Nội dung toàn văn Official Dispatch No. 353/TCT-CS, Guiding the finalization of enterprise income

|

THE MINISTRY OF FINANCE |

SOCIALIST REPUBLIC OF VIETNAM |

|

No. 353/TCT-CS |

Hanoi, January 29, 2010 |

To: Departments of Taxation of central-affiliated cities and provinces.

On June 03, 2008, the National Assembly issued the Law on Enterprise income tax No. 14/2008/QH12 that takes effect on January 01, 2009. The Government also took many measures in 2009 for boosting production and business, sustaining economic growth and ensuring social security. For ensuring the enterprise income tax finalization in 2009 is done in accordance with the Law on Enterprise income tax No. 14/2008/QH12, the Law on Tax administration No. 78/2006/QH11, the Government's Decree No. 124/2008/NĐ-CP dated December 11, 2008, the Circular No. 130/2008/TT-BTC dated December 26, 2008, and relevant legal documents, the General Department of Taxation guides some contents when finalizing enterprise income tax in 2009 as follows:

PART 1: ABOUT GENERAL ENTERPRISE INCOME TAX POLICY.

I. Method of calculating enterprise income tax.

1. For producing or trading organizations (hereinafter referred to as enterprises):

Enterprise income tax amount payable in the tax period equals chargeable income multiplied by tax rate.

|

Enterprise income tax payable |

= |

Chargeable income |

X |

Enterprise income tax rate |

If the enterprise sets up a scientific and technological development fund, the enterprise income tax payable is calculated as follows:

|

Enterprise income tax payable |

= |

( |

Chargeable income |

- |

The science and technology fund |

) |

X |

Enterprise income tax rate |

If the enterprise has paid enterprise income tax or a similar kind of tax outside Vietnam, the enterprise may deduct the paid enterprise income tax, but must not exceed the enterprise income tax payable as prescribed by the Law on Enterprise income tax.

2. The non-business units that provide goods and services subject to enterprise income tax of which the income is identifiable, but the cost is not identifiable nor recorded, the income from such business is calculated as follows:

Enterprise income tax payable (%) on the income from the provision of goods and services:

- For services: 5%;

- For goods trading: 1%

- For other activities: 2%

The non-business units eligible for enterprise income tax incentives that wish to enjoy enterprise income tax incentives must comply with the regulation of accounting and invoices, register and pay enterprise income tax as declared, and not apply the rate of enterprise income tax on stated above when enjoying enterprise income tax incentives.

II- Chargeable income

Chargeable income in the period is calculated using the following formula:

|

Chargeable income |

= |

Taxable income |

- |

Income eligible for tax exemption |

+ |

The transferred loss |

III- Taxable income

Taxable income in a tax period includes income from the business of producing, trading goods and services, and other income.

Taxable income in the tax period is calculated as follows:

|

Taxable income |

= |

Revenue |

- |

Deductible expenses |

+ |

Other income |

Income from the production of business of goods and services equals the revenue from it minus the deductible expenses on it. Enterprises engaged in multiple businesses that apply various tax rates must separately calculate the income from each business corresponding to the tax rate on such business.

Other incomes are taxable incomes in the tax period prescribed in Section V, Part C of the Circular No. 130/2008/TT-BTC Other income is subject to the common tax rate (25%) and not eligible for preferential tax rates.

IV– Revenue for calculating tax

1. The revenue for calculating taxable income (hereinafter referred to as assessable revenue) is the money from the sale of goods, processing, or provision of services, including subsidies and surcharges for which the enterprise is eligible, whether or not they have been collected.

- The revenue for calculating tax of enterprises paying tax using the deduction method is the revenue without VAT.

Example: Enterprise A pays tax using the deduction method. The VAT invoice contains the following figures:

Sale price: 100,000 VND.

VAT (10%): 10,000 VND.

Total amount: 110,000 VND.

The revenue for calculating taxable income is 100,000 VND.

- The revenue for calculating tax of enterprises directly paying tax on the added value is the revenue including VAT.

Example: Enterprise B directly pays tax on the added value. The sale invoice only state the sale price being 110,000 VND (included VAT)

The revenue for calculating taxable income is 110,000 VND.

2. The time for determining the revenue for calculating taxable income is determined as follows:

a) For goods sale, the time for determining the revenue for calculating taxable income is the time of transferring the right to own and use goods to the buyer.

b) For services provision, the time for determining the revenue for calculating taxable income is the time of finishing the provision of services for the buyer.

V– Deductible expenses and non-deductible expenses when calculating taxable income.

When calculating taxable income, expenses are deductible when the following conditions are satisfied:

- The actual expenses on the production and business of the enterprise.

- The expenses come with valid invoices and documents as prescribed by law.

The non-deductible expenses are expenses that do not satisfy the conditions stated above, and the expenses specified in Clause 2 Section IV, Part C of the Circular No. 130/2008/TT-BTC.

The deductible expenses and 31 non-deductible expenses when calculating taxable income are specified in the Law on Enterprise income tax and its guiding documents. When calculating taxable income and some expenses, apart from referring to legal documents determined the deductible expenses, the enterprises must follow the guidance below:

1. Expenses on depreciation of fixed assets:

From January 01, 2009 until the end of December 31, 2009, the Circular No. 130/2008/TT-BTC and the Decision No. 206/2003/QĐ-BTC dated December 12, 2003 of the Minister of Finance shall apply.

- When starting to depreciate fixed assets, the enterprise must register the method of depreciation that they choose with the direct tax authorities. Annually, the enterprise shall determine the depreciation of fixed assets according to current provisions of the Ministry of Finance applicable to the management, use, and depreciation of fixed assets, including quick depreciation. During the operation, a enterprise may change the depreciation rate within the prescribed limit. The deadline of changing the depreciation rate is the deadline of submitting the enterprise income tax finalization declaration of the year of depreciation.

- The depreciation of fixed assets being cars for human with 9 seats or fewer, civil plans, and cruisers:

The following amounts are not considered deductible expenses: the depreciation corresponding to the input value that exceed 1.6 billion VND/car, applicable to cars that have been just registered and depreciated from January 01, 2009 (except for cars serving passenger transport, tourism, and hotel); the depreciation of fixed assets being civil planes and cruisers not serving goods transport, passenger transport, or tourism.

Example 1: In 2009, enterprise A purchases a 7-seat car for 2 billion VND, excluding VAT, with valid invoices as prescribed. According or the provisions above, enterprise A may only add fixed asset depreciation to the expenses when calculating taxable income according to the input value of the car at a limited rate being 1.6 billion VND.

Example 2: In 2009, enterprise B purchases a 7-seat car for 1.5 billion VND, VAT = 75 million VND, the registration fee is 100 million VND. Enterprise B purchases this car by cash without paying through banks, thus the input VAT is not deducted and shall be added to the input value of fixed assets. The total input value of this car is 1.675 billion VND (1.5 + 0.075 + 0.1). Enterprise B may only add the fixed asset depreciation to the expense when calculating taxable income according to the input value of the car at a limited rate being 1.6 billion VND.

- Depreciation of constructions on leased land:

For constructions on land such as office buildings, factories, or stores serving the production and business that are built on land leased or lent by other organizations, individuals or households (the land is not leased by the State or industrial zones, Hi-tech zones, export processing zones), the enterprise may only add the depreciation to the deductible expenses on these constructions if the following conditions are satisfied:

+ The notarized land lease or land lending contract as prescribed by law; the leasing or lending period in the contract must not be shorter than the minimum period of fixed asset depreciation.

+ The invoices of the handed over constructions enclosed with the building contract, contract liquidation, calculating construction value, address and tax codes of the enterprise.

+ The constructions on land are managed, monitored and recorded in accordance with current provisions on fixed asset management.

2. Registering the reasonable consumption of materials, fuel, energy and goods used in the production and business:

The reasonable consumption of materials, fuel, energy and goods used in the production and business is set be the enterprise. The reasonable consumption is set at the beginning of the year or the beginning of the production period, and sent to the direct tax authorities within 3 months as from the commencement of the production. The deadline for sending the notification of the amendment and supplementation of the reasonable consumption is the deadline for submitting the enterprise income tax finalization declaration.

3. Expenses on salaries:

- The following payments are added to the expense when calculating taxable income: salaries, remunerations and benefits paid to employees as prescribed by law; the bonuses paid to employees as part of their salaries of which the conditions are specified in the labor contract or collective labor agreement. An enterprise may set up a reserve fund not exceeding 17% of the current salary fund to supplement the salary fund of the succeeding year in order to ensure that the salary payment is uninterrupted as long as such fund is not used for other purposes.

- The enterprise must not include the expenses on tuition of employees’ children written in labor contracts to deductible expenses.

4. Expenses on breaking meals:

The expenses on meals may be included in deductible expenses if such expenses have valid invoices as prescribed by law.

