual Property. LawSoft

always welcome your comments