For State-owned company, according to the Circular No. 22/2008/TT-BLĐTBXH dated October 15, 2008 (valid until April 30, 2009) and the Circular No. 10/2009/TT-BLĐTBXH dated April 24, 2009 (take effect on May 01, 2009) of the Ministry of Labor, War Invalids and Social Affairs, guiding the regulation on breaking meals in State-owned company, the expense on the breaking meals for employees must not exceed 450,000 VND/month before May 1, 2009, and must not exceed 550,000 VND/month from May 1, 2009. If a State-owned company is allowed to pay for breaking meals beyond the limit stated above, and the expenses on the meals have valid invoices as prescribed by law, such expenses shall be deducted when calculating taxable income.

5. Expenses on clothing:

The following expenses are not deductible: the expenses in kind on clothing of employees that exceed 1,500,000 VND/person/year; the expenses in cash on clothing to employees that exceed 1,000,000 VND/person/year.

6. The following expenses are not deductible: the allowance given to employees going on business trips domestically and overseas (not including expenses on traveling and accommodation) that exceed 2 times of the limit applicable to the State’s officers and public employees as prescribed by the Ministry of Finance.

The expenses on the allowance for domestic and overseas business trips given to the State officers and public employees must comply with the following documents:

- Domestic trips: the Circular No. 23/2007/TT-BTC dated March 21, 2007 of the Ministry of Finance;

- Overseas trips: the Circular No. 91/2005/TT-BTC dated October 18, 2005 of the Ministry of Finance;

7. Expenses on interest payment:

The following expenses are not deductible: the payment for the interest of on capital loan taken from subjects not being credit institutions or economic organizations that exceed 150% of the basic interest rate announced by the State bank of Vietnam at the time of taking the loan. The expense on the interest on the loan taken to contribute to the charter capital corresponding to the missing portion of the registered charter capital written in the company’s charter, even the enterprise has commenced their business.

Example: Enterprise A registers their charter capital = 90 billion. The charter of enterprise A stipulates that such charter capital shall be contributed within a certain period of time (3 years, 30 billion VND each year). Enterprise A contributes the charter capital in accordance with the registered contribution schedule being 30 billion VND per year, and pays the interest on the capital loan. Such interest payments come with valid invoices and do not exceed the limit. Then, such payment shall be included in the expense when calculating taxable income.

In the same example, but enterprise A fails to contribute the charter capital in accordance with the registered contribution schedule being 30 billion VND per year, the payment for the interest on the capital loan corresponding to the missing charter capital according to the registered contribution schedule shall not be included in the expense when calculating taxable income.

8. The provision against devaluation of goods in stock, provision against the loss of financial investment, provision against bad debts, provision against warranty of products, goods and constructions shall be made and use in accordance with the Circular No. 228/2009/TT-BTC dated December 07, 2009 of the Ministry of Finance.

Provision for securities investment:

a) The subjects of provision are the securities that satisfy the following conditions:

- The securities legally invested by the enterprise.

- The securities are free to trade on the market of which the market price is decreasing compared to that recorded in the accounting books at the time of making Financial statements.

The securities banned from free trading on the market such as securities restricted from transfer as prescribed by law, and treasury stock are banned from provision against devaluation

The organizations that register to do securities business such as securities companies, fund management companies, that are established and operated in accordance with law provisions on securities, the provisions against securities devaluation shall comply with separate provisions.

b) Method of making provisions:

The provision against securities investment devaluation is calculated as follows:

|

The provision against securities investment devaluation |

= |

The amount of devaluated securities at the time of making the Financial statement |

x |

The securities price recorded in the accounting books |

- |

The actual securities price on the market |

- For listed securities: the actual securities price on the market according to the Stock Exchange of Hanoi is the average transaction price in the day of making provisions; the Stock Exchange of Ho Chi Minh city is the closing price in the day of making provisions.

- For unlisted securities on the securities market, the actual securities price is calculated as follows:

+ For companies that have registered to trade on the market of unlisted public companies, the actual securities price on the market is the average transaction price of the market on the day of making provisions.

+ For company that have not registered to trade on the market of public companies, the actual securities price on the market is the average price according to the transaction prices provided by at least 03 securities companies at the time of making provisions.

If the market value of the securities is not identifiable, the enterprise must not make provisions against devaluation of securities prices.

- For securities being delisted or suspended from the sixth transaction day and later, it is the value in books on the nearest day of making the Balance sheet.

The enterprise must make separate provisions for each kind of investment securities that are devaluated at the time of making the Financial statement, and include them in the list of provision against investment securities devaluation as the basis for recorded to the financial expenses of the enterprise.

9. Payments to unemployment insurance funds of enterprises:

According to the Law on Social insurance, the Government's Decree No. 127/2008/NĐ-CP dated December 12, 2008, detailing the implementation of the Law on Social insurance applicable to unemployment insurance, taking effect on January 01, 2009, and the Circular No. 130/2008/TT-BTC of the Ministry of Finance:

The sources of unemployment insurance funds according to Article 102 of the Law on Social insurance:

- Payments for unemployment insurance made by employees being 1% of their monthly salaries.

- Payments made by the employer being 1% of salary funds for paying unemployment insurance of the employees participating in unemployment insurance.

- Supports from the State budget being 1% of salary funds for paying unemployment insurance of the employees participating in unemployment insurance, transferred once per year.

The payments for unemployment insurance made by enterprise as prescribed above are compulsory insurance. The enterprise may include it to the deductible expenses when calculating enterprise income tax (1% of salaries).

10. Making and using the provisions for redundancy pay and severance pay:

In 2009, if an enterprise pays unemployment insurance for employees and make provisions against redundancy pay in accordance with current regulation, such payments may be included in deductible expenses when calculating enterprise income tax.

The provisions for redundancy pay and severance pay must comply with the Circular No. 82/2003/TT-BTC dated August 14, 2003 of the Ministry of Finance, on making, managing, using, and recording Provisions for redundancy pay of enterprises.

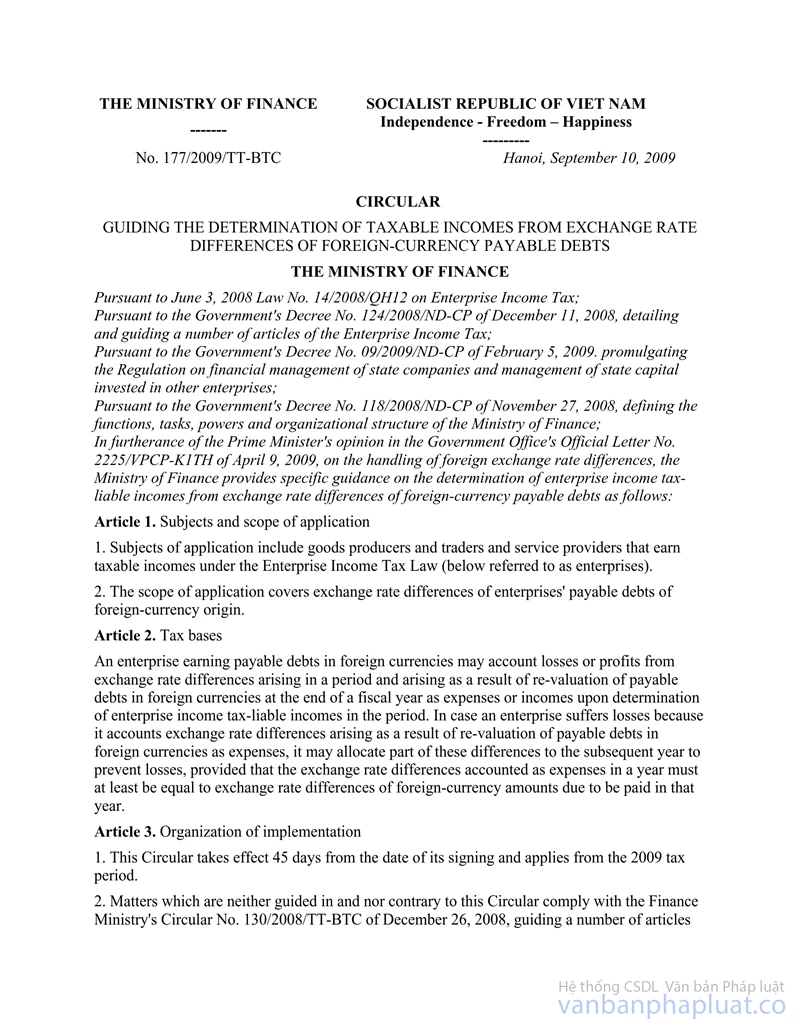

11. Exchange rate differences:

According to the Circular No. 177/2009/TT-BTC dated September 10, 2009 of the Ministry of Finance: for enterprises having debts payable in foreign currencies, the losses on the exchange rate differences in the period, and the losses on exchange rate differences when reassess the debts payable in currencies at the end of the fiscal year, shall be included in the expense when calculating taxable income in the period. In case the business of the enterprise is at a loss when including the exchange rate differences when reassessing the debts payable in foreign currencies in the expense, the enterprise may distribute part of the exchange rate difference to the succeeding year so that the enterprise does not suffer loss, but the exchange rate difference included in the expense of a year must at least equal the exchange rate difference of the foreign currency amount payable in that year.

Example 1: In 2009, the final income of enterprise A is 300 million VND, including the exchange rate differences when reassessing the debts payable in foreign currencies at the end of the fiscal year.

In 2009: the exchange rate difference when reassessing the debts payable in foreign currencies at the end of the fiscal year is -250 million VND, including -100 million VND of debts payable in foreign currencies.

Consequently, enterprise A in 2009 may include the losses on the exchange rate differences when reassessing the debts payable in foreign currencies at the end of the fiscal year being 250 million VND in the expense.

Example 2: In 2009, the taxable income of enterprise B is 200 million VND, including the exchange rate differences when reassessing the debts payable in foreign currencies at the end of the fiscal year.

In 2009: the exchange rate difference when reassessing the debts payable in foreign currencies at the end of the fiscal year is -250 million VND, including -100 million VND of debts payable in foreign currencies.

Consequently, if enterprise B shall be at a loss if it includes all the exchange rate differences when reassessing the debts payable in foreign currencies at the end of the fiscal year in the expense. The exchange rate differences shall be included in the expense when calculating taxable income in 2009 as follows:

- The exchange rate difference of the due debts in foreign currencies in 2009 is -100 million VND (enterprise A must include this amount in the expense of the period)..

- The maximum exchange rate difference when reassessing the undue debts payable in foreign currencies at the end of the fiscal year, that may be included in the expense is -100 million VND.

12. The following expenses are not deductible: expenses on advertising, marketing, promotions, brokerage commissions; expenses on receptionists and conventions; expenses on support for marketing, expenses, payment discount; expenses on complimentary publications of the press agency directly related to the production and business that exceed 10% of the total deductible expense. For newly established enterprises, it is the amount that exceed 15% within the first 3 years as from the establishment. The total deductible expense does not include the limited expenses prescribed in this Point. For commercial activities, the total deductible expense does not include the purchase price of the goods being sold.

The limited expenses on advertising, marketing, promotions, and brokerage commission stated above do not include insurance brokerage commission as prescribed by law provisions on insurance business; commission paid to agents that sell at the right prices; the expenses on market research: surveying, interviewing, collecting, analyzing, and assessing information; expenses on the market research support and development; expenses on market research consultancy; expenses on the display and introduction of products; expenses on commercial fairs and exhibitions; expenses on showrooms; expenses on materials and stuff that supports the display and introduction of products; expenses on the transport of displayed and introduced products.

The limited rate of 15% in the first 3 years is only applicable to new enterprises that have been issued with the Certificate of business registration from January 01, 2009, and not applicable to enterprises established from consolidation, merger, division, separation, or transformation of for or ownership.

Example: In 2009, the company A established in 2008 makes the enterprise income tax finalization report that contains the following expenses:

- The expenses on advertising, marketing, promotions, brokerage commissions; expenses on receptionists and conventions; expenses on support for marketing, expenses, payment discount; expenses on complimentary publications of the press agency directly related to the production and business that come with valid invoices: 250 million VND.

- The total deductible expense (excluding the expenses on advertising, marketing, promotions, brokerage commissions; expenses on receptionists and conventions; expenses on support for marketing, expenses, payment discount; expenses on complimentary publications of the press agency directly related to the production and business): 2 billion VND.

The deductible expenses on advertising, marketing, promotions, brokerage commissions; expenses on receptionists and conventions; expenses on support for marketing, expenses, payment discount; expenses on complimentary publications of the press agency directly related to the production and business being included in the maximum limited expense is:

2 billion VND multiplied by (x) 10% equal (=) 200 million VND

The total deductible expense included in the expense of 2009 is:

2 billion VND plus (+) 200 million VND equal (=) 2.2 billion VND

13. The following expenses are deductible: the payment for social

insurance and health insurance funds, the expenses on the Union that do not

exceed the prescribed limit. The contribution to the managerial budget,

contribution to the association funds as prescribed by law that do not exceed

the prescribed limit.

14. The following expenses are not deductible: the expenses that are not corresponding to the assessable revenue, the periodic accrued expenses that are not spent or completely spent at the end of the period. The accrued expenses include: expenses on periodic major repair of fixed assets, accrued expenses on the activities of which the revenue has been recorded, but the contractual obligation is not completely fulfilled, and other accrued expenses.

Therefore, the following expenses are deductible: the expenses that are corresponding to the assessable revenue, as long as such expenses come with valid invoices as prescribed; the periodic accrued expenses.

Example 1: the company A writes a software program for the company B, but the software service package is not complete. The company A has collected money and recorded the assessable revenue, but the expenses corresponding to the recorded revenue have not completely arisen. The unit may include in advance the expenses corresponding to the declared revenue when calculating taxable income in order to comply with the principles of expenses corresponding to assessable revenue when calculating taxable income.

Example 2: the company B sells air tickets to their clients in December 2009, but their clients do not fly until February 2010. The company A has issued invoices to their clients and recorded the assessable revenue in 2009, but the expenses corresponding to the recorded revenue have not completely arisen; the unit may include the expenses corresponding to the declared revenue when calculating taxable income.

15. Expenses on fines:

The following expenses are not deductible: the fines for administrative violations, including: violations of traffic rules, violations of regulations on business registration, violations of accounting and statistics regulations, violations of tax laws, and fines for other administrative violations as prescribed by law.

The expenses on fines and compensations for violations of economic contracts do not belong to the fines stated above. If such fines come with valid invoices as prescribed, they shall be included in deductible expenses when calculating taxable income.

16. Taxes:

- Personal income tax that is not included in deductible expenses when calculating taxable income is the tax deducted from the income of tax payers to pay to the State budget. If the labor contract stipulates that the salary paid to the employee does not include personal income tax, the personal income tax paid by the enterprise on the employee’s behalf is the expense on salaries, and shall be included in deductible expenses when calculating taxable income.

- Enterprise income tax (foreign contractor's tax) paid on behalf of foreign contractors is included in deductible expenses when calculating taxable income if the revenue received by foreign contractors and sub-contractors does not include enterprise income tax as agreed in the contract.

VI– Other incomes.

Other incomes are prescribed in Section V, Part C of the Circular No. 130/2008/TT-BTC Some further notices:

- According to the Circular No. 177/2009/TT-BTC dated September 10, 2009 of the Ministry of Finance: if an enterprise that has debts payable in foreign currencies, the exchange rate differences in the period and the interest on exchange rate differences when calculating the debts payable in foreign currencies shall be included in the expense when calculating taxable income.

- The income from fines and compensation paid by the parties that violate economic contracts shall be included in other incomes. When an enterprise have both receipts from fines for economic contract violations and expenses on economic contract violations, the difference between the receipts from fines and expenses on fines shall be included in other incomes when calculating taxable income.

Enterprises having expenses on fines and compensation for economic contract violations must comply with Point 14 in Section V above.

- The receipts from deposit interest and interest on deferred payment are included in other incomes when calculating taxable income. If an enterprise has expenses on deposit interest related to the production and business, such expenses shall be included in operational expense in the period.

- Convert the provisions against devaluation of goods in stock, provisions against loss on financial investments, provisions against bad debt receivable, and provisions for the warranty of products, goods and constructions that were made but have not been used or not been completely used at the end of the period into other incomes when calculating taxable income.

- The receipts in cash or in kind from sponsorships are included in other incomes when calculating taxable income.

If the organization receives a sponsorship for education, scientific research, cultures, arts, charity, or other social activities in Vietnam, such incomes are exempted from tax and shall be deducted when calculating chargeable income.

VII– Tax-free income

1. Income from farming, breeding, or aquaculture of organizations established under the Law on Cooperatives.

2. Income from providing technical services directly serve agriculture, including: irrigating, plowing and raking, dredging, pest control, harvesting services.

3. Income from the performance of scientific research and technology development contracts; income from the sale of products during the experimental production period, and in come from the sale of products from new technologies applied in Vietnam for the first time. The tax exemption period must not exceed 01 year as from the commencement date of the scientific research and technology development contract; the commencement day of the experimental production; the commencement day of applying the new technology.

3.1. Income from the performance of scientific research and technology development contracts must satisfy the following conditions:

- Having scientific research registration certificate;

- Being certified by competent State management agencies in charge of science;

3.1. Income from the sale of products from the new technology which is applied in Vietnam for the first time is exempted from paying tax as long as such technology is applied in Vietnam for the first time, and certified by competent State management agencies in charge of science.

4. Income from the production and provision of goods and services of enterprises of which the average number of employees being the disabled, detoxified people, or HIV sufferers in a year account for at least 51 % of the total average number of employees in a year.

Example: enterprise A has 290 employees according to the payroll of January 2009; in April 2008, the enterprise employs 12 people; 2 employees quit in October, 3 employees quit in December. The average number of employees in 2009 is calculated as follows:

|

290 + |

(12 people x 9 months) – (2 people x 3 months) - (3 people x 1 month) |

|

12 |

= 290 employees + 8 employees = 298 employees

The average number of employees in 2009 of enterprise A is 298. If at least 151 people therein are the disabled (298 x 51%), the income from the production or provision of goods and services of enterprise A is tax-free.

- The tax-free income prescribed in this Clause does not include other incomes.

- The tax-free income of the enterprises prescribed in this Point must satisfy the following conditions:

4.1. For enterprises employing the disabled and invalids, the number of disabled employees must be certified by competent health agencies.

4.2. The enterprises employing detoxified people must present the detoxification certificates issued by the detoxification centers or certification from competent agencies.

4.3. For enterprises employing HIV sufferers, the number of employees being HIV sufferers must be certified by competent health agencies.

5. Income from vocational training provided for ethnics, the disabled, impoverished children, and offenders If there are other subjects in the same vocational training facility, the tax-free income is proportional to the number of students being for ethnics, the disabled, impoverished children, and offenders.

The tax-free income from the provision of vocational training prescribed in this Point must satisfy the following conditions:

- The vocational training facility must be established and operated in accordance with legal documents on vocational training.

- Having the list of students being ethnics, the disabled, impoverished children, and offenders

6. The income distributed from the distribution, stock purchase, economic cooperation with domestic enterprises, after the contribution receiver, the stock issuer, and the cooperation partner has paid enterprise income tax as prescribed by the Law on Enterprise income tax, even the contribution receiver, stock issuer, or cooperation partner is eligible for tax exemption or reduction.

Example: enterprise B receives capital contribution from enterprise A. The pre-tax income of enterprise A corresponding to its contribution in enterprise B is 100 million VND.

- Situation 1: enterprise B is not eligible for enterprise income tax incentives, and it has paid the enterprise income tax, including the income of enterprise A. The income that enterprise A receives from the contribution is 75 million VND [(100 million VND – (100 million VND x 25%)], that 75 million VND of enterprise A is exempted from enterprise income tax.

- Situation 2: enterprise B is eligible for 50% reduction of the enterprise income tax payable, and it has completely paid the enterprise income tax, including the income of enterprise A. The income that enterprise A receives from the contribution is 87.5 million VND [(100 million VND – (100 million VND x 25% x 50%)], that 87.5 million VND of enterprise A is exempted from enterprise income tax.

- Situation 1: enterprise B is eligible for tax exemption. The income that enterprise A receives from the contribution is 100 million VND. That 100 million VND of enterprise A is exempted from enterprise income tax.

7. The sponsorships for education, scientific research, cultures, arts, charity, or other social activities in Vietnam.

If the sponsorship receiver does not properly use such sponsorships, it must calculate and pay enterprise income tax at the rate of 25% of the amount being used improperly.

The sponsorship receivers prescribed in this Clause must be established and operated in accordance with laws, and must comply with law provisions on accounting and statistics.

VIII– Guidance on calculating losses and transferring losses.

The losses arising in a tax period is the negative difference of taxable income.

If an enterprise suffers losses after finalizing tax, it may transfer the losses in the finalized year and deduct it from the taxable income of the succeeding years. The loss transfer period must not exceed 5 consecutive years, starting from the year succeeding the loss-arising year.

For the losses arising in 2009 and later, the transfer period must not exceed 5 consecutive years, starting from the year succeeding the loss-arising year. The losses arising before 2009 shall be transferred as prescribed in the legal documents at that time. If the losses are not completely transferred until 2009, the loss transfer period still continues.

If the loss that the enterprise may transferred by the enterprise is different from that calculated by the enterprise, according to the inspection from competent agencies, the conclusion made by competent agencies shall apply, but the loss transfer period must not exceed 5 years, as from the year succeeding the loss-arising year.

After 5 years as from the year succeeding the loss-arising year, if the loss is not completely offset, it shall not be deducted from the income of the succeeding years.

Example: the total loss of enterprise A in 2008 is 5 billion VND, and it is transferred for 5 consecutive years. In 2009, when finalizing tax, enterprise A declares the chargeable income (interest) being 1 billion VND, and it transfers the loss of 1 billion VND in 2008 to the chargeable income in 2009. When inspecting the enterprise income tax finalization in 2009, the tax authorities finds that the chargeable income of enterprise A in 2009 is 1.5 billion VND. The loss that arose in 2008 shall be deducted from the chargeable income according to the calculation of the inspecting agency (the offset loss is 1.5 billion VND). Depending on the faults, the competent agency shall impose fines for violations of law provisions on tax as prescribed.

IX– Enterprise income tax rates

From the tax period 2009, the common enterprise income tax is 25%. In additions, there are other tax rates (such as preferential tax rates according the business lines or localities; preferential tax rates on socialization… and tax rates on the exploration and extraction of petroleum and other rare resources in Vietnam).

If the fiscal year of an enterprise is different from the calendar year, the tax period 2008 shall apply the enterprise income tax policy prescribed in the Circular No. 134/2007/TT-BTC; and the tax period 2009 shall apply the enterprise income tax policy in the Circular No. 130/2008/TT-BTC If the enterprise is not eligible for preferential enterprise income tax rate when applying the fiscal year different from the calendar year, it may apply the enterprise income tax rate of 25% corresponding to the arising months in 2009 when calculating enterprise income tax payable.

Example: The tax period of an enterprise begins on October 01, 2008 to September 30, 2009. The tax period of this enterprise is the tax period 2008, and then it shall apply the enterprise income tax policy prescribed in the Circular No. 134/2007/TT-THE MINISTRY OF FINANCE. If enterprise Applying the common tax rate is not eligible for preferential enterprise income tax rate the tax payable is calculated as follows:

|

Enterprise income tax payable |

= |

Taxable income in the tax period |

x 3 months x 28% + |

Taxable income in the tax period |

x 9 months x 25% |

|

12 months |

12 months |

X- Locations for paying enterprise income tax.

1. Principles:

The enterprise shall pay tax where its head office is situated. If an enterprise has factories doing dependent accounting in other central-affiliated cities and provinces than the locality where its head office is situated, the tax shall be paid where the head office and the factories are situated.

The tax payment prescribed in this Clause is not applicable to dependent cost-accounting constructions and construction items.

2. Tax calculation and procedures for declaring and paying tax.

The enterprise income tax calculated and paid in central-affiliated cities and provinces where the factory doing dependent accounting is situated equals the enterprise income tax payable in the period multiplied by (x) the ratio of the expense of the factory doing dependent accounting to the total expense of the enterprise.

The figures to calculate the ratio of the expense of the head office to the expenses of the factories doing dependent accounting are determined by the enterprise themselves, according to the enterprise income tax finalization 2008, and such ratio is constantly used from 2009 and later.

If an enterprise opens or reduces factories doing dependent accounting in other localities, it must determine the expense ratio in the first tax period in such cases. From the succeeding tax period, the expense ratio is determined as prescribed above.

Enterprise At the head office must declare and pay the enterprise income tax arises at the head office and at the factories doing dependent accounting under the form No. 07/TNDN promulgated together with the Circular No. 130/2008/TT-BTC

3. Procedures for transferring documents between the Treasuries and tax authorities.

The enterprise shall pay enterprise income tax where the head office is situated to the State Treasury at the same level with the tax authorities where it registers to declare tax, and it must pay the tax payable of the dependent factories in other localities. The tax payment receipts must be make separately for each State Treasury, enclosed with the photocopy of the declaration made under the form No. 07/TNDN promulgated together with the Circular No. 130/2008/TT-BTC.

4. Tax finalization:

An enterprise shall declare the enterprise income tax finalization where the head office is situated. The outstanding enterprise income tax payable equals the enterprise income tax payable according to the finalization minus the preliminarily paid amount where the head office is situated and where the dependent factories are situated. When finalizing the annual tax at the head office, if the enterprise income tax is larger or smaller than the preliminarily paid amount in Q4, the outstanding enterprise income tax payable or the refunded amount shall be distributed proportionally where the head office and where the dependent factories are situated.

XI– Enterprise income tax from real estate transfer.

1. Taxable income:

Incomes from real estate transfer includes the income from transferring the right to use land, right to lease, right to sublease land of a real estate company as prescribed by law provisions on land, regardless of the infrastructures and constructions attached to land.

From January 01, 2009, the enterprises from all economic sectors that earn income from transferring the right to use land, right to lease, right to sublease land; real estate companies earning income from subleasing land must pay tax on the income from real estate transfer.

2. Assessable revenue:

- Revenue from real estate transfer is determined according to the actual real estate transfer prices (including the surcharges, if any) at the time of transferring real estate.

In case the price for transferring the right to use land is lower than the land price set by the People’s Committees of central-affiliated cities and provinces, the price set by the People’s Committees of central-affiliated cities and provinces at the time of transferring real estate shall apply.

- The time for calculating assessable revenue is the time the seller hands over real estate to the buyer, whether the buyer has registered the ownership of property or the right to use land with competent State agencies.

- When the State allocates or leases land to an enterprise to execute an investment project on infrastructure or houses to transfer or lease, that collects deposits from the clients according to the progress, then the time for determining revenue for calculating preliminary enterprise income tax is the time of collecting money from the clients.

+ if an enterprise can determine the expense corresponding to the revenue from the money collected from the clients, it shall declare and pay preliminary enterprise income tax by subtracting expense from revenue.

+ if an enterprise fails to determine the expense corresponding to the revenue from the money collected from the clients, it shall declare and pay preliminary enterprise income tax at 2% of the revenue, and this revenue may not be included in the revenue for calculating enterprise income tax in the year.

For the enterprises that have collected money from their clients according to the progress of the project before 2009, but have not declared and paid enterprise income tax, the collected money must be declared in 2009 to calculate the preliminary enterprise income tax as prescribed above.

- When handing over the real estate, the enterprise must recalculate the enterprise income tax payable. If the enterprise income tax preliminarily paid is smaller than the enterprise income tax payable, it must pay the outstanding tax to the State budget If the enterprise income tax preliminarily paid is bigger than the enterprise income tax payable, it may deduct the excessive amount from the enterprise income tax payable in the succeeding period, or have the excessive amount refunded.

- When finalizing enterprise income tax for construction projects on building houses for sale before 2008, and some of which have been finished and sold together with the land tenancy, that finishes in 2009 or later, the enterprise must separate the sold and handed over houses together with the land tenancy in 2008 and earlier on which the tax is completely paid in accordance with the tax policy 2008 and earlier. Such tax is calculated and paid in accordance with the Law on Enterprise income tax No. 09/2003/QH11 and its guiding documents; the houses sold together with the land tenancy since January 01, 2009 and later shall pay enterprise income tax in accordance with the Law on Enterprise income tax No. 14/2008/QH12 and its guiding documents.

3. Declaring, paying, and finalizing tax:

- Enterprises shall submit the tax declaration and pay enterprise income tax on the income from real estate transfer to the local tax authorities where the transferred real estate is located.

The tax declaration, tax payment documents, tax payment receipts are the basis for finalizing tax where the head office is located.

- Enterprises shall declare enterprise income tax for every real estate transfer under the form No. 09/TNDN promulgated together with the Circular No. 130/2008/TT-BTC The preliminary enterprise income tax on the deposit of clients collected according to the progress shall be paid at the local tax authorities where the transferred real estate is located, and be declared in part II of the Declaration No. 09/TNDN. When handing over the real estate, the enterprise must recalculate the enterprise income tax payable on real estate transfer and declare it in Part I of the Declaration No. 09/TNDN.

- If an enterprise that regularly transfers real estate requests to pay tax on every transfer and has declares enterprise income tax similarly to an enterprise that does not regularly transfer real estate, it may not declare preliminarily enterprise income tax every quarter, and may only declare annual enterprise income tax finalization.

XII– Enterprise income tax incentives

1. Some further principles of enterprise income tax incentives:

- The period of applying preferential tax rates starts from the first year the enterprise earns revenue from activities eligible for tax incentives.

- The tax exemption and reduction period starts from the first year the enterprise earns taxable income from an investment project eligible for tax incentives; in case the enterprise does not earn taxable income in the first 3 years as from the first year of earning revenue from the investment project, the tax exemption and reduction period shall starts from the fourth year.

Example: Enterprise A is eligible for tax exemption and reduction and has the first tax period in 2009, the tax exemption and reduction period starts from the first year it earns taxable income from the investment project eligible for tax incentives.. In case it does not earn taxable income in the first 3 years as from the first year of earning revenue from the investment project, the tax exemption and reduction period shall starts from the fourth year.

+ Enterprise B is eligible for tax exemption and reduction and has the first tax period in 2007, and has earned revenue. The tax exemption and reduction period starts from the first year it earns taxable income. In case it has not earned taxable income at the end of 2009, the tax exemption and reduction period starts from 2010.

+ Enterprise C is eligible for tax exemption and reduction, has the first tax period before 2007, has earned revenue without taxable income, and the tax exemption and reduction period has not started. The tax exemption and reduction period shall start from the tax period 2009.

- In the same tax period, if an enterprise earns an income eligible for various preferential enterprise income tax rates and tax exemption and reduction periods, it may choose the most advantageous enterprise income tax incentive.

- If the enterprise does not satisfy one of the conditions for tax incentives as prescribed during the enterprise income tax incentives period, it is not eligible for incentives in that fiscal year and must pay enterprise income tax at the rate of 25%.

- In the same tax period, if an enterprise engages in both business eligible for tax incentives and business ineligible for tax incentives, it must separately record the income from the business eligible for tax incentives and the business ineligible for tax incentives in order to separately declare and pay tax.

- If the business eligible for tax incentives is at a loss and business ineligible for tax incentives (except for real estate transfer) is profitable (and vice versa), the enterprise may offset it against the taxable income from the profitable business at will. The residual income after offsetting shall apply the enterprise income tax rates at the tax rate on the profitable income.

- an enterprise eligible for enterprise income tax incentives (including preferential tax rates and tax exemption or reduction period) as prescribed in the previous legal documents on enterprise income tax or the issued Investment license or Investment incentive certificate, it is eligible for such incentives for the remaining time. In case the enterprise income tax incentives include both preferential tax rates and tax exemption or reduction period which is lower than the incentives prescribed in the Law on Enterprise income tax No. 14/2008/QH12 and its guiding documents, the Law on Enterprise income tax No. 14/2008/QH12 and its guiding documents shall apply to the remaining time starting from the tax period 2009.

- During the tax exemption or reduction period, if competent agencies find that the enterprise income tax of the tax exemption or reduction period increases, the enterprise is eligible for tax exemption or reduction as prescribed. Depending on the faults, the competent agency shall impose penalties for violations of law provisions on tax as prescribed.

- The enterprise income tax incentives are not applicable to:

+ Other incomes.

+ Incomes from the exploration and extraction of petroleum and other rare resources.

+ Incomes from the business of prizing games and gambling as prescribed by law.

+ Other cases as prescribed by the Government.

2. Some further notices:

2.1. For enterprises that are no longer eligible for enterprise income tax incentives for satisfying the conditions for using domestic materials, for the export proportion of textiles and garments according to WTO’s Accession commitment, the Ministry of Finance issued the Official Dispatch No. 2348/BTC-TCT dated March 03, 2009. In particular:

For enterprises engaged in the textiles and garments industry, enterprises eligible for incentives for using domestic materials, if other conditions for enterprise income tax incentives are satisfied (apart from the incentives for satisfying the conditions for export proportion, using domestic materials) such as producing in industrial zones, producing in export processing zones. If the conditions for export proportion are not satisfied, the conditions similar to that of industrial zones shall apply (according to Clause 2 Article 2 of the Government's Decree No. 29/2008/NĐ-CP dated March 14, 2008); enterprises operating in impoverished localities in the list of prioritized localities, labor-intensive enterprises… shall continue to enjoy enterprise income tax incentives corresponding to the conditions that they have satisfied for the remaining time. Enterprises may choose one of the two options:

Option 1: continue to enjoy enterprise income tax incentives corresponding to the conditions that they satisfy for the remaining time (except for the incentives for satisfying the conditions for export proportion and using domestic materials) according to the previous legal documents on enterprise income tax at the issuance date of the establishment license.

Option 1: continue to enjoy enterprise income tax incentives corresponding to the conditions that they satisfy for the remaining time (except for the incentives for satisfying the conditions for export proportion and using domestic materials) according to the previous legal documents on enterprise income tax at the adjustment time in accordance with the WTO commitment (January 11, 2007).

For enterprises engaged in the textiles and garments industry, enterprises eligible for incentives for using domestic materials, if other conditions for enterprise income tax incentives are satisfied (apart from the incentives for satisfying the conditions for export proportion, using domestic materials) they may choose one of the 2 options above to enjoy enterprise income tax incentives for the remaining incentive period as prescribed in the previous legal documents on enterprise income tax at the time of issuing the establishment license or at the time of adjustment in accordance with the WTO commitment (January 11, 2007).

Example 1: An export processing enterprise producing garments for export that have projects in industrial zones. The enterprise is established in 1997 and eligible for enterprise income tax rates of 10% during the entire project according to the investment license; exempted from tax for 4 years as from earning taxable income and, and eligible for 50% reduction in tax for the next 4 years. The enterprise has earned taxable income from 1997.

- According to the investment license, it is exempted from tax for 4 years (1997 – 2000), and eligible for tax reduction by 30% for the next 4 years (2001 – 2004), and eligible for the tax rate of 10% from 1997 until the end of the project.

- According to the Government's Decree No. 152/2004/NĐ-CP dated August 06, 2004, the export processing enterprises engaged in production are eligible for 4 years of tax exemption (1997 – 2000) and 7 years of tax reduction by 50% (2001 – 2007), and applying the tax rate of 10%

- According to the Government's Decree No. 24/2007/NĐ-CP and the Circular No. 134/2007/TT-BTC from 2007, the enterprise is not eligible for the preferential enterprise income tax rate of 10% according to the conditions for export and tax reduction 2007. However, it satisfies the conditions for factories in industrial zones.

Option 1: if the enterprise wishes to enjoy incentives for the remaining time according to the provisions on enterprise income tax at the time of issuing the establishment license (the legal document at the time of issuing the license in 1997 is the Decree No. 36/CP dated April 24, 1997), then the enterprise being a factory in the industrial zone is eligible for the preferential enterprise income tax rates of 15% for the entire project; eligible for enterprise income tax exemption for 2 years as from earning taxable income, and not eligible for tax reduction. On January 11, 2007 (the WTO commitment date), the company has enjoyed tax exemption for 4 years and tax reduction for 6 years. When choosing option 1, it may enjoy the tax rate of 15% for the remaining time from 2007 until the end of the project.

Option 2: if the enterprise wishes to enjoy incentives according to the provisions on enterprise income tax at the date of WTO commitment (January 11, 2007) for the remaining time (the legal document at the time of issuing the license in 1997 is the Decree No. 24/2007/NĐ-CP), then the enterprise being a factory in the industrial zone is eligible for the preferential enterprise income tax rates of 15% for 12 years as from the commencement of the business; eligible for tax exemption for 3 years as from earning taxable income, and eligible for tax reduction by 50% of the tax payable for the next 7 years. On January 11, 2007, the company has enjoyed tax exemption for 4 years and 50% reduction in tax for the next 6 years (1997 – 2006), the company is not eligible for tax reduction for the remaining time, and may apply the enterprise income tax rate of 15% for 12 years (1997 - 2008). When choosing option 2, the company may apply the tax rate of 15% for the remaining time being 2007 and 2008. From 2009, the tax rate of 25% shall apply.

Example 2: The company B in a 100%-capitalized industrial zone produces garments for export. Its business commences in 2003. The company is eligible for preferential enterprise income tax rate of 10% during the entire project; exempted from tax for 4 years as from earning profits, and eligible for 50% reduction in tax for the next 4 years. The company earns income for the first time in 2005.

- According to the investment license, it is exempted from tax for 4 years (2005 – 2008), and eligible for tax reduction by 30% for the next 4 years (2009 – 2012), and eligible for the tax rate of 10% from 2003 until the end of the project.

- According to the Government's Decree No. 24/2007/NĐ-CP and the Circular No. 134/2007/TT-BTC the company is not eligible for the enterprise income tax rate of 10% and not eligible for tax reduction according to the export conditions. However, it satisfies the conditions for factories in industrial zones.

In this case, company B may choose one of the two options guided in the Official Dispatch No. 2348/BTC-TCT as follows:

Option 1: if the enterprise wishes to enjoy incentives for the remaining time according to the provisions on enterprise income tax at the time of issuing the establishment license (the legal document at the time of issuing the license in 2003 is the Decree No. 27/2003/NĐ-CP), then the enterprise being a factory in the industrial zone is eligible for the preferential enterprise income tax rates of 15% for the entire project; eligible for enterprise income tax exemption for 2 years as from earning taxable income, and not eligible for tax reduction. When choosing option 1, it is eligible for tax exemption for 2 years (2005 and 2006), eligible for tax rate of 15% for the remaining time from 2007 until the end of the project.

Option 2: if the enterprise wishes to enjoy incentives according to the provisions on enterprise income tax at the date of WTO commitment (January 11, 2007) for the remaining time (the legal document at the time of issuing the license in 1997 is the Decree No. 24/2007/NĐ-CP) then the enterprise being a factory in the industrial zone is eligible for the preferential enterprise income tax rates of 15% for 12 years as from the commencement of the business; eligible for tax exemption for 3 years as from earning taxable income, and eligible for tax reduction by 50% of the tax payable for the next 7 years. When choosing option 2, the company earning taxable income from 2005 until January 11, 2007 shall be eligible for tax exemption for one more year (200&), eligible for tax reduction by 50% in the next 7 years (2008 – 2014), eligible for the tax rate of 15% for 12 years (2002 – 2013). Thus until 2007, the company may apply the tax rate to the remaining time being 7 years (2007 – 2013). From 2014, the tax rate of 25% shall apply.

Example 3: A garment enterprise established in 2000 has the export proportion > 80% of its products. Thus it is and eligible for the enterprise income tax rate of 10% during the entire project; exempted from tax for 4 years as from earning taxable income and, and eligible for 50% reduction in tax for the next 4 years.

According to the Government's Decree No. 24/2007/NĐ-CP and the Circular No. 134/2007/TT-BTC the company is not eligible for the enterprise income tax rate of 10% and not eligible for tax reduction according to the export conditions. However, it satisfies the conditions for factories in industrial zones.

In the example above, at the end of the incentives according to the WTO commitment, after 4 years of tax exemption period, if that enterprise chooses option 2 (tax exemption for 3 years and tax reduction by 50% for the next 7 years; applying the tax rate of 15% for 12 years as from commencing the business), the enterprise is not eligible for tax exemption or reduction according to the Decree No. 24/2007/NĐ-CP and may only chose to enjoy the tax rate of 15% in 12 years as from commencing the business for the remaining time.

2.2. Enterprises are eligible for enterprise income tax incentives when satisfying the conditions for export proportion until the end of 2011 (except for textiles and garments).

From 2012, if enterprises enjoying enterprise income tax incentives for satisfying the conditions for export proportions satisfy the conditions for other enterprise income tax incentives (apart from the conditions for export proportion), they may choose and notify the enterprise income tax incentives for the remaining time to the tax authorities, depending on the fulfillment of conditions for investment incentives as prescribed in legal documents on enterprise income tax at the time of issuing the establishment license or at the date of WTO commitment (the end of 2011).

2.3. Clause 4 Article 2 of the Regulation on industrial zones, export processing zones, and Hi-tech zones promulgated together with the Government's Decree No. 36/CP dated April 24, 1997 prescribes: “Export processing enterprises are enterprises that produce goods for export, providing services for producing goods for export and the export activities, established and operated in accordance with this Regulation”.

- Clause 6 Article 2 of the Government's Decree No. 29/2008/NĐ-CP dated March 14, 2008, on industrial zones, export processing zones, and economic zones prescribes: “Export processing enterprises are enterprises established and operated in export processing zones, or enterprises that export all of their products in industrial zones or economic zones:.

The export processing enterprises are eligible for enterprise income tax incentives because of satisfying the export conditions. Thus the export processing enterprises shall have their enterprise income tax incentives adjusted according to the Decree No. 24/2007/NĐ-CP the Decree No. 124/2008/NĐ-CP; the Circular no. 134/2007/TT-BTC; the Circular No. 130/2008/TT-BTC and the Official Dispatch No. 2348/BTC-TCT If an export processing enterprise satisfies other conditions for incentives rather than the conditions for export proportion, it may choose to enjoy incentives as guided in the Official Dispatch No. 2348/BTC-TCT.

2.4. For the business related to the infrastructural development of industrial zones, export processing zones, and Hi-tech zones, the Ministry of Finance issued the Official Dispatch No. 4125/BTC-TCT and the Official Dispatch No. 13480/BTC-TCT dated September 23, 2009. In particular:

- If an enterprise engaged in the development of industrial zones receives land allocated or leased by the State to build infrastructures but does not build infrastructures for lease in accordance with the issued investment license or certificate of business registration, and transfer the right to use or to rent land to other enterprises, and such enterprises invest in building infrastructures for lease. The enterprise income tax on the transfer of the right to use or to rent land is not eligible for enterprise income tax incentives.

- Enterprises established before January 01, 2009 have investment projects on the infrastructural development of industrial zones, export processing zones, Hi-tech zones. The State allocates or leases land to such project before January 01, 2009 for the purpose of building infrastructures. After investing in the infrastructural development, the enterprises lease such land to other enterprises in the export processing zone, industrial zone, or Hi-tech zone. The income from that lease is an income from the business of infrastructural development, and is eligible for tax incentives as prescribed.

In 2009, the investment projects enjoying enterprise income tax incentives shall continue to enjoy enterprise income tax incentives for the remaining time based on the conditions that they satisfy.

- Enterprises established before January 01, 2009 having investment projects on the infrastructural development of industrial zones, export processing zones, Hi-tech zones that the State allocates or leases land to such project from January 01, and enterprises engaged in business of infrastructural development established from January 01, 2009 are not eligible for enterprise income tax incentives for the business of infrastructural development.

2.5. For mineral extraction: the Ministry of Finance issued the Official Dispatch No. 10254/BTC-TCT dated July 20, 2009. In particular: The enterprise income tax incentives are not applicable to incomes from the mineral extraction of enterprises that are established and issued with the investment licenses for mineral extraction from January 01, 2009. The enterprises engaged in mineral extraction that commence their business before January 01, 2009 and enjoy enterprise income tax incentives as prescribed by the Law on Enterprise income tax No. 09/2003/QH11, the Law on Petroleum, and legal documents promulgated by the Government before January 01, 2009, shall continue to enjoy the incentives as prescribed by the Law on Enterprise income tax No. 09/2003/QH11, the Law on Petroleum, and the legal documents promulgated by the Government for the remaining time. In the same tax period, if an enterprise engages in both business eligible for tax incentives and business ineligible for tax incentives, it must separately record the income from the business eligible for tax incentives and the business ineligible for tax incentives in order to separately declare and pay tax.

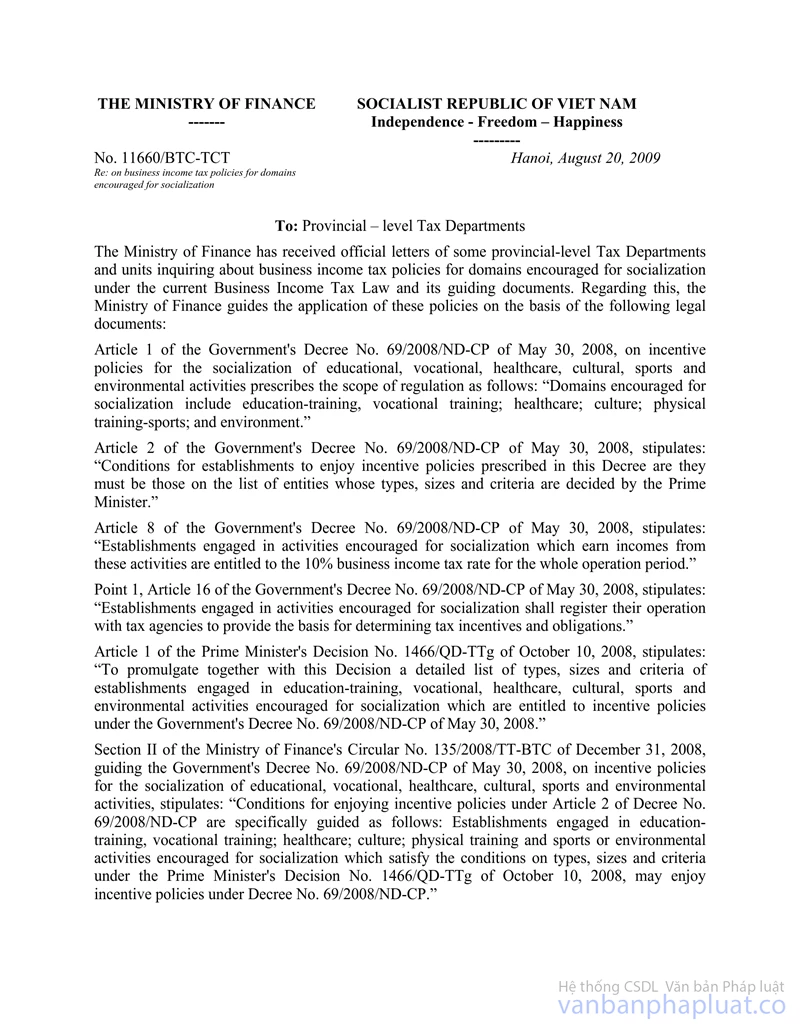

2.6. For socialization, the Ministry of Finance issued the Official Dispatch No. 11660/BTC-TCT dated August 20, 2009. In particular:

- The socialization establishments being subjects of regulation of the Government's Decree No. 69/2008/NĐ-CP dated May 30, 2008 (not being subjects of regulation of the Government's Decree No. 124/2008/NĐ-CP dated December 12, 2008) that earn income from the socialization activities that satisfy the criteria and standards promulgated together with the Prime Minister’s Decision No. 1466/QĐ-TTg dated October 10, 2008, and have registered with the tax authorities, the enterprise income tax rate of 10% applies when the Decree No. 69/2008/NĐ-CP dated May 30, 2008 takes effect.

- In case the subjects of regulation of the Government's Decree No. 124/2008/NĐ-CP dated December 12, 2008 are also subjects of regulation of the Government's Decree No. 69/2008/NĐ-CP dated May 30, 2008 and earn income from the socialization activities that satisfy the criteria and standards promulgated together with the Prime Minister’s Decision No. 1466/QĐ-TTg dated October 10, 2008, and have registered with the tax authorities, the enterprise income tax rate of 10% applies when the Decree No. 69/2008/NĐ-CP dated May 30, 2008 takes effect.

- In case the subjects of regulation of the Government's Decree No. 124/2008/NĐ-CP dated December 12, 2008 are not subjects of regulation of the Government's Decree No. 69/2008/NĐ-CP dated May 30, 2008:

+ For the enterprise that engage in other business but earn income from socialization, or business establishments that do not establish establishment doing independent accounting that earn income from socialization, if the conditions in the List of forms, scale criteria, and standards of socialization promulgated together with the Prime Minister’s Decision No. 1466/QĐ-TTg dated October 10, 2008 are satisfied, the enterprise income tax rate of 10% shall apply to the income from the activities of education, vocational training, health, culture, sports, and environment during the entire period of operation as from January 01, 2009.

+ For enterprises that have engaged in socialization before January 01, 2009 and apply the tax rate over 10%, if the conditions in the List of forms, scale criteria, and standards of socialization promulgated together with the Prime Minister’s Decision No. 1466/QĐ-TTg dated October 10, 2008 are satisfied, such enterprises may apply the tax rate of 10% on the income from socialization as from January 01, 2009.

Further notices when finalizing enterprise income tax:

- The assessable revenue from the sale of tickets and memberships of golf clubs must comply with the Circular No. 06/2010/TT-BTC dated January 13, 2010 of the Ministry of Finance.

- The application of the coefficient of land tenancy distribution to the apartments in an apartment building for calculating enterprise income tax must comply with the Official Dispatch No. 18044/BTC-TCT dated December 23, 2009 of the Ministry of Finance.

- The distribution of expenses on gas bottles must comply with the Official Dispatch No. 1484/BTC-TCT dated February 10, 2009 and the Official Dispatch No. 7776/BTC-TCT dated June 02, 2009 of the Ministry of Finance.

- The period of enterprise income tax incentives applicable to deposit and loan must comply with the Official Dispatch No. 118/BTC-TCT dated January 05, 2010 of the Ministry of Finance.

PART 2: THE POLICIES OF ENTERPRISE INCOME TAX RELATED TO THE SOLUTIONS OF THE GOVERNMENT FOR ENCOURAGING INVESTMENT AND CONSUMPTION; PREVENTING ECONOMIC DECLINE, AND RESOLVING DIFFICULTIES FOR ENTERPRISES

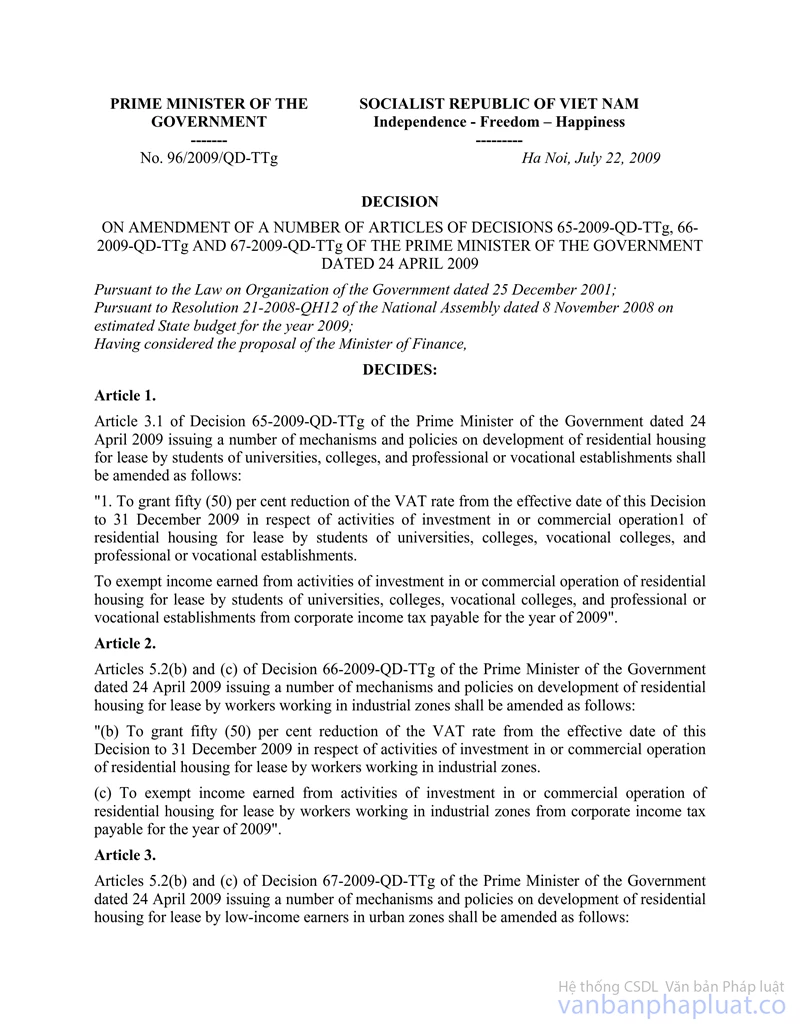

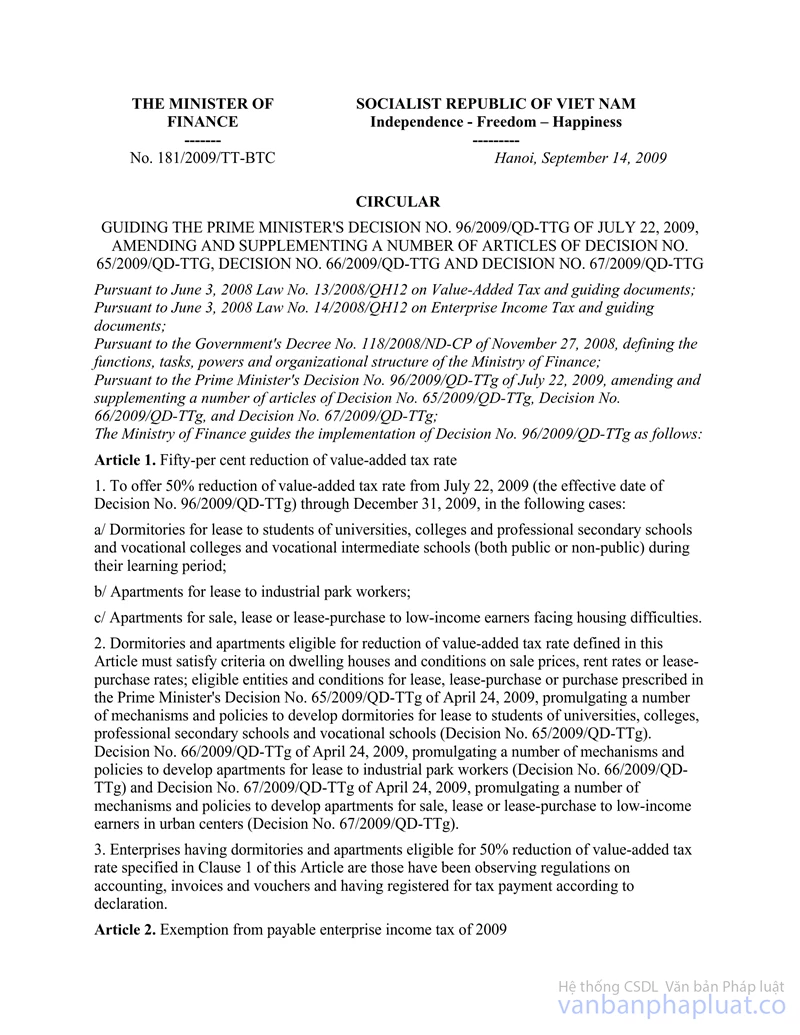

Pursuant to the Resolution No. 30/2008/NQ-CP dated December 11, 2008; the Decision No. 16/2009/QĐ-TTg dated January 21, 2009; the Decision No. 96/2009/QĐ-TTg dated July 22, 2009 of the Prime Minister, the Ministry of Finance promulgated the Circular No. 03/2009/TT-BTC dated January 13, 2009, the Circular No. 12/2009/TT-BTC dated January 22, 2009, the Circular No. 181/2009/TT-BTC dated September 14, 2009, and the Official Dispatch No. 1326/BTC-CST dated February 04, 2009, the Official Dispatch No. 10588/BTC-TCT dated July 24, 2009, the Official Dispatch No. 17665/BTC-TCT dated December 16, 200 , guiding the Resolutions and Decisions above. When finalizing enterprise income tax related to the cases eligible for tax exemption, tax reduction, or tax deferral according to the demand stimulation policy, it is required to consider the provisions and guidance in the documents above, in particular:

1. Scope and subjects:

1.1. Tax exemption or reduction:

- Medium and small enterprises are eligible for 30% reduction in enterprise income tax payable of Q4/2008 and enterprise income tax payable of 2009, including:

+ The cooperatives, people’s credit funds; units affiliated to enterprises and doing independent accounting ; member units doing independent accounting with legal status of economic corporations and general companies that satisfy the conditions in the Circular No. 03/2009/TT-BTC

The criteria in the Circular No. 03/2009/TT-BTC applicable to units affiliated to enterprises, doing dependent accounting, declaring and paying enterprise income tax at the head office such as factories, workshops, stores, or offices… (if any).

+ Non-business units

+ Local development investment funds: local development investment funds are organized and operated as prescribed in the Government's Decree No. 138/2007/NĐ-CP dated August 28, 2007, on the organization and operation of local development investment funds being subjects of regulation of the Law on credit institutions dated February 12, 1997, and the Law on amending and supplementing a number of articles of the Law on credit institutions dated My 16, 2004.

Medium and small enterprises are enterprises that satisfy one of the following criteria:

“- The charter capital stated in the Certificate of business registration or the Investment certificate that takes effect before January 01, 2009 does not exceed 10 billion VND; for the enterprises established from January 01, 2009 and later, the charter capital stated in the Certificate of business registration or the First investment certificate does not exceed 10 billion VND.

- The average number of employees in Q4/2008 does not exceed 300 people, including employees that sign short-term contracts under 3 months; for enterprises established on October 01, 2008 and later, the number of employees being paid in the first month (full 30 days) of earning revenue does not exceed 300 people.

- The enterprise income tax payable in 2009 on the following incomes is exempted:

+ Income from the rent of dwellings to students of universities, colleges, vocational high schools, vocational colleges, and vocational intermediate schools during their study;

+ Income from the rent of dwellings to workers in industrial zones;

+ Income from the renting or selling houses to low-income people that face difficulties of accommodation.

1.2. Tax deferral:

The enterprise income tax eligible for tax deferral is determined as follows:

- For medium and small enterprises, it is the reduced preliminary enterprise income tax every quarter in 2009 as guided in Section II of the Circular No. 03/2009/TT-BTC.

- For enterprises producing or processing agricultural, silvicultural and aquatic products, textiles and garments, leather and footwear, and electronic components, it is the preliminary enterprise income tax every quarter in 2009 on such activities.

If the enterprise fails to separate the preliminary enterprise income tax on the production and processing of agricultural, silvicultural and aquatic products, textiles and garments, leather and footwear, and electronic components from the preliminary enterprise income tax on other activities, the preliminary enterprise income tax on the former activities shall be deferred according to the proportion (%) of the revenue from the former activities to the total revenue of the enterprise in 2008.

- The enterprise income tax payable in 2009 on the following business (excluding medium and small enterprises as prescribed in the Circular No. 03/2009/TT-BTC dated January 13, 2009 of the Ministry of Finance):

+ Production of mechanical products being means of production;

+ Production of building materials: bricks, tiles, lime, paint;

+ Construction and installation;

+ Travel services;

+ Food trade;

+ Fertilizer trade;

Example: The charter capital stated in the Certificate of business registration issued on July 01, 2007 of the construction company ABC is 09 billion VND (the charter capital in the Certificate of business registration is not adjusted during the operation). The business line is building and installing civil and industrial constructions.

The charter capital stated in the Certificate of business registration issued on July 01, 2007 of the construction company ABC being 09 billion VND satisfy the condition of medium and small enterprises, thus it is eligible for the incentives being enterprise income tax reduction and deferral as prescribed in the Circular No. 03/2009/TT-BTC dated January 13, 2009 of the Ministry of Finance, and is not eligible for tax deferral as guided in the Circular No. 12/2009/TT-BTC dated January 22, 2009 of the Ministry of Finance.

2. Calculating the reduced or deferred tax:

2.1. Calculating the reduced or deferred enterprise income tax:

- Medium and small enterprises are eligible for 30% reduction in enterprise income tax payable of Q4/2008 and the enterprise income tax payable of 2009. In particular:

a) The reduced enterprise income tax of Q4/2008 equal 30% of the enterprise income tax payable of Q4/2008. The enterprise income tax payable in Q4/2008 is calculated as follows:

- If the revenue, expenses and taxable income of Q4/2008 are calculable, the enterprise income tax payable of Q4/2008 is calculated according to the recorded taxable income of Q4/2008.

- If the revenue, expenses and taxable income of Q4/2008 are not calculable, the enterprise income tax payable of Q4/2008 is calculated as follows:

|

Enterprise income tax payable of Q4/2008 |

= |

Enterprise income tax payable in 2008 |

|

4 |

b) The reduced enterprise income tax of Q4/2008 equal 30% of the enterprise income tax payable of the year.

- The enterprise income tax payable in 2009 on the income from renting dwellings to students of universities, colleges, vocational high schools, vocational colleges, and vocational intermediate schools during their study, income from renting dwellings to workers in industrial zones; income from renting and selling houses to low-income people that face difficulties in accommodation, is calculated according to the income statement of the enterprise, if the enterprise can separate the income from tax-free business. If the enterprise cannot separate the enterprise income tax payable on the tax-free business, the exempted enterprise income tax is calculated according to the proportion of the revenue from the tax-free business to the total revenue of the enterprise in 2009.

2.2. Calculating the enterprise income tax eligible for tax deferral:

The enterprise income tax eligible for tax deferral is determined as follows:

- For medium and small enterprises, it is the preliminary enterprise income tax every quarter in 2009 that has been reduced by 30% as guided above.

- For enterprises producing or processing agricultural, silvicultural and aquatic products, textiles and garments, leather and footwear, and electronic components, it is the preliminary enterprise income tax every quarter in 2009 on such activities.